May was the first month that has felt “normal” in a long time. I mean…I got to take my son to see his first movie at a theater. The GYFG family is definitely ready for some fun in the sun this summer. Although it’s not yet officially summer as I type, it’s only 23 days away, so we decided we would start the party early. We are gearing up for an epic summer retreat with my business partners (who also are our long-time friends) with our families to celebrate our continued success. Let’s be honest, the retreat gives us an excuse to have a good time on the company dime!

We will be hosting 11 adults, five kids between two and three years old, and two dogs at the amazing property in the YouTube video below. I’ve booked a private chef to prepare a four-course adults-only dinner one night after the kids go down for bed. Another night we have teppanyaki chefs coming to provide us dinner and a show that will be fun for the whole family! We will also be cooking many of our own meals since everyone in this group loves to cook (and eat). You better believe that we will be spending hours in the pool and on those amazing water slides…let alone all the other activities available on the five-acre property. Stoked!!!

The summer retreat will have completed by the time this article is published. A couple of weeks later it will be Father’s Day and we have booked The Montage Hotel in Laguna Beach for a nice weekend getaway. We have eaten at the restaurant and been to their amazing spa but this will be our first time as guests. This has been on our list of places to stay for at least the last five years. The views of the Pacific Ocean are stunning from this amazing property. They even have a kids camp where we plan to drop our son off for half the day so mommy and daddy can get pampered at the spa.

With all the talk of inflation in the news, we thought we ought to do our part by letting some lifestyle inflation creep in. We also have to do our part to help stimulate the hospitality industry after 14 months of forced hibernation. And as if all the aforementioned wasn’t enough recreation, Mrs. GYFG and I were able to secure a sitter for our son in July to escape for a Babymoon weekend at the amazing Rancho Valencia Resort – a 5-star resort (is this real life?).

Needless to say, we will be ruined after such a luxurious summer. We are about to embark into some dangerous territory and release some serious pent-up demand. We’ve deferred many of these luxury experiences and purchases for the better part of a decade now, as the trade necessary for achieving financial independence early in life. However, we have always known that we desired to enjoy the finer things in life eventually and planned to make them a possibility.

You may notice a new theme in this post (and future posts), which is that we are loosening up the purse strings to enjoy the money we have and continue to work so hard for. That doesn’t mean we are throwing all financial discipline out the window. In reality, our income has grown to a level that allows us to save far in excess of our 50% after-tax savings goal. In fact, last year, we spent less than 20% of our after-tax income. We are not necessarily trying to spend up to that 50% target, but rather use some of that delta to continue to live well and give well. The meaning of “live well and give well” has evolved and will continue to evolve as we grow through different stages of life as we should.

There are two other items of note:

(1) We finally got the new appliances we ordered last December and we plan to start the kitchen remodel in our new house sometime in the next 4-6 weeks. That said, we had originally planned to start this back in early March, so this means that our timeline to move into the new house has moved back to January of 2022, mostly because we don’t want to live in a construction zone. We already have a hectic life with both Mrs. GYFG and me running our own businesses, taking care of a 2.5-year-old, and expecting a baby girl in a couple of months. The real estate market is hot and if it stays that way into early next year, it may also prove to be beneficial when we eventually list our current house for sale.

(2) We think we may have found our nanny for when baby #2 arrives. We know we are going to need help, especially since Mrs. GYFG has taken over the family business, something she wasn’t sure she wanted to do but has decided to give a try. She doesn’t see herself as a full-time stay-at-home mom and wants to have both her professional life and motherhood at the same time. I support her 100% in whatever her choice is.

With that, let’s dive into the financial update, and go through the details of what allows the GYFG family to live well and give well.

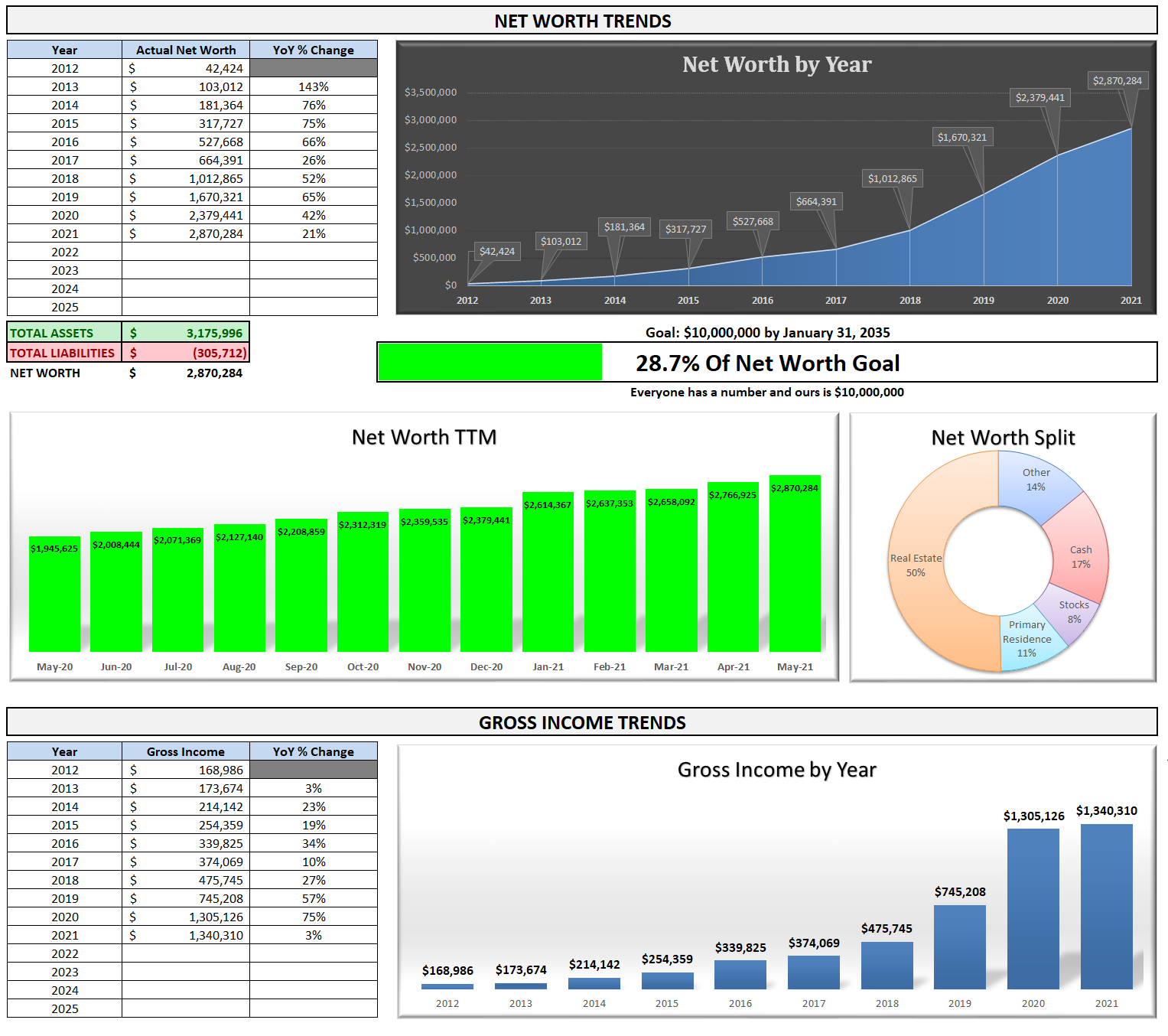

Financial Dashboard

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, six years later, at 28.7% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust 28.7% CAGR. Even more mind-blowing is that our net worth has been compounding at a 76.5% CAGR during that same time period.

Note: I’ve finally got the confidence to forecast an income in 2021 that will be higher than what we earned in 2020. That is even after accounting for the large $415,000 capital gain we had in February of 2020. A large part of this increase is coming from Mrs. GYFG who is absolutely killing it in Real Estate. The other is based on a little more visibility that I’ve gained in the performance of my business through the end of the year. Nothing is guaranteed but I have a strong level of confidence that we can hit this forecast income figure.

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. After falling off a cliff in February we continue to climb towards our previous peak in January of 2021. It’s going to take us the rest of the year to get anywhere close to that previous high, but now that we are on track to match our income for the calendar year 2020, it’s time to find another $150K to make a new TTM high (I’ve got a few tricks up the sleeve that I’m working on to do just that).

Based on how both of our businesses are performing I expect to narrow the gap by about $200K between the all-time-high set in January by end of July – maybe even more.

Net Worth

Current Net Worth: $2,870,284 (up $490,843 or +20.6% for 2021)

Previous month: $2,766,925

Difference: +$103,359

A fairly large portion of our net worth only gets re-valued periodically and I currently think our net worth is understated, which means we will periodically have large and lumpy changes to it.

Note: I’m still not holding a value for my business in my net worth. Depending on the multiple you use, the value of my business is somewhere in the range of $920,000 (1X EBITDA) to $9,200,000 (10X EBITDA). You’ll notice that I’ve moved the upper range of this shadow valuation to 10X from the previous 5X. Internally we still value the company at the conservative 5X, but the longer we sustain our triple-digit growth profile the higher the potential multiple, especially paired with our robust profitability. I’m hesitant to hold a value in my net worth for this until we achieve a liquidity event. That being said, below I’m going to start holding a “Potential Net Worth” figure as I think we will likely achieve a liquidity event in the next 12-18 months.

Potential Net Worth: $5,630,284

^This values the business at 5X EBITDA implying a value of $4.1M in total Economic Value (EV). I then multiplied the EV by my fully diluted ownership stake of 60%, which potentially adds $2,760,000 to our net worth.

Net Worth Break Down:

Real Estate (50%) – This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (11%) – I decided to split this out on its own because it is something I do want to manage separately from our overall holdings in Real Estate. Our primary residence currently makes up 11% of our total net worth (down from 23% in September 2020) due to a cash-out refinance (locking in 2.8675% for 30 years) that put a mortgage back on the property. I expect the concentration to continue its downward trend until we move into our new house in January of 2022.

Net Cash (17%) – We currently have $506,000 in cash vs. $498,000 last month.

Alternatives (14%) – This is a catch-all category that captures our investments in the following: life settlements, a special purpose acquisition company (SPAC), a private investment in the Robinhood trading platform, Bitcoin, and the newest addition of Bowery Farming – a vertical farming company that recently closed a $300M in a Series C funding round that I was lucky enough to participate in.

Stocks (8%) – Our 401K accounts are maxed out and we don’t have any new investment planned here for the year. The only thing that could tick this up is when we get the shares from a SPAC that we participated in that currently sits in the alternatives bucket above.

Total Capital Deployed in 2021:

This month we invested $50,000 into the Bowery Farming Series C raise as well as $37,059 into purchasing additional Bitcoin after it fell more than 50% off its recent high of ~$68,000. I also committed $50,000 to a new Industrial Real Estate deal that will be funded in June.

There are a number of liquidity events that I’m expecting later this year:

(1) $75,000 hard money loan at 10%. The original loan was for $150,000 and was made back in November of 2019. Half of it was paid back six months ago and I expect the remainder sometime in the next couple of months as the last property securing the loan is currently being listed for sale.

(2) Robinhood Investment. I invested in a round led by Sequoia Capital at a $8.3B valuation back in July of 2020. The last round they raised in August 2020 was at an 11.2B valuation. They announced that they would be filing for an IPO in 2021 and some of the chatter is that it could go public at a $40B valuation. I’m not going to make F-U Money but my $10,000 could turn into $40,000+. Only time will tell.

(3) Life Settlement Policies. I invested $70,000 across seven policies in late 2017 and early 2018. Four of those policies are now past the expected maturity date. I’ve had to make several capital calls to keep the policy active as the insureds have lived past the expected life spans. If all four policies payout this year, I will receive $59,300 on an original investment of $40,000.

(4) $38,000 in maturing hard money loans made on the PeerStreet platform. The volume has been significantly less since the Pandemic hit and of the new loans being added to the platform, not many have been matching my criteria of a max 60% LTV and 8% interest rate. Therefore, I have been transferring money out of the two accounts with PeerStreet as the notes mature. On top of that, the majority of my remaining notes are in some form of default.

I could see a continued deployment of capital in the range of $25,000 to $50,000 per month for the remainder of the year (mostly real estate and/or alternatives). That said, it also depends on the timing of our remodel and its cash needs, while maintaining a comfortable cash cushion.

Business Spotlight – Monetized Installment Sale

It’s no secret that I started my company with the ultimate goal of achieving a successful and lucrative exit. Every decision I have made has been in anticipation of setting up the company to eventually be bought by a larger company or by private equity. I initially thought that it would take about five years before we were in an attractive enough position to initiate sale discussions. A major theme in my life for the past three and a half decades has been that of accelerating timelines and low and behold the business has not been immune to that theme.

We are only a couple of months into our third year in business and yet we have already had multiple interested parties. We are currently quite far along in a conversation with what I consider to be a very strategic buyer…like we should be receiving a formal valuation and offer any day now. I’ve always been a big believer in having goals but I also believe that you have to be opportunistic. It’s hard to perfect timing so sometimes you have to strike while the iron is hot. I have no idea what their offer will be but they tick the boxes for everything else on my ideal partner list. This isn’t just a buyer who would allow my partners and me to take chips off the table, it’s a partner that would also provide us with jet fuel to take our company that is already growing at triple digits YoY (for its third year now) to potentially 10X its current growth and trajectory.

As is standard practice for me, I’ve been doing my homework to see how we could most optimally structure a deal so that my partners and I maximize our net proceeds from a potential deal. The gains from selling the business will already be at the lower capital gains rates vs. ordinary income (although, if you’ve been keeping up with the news, you will have noted that capital gains are in jeopardy of being increased). However, I wanted to see if there was anything else available that would allow us to reduce and/or defer the taxes from a sale. Enter the Monetized Installment Sale (there are only two companies that do these in the US – here is a link to one of them). This is a beautiful strategy that allows you to defer the taxes on capital gains for 30 years. Yes, 30 years!

You end up receiving 93.5% of the proceeds upfront and you defer the taxes on the capital gain for the next 30 years. You might be wondering where the other 6.5% goes and how is this structured. First, let me explain the high-level mechanics of the transaction. There are four parties involved in the transaction:

(1) A Seller (that would be my partners and me in this example)

(2) A Buyer (the one purchasing our company)

(3) A Intermediary Buyer or Dealer (they are facilitating the transaction)

(4) A 3rd Party Lender

Now for the high-level steps in the transaction:

(1) Instead of selling the company directly to the seller, we sell it to the dealer in an installment sale that is interest-only for 30 years, with a balloon payment due at the end.

(2) The dealer then sells the company to the buyer and the cash goes into an escrow account.

(3) The 3rd party lender provides a non-recourse loan to the seller equal to 93.5% of the purchase price for a 30-year term.

(4) Once the loan proceeds are received by the buyer the funds are released from escrow to the dealer.

Note: technically you could say there is a 5th party and that is the escrow company which handles all the money.

The interest paid by the dealer for the monetized sale exactly offsets the interest charged on the loan from the lender. And the payments are made automatically through an escrow company so the seller is never directly receiving the interest payments from the sale nor making the interest payments on the loan. Now that you know who is involved let’s cover where the 6.5% fee goes:

- 1% goes to the lender for the loan origination

- 5% goes to the dealer for facilitating the entire transaction

- 0.5% goes to the escrow company for facilitating the collection and payment of interest for the 30-year period.

Link to Executive 2-page Strategy Summary

You don’t get out of the capital gain but three decades of tax deferral for uninterrupted compounding would be a very magical thing. Of course, you risk capital gains rates being higher in the future but I still think the benefits outweigh that risk. Plus, there is a possibility to roll the gains into another 30-year term as long as you do it before maturity. Again, the risk of that is that the tax law may have changed by then, preventing another 30-year term.

This works similarly to a 1031 exchange but it’s superior in my opinion and you can actually use this same strategy for selling real estate instead of the 1031 exchange.

Have you ever heard of this strategy? Do you have experience with executing this strategy?

Closing Thoughts

That’s a wrap!

I’m very much looking forward to a busy but fun summer. It’s exciting to know that over the next month or two we will officially be hitting our financial independence number of $3M and we have plenty planned to celebrate this HUGE milestone. As far as continued wealth building, we will just keep stoking the FIRE with additional savings and deployments and maybe we might have some BIG liquidity event on the horizon that will propel us closer to our ultimate Financial Freedom goal of $10M.

Onward & Upward!

– Gen Y Finance Guy

14 Responses

Man, that estate looks incredible! Super stoked for you as you explore your business exit options. That’s a fascinating idea to do a monetized installment sale. I wish I had realized there were options like that when I sold. Stay blessed, my friend!

Thanks, Michael! The house was amazing and the retreat was EPIC! We do have our first offer in and expect 2-3 others to sprinkle in this month before making a decision.

Take a look at section 1202 of the tax code. Your business likely fits the criteria which would allow you to exclude $10mm of cap gains per owner all together without any extra steps or fees. You’d have to hold your business for 5 years for sure at least though.

Hey Paul,

Thanks for the comment. We did come across that code and found it interesting but we don’t meet two of the criteria:

1. you have held the stock for at least five years,

2. the stock was issued after August 10, 1993,

3. the stock was issued by a domestic C corporation, with a max of $50 million of gross assets when the stock was issued,

4. the company uses at least 80% of its assets in an active trade or business, and

5. you are a non-corporate taxpayer.

Source: https://www.brownadvisory.com/us/theadvisory/qsbs-tax-exemption-valuable-benefit-startup-founders-and-builders

Unfortunately, we don’t meet two of the criteria.

1. We have only been in business for 2 years and a couple of months vs. the 5 years requirement.

3. We are not a C-Corp, we are an S-Corp.

Ah got it… bummer! You could always move to Puerto Rico! That’s a great solution other than having to live on a little island haha. Best of luck getting a solid valuation for the exit -> you’ve created one heck of a cash flow stream in just 2 years by the way. After your exit you might want to reach out to a few PE firms to talk about operating partner roles. Being able to ramp businesses like that is a very in demand skill set across the industry.

Hey Paul,

You joke, but I have looked at Puerto Rico. If we weren’t so tied to California with our friends and family it would be a viable option.

That said, I did recently read an article about the IRS cracking down on people supposedly establishing residency for the tax savings.

Are you in PE? I’m curious what your background is based on your last couple comments.

Dom

It’s great to see life is actually starting to get back to normal and that we can actually go out and start doing stuff again.

Great update. I love the fact that you guys are loosening the purse and spending more than before to enjoy the money that you guys made. This past year, I feel like I slaved away saving so much money (the reason is due to the lockdown, not because I wanted to save money) and I can’t wait to unleash the pent up demand in another couple of months!

David,

Any big plans on the Horizon? How do you plan to release that pent up demand?

Dom

I am probably going to release my pent up demand by traveling more. More than likely internationally but more domestic travel before moving up to international.

I’ve been itching to visit Las Vegas again, that is my playing ground!

Dom I am marveling at your progress and forecast! Two things especially have me SOOOO jealous!:-) Your cash-on-hand to take advantage of opportunities that may present themselves, and your business valuation. I think you mentioned some years back about your ‘X Factor’ and I didn’t get it, then. But I sure do now! Your summer is shaping up very nicely, and glad you all will have time for fun (along with all the responsibilities you are shouldering). Thanks for sharing your climb with us!

Hey JayCeezy,

I just read your guest post on Financially Alert – great hacks!

Interesting to see you go 12% of NW into Crypto and would love to know your thought process and how you landed at that level of allocation. Are you in more than BTC?

Re: Jealousy

Yes, we have had a very consistent and robust cash flow, which has allowed us to deploy $50-$100K a month and still maintain about $500K in dry powder. It’s pretty nutty when I look back at where we were when you and I first crossed paths back in early 2015.

The Business Valuation is nice on paper but will be even better when realized. We did receive our first offer that validated the 5X multiple but we think we are worth more. We went from $430K in 2019, to $1.5M in 2020, and are currently tracking to $3.2M+ in revenue. That king of growth paired with 40%+ per-tax profit margins as we grow.

Thanks, Dom! I’m a big fan of ‘hacks’ and a book you recommended (and I greatly enjoyed!) by Tim Ferriss, Tools of Titans, included many great hacks I use, best of them was ‘weighted blanket’ for sleep.

The decision to move into the Crypto space happened within a few months, after looking into it for a few years. Long story short, there are some drastic changes being implemented in the financial system that are destroying currency value. With interest rates at ZIRP for 13 years, there are no longer possibilities for ‘rate normalization.’ With 5% y-o-y inflation (search it, and blow your mind!) appearing as a response to permanent structural increases to government spending, what had been safe acceptable returns are now clearly negative. Biflation is now gone!:-) Equities can no longer be valued with traditional fundamental metrics, and I liken them to ‘collectibles’ now where art, baseball cards, fine wine, NFTs and comic books are traded between Boomers and Pension funds; the value is whatever somebody else will pay. Have you heard about the $18,000 ‘invisible statue’? Just what it sounds like. I can’t explain it, and now there is no place else to go.

So. I’m about 50/50 into BTC and ETH. I can take a whack at 12% and have it go to zero, and my life will not change. But! After watching all pretense of fiscal responsibility abandoned by the Federal Reserve and elected officials, who signaled currency will be created in perpetuity to support (mostly government) Pension obligations and banks, it doesn’t seem prudent to expect continued value when the Fed can print unlimited dollars. Crypto is limited at the top for each coin, so the only way to ‘increase supply’ is to create another alt-coin. I picked the top two. And, are events scheduled later this year that will expand users and utilization.

While each dollar has equal value in the market, each dollar has a different value to me personally. The first dollar of my net worth has a much greater value than the last dollar of my net worth. I bought it, took it off the platform with a cold-storage-wallet, and am forgetting it for 10 years. It could be life-changing. Nothing else I’m doing can do that. So, it is a nice ‘maybe.’

P.S. – if you ever did a post on your ‘savings vs. investment return’ I would be very interested to see how that builds to your NW. Have a great and fun family summer!

Hey Dom,

Glad to doscover your blog as I was researching Monetized installment sales on the rec of my tax attorney. Would love to hear your thoughts on Liq Cap Partners vs SCrow (which is the one my attorney rec’d). Check out their thoughts on the recent IRS memorandum last month: https://monetizedinstallmentsale.biz/2021_M453_Ruling.pdf

Hey Jerry,

I think the strategy is very creative and so far seems to have been set up to be defended per the IRS code. Of course the risk is that the code changes to prevent this strategy.

Dom