The end of Q3’2022 was a significant milestone as we collected the third and final payment related to selling a majority share (60%) of the business I founded almost four years ago now. Not only did we hit the one-year anniversary of that transaction but it represents another inflection point in how and when I will work. If you were to study the weekly hours I put in over the last 24 months you would see a slope that was declining as I transitioned from 80-hour work weeks down to 32 – 45 hour work weeks (been here for most of the last 12 months). My love of money is really about the optionality it provides and that is especially true with how I spend my time. I don’t regret the 80-hour work weeks and I actually enjoyed them, so don’t take this the wrong way. I like to work! To be productive! And that isn’t changing any time soon…if ever. That said, starting in October I have officially adjusted my schedule to four days a week (Mon-Thur), but still allowing for up to 40 hours per week of work/productivity time.

For the last decade, I’ve been a big believer that if you’re willing to live and work like most won’t for ten to twenty years (less if you’re extra bright and/or lucky) then you can live like most can’t for the rest of your life. I graduated college in 2008 and work ethic has never been an issue for me. It took 14 years post-college to reach Financial Freedom and make work optional. Our financial success and the lifestyle we now enjoy are merely a result of taking the road less traveled.

One of the early money philosophies that I shared on this blog was the rule of 50/50. This rule states that you save 50% of your after-tax income and spend the remaining 50% guilt-free. First, it is something you grow into, at least it was for us. We had to focus aggressively on growing our income in order to find the balance between the lifestyle we desired and reaching our financial goals. It was simple, balanced, and something that allowed Mrs. GYFG and me to align on all things financial. As we transition into this next chapter of life, and with the money goals taking care of themselves at this point, we are now applying this rule to our time – more on that below.

A few call-outs:

(1) Our strong earnings engine produced almost $1,000,000 in income for the quarter. It was split approximately 70% from the final transaction payment and 30% from other recurring sources.

(2) Our TTM gross income has officially peaked at $4,062,996 and will spend the next 15 months in decline.

(3) Net worth was essentially flat vs. Q2’22, which in this market is a win, especially in the context of knowing that our net worth is still up ~5% YoY.

With that, let’s dive in!

Financial Dashboard

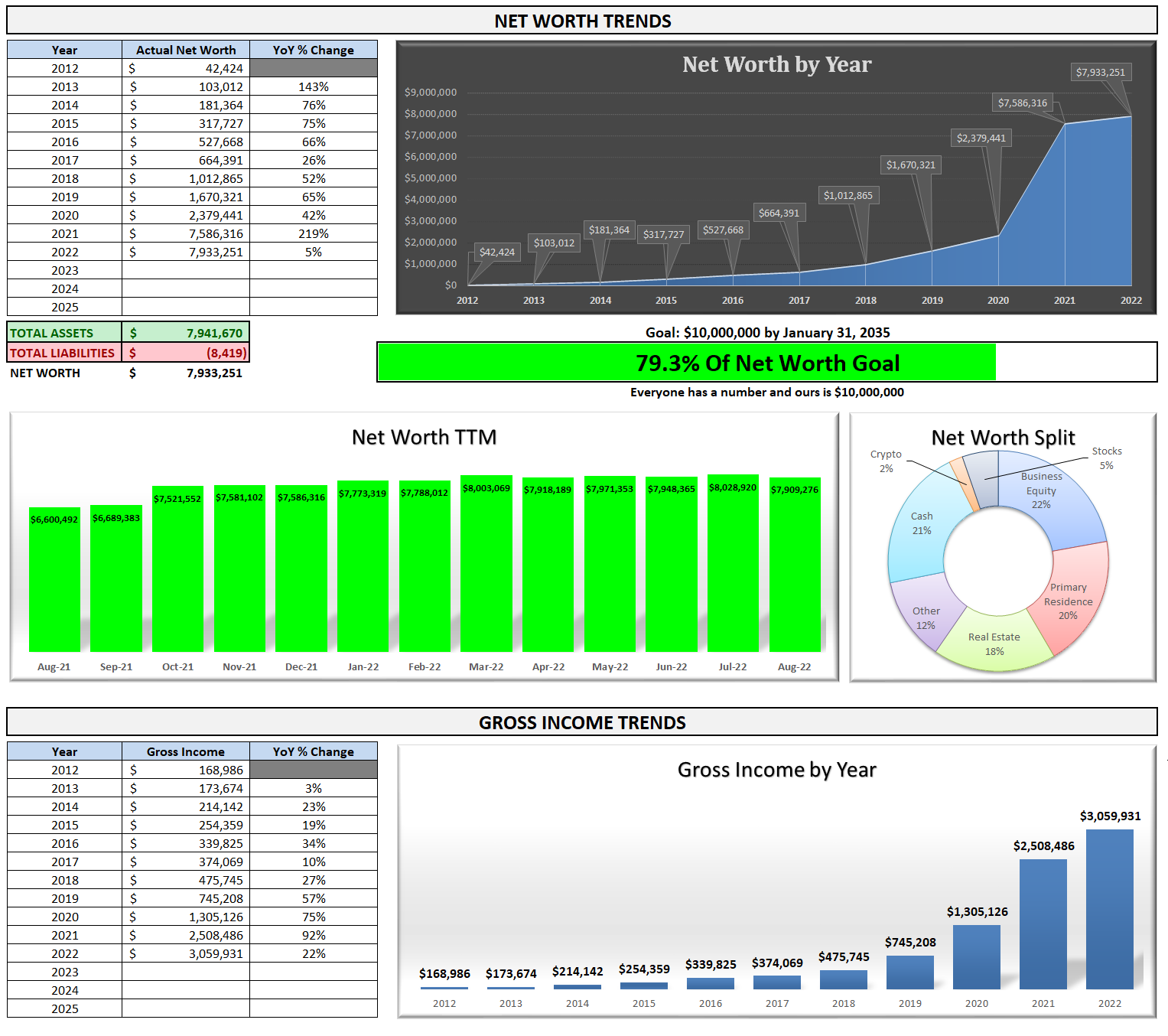

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, seven years later, ~80% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust ~40% CAGR. Even more mind-blowing is that our net worth has been compounding at a ~74% CAGR during that same time period. From the end of 2012 through September 2022, we’ve grown our net worth by 18,600%.

To put that in perspective, our net worth has doubled more than eight times in the last decade! AND 80% of the net worth increases (~$7.9M) between December 2012 and March 2022 have happened in the three years leading up to March 2022, which also happens to align with when I started my business. The magic of owning a business is that you get to quadruple-dip: enjoying a salary, profit distributions, and a more tax-efficient life, while at the same time building equity based on some multiple (on revenue or profits depending on what industry you’re in) of past results (adjusted with some assumptions of future performance in relation to past performance).

For example, let’s say you have a consulting business that generates $1M a year in profits and that you’ve been running it for at least three years. During your tenure of running the business, you paid yourself a $250,000/year salary and you own 100% of the company so you get to reap all the profits every year (ignoring working capital needs for this example). Also to simplify the example let’s assume that from day one that you were generating $1M a year in profits. So, over three years you got to enjoy $750,000 in cumulative compensation in the form of salary and $3M in profit distributions for a total of $3,750,000. That by itself is a pretty sweet deal…but that’s not all of the sweetness. Your business now is established with three years of history and has further value for you to extract. Multiples are all over the place but let’s assume that you find an interested buyer and they are willing to value your business at 5X profit. All of a sudden you now have another $5M if you decide to sell. There are an infinite number of permutations to this example but I think you get the point of how owning a business allows you to at least double-dip…and the importance of setting it up right from the beginning with all these considerations in mind, including a potential exit.

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. As expected we logged one more all-time-high in September at $4,062,996 and are now expecting a gradual decline over the next 15 months. Mrs. GYFG and I were having an interesting conversation about our income expectations for 2023 that would have sounded ridiculous to anyone else listening in…we realized that our income was going to drop 75% from its peak but that we would still likely be able to realize very close to a low seven-figure income in 2023.

Net Worth Conversion

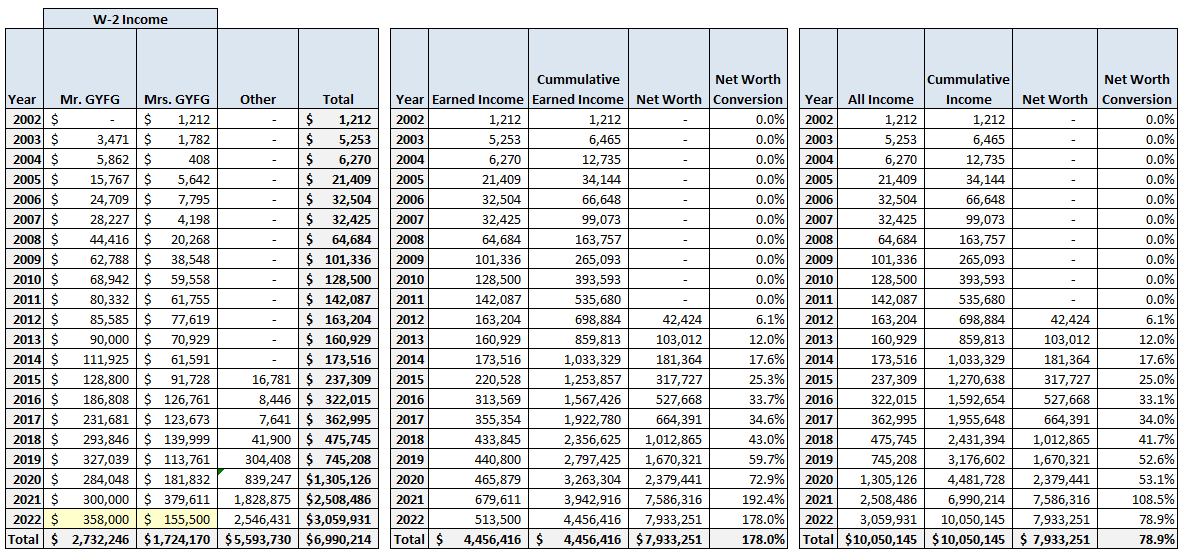

Last year, the big milestone was hitting both Financial Independence and Financial Freedom (see five major milestones). We also hit Financial Nirvana last October, which I defined way back when as the point at which your net worth exceeds your lifetime earned income (see Net Worth Conversion Ratio). You can build wealth either through labor or capital. The goal is to eventually get to a point where labor becomes optional and your capital does all the heavy lifting for you.

I like to look at this metric on both an “Earned Income” and an “All Income” basis. The reason I also like to look at the “All Income” version is to get a sense of both savings and tax efficiency. It’s not perfect but gives you an idea. For example, if you calculate the gap between the two lines for this month it represents a $2.1M delta between “All Income” and “Earned Income,” suggesting that between funding our lifestyle and paying taxes we have spent ~$2.1M (between 2012 and 2022).

Note the gravitational pull our goal of saving 50% (set in 2015) of our after-tax income had on this metric. If you pair the above chart with the actual numbers in the below tables, you can really start to see why a rising income was so magnetic in dramatically lifting the conversion rate between 2015 through 2022. There was not much delta in the early years on the chart between the red and blue lines. That delta started to dramatically increase in 2020 as we began experiencing liquidity events from equity we owned in other people’s businesses and our own. Prior to this we were saving and paying down our mortgage with nominal amounts going into other investments. With the benefit of hindsight, I can also share that our net worth was significantly understated in 2019 through mid-2021 since we were not carrying any value for my business in particular.

Current Net Worth: $7,933,251 (up $346,935 or +4.6% for 2022)

Previous Quarter: $7,948,365

Difference: ($15,114)

Given the latest declines in the market, I’m rather happy that although our net worth was down 0.2% for the quarter it is still up 4.6% for the year (stellar relative performance). So far it has been equities and crypto that have experienced the most painful declines this year. I credit the resiliency in our net worth relative to what has been going on in the market to the following:

(1) Our robust earnings, which have allowed us to offset declines with additional savings. This is supercharged by our extreme focus on tax minimization with our CPA, which requires proactive planning and management all year long – I literally began 2022 tax planning in January of this year and just completed all of my 2021 tax returns in September.

(2) The fact that the majority of our net worth that isn’t cash or stocks only gets re-valued periodically and we fully expect to periodically have large and lumpy changes up or down. To further punctuate this, I have ~$2M in investments that are being held at book value ($3.6M if you include our primary residence).

(3) Our ability to evaluate investments and the market through a risk-mitigation lens first and our willingness to constantly de-risk, even if that means potentially leaving money on the table. I’m a big believer in always leaving money on the table because it doesn’t allow greed to grow roots and it helps keep emotion out of matters where it doesn’t belong.

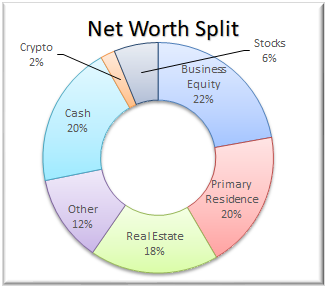

Net Worth Break Down:

For those that missed my last post, I shared a more detailed deep dive into what actually makes up the seven major categories reported below.

Real Estate (18%) – This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (20%) – Since late 2020 we have now plowed $1M of cash into this home and our portion is currently worth ~$1.5M. We expect to spend an additional $200,000 to finish up our list of renovations between this year and next (it’s taking longer than originally expected due to labor shortages and supply chain issues).

Net Cash (20%) – We currently have $1,590,815 in cash vs. $553,947 last quarter-end. This is understated by ~$71,000 of cash currently sitting in our brokerage account and picked up in the stocks category below.

Alternatives/Other (12%) – This is a catch-all category that captures our investments in the following: life settlements, Bowery Farming – a vertical farming company, Private Equity Fund, a Wine Village, and Cannabis-related investments.

Business Equity (22%) – This includes the value of the equity I still own in my business. It also includes the accumulated profits owed to me that have yet to be distributed and show up in a capital account on the balance sheet. The business makes quarterly distributions but only ~50% of the prior quarter’s earnings at the moment.

Crypto (2%) – This is 100% Bitcoin.

Stocks (6%) – This is up 100% vs. Q2’22 at 6% vs. 3%. We will continue to increase this allocation as we move throughout 2022 (the goal is to end 2022 in the range of 5-10% – on the higher end if prices continue to fall).

Note: I’m noticing that I am biased towards investing in illiquid assets and that is because I like the forced discipline they bring to the table. I continue to see a lack of liquidity as a benefit, not a bug…as long as you can maintain the right amount of liquidity in terms of monthly cash flow and cash in the bank. It’s funny because in my original $10M blueprint I had projected stocks making up ~60% of net worth, but that obviously isn’t the case as my current allocation is only 10% of that target. I do think the stock allocation will increase over time but I have a hard time seeing it getting anywhere close to 60% at my current vantage point.

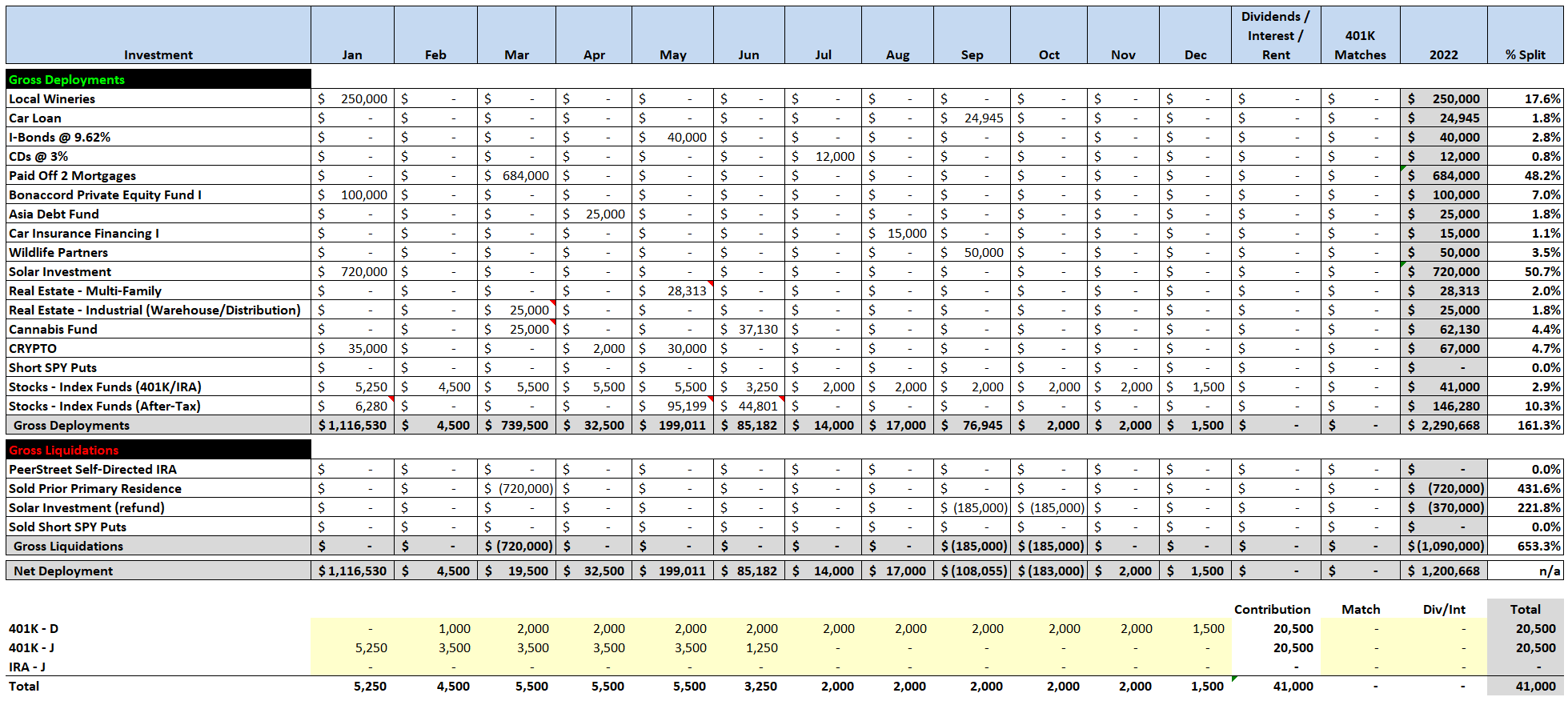

Total Capital Deployed in 2022:

Our net deployments were actually negative for Q3’22 due to the return of capital from an investment made earlier in the year. We had originally invested $720,000 into a solar project that ended up not going through. This ended up being a blessing in disguise. This was mostly done as a part of our tax planning for 2022 and by the time we found out in May that the project was not moving forward we had discovered that from a tax planning standpoint we now only needed to invest $350,000 (we ended up with a large net loss carryforward from 2021 unexpectedly). The good news is that the sponsor I was working with does more than just one deal a year and got us into another deal, which also was sweeter than the original due to the passing of the IRA bill. All that said, we needed to be refunded $370,000, and he asked if he could return half this month and half in October (as reflected in the table above).

Ignoring the $185,000 returned this month (and the same amount will be returned next month for a total of $370,000) we deployed $107,945 into the following:

- $12,000 into CDs to take advantage of the 3.0% interest rate at our credit union. Like the i-bonds deployment last quarter, we deposited a max of $3,000 per person for our family.

- $6,000 into my 401K that won’t be maxed out until year-end. We typically max these out early in the year but due to the market volatility, I extended my contributions through yearend as a hedge of sorts.

- $15,000 into a credit deal (paying 8%) to a Car Insurance company on the YieldStreet platform.

- $50,000 into WildLife Partners. If you are into exotic animals and conservation then check it out.

- $24,945 into a car loan at 4.79% for my brother. I had co-signed for a car loan for my brother as I had done in the past. I’ve been a co-signer for at least five years for my brother and he has been great about making payments. Unfortunately, he has been struggling a bit in getting enough hours to cover his bills and this car (due to the crazy used car market at the time of purchase) was more expensive than he could really afford. So, I decided to pay the loan off and reduce the payment by spreading it out over a longer duration. It helps him out and we created another cash flow stream. We carried over the same interest rate as the original loan.

We have deployed $1,200,668 of the forecasted $1,700,000 that we are projected to deploy for 2022.

Books I’ve Read Over Last 12 Months

- The EOS Life

- Traction

- Rocket Fuel

- No-Dram Discipline

- The Founder and the Force Multiplier

- How Will You Measure Your Life

- The Education of a Value Investor: My Transformative Quest for Wealth, Wisdom, and Enlightenment

- Adventure Capitalist: The Ultimate Road Trip

- The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution

- How to live on 24 hours a day

- Buy This, Not That: How to Spend Your Way to Wealth and Freedom

- Will

- Scam Me If You Can: Simple Strategies to Outsmart Today’s Rip-off Artists

- 75 HARD

- The Wim Hof Method

Reading now:

- Am I Being Too Subtle?: The Adventures of a Business Maverick

- What Got You Here Won’t Get You There

- The Soul of a Chef

In Queue:

- Get a Grip

- The Sovereign Individual

- Good Inside

- Incerto (Deluxe Edition): Fooled by Randomness, The Black Swan, The Bed of Procrustes, Antifragile, Skin in the Game I

- The Oxygen Advantage: Simple, Scientifically Proven Breathing Techniques to Help You Become Healthier, Slimmer, Faster, and Fitter

- Sleights of Mind: What the Neuroscience of Magic Reveals about Our Everyday Deceptions

- Zeckendorf: The autobiography of the man who played a real-life game of Monopoly and won the largest real estate empire in history

Applying the Rule of 50/50 to Time

Mrs. GYFG and I started living by this rule back in 2015 with respect to our financial lives. It was the linchpin to getting us both on the same financial page. It removed all ambiguity in terms of what success looked like financially from the savings perspective. Prior to implementing this rule, we would get into arguments occasionally because I couldn’t articulate how much savings was enough and that really put us both in a scarcity mindset. What it translated to for Mrs. GYFG was that I wouldn’t be happy unless we didn’t spend money when that was furthest from the truth. Implementing this rule not only answered how much we could spend but it allowed for lifestyle inflation – a built-in feature of this rule. It also focused on earning more income rather than spending less money. At the end of the day, it helped us both transition to a mindset of abundance.

I am now ready to apply this same rule to how I split my time between work and personal time. I may have sold a majority share of my business but I am still running it for at least the next four years and still have a few things I’d like to accomplish with the business and my partners. That said, I’ve been working my way into a more balanced approach to how I spend my time. For most of the last twelve months, I have managed to keep my work week to between 32 and 45 hours per week (a little harder to be on the lower end of the range during our busy season that runs May through September). This was a huge reduction from years of 80+ hours per week. I have always been fond of three-day weekends and wished there were more…like every week…and now I’m granting myself my own wish.

One of my goals post-transaction was to transition to a four-day work week. I’ve been preparing for this for the last 12 months by blocking out my calendar on Fridays from 11:30 am on. Effective in October I have officially transitioned to a four-day work week with office hours of 8 am to 6 pm Monday through Thursday. My target is to work only 32 – 35 hours per week but I’m willing to allocate up to 40 hours per week as needed as long as they fit within my office hours during my Monday through Thursday schedule. I need the flexibility because I have just hired our first sales professional and will need to make sure this person gets the support they need from me to be a success in getting this sales initiative off the ground. To this point, I have been the sole revenue producer and I still plan to be involved in sales, but in order to go from a ~$5M to a $10M revenue-generating business, we now need to build a sales team. During the next three to six months I should have also finished transitioning all of the back office stuff to the acquiring company, which has taken longer than expected but we are close.

There are 365 days in a year and if you split them evenly it’s 182.5 days of work and 182.5 days of personal time. That averages out to an average of 3.5 days or about 28 hours per week. So, it won’t be perfectly 50/50 but it will be close especially when you layer in 4-7 weeks of PTO (including company holidays). Let’s say my average work week before PTO is 35 hours per week, which represents 1,820 working hours, and adjusted for seven weeks of PTO (280 hours) leaving me with 1,540 working hours (or an average of 29.6 hours per week).

So where will I spend – or have I been spending – the extra time:

- Reading

- Writing

- Thinking

- Family & Friends

- Health & Fitness

- Travel

- Cooking

- E-Foil Boarding (the hobby I started post-transaction)

- Allocating Capital

- Pool Time (if we can ever get our project finished)

I don’t think of the above list as exhaustive or any one item as mutually exclusive.

Closing Thoughts

We are now moving from summer to fall, which is my favorite time of the year. Not only do we get my favorite holidays but the weather really cools down where we live. I tend to view the summer weather as barely tolerable towards the end (especially without a pool) and the other nine months out of the year as perfect where we live.

I continue to be pleased with how our financial lives are performing and more importantly how they have enabled us to both live well and give well.

Cheers,

– Gen Y Finance Guy

2 Responses

Hey Dom, great update! I’m excited for you to have more time to grow your personal life rather than the professional side dominating your focus. Perhaps we’ll be lucky enough for more frequent blog posts 🙂

I recently have been diving into the effort to electrify homes and thought that some of the resources may be useful for you as you finish up your home renovations. I’ll be installing an induction cooktop and heat pump when I wind up with my own home.

Perhaps some of these resources will interest you!

Rewiring America – Electrify Home Guide:

https://www.rewiringamerica.org/electrify-home-guide

Rewiring America – Inflation Reduction Act Guide: https://www.rewiringamerica.org/IRAguide

Rewiring America – Inflation Reduction Act Savings Calculator: https://www.rewiringamerica.org/app/ira-calculator

Database of State Incentives for Renewables & Efficiency:

https://www.dsireusa.org/

Awesome job with your finances. Nice to have a significant cash cushion to deploy given the market opportunities in listed stocks and crypto.

Really like your application of the 50/50 rule to your time. You know you have arrived financially when you have the ability to determine where you spend your time.