Today we have the 8th of a series of interviews. During this series we will be show casing other Freedom Fighters from around the world. I am excited to introduce you to our eighth guest, Kevin Shryock of InspiritFinancial.com. Read Kevin’s awesome story below. And if you would like to be featured in the Freedom Fighter interview series then be sure to check out the Guest Posting page for more information (it’s open to anyone that is willing to share their fight for freedom: Time Freedom, Location Freedom, and Financial Freedom).

Now I will turn it over to Kevin…

I used to think that all you need to become rich is a thrifty mindset and a well-paying job.

Now I know better.

I graduated from high school positioned towards success. I started an engineering degree at the local community college. To pay for it, I worked four jobs, gave myself a $2 per day allowance, rode a bike and stashed up as much cash as possible.

When I left for university, my parents generously provided me with a college fund just large enough to cover the last two years of tuition. I stayed diligent, kept my living expenses low and graduated with my bank account still nicely padded from my first two years of work.

I learned successful strategies to get interviews at any career fair and compare different job offers to find the best ones for me. By the time I graduated from University, I had a steady girlfriend and a great paying job with a big company.

I should have been in the perfect position from which to build wealth.

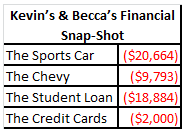

Then I did the least sensible thing I could with all that hard-earned money; I bought a beautiful new Scion FR-S sports car (her name is Zoey, by the way).

Without thinking twice, I wrote the check and walked away with $20,000 of car debt hanging around my once financially blissful life.

Soon, that joyful new car payment and my girlfriend’s student loans, car loans and credit debt began to weigh on us. When we finally combined our debt, it added up to a whopping $52,000!

Money had lost its fun. I knew that our lack of financial knowledge and our many sources of debt would form a rocky foundation for our relationship.

So what does an engi-nerd do best? Research.

I decided that the best strategy to being rich was to do what the rich people did. I found 7 simple steps that I now teach others to follow to guide their journey to financial freedom.

I’m going to outline our journey through the first three of them and show you our exact financial numbers.

(Note: I’ve put together a bonus resource section that you can access free at the end of this post. It walks you step-by-step through every strategy I learned and how you can use it to take control of your money today).

And so it began.

We cut our spending and began budgeting for the first time in our lives. Our first attempts were hard and caused many fights. Date nights went from restaurant outings to Redbox rentals. We even had to pass on a few family events to save on the plane tickets.

For example:

I remember getting invited out by my friends to restaurants and having no money to enjoy a meal. I would sit there with my friends, order a glass of water and leave a two dollar tip because that’s all I could afford.

Yes, my pride took a beating, but those were the sacrifices that needed to be made to dig myself out of the hole I was in.

After 10 painfully cheap months, we were able to pay off every single one of those ridiculous debts.

The biggest battle had been won, but the war wasn’t quite over.

All my research had shown that a true financial foundation needs an emergency fund. So, we pulled together the last of our will and kept up our thrifty lifestyle for 7 more months.

Finally, at the end of the 16th months, we crossed the threshold from crisis to peace.

We were out of the woods with a strong safety net around us. We began to slowly let our foot up off the gas and begin to enjoy all of the income we’d worked so hard to free up.

We increased our money allotted to entertainment and had some truly fabulous date nights. At one of which, I even proposed!

I remember shopping for her engagement ring. I learned all about the 4 c’s of diamonds and shopped with the intention of finding the best ring for the best price (after all, a less better price meant a bigger rock). Without fail, every shop tried to direct me towards their payment plans. But with the money I’d saved up, I just wrote a check. No stress, no worry.

We’ve started saving for bigger goals too, like a house!

We’re not eager to go back into debt, so we’re preparing to write as big a check as possible come moving day. We plan to find a modest home around $100k and move to bigger houses as family and other demands present themselves. At our current rent payment of $1120 per month, we should have our entire mortgage paid off in 7 years; just in time for Becca’s 35th birthday.

Although we’re young, we’re always looking ahead to the next challenge. Money is almost like playing a game now.

Did you know that half of Americans who are old enough to retire have less than $12,000 saved for retirement (Source)? That’s ridiculous.

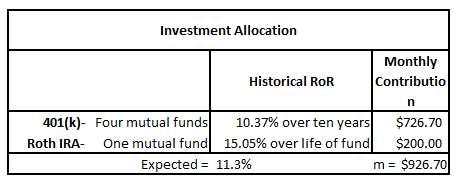

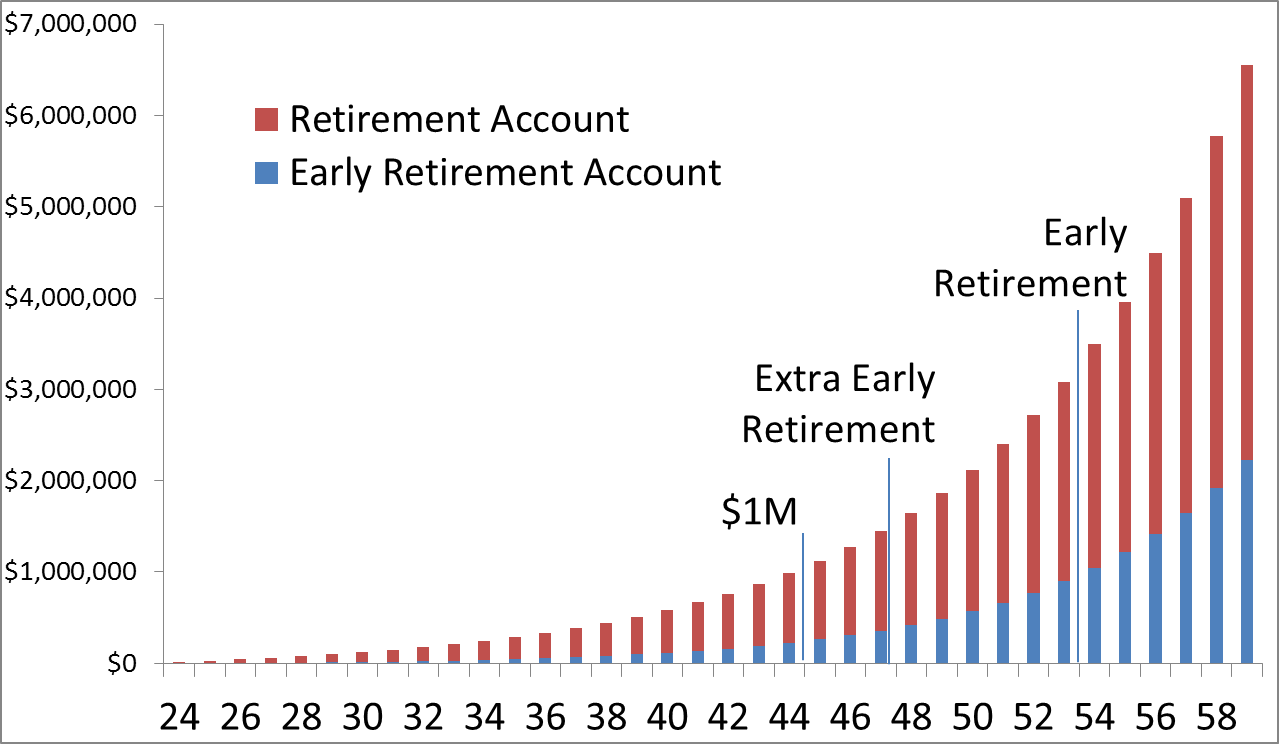

Because we’ve started so early, we’re going to have more than enough at retirement. In fact, we’ve decided to try and retire early by putting some of our savings into side investments. If all goes according to plan, with no house payment, no debt and a healthy nest egg ($1.4M), we could retire as early as my 47th birthday.

But if we choose to work the whole way, a whopping $6.5M could be waiting for us in our golden years.

All we did was choose to follow a plan. We started early, and it’s already paying off.

I founded InSpirit Financial to give out free lessons and provide coaching for others because I believe that a world filled with financial freedom benefits everyone.

Money fights and money problems are the leading cause of divorce in North America today. (Source)

15% of Americans couldn’t cover a $2,000 emergency without going into debt. (Source)

I don’t want that for you. I want you to become rich.

So, I’m giving you several bonus resources to help.

First- I’m putting together a step-by-step guide for how to walk from financial crisis to financial freedom.

Second- I’m sending out weekly money tips that are personalized to the questions you ask about. Each has specific examples and is filled with inspiration.

Third- I’m offering all who sign up a free, one-hour phone call with me to talk about whatever financial questions they have. I’ll personally help you make and implement a plan.

You can access it all here.

Kevin Shryock is the founder of InSpirit Financial. His mission is to empower you to take control of your life and your money. To date, Kevin has helped multiple people pay off debt and establish financial freedom. On his InSpirit Financial Blog, Kevin explains how he does it.

Kevin Shryock is the founder of InSpirit Financial. His mission is to empower you to take control of your life and your money. To date, Kevin has helped multiple people pay off debt and establish financial freedom. On his InSpirit Financial Blog, Kevin explains how he does it.

Favorite Quotes:

“People change their lives when they say I’ve had it!” Les Brow

“Find your voice and inspire others to find theirs,” Stephen Covey

Book Recommendation: 7 Habits of Highly Effective People by Stephen Covey

8 Responses

Congrats on paying off the debts! As a conservative planner myself, I’d be a little wary of the using past returns to estimate your future return of over 11%. Man I hope that’s the case though!

Hey Fervent! Thanks for the kind words!

I completely agree. Assuming the same returns as the past isn’t a sure thing, but it’s the only reliable data anyone has. Past performance is no guarantee of future performance, but it’s a great indicator!

To buffer for this variability, we’re shooting for an early retirement. That way, if we’re off (even by a lot), then we still get to retire on time!

Wow … you are really smart to get that debt paid off *and* start a nest egg. You’re right: most people don’t have nearly enough to retire. I know several people in their 50s who are living hand to mouth because they just can’t get jobs.

What’s even better is that you seem to have started your own business. I’ve always said that being able to get an income without a job is like career insurance. You’ve got it!

Plus you guys deserve a lot of credit for staying together. I hope she liked that ring!

Man, great job accumulating assets.

11% seems to much to me, but I think wise investing is very far from rocket science and, in this view, I believe you will be able to make half of that, surely.

Cheers!

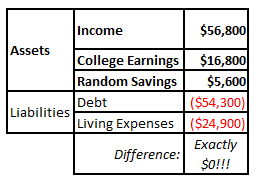

Kevin – Thanks for participating in the Freedom Fighter series. You really crushed that $52,000 worth of debt. I assume the different numbers you provided range from $51,341 to $54,300 because they were taken at different time???

Either way it is impressive that you killed more than $50K in debt in 10 months.

Other Questions:

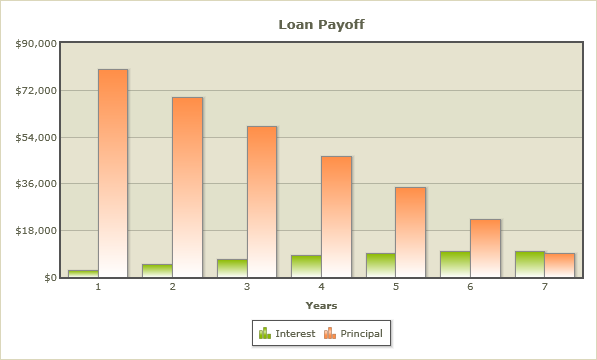

1 – On the Loan Payoff chart, I understand the Orange representing the annual principal reduction. Is the Green the cumulative interest paid over the life of the loan? I know it can’t be the annual interest costs because that would be decreasing with each passing year (not increasing). Just want to clarify for other readers.

2 – Why use the 11.3% vs. a more historical return of 7-8% that is touted? Not a criticism, just curious as to the thought process behind it.

3 – I think too many people forget how important the savings rate to their financial plan is. When I put together my road map to $10M, I realized that 40% of that value will need to come from saving alone. What percent of your fund at either $1.5M (early retirement) or $6.5M (normal retirement) is made up of savings (i.e contributions)?

4 – What kinds of investments are you making with your “extra early retirement account?” And what rate of return are you assuming vs. your 11.3% for your “early retirement account.”

Cheers!

Thanks for sharing your story Kevin! It was nice to get to know your background story. Looking forward to reading more of your updates on your blog.

Nice interview! Debt sure has a sneaky way of creeping up and then slapping us in the face with shock. Great job tackling debt head on and getting your finances back on track!

For me, it is so inspiring to know that you managed to come off from debt in a span of 10 months and building an emergency fund in the next 7. I know of people whose efforts to avert debt have proved to be futile and are in the brink of bankruptcy. congratulations on that successful endeavor and things are definitely looking up for you two in the near future. keep it up!!