They call it the double comma club and membership is open to anyone. Well, it’s open to anyone that is willing to practice simple disciplines of saving, investing, and living below their means. Let me clarify that when I say “living below their means”, I am not saying you have to live like a college student, instead you simply need to spend less than you earn and invest the difference. Ideally you should be saving and investing at least 20% of your income (although I recommend saving 50% as you build your income).

They call it the double comma club and membership is open to anyone. Well, it’s open to anyone that is willing to practice simple disciplines of saving, investing, and living below their means. Let me clarify that when I say “living below their means”, I am not saying you have to live like a college student, instead you simply need to spend less than you earn and invest the difference. Ideally you should be saving and investing at least 20% of your income (although I recommend saving 50% as you build your income).

J. Money over at Budgets are Sexy has started “The Million Dollar Club” for anyone who desires to become a millionaire can join. It started out of his own desire and pursuit of reaching a net worth of $1M dollars. Then in order to add some accountability and support he opened up the club to anyone else that was serious about joining the double comma club.

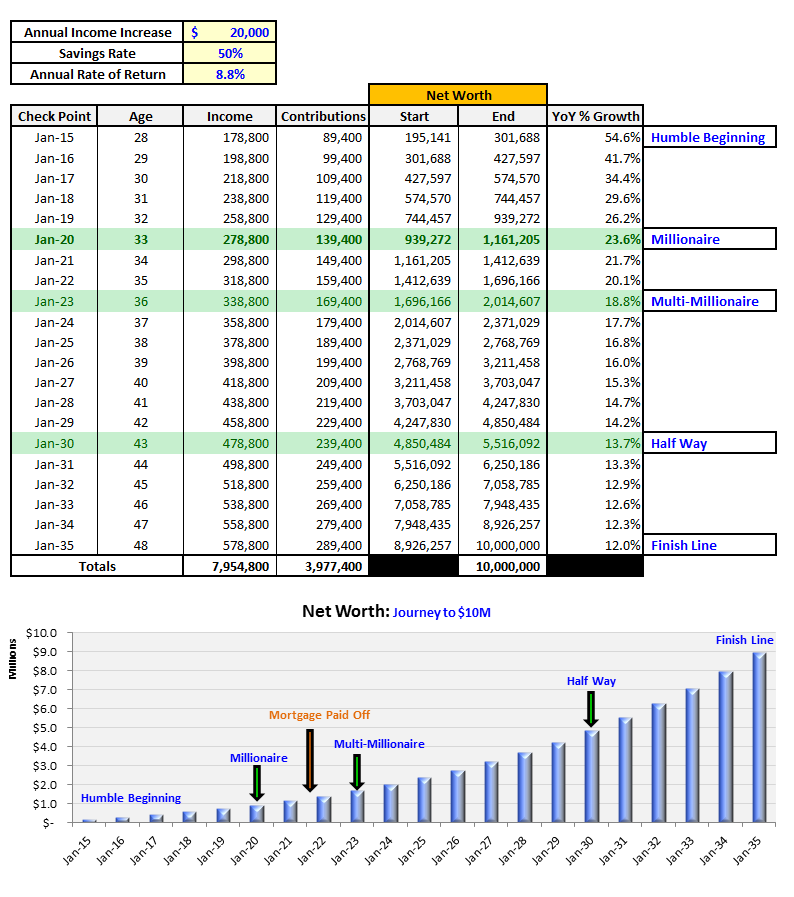

As many of you that have been reading for any length of time, I want to join the Million Dollar Club 10 times over with my goal to reach a net worth of $10M by the time I am 48 (I am 28 now). However, you don’t get to $10M without hitting the $1M milestone along the way. This is my official pledge to become a millionaire.

How to become a millionaire

When you break it down to a few simple practices, it’s really not nearly as hard as so many think to become a millionaire.

Here are the 3 activities that will get me to the all coveted millionaire status (and the can get you there too):

- Max out all pre-tax accounts every year: 401K, IRA, HSA

- Pay off the mortgage, following an accelerated plan.

- Save and invest 50% of our gross income less taxes (inclusive of retirement contributions and extra mortgage payments)

That’s right it’s only 3 simple activities and millionaire status is achievable. The time it takes to reach that status will depends on many different variables, both controllable and uncontrollable. But over long enough time-frame you can join the Million Dollar Club by following these 3 simple disciplines consistently over time. Based on the plan I put together to reach $10M following these simple practices, my estimated initiation into the club will be in January of 2020.

You can go read the detailed plan for the details (linked here), but in the meantime let me share with you the outline of my milestones:

Note: My next check in on my journey to $10M is in January of 2016, where I need to be at $301,688, which based on my current forecast is doable. In fact I am actually forecasting a Net Worth of $305,000 by then. The rate of return has not been anything near 8.8% in 2015 on any of our investments, but we have been on fire with respect to increasing our income.

If you want to follow along I am documenting every step of the way right here on the blog. There is an entire page dedicated to tracking all my financial stats and I publish a detailed financial report each and every month (example here). You will also notice the most current net worth reading in the top right corner of the side bar.

Do you want to join the million dollar club? How do you plan to get there? When do you plan to gain entry into the double comma club? Lastly, are your goals bigger than $1M? I would love to hear from you in the comments below.

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list below or at the top of the page and I will send you a copy.

- Mint.com (free) – Mint is great for setting up budgets and automating the tracking of your actual spending habits vs. the budgets you set.

- PersonalCapital.com (free) – This is like Mint, but is geared towards investments and net worth tracking.

28 Responses

Q: How do you become a millionaire in the stock market?

A: Start with $2 million!

Jokes stick around to become ‘old jokes’ when they are timeless, true, and funny.

Question, GYFG…what is the basis for the 8.8% annual return? This is a very interesting look at the planned path forward, and including your assumptions is very useful. One thought that may be interesting for you to look at, is making a three-outcome range; worst-case, current, and aspirational. Just a guess, but your worst-case will still be awesome! Thanks for taking us along on your journey.

Hey JayCeezy – Love the joke.

Always asking the good questions…

In all honesty the 8.8% is the rate of return I backed into in Excel after I set up my assumptions for income and savings rate over the 20 year period. I do have multiple scenarios run in my spread sheet and the results are not bad as you suggested, but they are not the ones I am aspiring too.

I don’t know if you buy into the law of attraction or not, but I totally believe and have witnessed first hand that the things you focus on become a reality. So, I have chose to focus on the best case scenario, and I plan to do everything I can to get there.

But to circle back to the multiple scenarios. Here are some of the other scenarios that I ran:

1 – At 3% return I still get to $5.5M (all other assumptions held static)

2 – At 5% return with a 35% savings rate and $10,000/year increase to income $3.8M (I would call this base case)

3 – At 3% return with a 30% savings rate and $10,000/year increases to income, I get to $2.7M (worst case)

And you already saw the 4th scenario which is the “best” case that I am using on my financial journey.

As you could imagine there are an unlimited amount of permutations that I could run.

The other thing I would point out is that a target of $10M is really only $5.5M in today’s dollars when you take into account the time value of money and a 3% inflation rate.

Cheers!

GYFG, did not mean to suggest your results will be anything but awesome. Good to know you have multiple scenarios, all have reasonable assumptions, and all will get you where you want to go. One thought on your income/deductions…if your wife can be recategorized as a 1099 contractor (and receive the monetary compensation for benefits in her hourly rate) that might fix your ‘deduction’ concern while eliminating the problem for her family business (it is a bigger deal and expense to set that up, than one might think!) That book on your list, “The Tax Racket”, has some real pearls that might help you with ideas for deductions, or come to peace with the idea of paying the taxes now. Always enjoy your posts and writing, thanks!

Hey JayCeezy – Sorry, I worded that awkwardly. I meant that even in the other scenarios I would be pretty happy with the results (that’s what I meant when I said “not bad like you suggested”).

In all honesty I love your questions because they make me think about things in a deeper way.

We tried to go the route of converting here to a 1099 contractor, but the CPA said that would not work for the escrow company due to certain regulations. Her mom has been wanting to get a plan set up for her employees anyways but has not taken the initiative. So I have officially volunteered to help do the due diligence in getting it set up.

Sounds like I need to order that book sooner rather than later.

Cheers!

Interesting. You chart out your million using math. Math, cold hard numbers are usually reliable. You can also use math in an accelerated method of getting $1 million.

I recently read an article that there are 3 methods the side walk, the slow lane, and the fast lane. Sidewalk being people with jobs who don’t invest and will never make it. Slow lane are people who invest and compound passive income over years, and the fast lane are people who do an equation like this…

$1M /(how much the sell of a product will net you – the cost per acquisition of customer) = number of units of a product you need to sell.

There is nothing wrong with focusing 100% of your finances on the slow and steady wins the race method of hitting the million. In T Harv’s millionaire mind intensive he talks about how rich people have the mental habit of not either or, but both.

Why not do them both them, have the passive thing building then get in the fast lane. The fast lane requires you to learn marketing though.

You’ll want to develop mental habits of a millionaire. Mainly because if your subconscious habits are set to you being comfortable with a certain level of money it will always try and put you back at that amount. Tai Lopez goes over these in depth in his 67 steps program.

If you are a person who’d want to keep his million after you make it, instead of losing it like lottery winners then it makes sense that you click my link and check out Tai Lopez’s 67 steps. – http://www.the67steps.com/

Kendrick – thanks for the recommendation to the 67 steps. I checked out Tai Lopez’s Ted Talk and really enjoyed it.

At your income level, I expect you’re probably phased out of the Roth and income-deductable range of Trad IRA. Do you just backdoor Roth?

Hey Taylor Lee – I am covered at work with a 401K, but my wife is not. This year we are cutting it close with the additional income, but with our deductions we should still be able to get our AGI to $183,000 or below for 2015.

This would still allow us to take the full $5,500 deduction for my wife’s traditional IRA. But we are going to run into a problem next year because based on my new compensation package, we will be phased out from this deduction which happens at an AGI greater than $193,000.

It pisses me off that the IRS rules are written this way. If we were both covered at work we would be fine, but we get penalized for making good money and having one of us not being covered with a work policy.

Here is the link to the IRS table if your interested: http://www.irs.gov/Retirement-Plans/2015-IRA-Deduction-Limits-Effect-of-Modified-AGI-on-Deduction-if-You-Are-NOT-Covered-by-a-Retirement-Plan-at-Work

Cheers!

We need more deductions.

Or what we really need to do is figure out how we can convince my wife’s family business that she works in to get a qualified plan set up so we are not hit with this issue.

The other thing we are looking at doing to increase our deductions is to pick up a third piece of real estate. The optimal situation for us would be to find something that is cash flow positive before depreciation, but then shows a loss on paper for tax purposes.

Non real estate professionals are allowed to pass $25,000 of “paper losses” from real estate through all other forms of income. Anything over this amount will accumulate and carry over from year to year. But this is only if you have an AGI of $100,000 or less. It completely phases out at $150,000. Which means you would only be able to use any paper losses against any gains on a future sale of the property.

However, if you qualify as a real estate professional, this deduction is unlimited and has no income requirement. Luckily for us, my wife qualifies as a real estate professional.

So it is highly beneficial for us to pick up property that shows a loss on paper.

Our income is projected to go up about $50,000 next year, so a property will help, but it will not be enough to offset our increase in income to be able to benefit from a traditional IRA.

That means you just made me realize that I really need to push for a plan to get set up at my wifes office. Need to go and sweet talk my mother in law….AKA the boss lady 🙂

Thanks for the thought provoking comment.

Hi! Love your charts and tables! Maxing out my 401k was one of the first things I did this year before I left my day job. I’m so glad I did. A big part of building wealth is using tax deductions and such to one’s advantage! Uncle Sam isn’t going to actively remind us to do so!

– Sydney

Hey Sydney! Glad you like the charts and tables. I am going to try to start incorporating them more often in all of my writing. It really helps to break up the content.

That’s awesome that you maxed our your 401K before you left the day job. Now that you are out of the corporate world have you set up a SEP IRA or something equivalent? Being self employed you now have a higher contribution limit at $55K a year (but I think the limit is 25% of your income).

Thanks for stopping by!

Welcome to the club! I found this to be a fun exercise when I did it as well. Hopefully you’ll be able to move those dates up as time goes on, as I plan on doing. Cheers!

Thanks FF!

The faster those dates come the better. The question then will be, what do I do next?

Cheers!

Unfortunately with inflation, the millionaire club isn’t even that big of a deal anymore. Like you said, anyone can join it as long as you live frugally and save up. To be considered “rich” I think you need to have at least $10 million in the bank.

Tony – You’re right, a Million is not worth as much as it use to be. However, I would argue that it is still a big mile stone for most.

Good thing I am shooting for $10M, which by your definition would be “rich” 🙂

Cheers!

Love it! That chart is off the chain, haha… I need to make me one of those too 🙂

Going now to list you as a member – welcome aboard, good sir. Thanks for passing on the word!

Thanks J. Money!

Thanks for putting this little club together.

Cheers!

Isn’t it amazing how super duper easy it is to become a millionaire these days? The strategy is actually quite straightforward – save significantly more than you spend, and understand that the stock market has, historically, turned millions of frugal Americans into millionaires.

For the record, we don’t have a money goal – we have a time goal. The end of next year, I’m done – I don’t care how much money we have invested. We will make it work. My wife and I will both retire before we’re millionaires, but by living cheaply (and off of savings entirely for the first year), we’ll realize double-comma status a couple years AFTER retirement, assuming very conservative historic stock market return averages.

And our strategy is very simple – we don’t spend money on crap. We save 70% of our combined income every year. We both completely max out our IRAs (the easiest strategy to take in this business) and simply save the rest in a brokerage account. Works like a charm. It’s simple. It’s straightforward.

Steve – It is absolutely AMAZING how easy it is when you break it down.

Happy for you and your wife and excited to follow your journey living out of an air stream 🙂

Cheers!

Hey GYFG –

I also wrote my plan to reach the Million Dollar Club, just this week, I like how succinct your version is, it makes it look even easier 🙂

I also have a target of 2020, so I guess we’ll ride along a similar path for the next 5 years. Looking forward to follow your progress!

Nick

Hey Nick – Looks like great minds think alike 🙂

I will head over and check yours out. Glad to have a accountability partner on the way up.

Cheers!