Did you know you can invest alongside the grim reaper? Yes, you can actually profit from death. I know this sounds morbid and probably a bit shady, but let me explain. At the end of this post, I think you will realize that the alternative investment class discussed today provides a win/win for all parties involved, and may just be the perfect addition to your own portfolio.

I’m constantly searching for new opportunities to allocate capital, specifically into investments that provide a HUGE margin of safety. This is because, unlike most, I approach investments with a risk focus first. Only after I understand the potential downside do I even begin to contemplate the potential upside.

The investment vehicle that allows you to profit from death is called a life settlement.

What Is A Life Settlement?

A life settlement is simply the purchase of an existing life insurance policy from the policyholder, by a third-party investor (or a pool of investors). This typically only takes place when the policyholder can get more than the surrender value offered by the insurance company.

According to leading actuarial firm Milliman, Inc., approximately 90% of all life insurance policies are surrendered or lapse without payment of a claim. – From Reliant Life Shares

There are three main reasons that someone may want to sell their life insurance policy:

- The policyholder can no longer afford the insurance premiums to keep the policy active.

- The policyholder no longer needs or wants the life insurance policy.

- The policyholder may need the money now to pay for medical bills or to maintain their standard of living during the remaining years of their life.

Life settlements have created a secondary market for life insurance policies. And the reason the secondary market exists is that the fair market value of a policy, in many cases, is much higher than the cash surrender value offered by the insurance company.

A 2002 study by the Wharton School at the University of Pennsylvania found that the fair market value of a sample of insurance policies was $336.3M vs. the surrender value of $93.4M. – From Wharton Study

The Wharton study shows that via a life settlement sale, a policyholder can get 3.6X what the insurance company offers as the surrender value. I should also point out that this applies to Universal life insurance policies only.

What Makes It So Attractive For Investors?

First and foremost, this is a non-correlated asset, which means it doesn’t matter what is going on in the stock market, bond market, real estate market, or the markets for any other traditional assets. From my research, I have found the following reasons that make life settlements attractive investments:

- Non-correlated, thereby reducing the volatility of your overall investment portfolio.

- Fixed return. You know exactly how much money your investment is going to make.

- Minimal risk. The only real risk is of the insured living past his or her life expectancy, which in many cases pushes out your payout, and lowers your expected return.

- Historical returns in the 12-14% range.

- The market for life settlements is primed to get much larger, with 10,000 baby boomers turning 65 daily. The current size of this investable market is about $20 billion but is expected to grow to $100 to $160 billion over the next 2 decades.

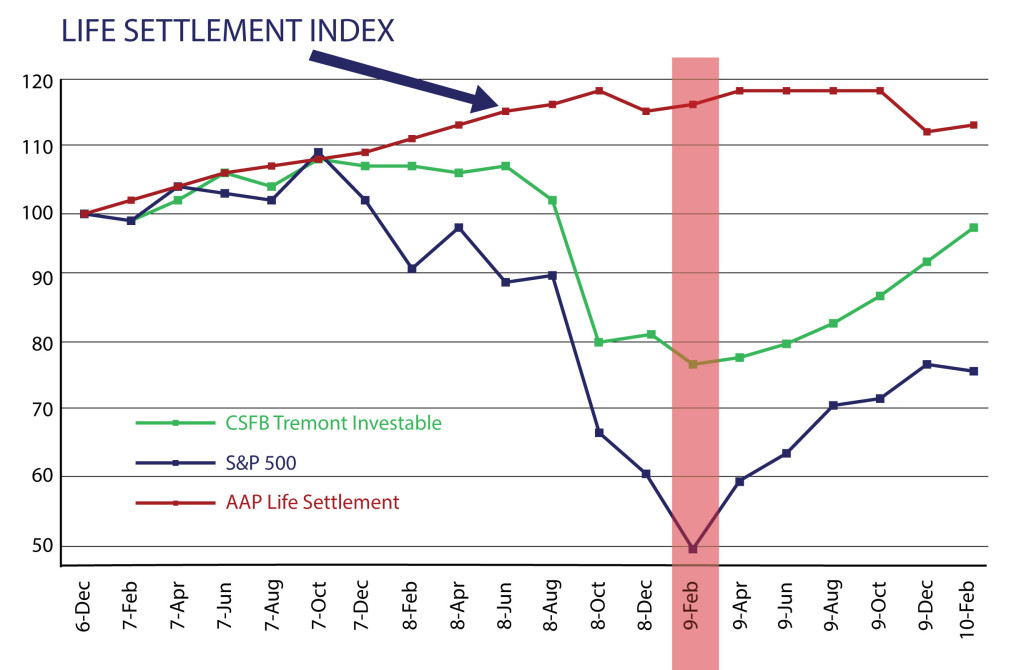

Look how life settlements performed as an asset class vs. the S&P 500 during the Great Financial Crisis of 2008-2009 (2009 lows highlighted in the chart below):

What Is The Downside?

No investment comes without risk, so of course there is a downside to life settlements as well, which should be examined. In my opinion, however, the risks of the downside are very minimal:

- No liquidity until the insured dies.

- If the insured lives past life expectancy, investors will get a premium call. The escrow account associated with the policy is only pre-funded with enough money to satisfy premiums through the expected life of the insured, so investors will have to pay any premiums on the policy past that predetermined age as long as the insured lives.

- Could continued scientific advancements extending human life and curing major diseases continue, making this scenario more likely?

- Your friends and family may think you’re a bit morbid investing in and profiting from an investment associated with death.

The Niche Part Of The Market That Interests Me

First, I should point out that a life settlement typically refers to a policy that covers an insured 65 years or older, with an estimated life expectancy of 13 years or less, but who is not necessarily terminally ill. This is different than a viatical settlement, which refers to a policy covering an insured with a life expectancy of less than two years and who is terminally ill.

Some familiar with life insurance may be scratching their heads recalling that with some life insurance policies the insured can get early access to the death benefit. True, but this usually requires a life expectancy of less than 12 months to qualify, which is another reason why both the viatical and life settlement markets exist.

The company I have invested with is Reliant Shares, located in California, where the life settlement market is heavily regulated in order to protect both investors, policyholders, and the insured. I have navigated towards Reliant due to their rigorous evaluation process and filter for the policies they decide to purchase and make available to investors. The other major benefit that I see with going with Reliant is that they keep their own skin in the game for every policy they make available to investors, usually owning somewhere around 20% of the total investment themselves.

The Filter Process

- Reliant’s policy acquisition team reviews $300 million worth of policies each month, with only a small fraction of that making it through their funnel. To give you further context, they have been in business since 2012 and have only made 30 life insurance policies available for investments, out of a selection of hundreds and maybe even thousands.

- Reliant’s face value sweet spot is $2.5M or higher.

- Their ideal targeted life expectancy is two to five years. Reliant goes the extra mile by providing multiple life expectancy reports from other licensed third-party underwriters for each policy they market. In addition to these third-party determinations, Reliant also discloses a Social Security Administration life expectancy estimate.

- They only offer universal life policies for investment.

- The insured is typically 70 or older, with Reliant’s ideal target being around 82 years old.

The Investment Process

- Reliant uses UNB, a 103-year-old bank, to handle the Escrow and Trust. Hence, you are not really investing with Reliant, but rather your investment is held in a trust with UNB. This very stable bank guarantees your fixed return.

- The minimum investment is $30,000 and will get you into three policies at $10,000 per policy.

- You can invest with after-tax money or through a self-directed IRA account.

- Once you invest, you do nothing more active than sit back and wait for the payout.

What Did I Invest?

I recently made my initial $30,000 investment across three different policies at $10,000 each. The three policies I purchased have the following fixed returns:

Policy #1 – 45% fixed return.

Policy #2 – 64% fixed return.

Policy #3 – 75% fixed return.

I love both the passive nature and known fixed returns at the initiation of my investment. As I mentioned above, the asset class has averaged 12% annual returns, which means if we take the fixed return and divide by 12%, then we can get the expected duration before payout (I used 12% as this is the rate Reliant is targeting in a diversified portfolio). So, if we take the fixed return of 45% above, I would expect a payout in 3.75 years (or sometime in 2021).

One thing to keep in mind is that the 12% is not the compound return. The compound return actually works out to be a bit lower if this pays out on time in the expected 3.75 years estimated duration. We know that with a 45% fixed return that $10,000 turns into $14,500. When you do the math to get the compound rate, you will find that the compounded rate that turns $10,000 into $14,500 over 3.75 years is 10.42%. Of course, the payout can happen earlier if the insured doesn’t make it to his or her estimated life expectancy, which would have the effect of increasing the annual compound return, but the fixed return remains constant at 45%.

Alternatively, the payout could be delayed if the insured lives past the estimated life expectancy, which would decrease the compounded return and could actually lower the fixed return due to out of pocket premium calls to keep the policy active, since (as described above) the escrow account is only pre-funded with enough capital to make premium payments equal to the estimated life expectancy.

Overall, I expect to earn 10.5% to 12.5% compounded returns from this asset class over the long term.

This is only my first investment in this product classification of many I plan to make. My short-term goal is to increase my investment from $30,000 of initial capital to $100,000 over the next 6-12 months. In a future post, I will go over more specifics with the three policies I purchased above.

If you would like to receive more information about this investment class and support this site at the same time, please send me a note about your interest in the contact form below. I have worked out a special deal with Reliant that will allow me to give you a $25 Amazon gift card if you decide to invest. You don’t have to go through me, but I do appreciate your support if you choose to. Once Reliant confirms your investment I will send you a gift card electronically through email.

Error: Contact form not found.

– Gen Y Finance Guy

4 Responses

This is a very interesting asset class and I’m glad you posted about it. There’s a reason Warren Buffett is investing in this. It’s one of the rare asset classes that did ok during the Great Recession and is totally uncorrelated to the stock market. I’ve stayed away from investing because I don’t know enough about the investment companies to totally trust them. A few have been busted as scams. I’m glad you found Reliant and I’ll be curious to see how your investments turn out. Three individual policies seems like higher concentration risk than I’m comfortable with. There is one shop I heard on a podcast recently that does a fund with hundreds of life policies in it.

One definite risk is increased life expectancy. There is a lot of new and exciting work being done in the cancer field including targeted molecular gene therapy and imaging, AI and machine learning. The ultimate goal is to tailor unique treatment to each individual patient.

For me, as a physician, betting and profiting on someone’s death sort of goes against the whole Hippocratic Oath thing. Another reason I’m shying away– just based on principle. I might just have to get over that. Great post!

Millionaire Doc – Yes, there are a lot of companies out there that are not legit. I chose Reliant because of both their filter process and the regulations they comply with here in California, one of the few states that regulate the market for life settlements. Because of this they only do business in California with California residents.

Three policies are just my starting position, but I plan to increase that to 10 policies over the next 6-12 months. But compared to hundreds, yes it is concentrated compared to most peoples risk appetite. It would be interesting to check out the company you heard about on the podcast. Let me know if you remember the name. During due diligence, the other thing that drew me to Relient was the criteria they had for these policies.

Life expectancy is the major risk I see as well, but these policies cover people in their 80’s with lots of medical issues and family history of medical issues. I also wonder the following questions with respect to the advancements in science and medicine:

(1) What kind of condition will the patient need to be in to qualify for new treatment?

(2) How long will it take to become available to the mass market?

Most of these policies that I have or will invest in have at least 5 years of cushion past the estimated life before you begin to lose any money.

But only time will tell. I appreciate your input and perspective.

Cheers,

Dom

Hi Dom,

So I tracked down the podcast. It was on CashFlow Ninja episode 213 with Kevin Nichols. He is the principal at Penumbra Solutions. http://cashflowninja.com/kevin-nichols/

They open a new fund every year which contains hundreds of new life settlements which they cherry pick. The older and unhealthier, the better. Morbid.

Re targeted therapy, many drugs have been used in the mass market for years already. Some well known ones include Herceptin, Avastin, Gleevec, and Nexavar. FDA is approving many more each year. These are used both as first line treatments along with conventional chemotherapy as well as for patients who have exhausted all conventional therapy. They are expensive but most insurance and medicare cover a chunk of it.