GYFG here checking in for the January monthly financial report. If you have been reading these reports for a while you will notice that I introduce each month with the same intro month after month. I do this for two reasons, a) for the newbies to the site (which make up about 50% of the sites traffic) and b) to remind everyone what these reports are all about. By all means if you have read the intro at least once, then please feel free to skip down to the “Summary of January 2016” section where the new content begins (click the orange link to be taken there automatically).

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgence of your choice.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

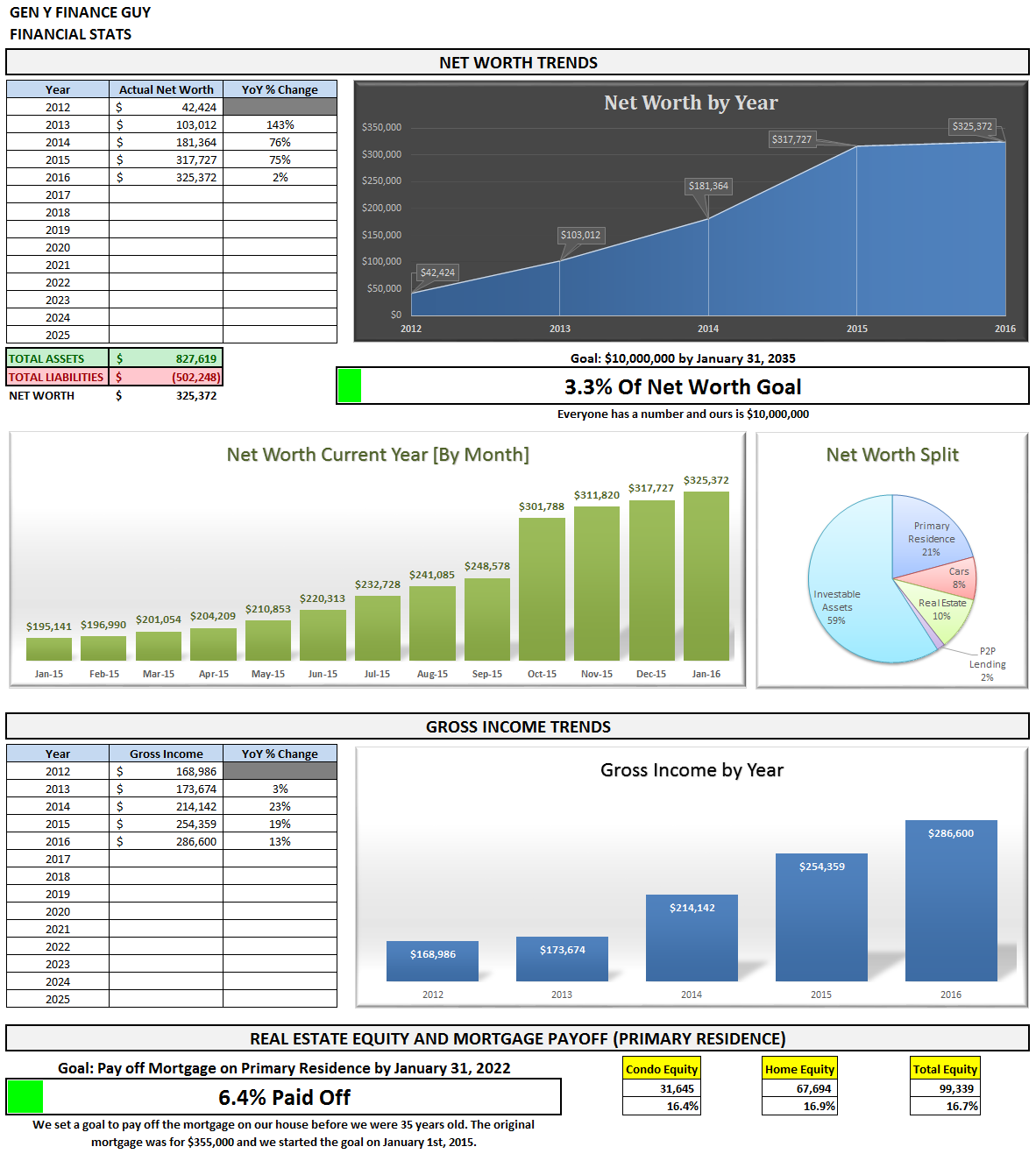

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate (NEW), and progress on the mortgage pay down goal.

Summary of January 2016

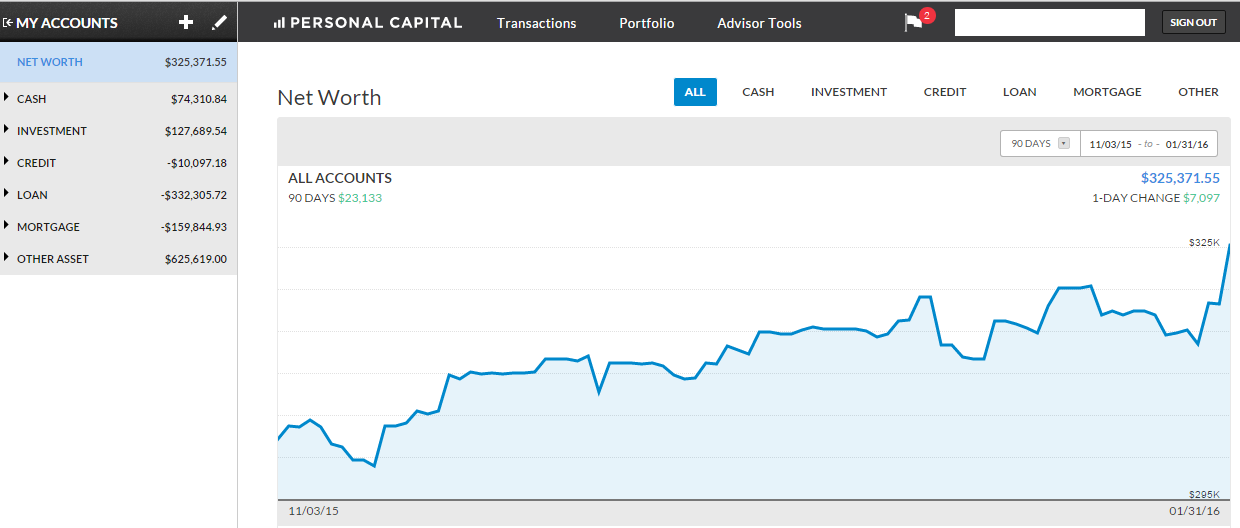

We use Personal Capital To Track Everything

I will continue to add screenshots of my Personal Capital account as another level of TRANSPARENCY in the numbers that I share. This month I actually remembered to get a screenshot of the last day of the month.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I then drop that information into my financial stats spreadsheet for this monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must, folks.

Personal Capital (which is free to use) is a great way for us to systematize our financial overviews since it links all of our accounts together and provides a comprehensive picture of our net worth. If you’re not tracking your expenses in an organized fashion, give Personal Capital a try.

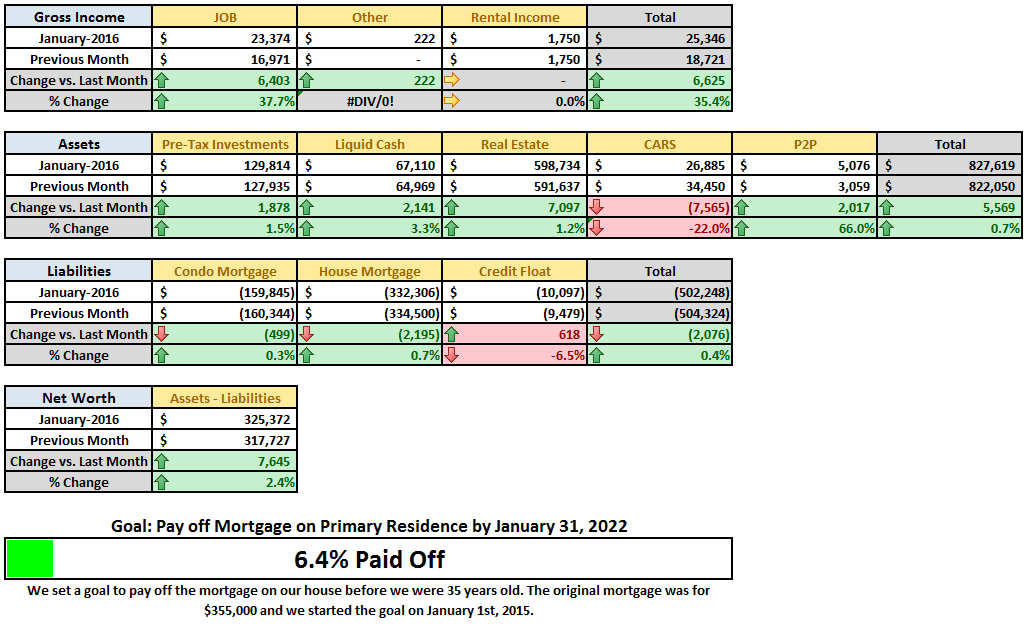

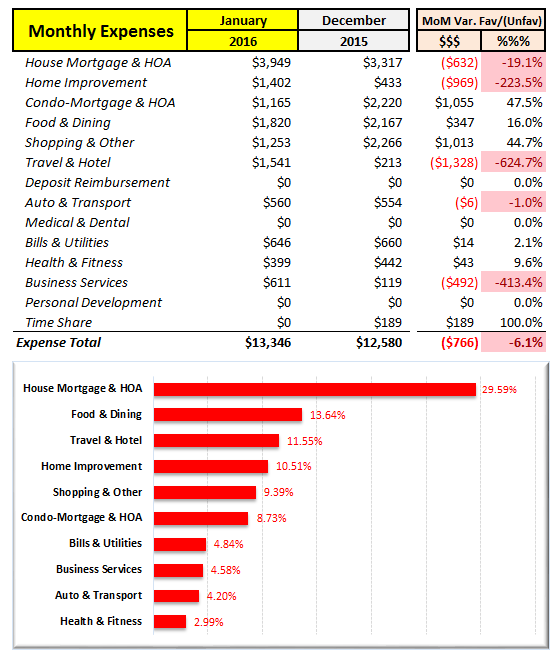

Month Over Month Financial Summary

Just two things to point out in case you missed it:

- I dropped the value of our cars by $7,565. I didn’t realize that Personal Capital doesn’t dynamically update the value and only found that out when I happened to log into my Mint account and see a difference. Now I know.

- I increased the value of our house by $7,000 based on comparable sales in the area (the value of our condo did not change). We will not look to update this again until June of 2016.

What went down in January?

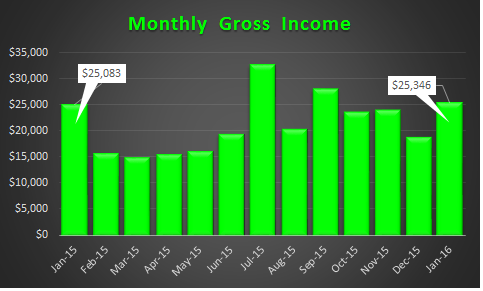

At the time of publishing the December 2015 financial report I thought that January was going to be a huge record setting month. But then here I am on the last day of January writing this report with no record to report. This is largely due to the fact that the company I work for processed bonuses later than normal and my bonus won’t hit my account until February 1st. That said, January was still a good month and about even with last year (which actually included my bonus).

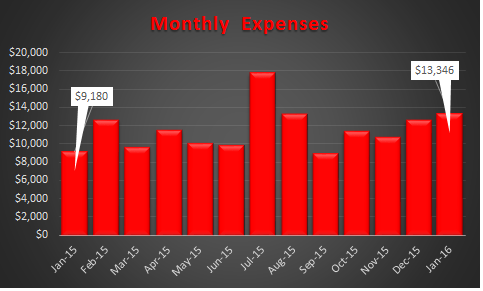

Here is a look at the trend for the last 13 months:

For 2015 we realized $254,359 in gross income, over the weekend I updated the 2016 forecast, and it’s now forecasting gross income of $286,600 for 2016 (based on new information, and I think we will actually come in closer to $300K or more). If you’ve read my blueprint for how I plan to reach $10M, you will notice that we have jumped about 6 years ahead of schedule on the income front.

I didn’t have us at this earning level until 2021 in the original blueprint…which will obviously need to be updated (post to come probably late February).

Looking ahead, February of 2016 is going to set an all-time record month. It is shaping up to be a $55,000 (or more) month (3.5X that of February of 2015).

The Juicy Details

- Previous Month: $18,721

- Difference: +$6,625

Income in January was up 35.4%. As I mentioned above, the increase was expected but missed forecast due to timing of yearend bonus.

Now where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it is a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here.

Note: The format of this section of the report has been changed to show a better view of month over month expenses and to help reduce the time it takes to put this part of the report together every month. Let me know what you think in the comments below.

The four major increases for January were for the following:

- House Mortgage & HOA – This month we started year 2 of our accelerated mortgage payoff and increased our additional principal payments from $800/month to $1,600/month. The reason you don’t see the full $800 increase is due to the fact that I got charged for 2 months worth of HOA last month and none this month, which accounts for the $184 difference.

- Home Improvement – We had an unexpected plumbing issue that cost us $1,025 to fix.

- Travel & Hotel – We booked our flights for our Costa Rica trip this summer as well as our flights to Northern California in February.

- Business Services – I prepaid my year hosting with WP Engine to get 2-months free. And I paid for FinCon in September.

These were also partially offset by favorable variances from a few other categories. I expect expenses to likely be a bit higher next month due to a home improvement project to re-finish our kitchen cabinets and a trip to Northern California for 4 days.

Expenses were up 6.1% this month vs. last month.

Here is the trend for the last 13 months:

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

- Our mortgage payment is automatically set up to pay $1,600 in additional principal.

- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

What were Investments and Contributions?

- Contributed $0 There is no longer any tax benefit for us to contribute to my wife’s IRA due to our income level in 2016.

- Previous month: $500

- Difference: -$500

- Contributed $1,442 Into my 401K.

- Previous month: $728

- Difference: +$714

- Prosper Lending $2,000 We now have $5,000 invested here.

- Previous month: $0

- Difference: +$2,000

- Rich Uncles REIT $97 This was from reinvested dividends. We currently have $5,255.

- Previous month: $0

- Difference: +$97

- Increase in Savings $2,141 This includes checking, savings, and CD’s.

- Previous month: $2,105

- Difference: +$36

- HSA Contribution $669 This is set up to max out by the end of the year. We currently have $6,536 here (JUST SHY OF MAXING OUT).

- Previous month: $1,000

- Difference: -$331

Total Investments & Contributions $6,349

- Previous month: $4,333

- Difference: +$2,016

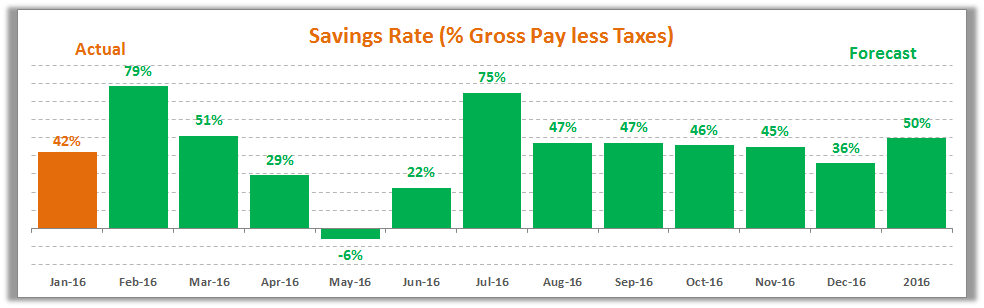

Savings Rate

Below is how we’re tracking to our goal of saving 50% of our after tax income.

You can see that although our goal for the year is 50%, we bounce all over the place on a monthly basis. We did end up missing our goal of 50% in 2015 and ended the year at 44%. It was a goal that was set mid-year, so I still consider it a win.

So far in 2016 we are on target to hit our goal of 50%.

Speaking of savings rate, have you checked out my recent post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

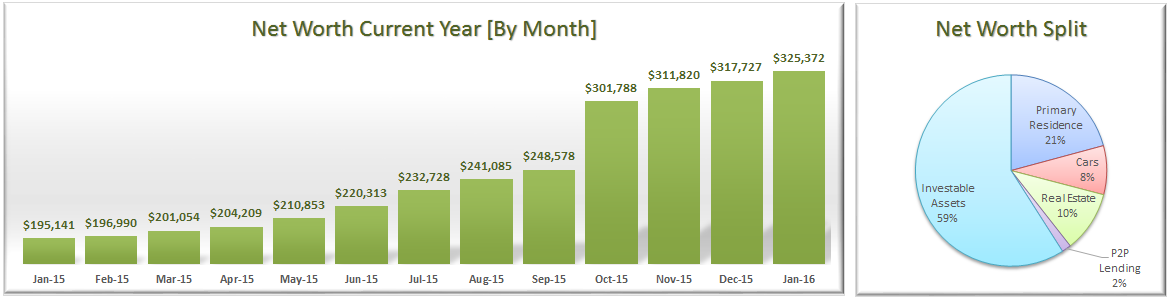

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income (at the end of January we are officially 3.3% there). Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate (just take a look in the side bar for growth at a glance). If you want to see how I plan to get there you can read all about it here (soon to be reviewed and updated in February of 2016).

January Net Worth $325,372 (this puts us up $7,645 or 2.4% vs. 2015 with 11 months to go)

- Previous month: $317,727

- Difference: +$7,645

Since publishing the first financial report we have been able to post 13 consecutive months of positive gains to Net Worth. Let’s see how long we can continue this trend. The larger the number becomes (and the more invested we become), the more difficult it will be to continue this trend.

Net Worth Component Break Down:

You will notice that in the second chart above that I have broken our net worth out into 5 categories: Primary Residence, Cars, Real Estate, P2P Lending, and Investable Assets. I want to continue to see our primary residence and cars make up a smaller and smaller piece of the overall pie. Over time I can see myself potentially adding more categories.

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote: Savings Rate – The Most Important Variable to Wealth Building [and the math to prove it]

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 5.8%, which means we picked up another 60 basis points in January.

In a few of the previous 2015 reports I had hinted that we may be changing up our strategy of paying down the mortgage. It now looks like we will continue as originally planned. So, starting in January of 2016 the additional $800/month we have been paying has increased to $1,600/month. This has us amortizing the loan at about $2,200 month in 2016.

There still will be a post dedicated to updating everyone on where we are, our thinking, as well as concerns we will be watching out for closely.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list (sign up form in the right side bar) and I will send you a copy.

- PersonalCapital.com (free) – I track everything in Personal Capital and then enter into my custom Excel template. Check out my Personal Capital Review to see if its right for you.

22 Responses

Great work, Dom!

Couple of questions:

Why have so much in (liquid) cash? Why not make that money work for you?

Do you have any bonds? How will you diversify?

Thanks R!

First off we tend to prefer to have at least $50,000 in cash on hand. This represents at least 12-months of bare minimum expenses if something was to happen to one or both of our jobs.

Beyond this there are a few things that we are stacking up cash for over the next 3-6 months:

1 – We plan to do a cash-in refinance on our investment condo. I have a post coming out later this month on the details of this. But the short story is that we plan to put in $15,000 in order to refinance the loan to free up $2,500/year in cash flow. That is a 16.5% cash on cash return.

2 – We will have to pay additional income taxes in April in the amount of $2,600

3 – As I type this we have just finished refinishing our cabinets, and that put us back about $2,000

4 – We have property taxes coming in April for the Investment Condo in the amount of $1,100.

5 – You asked what we plan to do to diversify. We actually plan on adding a new asset allocation to our net worth over the next couple months. We will be working to build a position in physical gold. To start we will be aiming at a 5% allocation. In the short term I can see us using $5,000 to $10,000 in cash to start this allocation.

6 – We don’t have any bonds, but comprised in the $67,000 cash position, we do have $6,000 worth of CD’s that are paying 3% (12-month maturity through our credit union).

As you read in the post above, our cash position was about $67,000. By the end of this month we will likely be closer to $90,000 and growing.

I personally don’t see any reason to hold a bond allocation as long as I have mortgages that I could be prepaying. On top of that I would consider my P2P lending activity another substitute for bond holdings.

Lastly, we do have preliminary plans to potentially look to add a 3rd piece of real estate to our portfolio depending on the market.

Other than that I am in cash accumulation mode building the opportunity fund. I am pretty bearish stocks and my 80% cash position in my brokerage accounts reflect that as well. I think 2016 will be much worse than 2015.

Cheers,

Dom

Pretty damn impressive that you were able to stay in the black despite the poor market returns in January.

Judging on your February trajectory, it looks like you are about to blow your growth out of the water next month, nice job!!!

Hey Fire Guy,

It is always great to watch net worth continue to climb up and too the right. However, I must point out two things regarding my performance relative to the market move:

1 – My investments accounts are sitting in 80% cash, so they are very much unaffected from the market moves…at least with regard to how much the move can effect my overall net worth.

2 – The investments I do have are options based positions that are pretty much direction neutral as long as we are in the range of $165 to $225 on the SPY.

3 – My contributions are still a very large % of my net worth…and at this stage in the journey they are and will continue to be more than enough to absorb any losses the portfolio suffers to show month over month increases. This will become more difficult as net worth gets larger.

Regarding February, yes, it will be a great month and net worth with jump substantially from a YoY growth perspective. Probably 10-12% growth in February alone.

Cheers,

Dom

With the economy and stock market falling apart, it is impressive that you managed to grow your net worth in January!

Wishing you continued growth.

S

Hey Sam – It’s only because I am sitting in 80% cash in my brokerage accounts. And the positions I do have on are very delta neutral. Also se the comments I left to dafireguy above.

Why not a backdoor Roth for your wife’s IRA?

Hey MBB_Boy – I have thought about it, but since we knew we were going to lose the deduction we started maxing out our HSA instead, which can also function as a retirement account. I prioritize pre-tax investments over post-tax savings.

We also have the complication of both already having IRA’s that have pre-tax money. It get complicated when you comingle the assets of pre-tax and post tax.

Here is a comment that Bubba from SouthernFriedFinance.com left a while back on this very topic:

I have not looked into this closely enough, but maybe a way around this is to open a completely separate IRA to avoid the issue? Honestly it is just not a priority right now.

But if you have further thoughts and suggestions I am always open to listen (i.e reading your comments).

Cheers!

Congrats on the 50% Savings. Can you provide more details on your savings? I see in Jan you had 13.3K in expenses and you detailed 6.3K in savings, what made up the other 7K?

Matt,

First to be clear, my savings rate for January was actually 42% and not 50%. The 50% is what we have forecasted for the entire year of 2016.

Here is the formula that I use for savings (Contributions + Amortizations)/(Gross Income – Taxes)

($6,349 + $2,800) / ($25,346 – $6,190) = 42%

Does that make sense to you?

It is all based off of after tax income. And in order to get the savings rate you have to add back loan amortizations to the contributions.

No worries, just curious. I’m aware of the pro-rata issue, but I go all roth for our IRAs (pretax for 401k) so its not an issue for me. If you’re going after the HSA instead no worries, still tax advantaged. You may want to rethink once you get to where you can max out all 401ks and the HSA. My wife and I max out two 401ks and IRAs (including a 401k that allows the 10% income kicker past the 18k limit, which not all companies offer). We aren’t HSA eligible however.

Wow! Great work, and being soo young! I love reading your growth and dedication to increasing your net worth.

Something to consider: I know it’s your mission to pay down your mortgage, I understand that you have a commitment to do it, but have you considered dialling it down to leverage cheap interest rates, accumulate more cash to buy another asset?

Just wondering what made you decide to go down this path rather than investing more aggressively while you are young.

I’m wondering because by the time you pay off your mortgage, you might have kids and other expenses and be even more risk adverse and more likely to reduce risk and preserve capital…especially when you launch a full time entrepreneur gig. Food for thought and just curious me.

Hi Tracy – Thanks for reading along.

I have definitely considered keeping the mortgage and investing the difference. However, some people have bond allocations, and to me paying down the mortgage is a bond substitute for me. This goal does not keep us from making investments. On any given month our investments/savings outpaces our mortgage pay down by at least 3 to 1.

We purposely bought a house that was 50% what we could afford, knowing full well that we could pay it off far earlier than the 30 year term. About 14 months ago my wife and I were sitting down and I had done some back of the napkin math that at the time showed would would be earning about $1.4M in gross income over the next 7 years. We both decided right then and there that it would be irresponsible for us not to pay it off. Since then our income has grown substantially.

It’s all a balancing act right?

I think it would be a different story if we were not also investing outside of paying off the mortgage. We are also managing this strategy by making sure our house does not comprise more than 25% of our Net Worth. And a secondary measure to keep an eye on our liquidity. We tend to like to keep 6-12 months worth of reserves.

Speaking of another asset, we actually have it on our list to buy a 3rd property this year.

When it comes to leverage I tend to not want to exceed 2-3X our annual income. So, based on that, paying down the mortgage on our primary residence only frees up borrowing capacity to continue adding assets. As you and I both know, leverage is a double edged sword…and in good times I think people have a tendency to forget that.

I totally see what you are saying. But right now this is just a small piece of a much bigger puzzle. If you look closely at the graphic above you will see that our home only makes up 21% of our net worth, while we have almost 3X that amount in investible assets (59% or 71% if you include our rental property and P2P lending).

Over the next few weeks and months we also plan to start a new asset allocation in GOLD, with a goal to build that up to 5% of our net worth.

I don’t know if you have read my $10M net worth blueprint (its a 20 year plan), but based on our earnings and where we are going, a paid off mortgage will be a drop in the bucket.

Who know what twists and turns we will take over the coming years.

Cheers,

Dom

Love your blog, especially the fact that you are prepared to show your actual financial situation.

I get the impression that you live pretty well on your income and it seems to me that you could speed up the achievement of your goals by holding down your cost of living. You know that you are already having a good time so if you slow down the inflation of your living costs relative to your income growth it would give you more money to invest sooner. You don’t have to spend more just because you earn more is what I am trying to say I guess.

I am not advocating extreme frugality but I would think the net worth amount would accelerate considerably if you adjusted the 50% spend and let the gap widen faster between expenses and income…..

Hey Troy,

Glad you are enjoying the blog and the full transparency that comes with it. We do live well indeed and to your point we are tryying to widen the gap.

In 2015 we ended the year with a 42% savings rate and are aiming for a 50% savings rate in 2016. As our income continues to climb I don’t expect that lifestlye inflation will be a 1:1 relationship.

Our spending is also a little decieving since it includes both regular and extra amortizations of mortgages, which is really just a balance sheet move and not an expense (sorry to go accounting and finance geek on you). Also, our savings rate is purposeley understated due the the way I treat our invetment condo. Most people would just include the net cashflow, but I include both the gross revenue and the total expense, which creates a drag on our savings rate.

At the end of the day I totally agree with you that we could be building this faster than we are. But honestly it is a very balanced approach.

I would not be surprised if we are saving 60% plus of our net income by 2017 based on a few things in the works.

I get the simple math that a 50% savings rate translates into a year of work for a year in the “BANK” if you will. If we can get our income to a place where we save 75% then we would be working 1 year while “BANKING” 3 years. Actually I have a post on this very topic coming out later this month I think.

Thanks for your comment and your thoughts. I hope to see you around.

Cheers,

Dom

Nice job! Keep moving up. I have been so insanely busy which is why I am just now reading this blog post! This report is obviously a couple weeks later than your reported numbers, but I am currently at $371k. I have a huge income month coming in March which will safely push me over $400k.

I am in the process of buying my first rental property in Little Rock, Arkansas. I have an offer in on 2 different homes that I like each. My intention was only to pick up 1 to start, but if both my rock bottom offers get accepted things will get interested as I would likely buy them both.

The one I am most interested in they countered at $185k and my best and final was $180k. Hoping they come back to accept. It’s a nice 3 bedroom in the best neighborhood in Little Rock, much to my surprise multi million dollar homes are literally blocks away from this house on the Arkansas river. This is a 3 bedroom house that should fetch around $1600 a month in rent.

I will keep you updated if we end up getting the offer accepted! My goal would be to build my Arkansas portfolio to 5-10 properties over the next 3-5 years.

Hey Sean – It sounds like we will be pretty close by the end of this month. I thought January would be a big month for me, but then my bonus did not end up hitting my account until 2/1/16. I am forecasting about $365K by the end of February, but you still have me beat 🙁

And it sounds like you will only be pushing further ahead in March. Just when I thought I would get a bite of that carrot I get whipped with the stick again 🙂

Are you going through a turnkey real estate service for the out of state properties?

I hope at least one of your offers gets accepted. Would be cool to have you write about the experience if you were up for it and why you chose the area and all that good stuff.

Cheers,

Dom

Hey Dom –

Wow nice big Feb for you! Something tells me we will be passing the torch back and forth many times 🙂

I actually looked extensively into a turnkey provider and even putting an offer on a property with them but backed out last second. There were a lot of things that ended up rubbing me the wrong way, specifically on the back end with the property management. Most property managers have a very simple business model: 10% of monthly rent. This turnkey property manager was actually only 8%, but had an enormous of hidden fees. They charged $750 every time getting a new tenant in as well as a $125 lease signing fee. They also charged 15% of whatever maintenance was required to help orchestrate it. new toilet for $300? Property manager would charge $45. Also, as a prudent investor, I wasn’t comfortable with paying retail price on a home. I interviewed a couple real estate agents and property managers and decided to piece the deal together myself. My property manager is great and been a valuable resource for me even before getting paid a single dollar. They also operate very simple, 10% a month with no additional fees or charges whatsoever.

I will definitely keep you updated on how it goes!

Sean – I agree…this is going to be a close race, which is going to make it a lot of fun that we are so close to each other.

Sounds like you found the right property manager. My wife used to do property management on the side and did charge half the first months rent when placing a tenant and 10% of the monthly rent, but did not up charge any of the maintenance or repairs.

We actually have a property management company in place with our rental condo and they charge a flat $95/month, which is really awesome (comes out to about 7% or rent). They do a fantastic job.

Man this thing is getting longer or at least I feel like it is haha 😉

Liking the trend though and definitely catching up on your back catalog :).

Looking forward to reading the record breaking year you’ll have!

Yes, I think the report has gotten longer over time.

You are closing the gap, only about 8 months to go 🙂