Today we have a guest post from Simple Money Man on saving and spending. He has been a long-time reader and regular commentator on the blog and so when he reached out I was more than happy to host a guest post from him. Although our opinions differ on a few points in his post below, I know that not everyone to this site resonates with my philosophies, and some may be early in their journey and need to practice more of what Simple Money Man recommends below.

A part of me has this weird conspiracy theory that we spend so much because we are subliminally trained to do so. This is evident with incentives like rebates, points, rewards, free “trials”, cash back and even free merchandise (which is not really free since we did spend in order to be eligible for it in the first place).

There are also so many ways or methods of spending which are so easy and right at our fingertips and thumbprints. We don’t even have to take out any real money or even credit cards. Merchants may have our payment information stored online or we may have payment information stored in our smartphone that we can just scan at so many places. By the way, the security around this is a whole other story, which I won’t get into here.

Therefore, if we can make saving easy and spending hard, it can help us achieve financial goals including a respectable retirement balance or an emergency savings cushion that allows us to sleep at night.

Make Saving Easy Using Automation

Automate Savings

Simple things can be done to automate your savings; all of these just follow a set it and forget it mentality:

- Automate contributions to your retirement plan – whether you work for a company or are your own boss, you can contribute to your retirement plan on regular intervals. If your employer offers a matching contribution, be sure to contribute at least up to the amount of that match.

For example, let’s assume your employer matches 50% of your contribution up to 5% of your base pay. Let’s say your base pay is $50,000. This means that 5% of your base pay is $2,500 ($50,000 X 5%). So you should at least contribute an annual amount of $2,500 simply to obtain the employer match which is FREE money.

- Automate Health Savings Account contributions – you can contribute to your health savings account every pay period. This is an account that allows you to contribute pre-tax dollars into a fund. Generally, participants receive a credit card that can be used to pay for copays, prescriptions and for other medical related expenses. You can set the amount you’d like to contribute and best of all, it lowers your taxable income!

- Automate contributions to your brokerage account – you can set automatic deposits from your checking account into your brokerage account at intervals, such as monthly. Then you can invest in stocks and ETFs. It doesn’t have to be a big amount, but something to get the ball rolling – the snowball of investing.

The key is consistency in your savings. Once consistency is established you’ll be in a better position to reevaluate and up your savings rate. Maintaining a high savings rate is crucial in establishing lasting wealth. Over time, saving becomes easy with the help and power of automation.

Using automation as a tool for saving has proven to work. From a study in Denmark, John Friedman of Harvard’s John F. Kennedy School of Government indicates that you actually save more when you do not pay attention. He goes on to say that the implementation of passive saving policies like automation are significantly better than active such as tax incentives to save.

Automate Investing

The brokerage account I’ve had for years, Scottrade, has a Flexible Reinvestment Plan tool. I just go into my account every so often and to make sure it is operating as intended (i.e., the securities of funds I want to reinvest in are designated at the proper percentages, what my flexible reinvestment balance has accumulated up to, when the next trade date is, and the transaction history to make sure dividends are transferring into this account as they should be).

Apart from Scottrade I also use Robinhood. This platform doesn’t have an automatic reinvesting tool, so I manually reinvest about once a quarter. But the benefit is trading is free on Robinhood, which is one of the reasons I signed up for an account over a year ago.

One of the key benefits in automating your investing is dollar-cost averaging. This is the art of consistently investing in the stock market so that the prices you buy at average out over time. And we all can agree that over time the stock market does provide positive returns.

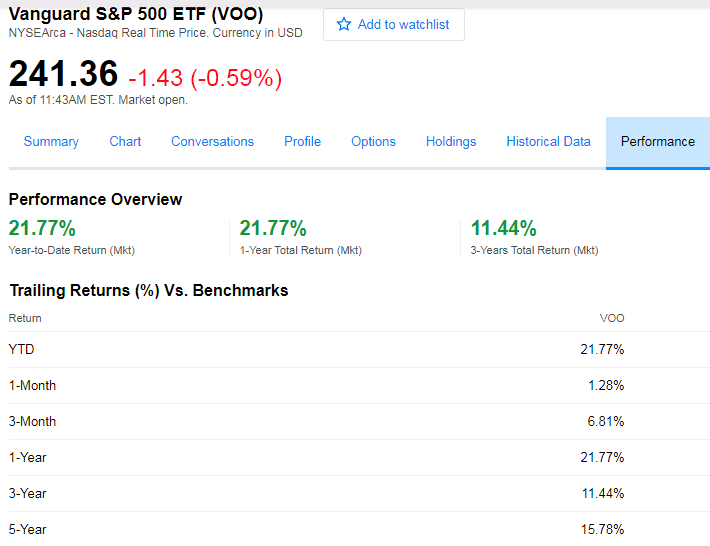

And even if you started with dollar-cost averaging 5 years ago into Vanguard’s S&P 500 Index Fund (VOO), your investment would generate a return of almost 16%:

[GYFG here; I’m a big fan of automation. This ensures you follow through with your goals and shifts the burden from you to a machine.]

Make Saving Easy Thru Reinvestment of Dividends

Dividends are one those great things that make saving super easy. Once you invest in stocks or funds that pay out dividends, you can just sit back and relax, a little bit that is.

As I mentioned earlier, some brokers have a feature which automatically reinvests dividends earned into securities you designate. If yours doesn’t, be like me and set a reminder on your calendar to check up, maybe quarterly, to reinvest your dividends.

As time goes by, dividends earned and reinvested will begin to accumulate and it may be a good idea to consider tax efficiency on dividend income.

Make Spending Hard By Using Only Cash

It may be hard going to the ATM on a regular basis and withdrawing cash. But I know people that do that and as a result, they are disciplined with their spending. Try it out and see if it works for you.

It may be good to start out with a small amount as it may make you cognizant of your routine spending. Of course, the amount is different for everyone whether it’s $20 or $40 or $100 a week. Once you get used to using only cash, you’ll actually become better at researching purchases to find the best deals and ignore bogus sales tactics.

[GYFG here; Although this may work for some, I’m more a proponent of using rewards credit cards, that allow you to get paid for the spending you were going to do anyway. But this is ONLY a good idea if you have the discipline to treat charging as you would cash, meaning you don’t spend more than you can afford to spend or more than you would spend if you had to pay cash. In 2017, I earned almost $10,000 in cash back based on our regular household spending.]

Making Spending Hard By Preplanning Your Weekend or Leisure Time

Often times the weekend will come around and we have no idea what we want or need to do. We have no plans or preparation in place and that can be dangerous. As a result, you may not have meals prepared and will eat out more. You may not have free activities scheduled so instead may drive to your local mall or shopping center and become a consumer looking to buy something just to fill in the time.

By preplanning your weekend, you’ll be able to deliberately put thought into activities and run the costs/benefits and advantages/disadvantages of those activities. This doesn’t mean you should deprive yourself. You’ve worked all week, and may have to work on the weekend too. You deserve to indulge in something you or your family will enjoy. There are plenty of low cost or free activities to enjoy such as a picnic at a part, visit to the museum. If you live near a metropolitan area, there are museums that cover so many topics (e.g., history, outer-space, and nature).

And if you need to buy groceries or run errands, try using a list. We’ve implemented this and it really helps on staying focused in the store(s), saving money and time. There have been many times in the past where we’ve either bought something simply because we were indulged at the grocery store and at the same time forgot to buy something we actually needed. This was the result of not using a list.

[GYFG here again; This is one way to look at it. For me, this puts too much emphasis on the expense side of the equation. Not that I’m recommending anyone spend recklessly, but I promote and prefer that people focus more attention on the income side of the equation. Work to increase your income to a point where these types of expenses or indulgences matter less. Practice what I call relative frugality.]

Have you implemented any of these saving or spending strategies? Which ones are the most and least effective for you?

7 Responses

SMM, excellent post. Appreciate your illustrating the processes, and providing ideas for implementation.

Am dating myself here, but your ‘savings hard’ part reminded me of a Jerry Seinfeld joke from the ’80s…

“Spending is too easy with credit cards! There’s no pain! When you hand over cash, it’s painful! There should be pain involved with using a credit card. Every time you use it, they should run your hand through the machine too!”

GYFG, almost $10,000 cash back?!?!! Awesome. Can you share what you spent to get that? Thanks in advance!

JayCeezy – The $10,000 was on about $100,000 of spending on credit cards. Keep in mind that I also travel for work and get to put all of that on my personal credit cards. And at least 50% of the $10,000 was from the sign-up bonuses. Oh, and we always sign up for the same card in both my name and then another account in Mrs. GYFG’s name in order to get double the sign-up bonuses. I churned several different cards last year:

(1) Chase Reserve

(2) Citi Prestige

(3) Delta Gold America Express

I love Seinfeld; have seen all the episodes at least twice! I can imagine Jerry saying that. 🙂

A little pain every now and then in the short-term is good in the long-term and I like to think long-term.

Thanks for the guest post opportunity Gen Y Finance Guy! 🙂

Boom, excellent read yet again!

Hey SMM and GYFG,

I’m a huge fan of dollar cost averaging and automatic investing. When the decision is made for you already, there’s no temptation to direct the money elsewhere. I find that this is one of the big advantages of robo-advisers, in that some (like Betterment and M1) can be set to automatically transfer a set amount of money every month into your investment account, and they’ll take care of the rest (including re balancing).

Cheers,

Miguel