And we’re back! Halloween always seems to be the line in the sand that separates summer from fall where I live and it marks the start of my favorite time of year. The weather has cooled down significantly and the AC will be off for the next six months. Even better, the clocks will “fall back” for daylight savings time in California and psychological trick or not, I always feel more rested when this happens.

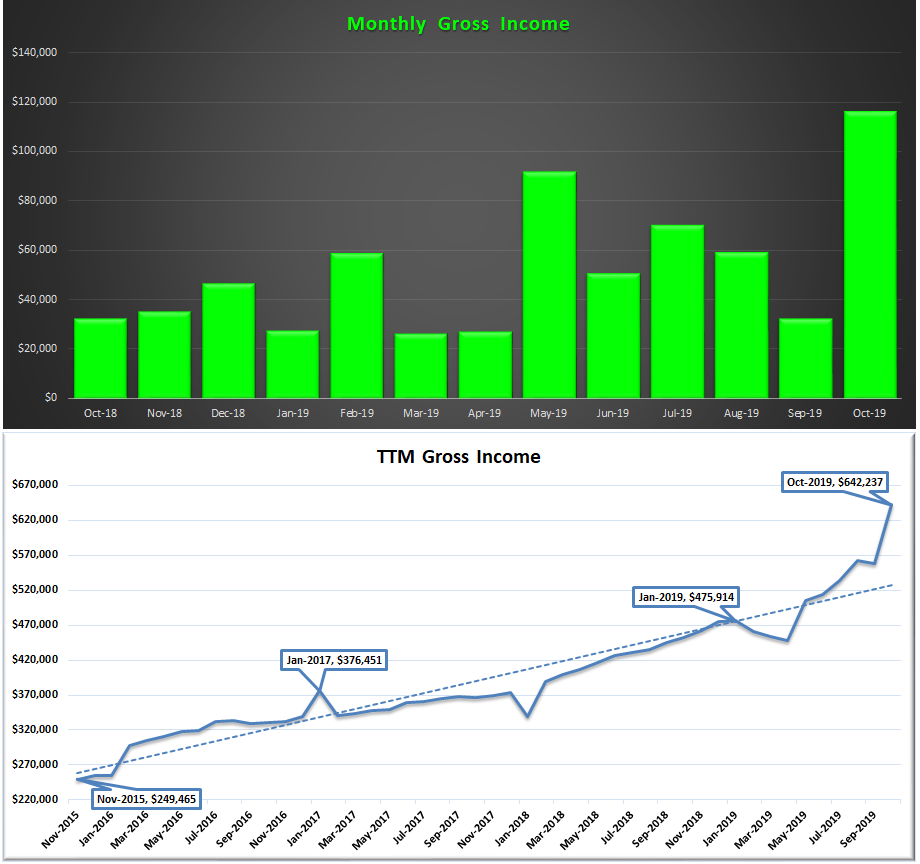

October was a month for records, both in the markets and the GYFG financials. It is also an odd month where our income hit an all-time high at $116,170, we deployed almost $225,000 in capital, and our savings rate was almost 80%, yet our net worth declined by almost $18,000. This is only the second time in 58 months (almost five years) that we have seen a decline in our net worth, so I can’t really complain, nor am I upset. The reason it happened was that I made a big move with my idle cash to create a $343,000 tax deduction against my 2019 income. Yes, I bought a deduction! It cost me $68,600 in order to get a $343,000 tax deduction, which equates to about $150,000 in tax savings.

I have been working closely with my new CPA to work on tax strategy for 2019 and we concluded that this was the best route – at least for this year. It was mind-blowing going through the exercise of estimating our final annual income for 2019, which is currently projected at $667,000. This wasn’t the only big move I made in October.

An opportunity came across my desk to extend a $150,000 hard money loan at 10% interest for the next 6-12 months (half of this was funded by my HELOC at 6% temporarily for cash flow reasons). This is with a very close and trustworthy family friend that flips and invests in real estate for a living. We have done one deal with him in the past, but it has been several years. The economics of the deal are great in my opinion. He purchased two manufactured homes in good parks for $265,000 (total) and when he swaps them out with better units they will be worth $280,000 each (or $560,000 total). It’s going to cost about $150,000 – $200,000 to replace the properties, leaving $95,000 – $145,000 in profit.

The other move I made was to put a whole life insurance policy in place for my son. We are pursuing this route in place of the more popular 529 plans. We chose a policy that comes with a $5,000 annual premium and should be worth at least $120,000 by the time he is 18. This will give him maximum flexibility in how he wants to use the money when that time comes. I don’t know what college and tuition is going to look like by the time he is 18 (in 2036), but I do think it is ripe for disruption and currently on an unsustainable path. There are so many different ways he could pursue an education; if he does go to college, he could choose to go to a state school like I did and use the difference in this fund to buy his first house. Then, while in school, he could house hack by renting out the rooms to create an income while he focuses on school without having to work a job. Lots of ideas, and quite a few years yet to mull them all over.

That’s the view of our financials for 30,000 feet, now let’s dive into the details.

If you’re a regular reader and only want to read the new content, feel free to just skip the intro below, and head to Net Worth. If you are new or haven’t read many of these reports, I encourage you to take two minutes to read the intro below, which does change periodically.

Why I Share These Monthly Reports

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

For those of you new around this corner of the internet, these monthly reports are about full transparency. And, they are just as much for me as they are for you. It was a hard decision to make all of my financial details public, but it has proved to be a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141 and our gross income was on pace to hit $178,000 that year.

Four years and ten months later, our net worth currently clocks in at $1,342,681 with a gross income over the trailing twelve months of $642.237.

- That’s a 6.9X increase in net worth due to a compound annual growth rate of roughly 50% for the past four years.

- At the same time, income has increased 3.1X, which translates to a compound annual growth rate of roughly 27%.

Honestly, I don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will share our results with you readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack does. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle to only then have the means to check off bucket-list items when my body might no longer be physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. Choose to spend on what is meaningful to you. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. Keep this famous Jim Rohn quote in mind:

“If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!”

You must be intentional with your finances if you ever want a fighting chance to make it to financial freedom. But it does not have to take 40-50 years of slaving away for “The Man” before you have the option to retire. I think 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two of the vital components of a good recipe for the 10-year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not so many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, and I think real life examples and numbers can help slice through the complexities (and the BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere, so I always intended to share my own.

You can find all my previous reports on the Financial Stats page.

Financial Stats Dashboard

At the end of each month, I download a .csv file from my Personal Capital account and drop it into my custom built Excel workbook in order to update the dashboard you see below. I’m blown away every month by the progress we have made in a relatively short period of time.The only number below that is not an actual number and instead is a forecast is the current year projected income of $666,992 in the gross income chart below.

Now that we have seen the overall, let’s take a closer look at a few of the items below.

Net Worth

As I mentioned above, we experienced a decline in net worth during the month of October. The two main drivers for the decline are as follows:

(1) We bought a $343,000 tax deduction for $68,600. Yep, we will never see that money again. That said, this is going to save us approximately $150,000 in taxes. When you boil it down it was either write a check for $68,600 or $150,000. The math was a no brainer. The net savings is $81,400 or 118% return. I don’t know of many any opportunities for that kind of return. You are probably wondering how this is possible, right? It’s accomplished by buying land (or into a partnership that does this) and then establishing a conservation easement that involves donating the land and receiving a charitable contribution in return. The tax deduction is calculated based on the highest and best use of the land if it were tobe developed and not the actual purchase price (in my case, you will notice that the tax deduction is five times the amount of the actual donation). The land is then conserved and no one can ever develop it.

(2) We extended a $150,000 hard money loan with a 10% interest rate paid monthly for a duration of 6-12 months. Due to the above, we didn’t have all the cash to fund this, so we decided to pull $75,000 from our HELOC to manage a temporary cash-flow issue. We should have this paid back within the next month or two. For example, next week I will receive about $30,000 that is owed to me from my business, which will go directly to pay down the HELOC loan. The business still owes me about $40,000 through October (above and beyond the $30,000 mentioned above). It’s also a three pay period month for me in November and Mrs. GYFG is forecasting a significant increase in her commissions over the next several months. On top of this, we also have about $40,000 sitting in our checking account.

(3) We paid the first $5,000 premium on the new Whole Life Insurance policy that we put in place for our son. (As I type, I realize that I didn’t actually capture the $3,147 in cash value that the policy has after making that payment, but I’ll just pick that up next month.)

Add those together and that is a hit of $148,600 to our net worth month over month. To add further context, that means that we actually had $130,826 in increases that offset a large portion of this decrease, which resulted in our decline of $17,774 this month.

October Net Worth $1,342,681 (up $329,816 or +32.6% for 2019)

- Previous month: $1,360,455

- Difference: -$17,774

Net Worth Break Down (MoM):

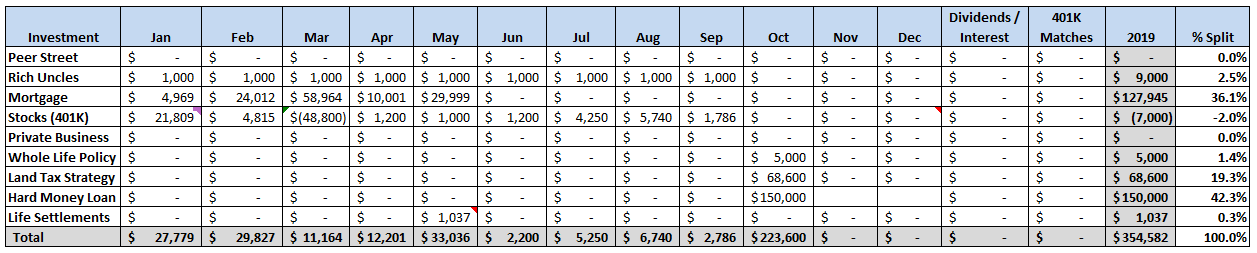

The Real Estate ($718,050) category increased from 47% to 53%. This category includes the equity in our primary residence ($463,896), a new hard money loan in the amount of $150,000 at a 10% interest rate ($75,000 net of HELOC Loan), our investment in the Rich Uncles commercial REIT ($76,672), and our hard money loans through the PeerStreet ($102,482) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000 (which is why the PeerStreet value hasn’t been changing much MoM).

The Real Estate ($718,050) category increased from 47% to 53%. This category includes the equity in our primary residence ($463,896), a new hard money loan in the amount of $150,000 at a 10% interest rate ($75,000 net of HELOC Loan), our investment in the Rich Uncles commercial REIT ($76,672), and our hard money loans through the PeerStreet ($102,482) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000 (which is why the PeerStreet value hasn’t been changing much MoM).

Net Cash ($117,013) decreased from 16% to 9%. We actually have $117,538 in cash but net cash is only $117,547 after you adjust for our current credit card balance of $525 (a record low), which we pay in full every month based on the statement due date. Keep in mind that of that $117,013 a portion (~$65K) is related to what my business owes me (a combination of my direct billable work and the profits of the business). The money the business owes me decreased substantially and will talk about that in the next section.

{kind=link}

The Business ($234,962) category remained flat at 18%. This represents the ownership I have in the private company that I work for. This is an illiquid investment that only gets an update to its value one time per year. I net the company stock asset value of $446,962 against the company stock loan of -$212,000 to arrive at the $234,962. I’m looking forward to updating the value of this at the end of the year (currently looking at a six-figure increase in value).

Life Settlements ($94,109) remained flat at 7%. We currently have investments in seven policies at $10,000 each. They are accreting in value by about $1,000 per month. For anyone familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with this fixed return you are amortizing (realizing) that value with the passing of time.

The Stocks ($178,547) category remained flat at 13% and represents the cumulative value of our brokerage accounts (retirement accounts) that are invested in stocks. However, this is not all of our retirement money, as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $82,000 and counted in the Real Estate category of the pie chart).

Total Capital Deployed in 2019:

I kind of stole the thunder from this section, but it was a huge month! To date for 2019, we have officially deployed almost double the expected $182,000 that I had originally planned to deploy this year. There were no new contributions to Rich Uncles as they have temporarily put a hold on new investments while they work through an acquisition. And since our 401k’s were officially maxed out in September, there will be no new investments there either. I’ll add in all the 401K matches and the reinvested dividends/interest at the end of the year (oh, and the payments to the 401K loan that I took in March).

Gross Income

Income for the month of October was $116,170 vs. $32,342 in September. On a cumulative basis, we have earned $560,308 through October of 2019.

Well, I completely flipped my decision to defer further compensation from the business until 2020. That was driven by the tax strategy I mentioned above because at the end of the day I was only trying to reduce my tax liability for this year by deferring the income. And since my goal is to only increase my income in 2020, my CPA and I decided to recognize as much income as possible in 2019 to use up the $343,000 tax deduction I purchased. The IRS rules say that I can only use up the tax deduction for a maximum of 50% of my AGI, which means my AGI needs to be $686,000 in order to use up all the tax deduction against 2019 income. The good news is if we do fall short the rest will roll over to next year (I believe I actually get 15 years to use it).

Although I’m currently projecting $666,992 in total income for 2019, there is a high possibility to achieve something north of $700,000. I now officially feel like a bonafide sandbagger. Since there are no guarantees, I like to under-promise and over-deliver – psychologically it is very rewarding.

In the second chart above, I also track our income on a trailing twelve months. We recorded a new all-time record in TTM income at $642,237 (up from the TTM of $558,738 last month).

Savings Rate

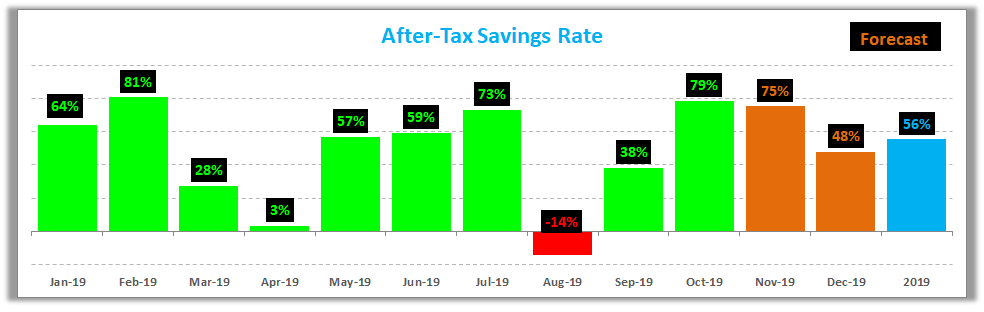

Below is how we actually did towards our goal of saving 50% of our after-tax income. In the chart below, the green bars represent our actual savings rate for the month, the orange bars are what we anticipate based on our 2019 budget, and the blue bar is the projected savings rate for all of 2019.

Our savings rate jumped to almost 80% in October. And some may be scratching their heads wondering how it’s possible when I just wrote a check for $68,600 for that tax deduction I can’t seem to stop talking about. However, the reason you don’t see a huge hit to the savings rate is because my reported savings rate is based on an estimated amount of taxes and not the actual taxes paid. I don’t actually plug in the taxes I pay every month since I do a lot of management with my withholdings throughout the year. My calculations are always conservative (in that I over-estimate my tax obligation) and so I have used this opportunity to true up the calculation based on the work I’ve done with my CPA.

Do you want to calculate your own savings rate? I’ve made it super easy for you with the savings rate calculator included in the free GYFG FI Toolkit that you can download instantly by clicking the link below. Here’s a peek. Did I mention it’s free? You have nothing to lose and everything to gain, Freedom Fighter! Remember, what gets measured gets managed.

Speaking of savings rate, go check out my post where I mathematically prove the importance of your savings rate as a higher priority in achieving financial independence than your compound return. If you’re trying to build wealth quickly, then you have to read this post.

Closing Thoughts

Since returning from vacation, I’ve been moving at a much slower pace on the business front, and that is by design. My goal was to push as hard as I could until October and then to coast through the end of the year in order to enjoy the holidays and make space for some strategic planning and tackling a few strategic initiatives that will help me scale further in 2020. I’m looking forward to a slower November and December. I can’t wait to work on my 2020 goals during Thanksgiving week – like I do every year!

– Gen Y Finance Guy

p.s. Personal Capital now offers a 1.55% high yield savings account that is FDIC insured.

10 Responses

Another killer month. Not many people go the conservation easement route, so it’s interesting to see someone doing it and talking about it. I’m glad it worked and it’s something that I expect to make use of myself down the line when it’s appropriate. Have you considered a Donor Advised Fund as another option to reduce taxable income?

Whole life policies get a lot of hate, but they make sense for very specific situations if you know what you’re doing and the agent isn’t trying to take advantage of you. Any chance you can post the details of the math on it along with the fees and all that?

Hey Kevin – The conservation easement is only something I learned about recently from my CPA. I wish I knew about it sooner. It makes a lot of sense for high earners that only have W-2 income. It’s a win/win, you get to save money on taxes, and you conserve some land in the process to help people save the places (natural beauty) from being over-developed. The added cherry on the top is that the net tax savings are much larger than the donation itself (mind-blowing to me). I think it’s not talked about much for three reasons:

(1) It’s really an option that makes sense for high-income earners – the lower one’s income the less favorable the economics are.

(2) As I was doing my research it seems to be a little controversy over whether this should be allowed or not. But the tax law is very clear that this is very very legal. Maybe people feel ashamed to talk about it if they are using this strategy.

(3) Many people probably have no idea this exists. I had done my own taxes all my professional life until starting a business and engaging a CPA. I now wish I had done this much sooner. I’ve spent $300 in consulting fees and my CPA has already saved me six-figures in taxes. And he has made very valuable connections in the process.

Re: Whole Life Policy. Yes, I do plan to eventually write about this. The short story is that the fees are hidden in the premiums and this policy will take about seven years before the cash value is equal to the premiums paid.

Cheers,

Dom

One thing I’ve never actually looked into, but now I’m curious about, is whether this conservation easement strategy can be used to offset the “income” created by doing a Roth conversion on your retirement funds if you retire early and want to get everything converted to Roth to avoid RMDs. Everyone tries to do the conversion up to the top of the 12% tax bracket each year, but that may not be enough for larger balances. I know things like cost segregation studies with real estate can be used to offset the income, provided your W-2 income is below $150,000 per year or you are qualified as a real estate professional. Did you run across anything about this when talking to your accountant? I don’t know if there’s a restriction on the type of income you can write it off against, but retirement account withdrawals and Roth conversions are technically income

The only restriction is that you can only apply the tax deduction on up to 50% of your AGI.

The economics of the deal are better the higher your marginal tax rate. It would make sense every tax bracket. For example, if you are in the 12% tax bracket, a $10,000 donation with a 5X benefit of $50,000 would only save you $6,000 – so it doesn’t pencil.

Dom

Well if it’s based on AGI, then the answer to my question is yes. You could use a conservation easement to offset the tax generated by a Roth conversion. I know it works out better the higher your income.

Basically in the scenario I was asking about, you could do a conversion of $181,900 (in 2019 while married filing jointly), subtract the $24k standard deduction (for simplicity), leaving $157,900 left for AGI. Split that in half with the conservation easement, leaving you $78,950. That’s the very top of the 12% bracket, so you’d pay a total of $9,086 in federal tax (4.995% of $181,900) to convert from traditional to Roth. This is assuming you have no other income at all.

I read that you chose a whole life policy vs 529 plan. My understanding is that 529 withdrawals for qualified education expenses are not taxed, while cashing in a whole life policy may result in taxable income for your child (albeit at his marginal tax rate). Combined with the expenses of a whole life policy, I am curious how you analyzed this. I have both for my kids… Thanks!!

Hi Scott,

I’ll be honest, I didn’t actually do a lot of number crunching. I chose it over the 529 plan because it gives more flexibility if you choose to use the funds for something other than college. There is also a strategy to use the policy’s cash value and never trigger a taxable event. The premiums can be pulled tax-free because they went in post-tax. However, I want to teach my son when he is ready, how he could “be his own bank” by borrowing cheap money from himself to finance major purchases like a house or car or funding a business. I don’t know what school will look like in 18 years, nor do I know if my son will want to travel the traditional/conventional route.

When our son is old enough, he will become an employee in my business, so that we can start a Roth IRA for him as well. Another pot to pull from.

Dom

Love the update! As a 23 year old seeing these sort of numbers and moves is extremely motivating. In fact it was details of your journey that helped push me to switch jobs which resulted in my compensation going from ~$70k to ~$95k. I’m hungry for growth in all aspects of life and I love your philosophy. Enjoy the easier months of this year as you prepare to break out in 2020!

Hey Keenan – thanks for the comment. I’m always stoked when I hear someone got motivated and inspired by my story and transparency here on the blog. We should all be learning from each other so we can all push each other to be the best we can be. Congrats on the job swap and the increase in compensation. You are already ahead of me at your age from an earning standpoint. I didn’t start earning $95K until I was 27. Keep that momentum up and you are going to be in a nice spot.

Just remember that it doesn’t happen overnight. Keep killing it!!!

Dom

The income from your business is insane. With that kind of engine driving your net worth, you’ll hit the $10M number in no time.