Over the last several months I have written about how I plan to pay off my 30 year mortgage in 7 years and also debunked the whole loss of the tax deduction. In the post about losing out on the tax deduction I presented the math that proved the interest savings over the 7 years was far greater than the loss in the tax savings as a result of lower tax deductions. The math showed that while I lost $10K due to an increased tax bill over the 7 years, the interest savings more than offset that with a total savings of $27K or a net savings of approximately $17K.

In that same post, I briefly addressed why I am doing this vs. investing the extra money in stocks. I won’t repeat that here, but I will admit that I didn’t spend any time covering the opportunity cost of executing such a strategy, or what the performance would look like over a 30 year period. This brought up a good question from one of our readers.

Question from Even Steven:

I’m curious of the numbers over the next 30 years (7 year mortgage payment and 23 investing vs 30 year investing and 30 year mortgage payment). I know it favors the investment just with putting your money in early rather than later in big chunks for the most part.

The Opportunity Cost Over 7 Years

Before we look at the longer term time frame, I thought it would be a worthwhile exercise to look at the shorter 7 year time frame in order to quantify what we are “potentially” missing out on. Are we missing out on anything? Let’s see…

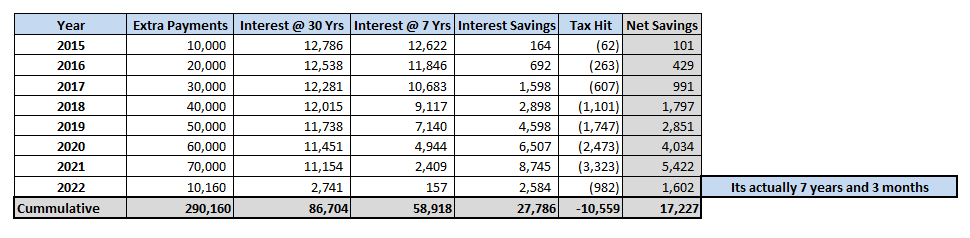

In typical fashion, I turn to Excel in order to help me answer these types of questions. The table below shows you the following starting with column 2 (“Extra Payments”):

- The extra payments made by year over the course of the 7 years (and 3 months).

- The interest based on the original 30 year amortization schedule.

- The actual interest paid during the 7 year accelerated pay down plan.

- The interest savings between the 30 year pay down vs. the 7 year pay down.

- The increased taxes due to a shrinking tax deduction (lower interest = higher taxes).

- And finally the net savings between the interest savings and the increase in taxes of 7 years.

Note: Tax hit is calculated using a 38% effective tax bracket (28% Federal, 10% State).

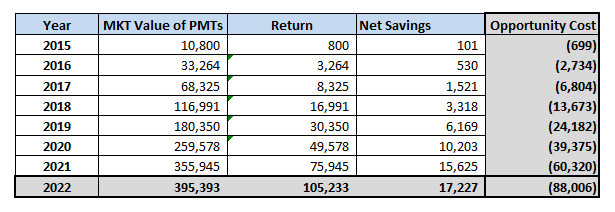

This table essentially summarizes the math I presented in this post. Now let’s build on this and see what that extra $290K over 7 years does when invested into an S&P 500 index fund. Let’s assume the standard 8% that almost everyone uses across the web. And to keep the example simple, we will assume that the money is invested at the beginning of the year (this will make it look a bit better than reality).

Note: The second column (MKT Value of PMTs) in the table above is displaying the cumulative value of the extra payments as if they were invested in the market earning a compounded 8% return. The 3rd column (Return) is the actual cumulative profit you made on investing those extra payments.

So what this table is telling us is that at first glance the opportunity cost of making extra payments on the mortgage vs. investing in the money into an index fund at 8% is costing us $88K (after you net it against net savings calculated in the first table).

Now some people may stop there and come to the conclusion that you’re better off investing the money vs. paying down the mortgage early. Not us! We like to ask the questions that might poke holes in this massively adopted assumption. Before I jump into some of the questions that pop in to my mind, let me first state that the 8% return assumption is based on historical performance and as we all know is “not an indication of future performance” (how many times have you read or heard that one…I am gagging myself for even repeating it here). This is also an assumed rate of return that is based on time frames much longer than 7-years.

Let’s also point out that we are now entering our 7th year of this incredible bull market. The longest run prior to this before a new recession was 10 years. So even if we match that or beat it, in my opinion, we are likely to enter a recession sometime over the next 1-3 years. Typically this could lead to a 20-40% pull back in the market.

And lastly, I will point out once again that this is not a strategy that I recommend in lieu of investing in the markets. Like I have mentioned in previous posts, I look at this as the safe portion of my portfolio where many would be allocating capital to bonds. So that means that during this time I will also be investing in the stock market in parallel with paying down the mortgage early.

Questions that we need to ask ourselves regarding the tables above

- What about any appreciation that occurs on your house?

- I don’t think we should consider that, because that is appreciation you would have received regardless of the accelerated pay down or investing the extra payments in the market.

- What is the break even market return to make the opportunity cost zero?

- Wow, you read my mind…oh wait, these are questions from my own head. Either way, I did the math and calculated the break even return rate. If the market return averages 1.5% over the next 7-years the opportunity cost is zero.

- The 8% is not a guaranteed return. However, the 3.675% I will no longer be paying on my mortgage is essentially a guaranteed return.

- If the market is flat in 7-years then you are $17,000 better off in my personal example.

- What about the psychological win of paying of your mortgage early and the options that it affords you?

- This can be a very personal decision. I don’t know about you, but there are not that many 35 and under folks in my circle of influence that don’t have a mortgage. I think it gives you the courage to make decisions that you could not make when you have to make sure the mortgage is paid.

- What about the savings from the remaining 23 years on the mortgage? What is the present value of that? Shouldn’t that be netted against the opportunity cost?

- Yes, I do think we should at least note the present value of the interest savings over the 23 years. The question is what should the discount rate be? I think we should use the same 8% assumption we used for the market growth. With an approximate savings of $170K over the 23 years, the present value of that figure is about $79K. We won’t net this against the $88K calculated opportunity cost in the above table, but it’s something to keep in mind.

What is the dollar and cents conclusion over the short term?

I can’t argue that if the market returns its historical 8% per year average that I will be missing out on $88,000 in market returns by paying off my mortgage early. I also can’t argue with the fact that I would have $370K in capital tied up in my house once it is fully paid off. Nor will I waste any time trying to convince someone that it is the right move. That’s because this is a personal decision. All I can do is lay out the facts and let others decide what is best for them.

In all honesty, I think that giving up a “potential” (oh, there’s that word again) $88,000 to be mortgage free is worth it. It’s a major goal that will be very liberating both financially and psychologically. The other thing to consider is the increased free cash flow that I will have available to start investing in the market once the mortgage is officially put to bed. If you read the first post where I outlined this strategy you will remember that it’s based on the “pay more tomorrow” framework. Whereby, I plan to increase my income by $10,000/year, and each year I will throw that against the mortgage. So by the end, I will have an extra $70,000/year to invest.

Okay, yes, I will admit that there are taxes that I will have to deal with and we will continue to iron those out as we move forward. Here are a few things we are doing to help on the tax side of the equation:

- Maxing out my 401K at $18,000/year

- Maxing out a IRA at $5,500/year for the wife

- Changing our medical plan to a HSA (we can contribute up to $6,000)

- Set up a SEP IRA for side business activities (up to $55,000 in contributions)

- We will likely be starting a family in the next couple years (so that will help with tax deductions as well)

At the end of the day, I am sticking to the plan and will be at peace with the “potential” loss of $88K.

Now back to Even Steven and the comparison of returns over a 30 year time frame

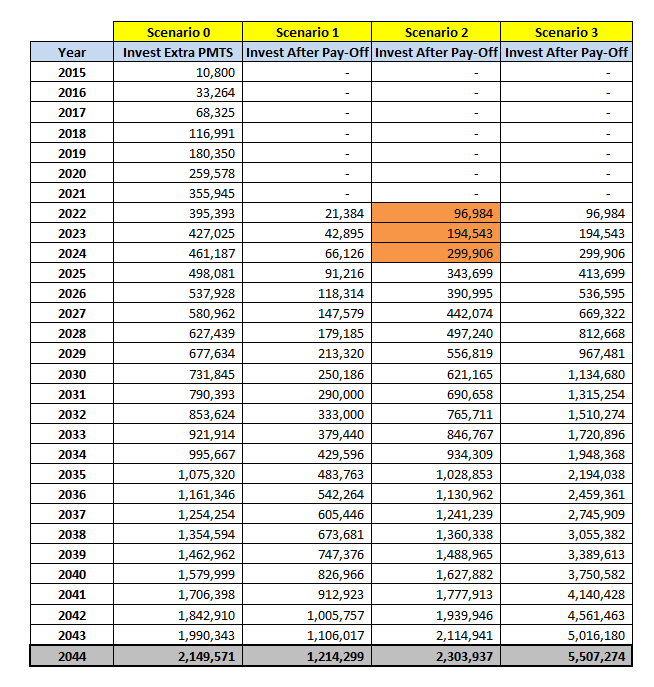

Above, Even Steven wanted to see what it would look like if you invested the extra payments ($290K over 7 years) into the market and left it invested for the full 30 year term compared to paying off the mortgage and then investing.

This is for you Even Steven…

Scenarios Definitions

Scenario 0: In this scenario I would invest the money I had planned to apply to the mortgage in order to pay it off in 7 years. The assumption here is that the money would compound at an 8% annual rate of return. It also assumes that no additional contributions will be made beyond the extra payments that would have otherwise been applied to the mortgage (that totals about $290K).

Scenario 1: In this scenario I pay off the mortgage early and then start investing what used to be my monthly mortgage payment. This is approximately $20,000/year. I think this is the scenario that Even Stevens was suggesting we compare against scenario 0.

Scenario 2: In this scenario I pay off the mortgage early and then start investing what used to be my monthly mortgage payment like in scenario 1. But with a kicker, I make a lump sum contribution of $70,000/year for three years in order to jump start the returns to catch up and eventually beat scenario 0.

Scenario 3: In scenario I do everything exactly the same as scenario 2, except I keep making extra contributions of $70,000/year for the full 30 year period. Which by the way, this would put me at 58 years old.

I personally think I will fall somewhere in between scenario 2 and scenario 3.

Given the math, what would you do? Let us know in the comments below.

– Gen Y Finance Guy

Oh, you’re still reading.

Do you want to help keep our lights on? You’re under no obligation, but if you were already thinking about it or were a little bit curious, why not help us out?

Here are a few ways you can help us out:

- Personal Capital – You know how big I am on tracking my finances, that’s why I totally recommend Personal Capital’s FREE software that helps you see all your financial accounts in one secure and convenient place (checking, savings, investments, and retirement accounts). Without a tool like Personal Capital, these reports would take 2-3 times as long to complete. You want to track your income? Your expenses? How about your Net Worth (who doesn’t like watching that bad boy climb). Just sign up and link your accounts today. Absolutely free to you!

- Amazon – I order just about everything from Amazon. Not only does Amazon have the lowest price, but with Amazon prime I get FREE two-day shipping as well as the following: 1 Million ad FREE songs, FREE instant streaming of thousands of TV shows and movies, FREE unlimited photo storage in the cloud, and FREE books for Kindle. Lets be honest, at some point you actually need to spend money, but you might as well get the best price. Anytime you use this link and make any sort of purchase on Amazon within 24 hours, we will get a very small commission at no additional cost to you.

- Blue Host – Have we inspired you to create your own blog? Well let me save you some money. This is the hosting company that I use for this blog. It is stupid cheap and the customer service is amazing. The normal price is $5.99/month, but if you use this link you will get a 34% discount (only $3.99/month). It took me less than 5 minutes to buy my domain, install wordpress, and get the first version of this site up and running.

OR you can check out our Recommended Products and Resources page.

43 Responses

Good analysis. I’m constantly struggling with this as well – pay debt early or invest the extra. But I still can’t decide so I keep on diving my extra money between the two.

Thanks Money Spot!

Even with this plan I still max out my pre-tax accounts and plan to invest in another piece of real estate sometime in the next 6-12 months and will soon be putting some money back in my Prosper account.

If the market were to puke tomorrow and drop 40% I would definitely redirect funds to more investments in after tax accounts. But until that happens I am just making what I perceive as a better risk/reward trade off with the money I am throwing at the mortgage.

Cheers!

Isn’t is as simple as […] mortgage rate*(1- marginal tax rate) vs investment return rate * (1- tax rate)?

My opinion is starting to evolve a bit on the paying off the mortgage early debate. I see some qualitative benefits to NOT having a mortgage. And I think I am going to throw a couple hundred bucks per month at it, but the bulk will be saving in a taxable account (and investing in equities).

Early in my short career, I sat in a workshop and the presenter asked, “If a company has cash, what can they do with it?” And then he proceeded to write down everything we said [my suggestion was give its employees a bonus]. But the point is, if you have cash, you have decision making power.

So, if one is to invest and then make the decision when they have enough to pay off the mortgage, one could argue [and I do] that is a superior position to be in. You are capturing the upside [with risk] and then you have decision making power. You have the money, and you can decide what you want to do with it.

On the flip side, if you don’t have the $150k or $450k to pay off the mortgage, but have been widdling away at it with everything you have, you can’t make decisions with that money once it goes to pay down the mortgage. The choice was made early on.

Either way, there is risk in the market, but it never has to be just this or that. You can always split it up until you are happy with where the risk is. But, I doubt for someone young and hoping to have a $10MM nest egg one day, that they are completely risk adverse when it comes to this subject.

Hey Elroy,

I think it is as simple as the equation you included, but only when looking at it from a truly academic perspective or at the very least over a much longer time period. 6 years ago I had a radically different opinion about this than I do now. So maybe my opinion is only slightly more evolved than yours and is likely still subject to evolution after writing this response.

First and foremost I look at the extra payments that I am throwing at my mortgage as a bond allocation. So with that in mind I have no exposure to bonds since my mortgage is playing that role for me.

Next this is second on the priority list to maxing out the available pre-tax accounts. So that means $18,000 into the 401K and $5,500 into the IRA for my wife. So I think we are on the same page here.

And I can’t argue that Cash is King. With cash you have options. You bring up a good point about holding onto the cash until you can pay off the mortgage in one lump sum. I have contemplated this, but here is why I am not doing it that way at the moment:

1) The market is at all-time highs and in my opinion the risk/reward favors the downside. And with interest rates near zero percent I would essentially be sitting on way to much cash losing purchasing power. I admit that I might think I am smarter than I actually am, by trying to time the market. The S&P 500 March 2009 low was 666 and the most recent high was put in at 2118 in February 2015. This puts the market at more than 3X is March low and is up over 218% over the 6 year run. If you convert that to a compounded rate over the last 6 years you are looking at a rate of 21.3% per year. And if you believe that the market is mean reverting like I do there is only 2 ways that we get back to a historical rate of return:

A. We have a significant market correction that gives us a lower base to continue compounding from.

B. Or we have years of low returns in the market. If you extrapolate it out to the year 2022 when I plan to have the mortgage paid off. The market would have to lose 2% a year to get the historical rate of return back down to

around 8% (before considering dividends). Now of course it might not normalize over 7 years and could take much longer. However I think technology is actually speeding up these sorts of cycles.

Either way I think there are much better prices ahead. I am patient and not risk-averse, but I also don’t like to overpay for things. Some of the best investors in the world invest when the risk/reward is 5:1. I currently see the inverse risk/reward ration. I completely buy into Warren Buffets rule of buying into weakness, as that gives you a margin of safety to be wrong. It is all just a numbers game to me.

2) I have a 5/5 ARM mortgage that could potentially increase by 2% in 2019 if rates do in fact increase. Since the amortization schedule will reset with 25 years to go I have done the math and I need to pay down the principal by an additional $50,000 on top of the regular payment over the first 5 years of the loan to keep my payment at the same $1,615/month. More of a psychological thing.

My market hypothesis could be completely wrong and stocks could continue marching higher at a high rate of return. This would leave a lot of money on the table. But I would have my mortgage paid off. I also think that it would be offset by faster advancements in my career and thus earnings. If the economy continues to pick up speed my company will continue to grow and it will only get me to where I want to go faster with higher income. I can’t get to where I want to go on saving and investing alone. 40% of my $10M net worth goal is from saving 50% of my income.

Thanks for the insightful comment.

Cheers!

You seem to make a ton of spreadsheets for things. I was wondering if you’d be willing to make them available for download from your website? I think they could be useful to some of us that love number crunching.

Yes Kevin, I spend a lot of time in Excel for the blog and for work.

Brian over at Debtless in Texas is actually doing that very thing on his site. I was going to send him some of my spreadsheets and he is going to make them available on his site.

Some of the things I do are ad-hoc. Others I set up as templates with inputs to make them a bit more dynamic and easy to update.

Any particular spreadsheet graphic from any of my posts you interested in?

Cheers!

Nothing in particular. I love playing with numbers and spreadsheets though, and sometimes by looking at what others have created/how they did it, I can use pieces of it for my own stuff. I’ll take a look at Brian’s site.

Nothing wrong with paying down early, especially since your contributing a lot to stocks in your 401k and IRA. Personally I’ll take the market over my 3.25 fixed 30 year, but there are a lot of great reasons to pay down.

One alternative not mentioned would be to invest the money in to P2P and consider that your bond allocation.

Totally agree Adam. Its not for everyone and is a very personal decision.

Good point on the P2P lending. I actually plan to start dumping some new money into my prosper account that has been largely inactive for the past 2 years while my focus has been on other things. But this will be in addition to paying down the mortgage early.

Cheers!

I think about this every day. So far, I haven’t thrown so much as an extra dime at the mortgage. The money is just too cheap (3.25% at 15 years).

However, the market valuations scare me too. I look at http://www.multpl.com/ every single day. The current P/E is quite lofty.

Just curious, if the market dropped in half tomorrow, would you change your plans?

Trust me Mr. 1500 I have this mental battle daily. It just doesn’t jive with my formal finance training.

Your suppose to invest cheap money, but I don’t like the risk reward. With the S&P 500 sitting at 3X its 2009 March low and 21% compounded rate of return over the past 6 years…I can’t commit new capital to all time highs. I do believe that in the long run the market will always go up, but I also believe the market is mean reverting. And as I outlined above in my long response to Elroy, there are only two ways I see the market reverting back to the mean:

A. We have a significant market correction that gives us a lower base to continue compounding from.

B. Or we have years of low returns in the market.

(see my expanded explanation above in my response back to Elroy)

So for now until A or B or my view changes I will continue on this path.

To specifically answer your question…YES!

I know this sounds sick, but I am happiest on down days. Especially when the S&P 500 is down 20-30 points, because I get excited that maybe this is finally the correction. We will get a 20-40% move lower and I will buy in tiers on the way down.

I was most excited in October of 2014 when the market traded down like 10% at the low, I even put on new positions (which I have since liquidated). I made some nice easy returns but the market bounced back and then some by traded up some 14% in a few weeks.

Also I will point out that because I like to sell into strength I am sitting in almost 50% cash waiting patiently to add new positions.

YES, YES, YES, if the market fell 50% tomorrow I would consider it a gift from the gods. I wouldn’t even worry about averaging in, with a 50% haircut I would invest all my pre-tax idle cash in one lump sum (about $50K right now is sitting in cash). I would also transfer at least $25K from my savings account cash stash into my after-tax account and invest it all.

If I am wrong then I make still make progress, but not as much as I “could have”. But you know there is trouble lurking in the shadows when everyone in your brother is telling you that you have to invest in the market. I have also noticed a huge uptick in credit card offers and credit balance transfers. Maybe its coincidence, but its the exact same thing I saw in 2007. Maybe I am reading into it. Only time will tell.

Cheers!

I vote for A and it probably won’t be long now. The world is a volatile place lately and I’ll bet something comes along to shock the market lower. Perhaps it will be Greece’s exit from the Euro?

In any case, like you, I’d love to see a return to normal valuations so I could invest with confidence. I’d also throw the 40K I have now in bonds back into equities. Come on baby!

Sometimes I almost feel anti-American getting excited for a market crash and none of my friends and family would understand.

Which by the way…what did you end up doing with your Apple stock? Do you liquidate any of your positions? Sell some calls against it?

It’s just long term thinking. If your time horizon is long, of course it’s better to buy low.

I had a trailing stop-loss order that executed, lightening my Apple shares by 175.

Fantastic analysis GYFG…as usual. I am wrestling with upping the mortgage payments significantly, but while investing at the same time. I guess it comes down to personal decision, but I kind of like getting a piece of both pies.

Thanks Brian!

I constantly look at this stuff from different angles to make sure I still like the strategy and think it makes sense. Of course I am still maxing out the pre-tax accounts as a number 1 priority. So kind of want to have my cake and eat it too.

Cheers

GYFG,

Another solid post. I know you are looking at the March 2009 market low as your starting point in your reversion to the mean example, but if you go back to say March 2000, then you have the S&P 500 at 1500. Using a 15 year time frame the the S&P 500 has maybe kept up with inflation and most likely is 4-5% per year below its 100 year mean. I remember shares of GE trading at $60 in 2000 and $6 in 2009. They are currently at $25 and I can’t tell you if the next stop is $24 or $240. I do love mean reversion and many times I use the DJIA Dogs to buy unloved/undervalued companies at part of my overall strategy.

With that said, I paid off my house in 2010 and haven’t looked back or regretted it for one second. There are a lot of opportunities competing for our hard earned capital and it’s difficult to make these decisions during the middle of a multi-year FI battle. Do the best you can and make decisions that will help you sleep at night!

MDP

Thanks MDP!

You bring up a good point, that over the longer term the mean is going to be much different.

Congrats on getting the house paid off. Do you mind if I ask how old you were when you got it paid off in 2010? How long did it take you? And what was the original mortgage amount?

I appreciate the comment.

Cheers!

GYFG,

No problem at all. I bought the house in 1997 for $84,000 at the age of 25. By the way, I live near Houston so obviously housing prices are much lower than other parts of the country. I was either 38 or 39 when I paid it off. The crazy thing is the interest rates for good credit back in 1997 were in the high 7% range. Since then I have been putting all my efforts into building my passive income streams and am currently at about $1300/month. Hopefully within 4 years or so (age 47) I will be able to starting living on a combined dividend and withdrawal income of around $4000 a month. We’ll see.

MDP

Thanks for sharing MDP!

Wow, wish I had a starting mortgage of $84K.

Looking forward to seeing you continue building that pipeline and hit your goal at 47.

Cheers!

At the end of the day it seems like paying off your mortgage early will give you a lot more peace of mind than angst over the gains you may have gotten by investing the extra principal payments. It’s a balance of the spreadsheets and your peace of mind. So somewhere in the middle is usually the best bet I’ve learned!

Exactly FF!

We don’t even have the tax deduction argument. Our mortgage is so low that we don’t itemize.

So I definitely want to pay off the house early. That said, I need to make maxing our retirement accounts the first priority. So I figure that’s what we’ll do in 2016, while raising our monthly mortgage payment $100. In 2017, we can raise the mortgage significantly and really start paying down this thing.

For me, it’s psychological. I’ll feel better not having a debt hanging over us rather than playing a tricky stock market. Sometimes you just have to play to your psychology.

Hey Abigail,

Sounds like you have a plan. I would definitely make it a priority to get those pre-tax accounts maxed out.

Totally understand about not wanting to have the burden of debt. I am not opposed to leverage, but only when I need it and only to a certain point.

Looking forward to hearing your progress.

Cheers!

Right there with you. If this were a bear market I’d just go with whatever has the highest pure ROI. But considering things are how they are, your approach seems spot on. Most importantly, you’ve thought it out and are making the decision your own.

Right on Simon.

I have thought it through and there isn’t a day that goes by that I continue to go through different scenarios in my head. And I am sure this will not be the last post on the top looking at it from different angles.

Next one up will be the benefits of accumulating the cash in savings and paying the mortgage off in a lump sum vs making the extra payments along the way.

Cheers!

I have a strong bias towards accumulating savings because of the liquidity. We never know when a setback is around the corner (job loss, change in health, etc.)

If you face a cash crisis, the mortgage company still wants the next payment – even if you are years ahead of the repayment schedule. It is far easier to manage inevitable life challenges with a comfortable cushion in savings.

You make a great point Kevin!

This is something I think about often and plan to write a post with my thoughts.

But this is definitely a risk in this strategy. With $40K in liquid savings I feel pretty comfortable with that risk.

This is something I am constantly evaluating.

There is certainly a chance in the future that I will stop making the extra payments to the bank and instead just accumulate the money in savings until I can make one lump sum payment. But for now I will stay the course.

Thanks for a great comment.

I paid off my first house in 2004 – it took me five years. For my second house, I bought in 2006 and paid it off in a couple years. The mortgage rate was much higher then and I had no regrets whatsoever. different people have different opinions on this – but I am happy.

That is awesome Div4son. I can only imagine the feeling.

I don’t think I will regret it either.

Cheers!

Great analysis. I always was curious to know what difference it would make between paying off mortgage early vs invest. Of course it would really depends on the market at the time but it helps me see the picture. Maybe balancing out would be a great idea e.g. paying off some mortgage while utilizing tax deferred and free investing tools such as 401K, Roth, TFSA, RRSP.

BSM,

So true that it all depends on the market. I personally think that the market is going to average very meager returns over the next 7 years. Either way I will have a house free and clear.

Also like you mentioned it might be good to balance this out with contributing to tax deferred accounts. That is exactly what I am doing. I am still maxing out my 401K and my wife’s IRA. I also have plans to make other investments utilizing after tax accounts as well.

Cheers!

Great post and great timing. I have been looking the past 2 weeks into speeding up the mortage payment of our house.

In Belgium, the rules a simple: there is a house bonus that is tax dedcutible: you can count interest and principal payments to a max og 2280EUR. Then, you get around 40-50pct of that refunded. In my current situation, only my wife has this bonus, thus limiting the tax advantage.

But it is still a sweet deal: from now till the end date of the mortage, we have more advantage than interest to pay. So, why pay the mortage faster?

On the other hand, I am thinking like you: the long term average return of the markt is far lower then where we are today. And I also believe in mean reversal. So, something should happen. What and when: no clue.

Here is my current approach: Fill up each month the tax advantage savings, pay the mortage in a normal way and cash up everything else. By the end of this year, this cash will be used to either lower the outstanding mortage or will be used to profit from the mean reversal. Either way will make me happy.

Reasons to lower the mortage: I will be truely debt free sooner or I will pay less per month (We ca choose this when paying back a lump sum). This will give me more options going forward, and creating options is my final goal: have the freedom to choose between alternatives.

Blegger,

I like it…A man with a plan. Sounds like I need to get myself a house bonus 🙂

It sounds like the house bonus is similar to our interest tax deduction here in the states. But from what you write, it sounds like you get a benefit on both the interest and principal paid.

Thanks for sharing!

I have gone back and forth on whether or not to pay my 2.625% 15 year mortgage off early. At this point, I have shifted back to investing more. Given my average size mortgage, I am not far from just taking the standard deduction on my taxes anyway. Right now my plan is to pay it off once I retire in 7 years so that my FI savings can grow in the meantime. Good post!

Nice mortgage rate Vawt!

Sounds like you have a plan. That is awesome that you are planning your retirement in 7 years.

Cheers!

Wow, very detailed post! I struggle with the question of paying off my mortgage entirely or making extra payments and pay it off early. It seems to be a struggle for most bloggers here, but it’s a good problem to have, many people don’t have that option.

I personally want to keep investing every penny I have and not pay off my mortgage for now. For me it’s a question of what I feel comfortable with, and less of a question of hard numbers. I feel more comfortable and secure with having more investments and a mortgage, and now I’m on a roll with getting real estate investments. I know the time will probably come when I will want to slow down and then I think I’d pay off the mortgage. It definitely is a very personal decision, and I guess each person has their own ideas of how the mortgage should be handled.

The diversity of this community is what makes it so interesting.

Thanks for the comment.

Man loving your line of thoughts here! I’d say paying off your mortgage makes sense if you believe it does.. You’ve really made me want to investigate the math behind my own situation & speak with my accountant on the benefits of tax deductions for the interest vs. having it paid off.. Having said that I feel that out here I can have the best of both worlds using an “offset” account.. Not sure if you guys have that in the states?

Hey Jef – I have heard from other readers about an offset account, which is something we don’t have here in the states.

Late to this article but wanted to toss my hat in anyway. I’m a 30 year mortgage guy because I liked the security of a lower payment in the seneriou where work stoppage might happen. But from an investment standpoint, I don’t own bonds. I’m 100% S&P index in the Bogle old school sense and will never change that allocation.

However, in periods when I see historical market highs (like now) I throw my extra investment dollars into my mortgage as I’m guaranteed a 4% return. I treat my mortgage as an investment vehicle when I objectively see the market is in a bubble. No point sinking more money int an overvalued market (I know this brakes the sacred rule about speculation) but as I’ve always argued, bubbles are observable and repeatable. Building the mortgage into an investment strategy to substitute for conservative vehicles like bonds is a great risk mitigation tool.

Hey Ycats – You know what they say “better late than never”…I like your strategy and the historical market highs and bubbly nature of the current market is what got me started on this path of paying off the mortgage early.

I don’t remember the post, but I did state that one of the reasons that I was not to concerned about paying off the mortgage, was that I thought we were going to see either a major market correction or an extended period of lower than historical returns in order to compensate for the above market returns we have experienced in the past 8 years (due to reversion to the mean).

Like you, I also don’t have an allocation to bonds, at these rates I just done see the point. As we pay down the mortgaged at an accelerated rate we do monitor our concentration risk as a percentage of our total net worth, working to keep it at 25% or less, with the longer term goal to get it below 10% of our net worth.

We also continue to max our our 401K, HSA, and other after-tax investments.