The following is a guest post submitted by community regular JayCeezy, sharing a few ideas he has picked up along the PF road we all travel. GYFG welcomes guest contributions, please click here for more info.

A financial mentor of mine told me something that stayed with me: “A million dollars isn’t $h1t. Unless you don’t have it.” But once you have it, what are you going to do with it? Why? I’m not an expert, but I am experienced, and want to share these ideas, passing along useful tactics and strategies my PF mentors generously shared with me. Maybe you will find some of this worth passing along, someday.

You might not need a million if everything goes your way, but if you don’t have a pension, inheritance, personal-injury settlement, or other windfall, it is a reasonable baseline that will keep you from having to return to work or take in a roommate. Some of these things worked for me, and some of them are things I wish I knew and applied. Consider this slapped-together compendium my Personal Finance equivalent of “Meditations” by Marcus Aurelius, Thomas Edison’s “Innovation” notebook, or “Jackass 3D”.

Personal finance consists of two things at the core: save more, spend less. Everything else follows. We read PF blogs mainly because we are all looking for that “magic bullet” that will be the secret to wealth, and the freedom that wealth can provide. GYFG has the $10 million dollar goal covered, and it is a worthy one. This is for people who want out of the rat-race, don’t care about impressing anybody, and have a $1 million dollar goal, to start.

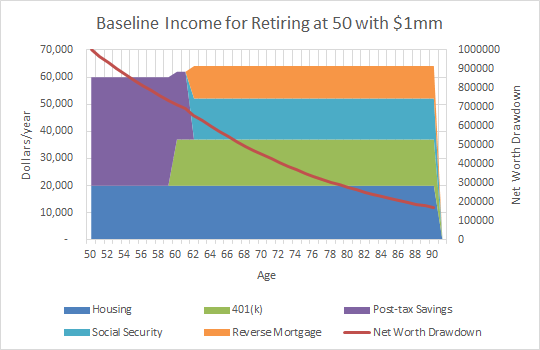

The figure below (and to the right) shows a conservative baseline for cash flow thrown off by a $1 million critical-mass. It is calculated with a starting salary of $40,000/year with 4% annual raises, a 20% savings rate at 3.5% growth, working 26 years. You can acquire $1 million by age 50 using the above assumptions, so you don’t have to make a lot of money, take big risks, or hit investment home-runs.

This example shows imputed rent of about $20,000 for the reverse-mortgage; you don’t pay taxes on the payout, either. The dollars are current-year. This is the base case for a secure retirement, achieved with minimal risk. If you want more, then earn more, save more, risk more, or work longer. But this should be within most reader’s ability to accomplish, and my belief is that everyone still reading will do so, easily.

Many of you will hit this milestone much earlier, and my thought is that additional savings and investment can be utilized with increasing risk-levels, since you have your baseline handled.

These next thoughts are intended to provide contrarian choices as you pursue financial independence. These don’t apply to everybody, or in all cases. But they worked for me, or would have if I knew then what I know now. If you find these useful, you may really get a lot out of “More Wealth Without Risk” by Charles J. Givens

• Split after-tax savings and pre-tax savings 50/50. If you are fortunate enough to participate in a 401(k) with a match, save up to the match amount first. You will use the after-tax savings for a down-payment on a home or a car purchase, and unexpected life-events before age 59.5.

• Don’t buy a house as an investment, tax-write off, or if you are single. The costs of ownership are too great, until you are part of a dual-income household or earning above $100,000. Owning a home locks you into a geographic region, subject to market conditions beyond your control, and will be the controlling factor of many upcoming life decisions. Don’t let investments control you, make sure you are controlling investments.

• Pay cash for cars. If you can’t pay cash, don’t buy it. If you really want it, save for it. Cars, watches, conspicuous consumption are fine, if impressing strangers is a priority.

• Reverse-mortgage – you have to be 62. You can get a loan for 2/3 of the value of the home, and stay in it as long as you can. If you move, you have to pay off the loan; this is a great deal if you do it early and live a long time. Otherwise, a bad deal. More at this link.

• Life insurance – Don’t buy it. It’s not an investment. A single person doesn’t need it. A young couple doesn’t need it. A middle-aged couple doesn’t need it. An old couple doesn’t need it. I have seen contemporaries insure their toddlers. Why? It is a perverse-incentive. It only pays off if there is a tragic event, and the return is greater the sooner tragedy strikes. In the meantime, it bites into cash flow which could be used for additional savings or debt-elimination. One exception: buy life insurance to provide for a loved one who can’t provide for themselves.

• Insurance – don’t get comp for autos; if you have an accident and it’s your fault, pay to fix it (or don’t). As a young man in the high-risk category, I had several years where an insurance salesman convinced me to comp/coll, and I wound up paying more per year than the car was worth! Once your NW gets above $200,000 or you are a homeowner, buy an ‘umbrella policy’; it is just a few hundred per year, and will keep a lien or garnishment of future earnings from crushing your finances in the event of a lawsuit. Long-term nursing care – Self-insure, and save the cash flow.

• Children – speaks for itself. If you have children, Early Retirement is no longer a top priority.

• Don’t buy or sell anything primarily for tax reasons. Transaction costs and maintenance for real estate will be 1.33 times your original estimate.

• When calculating Net Worth, it is fine to include IRA/401(k)/403(b)/457 balances. Just don’t pretend to be surprised when you pay taxes on the back end, and if your NW is $100,000 in an IRA then acknowledge that it isn’t really $100,000.

• Social Security – My wife and I plan to take benefits as early as possible for two reasons. 1) 85% of the S.S. benefit is taxable beyond $24K/yr in earned income (this includes IRA, 401(k), 457(b), etc. withdrawals). 2) the ‘break-even’ for taking early benefits (62 at 70%) to our regular payout (67 at 100%) is age 78. Not only is the risk for an early demise removed for 15 years (not once, but twice for each of us), but we feel the utility value of a few hundred dollars a month in extra benefits after age 78 is lower than in earlier years. More info on the taxation of SS benefits here.

• Your personal Social Security payout(s) can be determined here and you can perform different scenarios in which you work different durations or earn varying amounts. Talk about “means testing” has been around since the 1980s, and the problem is that it provides a disincentive to save (in direct conflict with the 401(k) rule, IRAs, lower Capital Gains rates for investments, etc.) I think it is OK to plan for receiving it, and respect your opinion if you choose not to.

• Taxes and IRA Rollover withdrawals – We have determined the tax implications, and find the potential for compounding is outweighed by the benefit of minimizing taxation. Our plan is to begin early withdrawals using the 72(t) Rule, realizing smaller amounts over more years. This will significantly reduce our tax bill, as well as keep our S.S. payments from being taxed at greater amounts. The traditional advice is for leaving tax-protected income as long as possible to allow maximum compounding; withdrawing tax-protected income with 72(t) in the 10 years before SS eligibility will allow us to be taxed at the lowest brackets over a longer period of time. You can find more info and run test scenarios here.

• Two can live at 1.3 times the cost of one. The first child will add 30% to the cost of one. Each additional child, reduce by 5% (i.e. 25% for second, 20% for third). A household of five will cost twice what a household of one costs. You can eyeball this, and see that the fastest way to save more, spend less is to be part of a double-income, no kids, household.

• When selling a residence, count on receiving 93% of the sales price.

• When buying a residence, count on paying 104% of the sales price. If you pay cash, 101%.

• A ‘quick-and-dirty’ retirement calculator I like for running various scenarios is free at Vanguard, found here.

These last two thoughts are indirectly related to personal finance, in that the quality of one’s time and lifestyle are really the main reason to save more, spend less. Attention to these things can make one’s life much better, while inattention can be very expensive financially and otherwise.

Personal Improvement

It isn’t too late to change, at any age. Just try. If you are chronically late, you are burdening others with your selfishness and disrespecting their time. If you ask for favors or a recommendation and don’t follow through, you are not flattering the person; you are insulting them [GYFG Here – I was compelled to add a comment on this. I call these people “Ask Holes”, don’t be one!]. You already know your shortcomings; they don’t have to be lifelong flaws, unless you choose them to be. Some people are born knowing all they think they need to know, but 20 minutes a day of reading can bring life-changing knowledge.

Guard your time

You can spend endless hours calculating and tracking personal finance. Endless hours on retirement calculators. Endless hours on LinkedIn building up a network of people you never met, live on another continent, you used to know decades ago, etc. and in the end the only people benefitting from your network will be the HR links. What is your time worth? Not all analysis is useful, so find the analysis that will help you save more, spend less and leave the rest.

Learn these phrases to deal with people that don’t respect your time: “We’ve had this conversation before, is there something new I need to know?” “What is your bottom line?” “Why are you telling me this?” “I just have a few minutes, what can I do for you?” “I prefer not to discuss things like that.”

Hopefully some of this will be useful to you on your journey as a Financial Freedom Fighter. I really enjoy the PF community, and supportive positive attitudes of those who share this interest. Continued success to everyone, thanks to GYFG for providing this opportunity to share, and thank you for reading!

-JayCeezy

17 Responses

Re: Life insurance. I think you might want to distinguish between Whole Life Insurance, which is indeed a waste, and Term Life Insurance, which is significantly cheaper and meant for dependents.

I think you just did!

Hubbard – Have you done much research on Whole Life Insurance that is set up in a way to minimize the death benefit and maximize the Cash Value?

I am actually still in evaluation mode, but there are certain aspects of this sort of policy that I really like, given several needs I am trying to fill.

I realize that these policy’s are front loaded with fees, but if set up correctly, they still seem interesting. By using PUA (paid up additions) an minimizing the death benefit, you can slash typical commissions by 70% and get 90% + of your first years premium immediately as cash value.

The policy that I have been designing with an agent over the past few months hits a break even point in 5 years…and has a contractual compound return of about 4.0% over 20 years and 4.5% over 30 years. And that is based on historically low interest rates and their current dividend rate.

Well that sentence is a little misleading. The contractual return is based on current market interest rates and range in the 2-4% range. Then you get a dividend on top of this…that isn’t guaranteed, but the companies that do these policy’s have not missed a dividend in over 100 years (even through the different financial crisis that have hit).

Now obviously if your not in this for the long term, these kinds of policy’s are a horrible idea.

But there are a lot of benefits/utility to the policy:

1 – You get instant access to the cash value of the policy, no questions asked, up to 95% of your cash value. The best part is that it comes with uninterrupted compounding. Meaning the insurance company loans you the money while your money continues to grow. You get to become your own bank.

2 – Based on #1 you get dual compounding. Meaning you can put your money to work in two places at once. Obviously you would want to do this only if you could achieve a return higher than the rate the insurance company is charging you.

3 – Your principal is guaranteed to never go down in value. It doesn’t matter what the market is doing. In fact you get your contractual return every year as well.

4 – You do get the added benefit of a death benefit in the event something happens to the insured. But that is just a side benefit and not the purpose of the policy. The policy is really designed more for the living benefit than it is for the death benefit.

5 – You can access the cash value including the gains tax free.

6 – In most states people can’t come after your life insurance policy in the event they try to sue you.

The policy that I am currently designing hits break even at year 5…meaning that my cash value will be exactly equal to the amount of premium that I put into the policy. Traditional Whole Life Insurance policy’s take 10-15 years to hit this point. I have heard of some, if set up correctly, reaching break even in 4 years…that is what I am shooting for in designing the policy with my agent.

I have been in due diligence mode for over a year now and will likely pull the trigger in January of 2016.

I don’t have the time to go into the different needs I have that I think this sort of policy will fill…but I will just leave you with the opinion that although not for everyone…this sort of policy may be viable for the right person with the right needs.

It’s hard to ever put a blanket statement on anything.

Interested to hear your thoughts on the matter if you care to share.

Cheers,

Dom

GYFG, sounds like your reasons for considering Whole Life are personal, and they should stay that way. My thought stands, as noted above, on the subject. My bottom-line on the subject is this: you probably know the person selling it to you (it is always ‘sold’, never ‘bought’). Maybe a friend from school or relative. So…if you would buy the ‘product’ (not an ‘investment’) from a total stranger, then proceed. If you are reluctant to back out or decline after discussing this for a few months hammering out details, then your concern is the ‘relationship’ and not the product. If the salesperson were to switch jobs or companies, would you then look at what they sold you differently? I’m sure you are doing due diligence, and your decision will be the right one.

Agree JayCeezy, every decision should be based on one’s own goals and needs.

I actually do not know the person that I will be selling me the policy and in fact I have talked to three different agents from three different companies over the last 12 months. The education process with the agent I am currently working with impressed me and also happened to coincide with the timing of when I was actually ready to execute. The company I am working with now has spent months with me going over the policy through a very comprehensive education process. It is a very low pressure process, and at the end of the day, he only wants me to get the policy it it fits my needs and goals. Of course he wants to get a commission for all the hard work he has put in…but he in particular puts the clients needs first (that’s my opinion).

In this time I have also read several books on the subject and have been crunching numbers like crazy.

I eventually plan to do a post (probably more like a series of posts, because there is a lot more too it than meets the eye).

At the end of the day it is a financial product that comes with a cost. The question is whether the cost is worth the features and benefits…and like you said that is a very personal answer.

Cheers.

Glad to see you have put so much analysis and research in doing your due diligence. Looking forward to your post on the subject!

I have to disagree with your statement: “If you have children, Early Retirement is no longer a top priority.” Children is precisely the WHY behind our journey to early retirement. We have three of them and make less than $100,000/year, but our path is still very doable. If we wanted to save $1 million, it would take us 8 years to do so. But I want to give my kids all the experiences I can before they leave here. And financial independence will allow us to do that.

Maggie – The best thing about personal finance is that you get to cherry pick the stuff that resonates with you and throw out the rest. I love dissenting views, as that is what makes for good conversation. Forces people to think. As you know, there are a million and one ways to reach financial freedom.

Question: You mention that saving $1M would take you 8 years, yet you also mentioned that your household brings in less than $100K. Are you saying that it will take you another 8 years to get to $1M based on where you are now?

BTW, kudos to you for wanting to give the kids the ultimate gift, time with their parents. That is one thing I never really had growing up, but definitely plan to give to my kids…when we eventually start a family.

Cheers!

Looks like I hit a nerve! No offense intended. “These next thoughts are intended to provide contrarian choices as you pursue financial independence. These don’t apply to everybody, or in all cases.”

I read the disclaimer and am not negating your thoughts. Just adding my own experience. I do love your thoughts on personal improvement and guarding your time (I can always improve in that category!). Thanks for your thoughts JayCeezy!

Thanks, Maggie! I picked up the ‘self-improvement and motivation’ bug from my father, and a coach in school who had a sign over his desk, “Good, Better, Best, Never Let It Rest, ‘Til the Good is Better, and the Better is Best!” Another coach told me, “Every day you don’t practice sets you back three days: 1) the day you took off, 2) the day your opponent showed up, and 3) the day you will need to get back to where your skills were the day before you took off.

All great ideas that I can agree with. Although I don’t think the pay cash for a car thing applies to people in personal finance. I bought 2 cars this year and could easily have paid cash for both, but made a no brainer decision financing them at 0.9%. People who have a hard time saving or making payments should definitely pay cash, though!

Absolutely, Sean. Sounds like you have a very favorable interest rate on your loan. My point was “if you can’t pay cash, don’t buy it” and you obviously can pay for the car (not just make the payments). So many of my contemporaries, right out of school, tried to front off and started driving luxury cars with horrendous monthly payments that prevented them from advancing their PF goals (if they had any to begin with). So they looked cool for a couple of years driving a BMW, but after five years they became “the guy who drives a 5-year-old Beemer!”:-) To my knowledge, none of those guys would ever acquire a car of less ‘status’…that is until their first divorce. One of those dudes is an attorney, with four kids not yet in college, alimony payments, and he lives with his current wife in the very upscale Palos Verdes neighborhood…wait for it…in a rented house. And drives a 7-series BMW ($80K+) But he looks cool!:-)

Thanks again JayCeezy for sharing your wisdom over here on the GYFG blog.

Thanks for the chance to share, GYFG. The PF community (and the GYFG community you are building) is really something I enjoy participating and sharing with. In ‘real life’, not many people are interested in the subject to great degree, so it is nice to exchange thoughts and experiences. My own thoughts in the post are not so much ‘wisdom’ as bits-and-pieces that have been passed down to me from mentors, learned and applied from books, and real life mistakes (kind of like those guys showing their scars in ‘Jaws’, I paid a price but am still alive!). Continued success to you, and to all!

Good stuff. Very blunt. That can be tough to swallow sometimes but being blunt is almost always the best way to be. Lately, I’ve been thinking a lot about my weaknesses and flaws, and your post reminded me of them again. I need to address them – like now. I need to focus on becoming the person I want to be. Thanks again.

Thanks, Mattattack! Sometimes ‘blunt’ can be hostility disguised as honesty, and my intention was to save the reader time. They can take or leave what is in the post. I like what you said, because sometimes I have received a “truth” that “left a mark!” This is a good time of year to reflect on what has been done, and still needs to be done. I’m doing it myself. Wishing us both (and all the PF community) success in this endeavor! Thanks again.