I would like to say that I have always been a goal oriented person, but that would not be the truth. Although I have been AMBITIOUS for as long as I can remember, I haven’t always given myself a clear path to success. It wasn’t until I read the Slight Edge

As humans, we tend to overestimate what we can do in a day or a week. But we also tend to under estimate what can be accomplished in a month, quarter, or year.

Writing (or typing) out your goals and then reviewing them on a regular basis, keeps them top of mind. It is not just the mere action of writing them down that makes setting goals so powerful. It is the daily review that keeps you in achievement mode. This daily practice is the first step in success. You start to visualize yourself accomplishing your goals, and your subconscious continues to work around the clock to find a way to ensure success with enough repetitions. Some people call this the law of attraction…and if that is a little to hoke for you, I tell people that your FOCUS goes where your energy flows.

The things we think about the most, tend to become self-fulfilling prophecies. The mind is one of the most powerful assets we have, and if fully leveraged can find a way to get just about anything we desire. This is not meant to offend anyone, but I don’t believe that any of our fulfilled desires are a result of any magical force or god. None of us are so special that we get special treatment…that is just ridiculous. We are in control of our own destiny.

We are the most intelligent being on earth. Most of us take that intelligence for granted, while others go on to change the world and live the life they first dreamed and then designed. Think about the world we live in for a moment. 99% of the things in our daily lives did not exist a mere 100 years ago. Everything we see was based on someone’s idea. At some point ideas are transformed into goals, which are then transformed into reality.

How powerful are we?

We have been blessed with a gift to turn ideas into reality. We are only limited by our own limiting beliefs.

“Most people fail in life not because they aim too high and miss, but because they aim too low and hit.” – Les Brown

Let’s break through the glass ceiling we have placed on our potential and start setting goals that get us out of our comfort zone. When you set your goals, make yourself uncomfortable, by setting goals that will stretch you to grow. Goals that you’re not sure exactly how your going to accomplish based on the person you are today. Jim Rohn use to say “if you want more, you must become more.” The most powerful thing about setting goals and accomplishing them, isn’t the end result of the goal, but who you have become in the process.

You begin to realize that the mind can ACHIEVE anything YOU can BELIEVE.

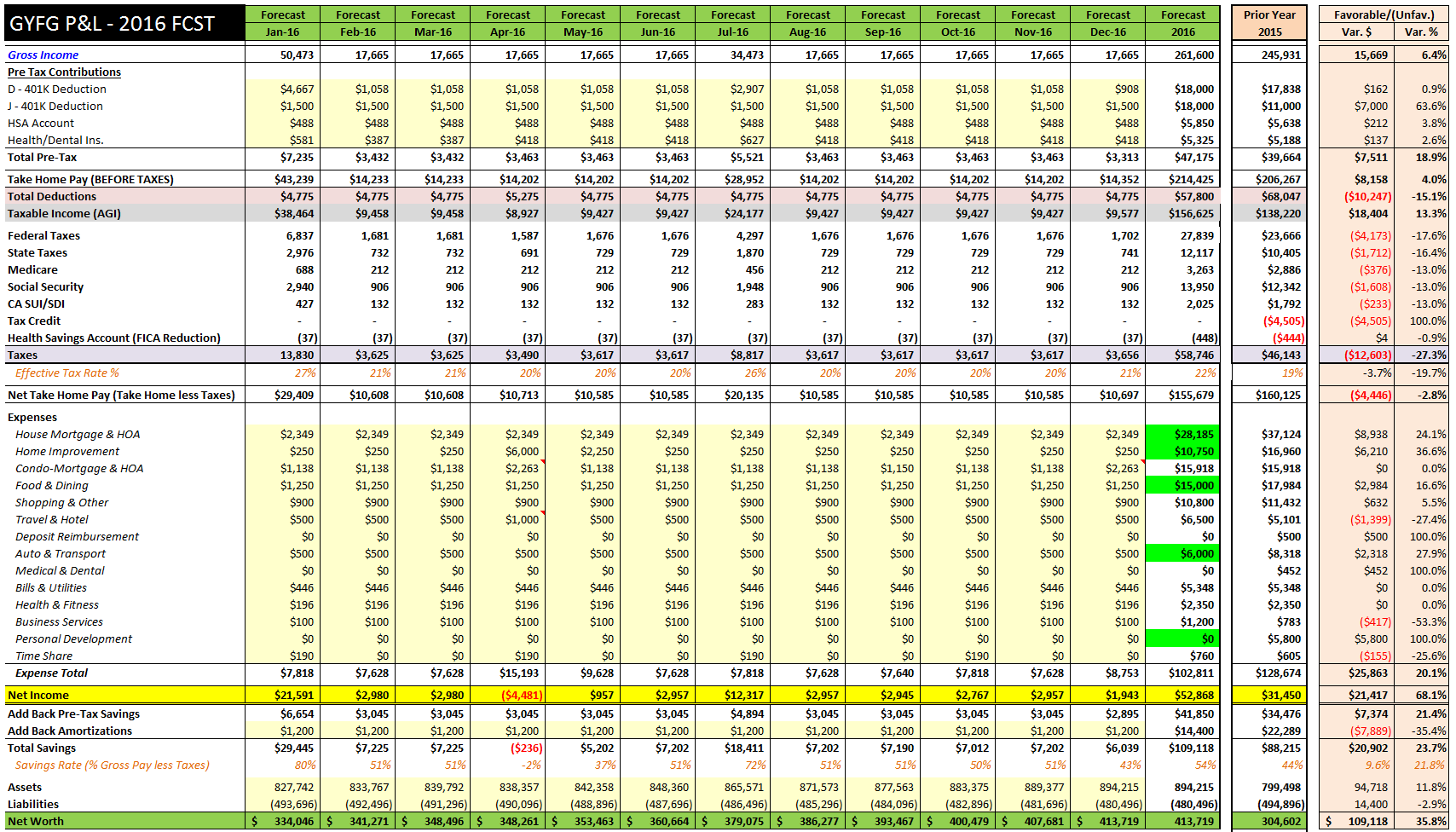

Our 2016 Financial Goals (1st pass)

I have always been a little obsessed with numbers and tracking, but I will admit that I have taken that obsession to a whole new level since starting this blog. This past year, I have gotten more granular than ever before.

It’s important to track where you have been so you can figure out how you are going to get to where you want to go. Personal Capital is my tool of choice for automated tracking. It’s a FREE tool that aggregates all your accounts into one place and provides you with summaries (and detailed transaction) of all your financial data.

I have recently been using this aggregated data to set up my financial plan (cough…budget) for 2016. My idea of a budget is not like that of most. I don’t set a budget to live and die by, rather to set targets and goals to aim for. It’s my best guess and a bit of a stretch for me to accomplish.

Some of you may be thinking that 2015 isn’t even over yet, how can you already be focused on 2016. Maybe I have been in Corporate Finance for too long, because we always start planning for the next year about 3 months before the current year is over. We also need to realize that 2016 will be here faster than we realize.

Here is what I have come up with so far:

In order to complete the year over year analysis, I also had to go through the exercise of forecasting how we plan to finish 2015. Something else I should point out, is that this is draft number 1. Meaning I have started with what I consider to be the base case for 2016 based on the information I currently have and with no layered in initiatives or goals if you will. This should on auto pilot.

The Big 6 Highlights:

- Gross Income is on track to go up by 6.4% in 2016. This is largely due to the mid-year raise I received that we will get to experience the full benefit of next year. In this first pass we have no assumptions for any raises and we have pushed my wife’s income down by $30K going into 2016, as a large part of here monthly income is commission based. We think the market will stay strong going into an election year, but are putting a bit of conservatism in the first pass (or base case). We want to see what we know we can do, and then use that as the launching pad for setting our stretch goals.

- Taxes are projected to go up 27.3%. This is due to several things. First our taxable income is going up by 13.3% due to the increase in income. Additionally, we are losing some of the deductions and a one-time tax credit we have for installing Solar. Before the end of the year I plan to run my numbers through a mock tax return using my tax software, and will compare that to what I calculated recently, which as come down a bit since my “Oh Shit” moment.

- Our Take home pay is actually going down by 2.8%. A big piece of this is the fact that we will be contributing to my wife’s new 401K in 2016 which will allow us to put $18,000 away vs. the $5,500 we were putting away in the IRA. The timing could not have been better, as we are getting dangerously close to being phased out by the IRS income limits for deductible contributions. The other piece is the increase in taxes.

- We are actually forecasting a 20.1% reduction in expenses. The savings is coming from 5 major categories (highlighted in bright green): home & mortgage, home improvement, food & dining, auto & transportation, and personal development. Our two big home improvement projects in 2016 will be to install new flooring on the bottom floor of our house, and to refinish the cabinets. Believe it or not, work we plan to do ourselves. Even in the face of my lack for skills and ineptness when it comes to DIY home improvement. You may also recall from my August Financial report that we were going to be making a shift in our strategy to pay off the mortgage early (more details to come in early 2016).

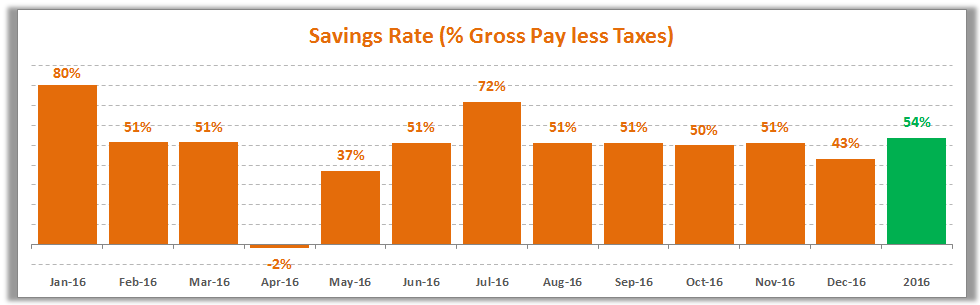

- We are forecasting a 9.6% increase in our savings rate (up 21.8%). It looks like we are going to be just short of our goal to save 50% of our income in 2015 (we set the goal mid-year). 2016 is looking like it will come in right at 54% in this first pass.

- Net Worth is forecasted to finish up $109K or 35.8% (to $414K). In the plan I outlined to hit $10M in a 20 year period (2015 was year 1), we have miles stones of $301K (2015) and $428K (2016). This is short by $14K of the 2016 milestone, but does not include any market appreciation or depreciation (assumptions are currently 0%).

What’s Next?

This post was really intended to push you into planning mode for 2016. When you fail to plan, you plan to fail. The reason we start thinking about this stuff so early, is so that we have plenty of time to put the systems in place to accomplish these goals. And so that we have enough time to think through all the details and the different initiatives that we need to layer in, to achieve the next milestone in our longer term plan.

In my next iteration I will be layering in assumptions for the following:

- A pay raise for me, even though I just got one in July.

- Stock options in the company of my day job.

- An additional Rental property in 2016.

- Higher income for my wife.

- My initiatives for producing side hustle income in 2016.

- Overall plans for creating more passive income in 2016 (i.e. cash flow real estate).

- Life Insurance (this should make for a controversial, but interesting post series)

- Family Trust & Will

- An expense line for Charitable Causes.

During the remainder of the year, I will also be taking time to think about other non-financial goals that I want to accomplish in 2016. It’s not all about the money, right?

What kinds of goals are you planning for 2016? Who is ready to make 2016 an EPIC year with me? When will you start and finish your planning?

-Gen Y Finance Guy

p.s Did you notice the NEW “Start Here” page? It’s a curated journey through this blog and it’s content. Check it out!

35 Responses

I also like “The Slight Edge”, a very inspiring book.

When you click on the spreadsheet image the slideshow starts. This was confusing, maybe you want to turn that off by default. Thanks.

Hey EurFI – The Slight Edge is my favorite book.

is my favorite book.

Thanks for letting me know about the slideshow issue. It is a new plugin. I have changed the settings to disable the slide show mode.

Cheers!

Thanks for the inspiration. I have some general financial goals for 2016 floating around in the noggin. Now its time to transfer it to excel and crunch those numbers.

Glad to be an inspiration Mattattack!

Any big goals you want to share?

Well, my income level isn’t as high as most, but I hope to max out my 401K next year (this year I’m on track for about $14K). My wife’s new job doesn’t offer any retirement savings account so I want to get her started on an IRA and contribute the $5500 max. I’d also like to roll over her previous 403b accounts to this IRA. I sock away about $5500 into taxable/savings accounts. I want to get that to $8-10K. That’s what I have for now, next is reducing our spending.

Mattattack – Those sound like some great goals and improvements vs. the current year. So, doing the quick math, that means you will be saving/investing an additional $12K to $14K in 2016 which is an amazing 85% to 100% increase year over year. Sounds like a win to me.

Cheers!

This is definitely something I would get a big fat F in. I generally just live life how I want and let the chips fall where they may. The only real budgeting I do is that I want to save minimally $5,000 a month, of which can come from 401k, payments to principle, or any other source that positively effects my net worth. Although I require this $5,000 in savings to be from active sources of income. IE my investment income does not get counted towards this $5,000. I am sure it would be an enlightening experience for me to sit down and forecast like you have done!!

Hey Sean – I hate calling it a budget, that is why I call it a forecast instead. It is a very enlightening experience. I would highly recommend it.

As you have probably already read somewhere on the blog, we are aiming for a 50% savings rate, so that is the only thing I really care if we hit. If we exceed it then great, but we enjoy life as well, so we don’t feel guilty spending the other 50% if we have things we want to do. Would much rather find ways to increase the income that force expense cuts in order to save more. But no doubt about it, my goal is to save more absolute dollars every year.

$5,000/month is a solid number to save every month. Our income can be a little volatile with my wife’s commission structure and my new bonus structure, so using an annual target works a little better for us than a monthly target.

Cheers!

It looks good overall. Definitely a great plan. I’m curious to know why you’re only going to contribute $5,850 to the HSA when the maximum allowed by the IRS for 2016 is $6,750?

I’ve seen your recent tax calculation spreadsheets from the other posts, as well as this one, and I’m wondering if you’re going to offer them for download?

Hey Kevin – Good question on the HSA. The reason I am only contributing the $5,850, is because my company contributes the rest to get me to the max. If I contribute the full amount I don’t get the companies contribution. Doesn’t work like a 401K 🙁

I had initially said I would, but I have been second guessing that decision. I don’t want anyone to get upset when the calculation isn’t 100% accurate, it is only meant to be an estimate, and there are a lot of variables that can very substantially. I have kind of created it custom to my own tax situation.

If you do want a copy, I do have a more generic version I created that I can send you, just send me an email at mrgenyfinanceguy@gmail.com

I knew there had to be a reason why. I know it doesn’t work like a 401(k), but you didn’t mention the company match in the post. Or if you did, I must have missed it. It makes sense now.

It totally didn’t even occur to me to mention it. Glad you asked the question though.

Cheers!

Love the transparency with putting everything of yours out there. I have started to think about 2016 planning, but not at this level of detail – YET! But I like this idea of creating our own personal Annual Operating Plan at this detailed level. I think it will help with the vision of the next year and add to the fact that my wife thinks I’m a humongous nerd (duh, we all already knew that!).

Hey Fire Guy – Glad you like the transparency.

I think you will find putting together an annual plan very enlightening. And of course another opportunity to nerd out 🙂

Hey GYFG,

That is quite a detailed plan that you make for 2016. It means you have agreat way of tracking what/where you will end up.

For our 2016 personal finance goal, I stay more high level. I work with a fixed monthly budget for expensens and fun money. Next to that, there are contributions to the “big work” pot that we do each month. This way, I try to even out bigger expenses.

I the longer year planning, I try to estimate what and when we will do as big works in our house. This stays a big guesstimate work.

My next action would now be to update the LT planning and adjust where needed.

One of the changes I will make is to allocate more money to family travel as our girls start asking about other countries, sleeping in hotels an plane travel. I prefer to give them these experiences rather than to retire 2 years earlier.

Hey AmberTree – you have to find what works for you. Glad to here that you do some form of planning, it helps.

Your girls are going to get so much out of traveling. When we eventually have kids, we plan to do the same thing. Our plan is to spend 3-6 months a year in another country.

Cheers!

Very detailed forecast! I just did something similar to figure out how much I could save in 2016. Best of luck to you in 16!

Likewise FF!

Let’s kill it…

Wow, incredibly detailed financial planning… Nice work!

Ha…you think this is detailed, I have lines that are grouped and hidden from the screen shot I posted. It is even more detailed than what you see.

Yeah, I hope to build something similar eventually. Also, I’m sure you have it in the background and in other spreadsheets, but I was thinking of building out the balance sheet side in detail as well (i.e., drill down in assets and liabilities), and then link them all with a cash flow statement. I’ve also been working in corporate finance for way too long!!!

I don’t have a cash flow statement, but definitely a simple balance sheet.

This is fabulous and I find myself starting to do this at the beginning of October as well… just getting ready. Since my husband is much less numbers and spreadsheets-oriented than myself, I usually take a good 2 months figuring out where we’re at, what’s possible, and what the goals are going to be and then have a night where I bring it all up with him and he gets on board. Time to start strategizing for real!

Excellent post Dom! 2016 is literally around the corner. 🙂

Anyhow, I love your details (even the hidden ones…heh) and your personal drive to make 2016 an EPIC year! You’ve got some great momentum rolling already. Where are you thinking for the next rental property?

Hey Michael,

2016 will be here before we know it. If we can stay in the surrounding area for around $200K we will, otherwise we may open up to out of state. I have been looking at some properties from JasonHartman.com, he runs a turnkey real estate shop. He is actually down new you these days. He has a good reputation.

Do you have suggestions? You may be partial to Vegas 🙂

Will just need to make sure I get something I can rent out…learn from you!

Nice. I wonder if Alex from Cashflow Diaries has had any interaction with Jason before.

Although I like the proximity to the Las Vegas market, it’s appreciated too much the last few years. So, it’s harder to find cash flowing properties these days (at least easy ones).

Other areas of interest for me are Florida, Tennessee, Oklahoma, Texas, and Ohio. But, I’m not up to speed on these markets completely at the moment.

At some point I will probably reach out to Alex. I have one financial priority to finish up in January first, and then the search can really begin.

Cheers!

Hey there GYFG,

Just found your blog and I have to say I am impressed by the level of detail you apply towards tracking your finances! Although I know you like using Personal Capital as well, I am a die hard Excel guy myself. I was wondering if you would ever consider sharing your spreadsheets to your readers? I am sure there are plenty of people out there that would love to use them!

Also, I see you have a line item for Amortizations every month to the tune of $1,200. Can you explain what this is?

Thanks and keep up the great work!

Eric – Sorry for the delayed response. It has been a crazy pas few days.

Glad you like the level of details. Hope it helps to “Humanize Finance,” which is a part of the mission statement of the site. I love personal capital for account aggregation and some of the other tools, but I am still a die hard Excel junkie myself. It is just one of many tools in the arsenal.

I have thought about and do plan to make my templates available to people. Just need to find the time to do it in a systematic way. If you are interested you can download a copy of the generic version here.

Regarding $1,200 amortizations. This is the amount of money included in my monthly mortgage payments on my house and condo that go to pay down principal on the loans.

Cheers,

Dom

Love those goals Dom! Looking forward to hearing more about them as I progress through the posts :).. The thing I genuinely like about them is your focus on helping others i.e. your wife & charitable causes too.

My #1 goal is to get on top of all your posts 😉 haha (kidding).

I’m not as clear as I’d like to be on my financial goals & focus more on the process however my general idea is to have 200K “passive” income minimum by 2029 (the time I turn 40)..

I plan on getting involved in property development, continue to learn about investments & growing the net worth through gaining large chunks of cash..

I’ll get more specific on this though, which is why posts like yours are awesome! 🙂

Cheers