How long will it take to double your money? Can you do the math of compound interest in your head? Do you want to extrapolate how long it will take your money to quadruple, octuple, or to hit an even bigger Big Hairy Audacious target, Freedom Fighter?

Do you wish there were a shortcut to all these answers?

Well, I have good news for you! There is a simple formula you can use to get a decent approximate answer – all without any fancy or complex math. It’s the “Rule of 72.” This simple shortcut will give you an approximate time – in years – that it will take to double your money (investment, net worth, etc). All you have to do is divide 72 by the annual interest rate you expect to earn or compound your money at:

72 / Compound Annual Growth Rate = Time to Double

As an example, let’s say you expect to earn a 10% compound return (nice!). Plugging this into the formula (72 ÷ 10) would result in a 7.2 years journey for your money to double. And it will double again every 7.2 years.

72 / 10 = 7.2 Years

Note that your expected return of 10% gets plugged into the formula as 10 and not 0.10. Doing the latter would give you an incorrect answer of 720 years. Not exactly a “get rich fast” trajectory! Also, remember that this will get you very close to actual, but is technically only an approximation. The formula to get an exact answer is a bit more complicated and not one most people can do in their head, including me. But if logarithmic calculations are your jam, knock yourself out:

T = ln(2) / ln(1.10) = 7.273

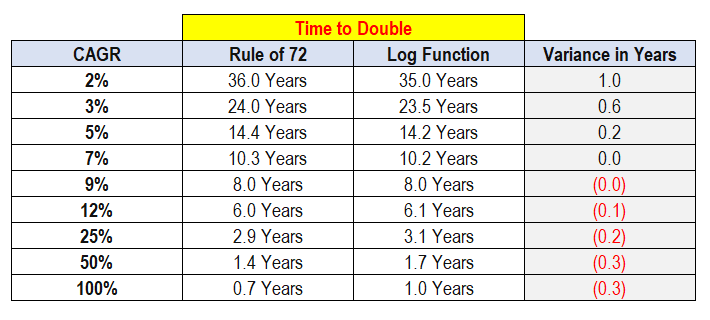

As you can see from the example above, you get almost the same exact answer (especially above 3%), which is good enough for me. Further justification? Let’s take a quick look at the variance between the logarithmic function and the rule of 72.

I don’t know about you, but the level of precision provided by the shortcut is good enough for me, and another example of “done is better than perfect.” If I want something more accurate I will just go to an Excel spreadsheet, otherwise I will use this simple shortcut to either do the math in my head, or even on the basic calculator installed on my phone. And I’ll also shoot for >5% returns!

I don’t know about you, but the level of precision provided by the shortcut is good enough for me, and another example of “done is better than perfect.” If I want something more accurate I will just go to an Excel spreadsheet, otherwise I will use this simple shortcut to either do the math in my head, or even on the basic calculator installed on my phone. And I’ll also shoot for >5% returns!

Fun Thought Experiment

Just for fun, take your current net worth and figure out how long it will take to increase by 8X based on a 7% compound rate of return. Let’s say your net worth is $100,000 (congratulations! you’ve made the six-figure club) and you want to find out how long it will take for that $100,000 to turn into $800,000, while earning a 7% compound rate of return (assuming no additional contributions).

You can use the table above as a cheat sheet.

– At 7% we know that it will take approximately 10.3 years to double, which means your $100,000 turns into $200,000.

– The $200,000 takes another 10.3 years to double to $400,000.

– Finally, the $400,000 doubles to $800,000 after another 10.3 years of compounding.

So, it will take approximately 30.9 years to turn your $100,000 investment into $800,000 (or 30.6 years if we adjust for the minor error of this shortcut).

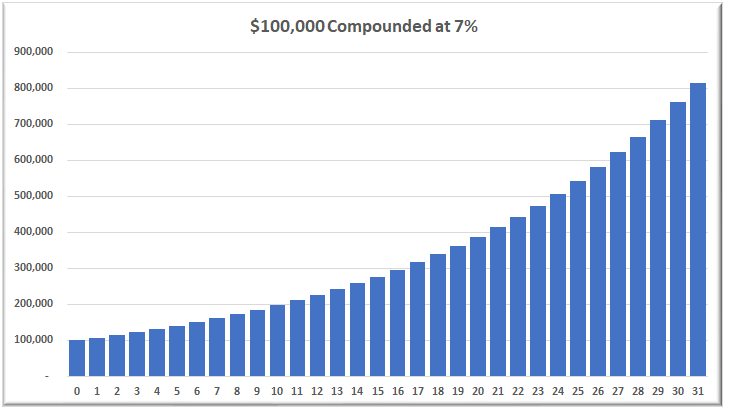

Now let’s visualize this:

If you plot this out in Excel, like I did to create the above chart, you will notice that from Year Zero to Year One the increase is $7,000 due to compounding. However, by Year 31, the increase from year 30 is 7.6X larger at $53,286 (assuming a full 31 years of compounding, which gives you $814,511).

Don’t miss this: From Year Zero to Year One the increase is $7,000. But by Year 31, without any further contributions, the increase from Year 30 is 7.6X larger at $53,286!

I point this out to reiterate the importance of starting as early as possible. The power of compounding is much more powerful in the later years than it is in the early years. Get that first $100,000 saved and working for you ASAP. “Money makes money. And the money that makes money makes more money,” Benjamin Franklin.

If you’re anything like me, you will use this quick little shortcut to project your current net worth from time to time. I actually just did it in my head as I typed this sentence simultaneously. My current net worth as of April 2018 is $754,000. If left to compound at 7% uninterrupted, even with no additional contributions, it will grow to approximately $6,000,000 in about three decades time. Duh – I’ll still be contributing the heck out of it for a long while, but it’s validating to know that I’m headed in the right direction toward my $10M goal.

There is a further benefit to doing this exercise. When you see your own net worth in terms of future numbers, BIG numbers, you are telling your subconscious something powerful: this is where I am headed. Beyond just making sure you are headed in the right direction, this exercise will inform and familiarize your mind with those big numbers. This equips your unconscious mind to 1. look for opportunities to get to that destination even while you are unaware this is happening; and 2. enable you to instinctively act like someone characterized by those big numbers, kind of inoculating yourself against stupid behaviors that would divert you from your goal.

Do this same exercise with your own net worth. Then imagine how much more powerful this becomes if you are still adding to your investments and how a 50% plus savings rate could supercharge your results. Now take a look at your expenditures. Every dollar you spend now is like a soldier you send out into the world, whether to fight for your Financial Freedom, or to fight for someone else’s Financial Freedom. Did you just discharge that $1 soldier from your own Freedom Fight unconsciously, or intentionally?

Perhaps you receive a windfall, like a big bonus, an inheritance, or a tax “refund” (fix your taxes for next year if that happens, FF, so you don’t lend the government any more money at 0%). Plug a big chunk into the formula and see how your sails fill with that wind and really speed things up!

Time plus the “Eight Wonder of the World,” as Albert Einstein described compound interest, are your weapons for the taking. Or not.

Did you find this shortcut handy in extrapolating the time it takes to double your money? How do you feel when you futurecast your net worth – does this make you stop and course correct, or smile and pat yourself on the back? Let me know how you’re doing in the comments.

– Gen Y Finance Guy

7 Responses

$10 mill? At this point i think you are sandbagging Dom. If you even worked only 10 more years you would smash through that goal easily. in 30 years. Isn’t that crazy to think about?

Congrats man. You’re killing it!

I believe the $10 million goal is by age 48. Of course, Dom will end up with more than $10 mil over the long haul. I wouldn’t be surprised if it turns into $30 mil or more by the time he’s in his 60s

Kevin – The math makes $30M look easy and inevitable. But I admit I get tired thinking about the work that needs to be done to still get to the $10M and with a kid on the way…the sleepless nights…must fight through!

Thanks for your vote of confidence!!!

Dom

HLF – I hope I’m sandbagging. Until I’m halfway I can’t let my foot off the gas.

Thanks for stopping by!

Dom

I think your source for the Ben Franklin quote is a bit off. It should be “Money makes money. And the money that money makes makes more money.”

Windfalls are important to note. Pretend you only got a small percent (5% to 10%) of that windfall) and lock up the rest in investments quick!

I didn’t know this shortcut but sure it’s a nice one. If I stopped saving now, and expect that 7% return per year, I’ll be able to retire comfortably at exactly…65. That’s encouraging/disappointing at the same time.

I’ll add this to my math shortcuts collection and use it from now on. I only have one more shortcut in the collection though, converting Celsius to Fahrenheit degrees: (Fahrenheit degrees) = ((Celsius degrees) + 32) / 2 (I’m too lazy to multiply by 5/9).