Hi, I’m Xyz from FinancialPath, working until 65 is nothing I could dream of and with a solid plan, my path to financial independence at 35 is clear. With the power of compound interest and a high savings rate, I am confident that I can achieve financial independence and early retirement within 10 years. I currently save over 50% of my income and hope to increase this savings rate up to 70% to finally accumulate enough assets to passively pay for all my expenses.

I am more than happy to share this guest post with GenY Finance Guy today. I wrote about my views on Bonds and their place in a portfolio, I hope you enjoy! Feel free to comment and share.

If you read a lot of investment blogs or listen to investment news, you might have heard that bonds are earning next to nothing these days. The yields have dropped to record lows and the future might look bleak. If you follow investment news (which I really don’t recommend if you are a long-term investor and wish to stay sane) you probably heard things that associates the bond market with safety, but is it any safer?

People complaining about how risky the stock market is ought to take a look at the so-called safety of today’s bond market. – Kelly Evans, CNBC

In addition, some say that you should always invest a portion of your portfolio in bonds according to your age. Financial planners used to say:

Subtract your age from 100 – and that’s the percentage of your portfolio that you should keep in stocks.

But now most planners are using 110 or 120 minus your age since people are living longer and need the extra growth that stocks can provide. As I see it, bonds play a lesser role in portfolios than they once did but you shouldn’t disregard them completely.

Historically

Looking back, bonds acted as volatility stabilizers for investment portfolios. They often rise in price when stock prices fall or at least, keep their value. Below you can see how the Vanguard Total Bond Market ETF (VBTLX) compared with the S&P 500 index in the last 10 years.

Credit Vanguard

You can easily see how bonds (the blue line) kept a steady uptrend even during the 2008 market crash. However, the S&P 500 index clearly got ahead in the following boom. Doing this on longer-term periods will show an even bigger discrepancy between returns. The yield on a U.S. 10 Year Treasury Note, pretty much the safest bond you could get, has fallen from 14% in 1984 to 8% in 1994 then to 4% in 2004 and to under 2% today. Looking back since 1926, having a considerable portion of your portfolio in bonds would reduced volatility without greatly reducing total returns but those conditions no longer exist. Today’s rate are so low that there is little room to fall and at some point will go up. Once rates start going up, bond prices will fall.

I don’t think that the old rules of thumb stands any more. The rates are at record lows and the long-term prospects are dim.

As a fun exercise (I know I’m weird to find this fun 🙂 ) I tried multiple scenarios in FIREcalc to get an idea of the difference. FIREcalc is a retirement calculator that uses Monte Carlo simulations to see how your portfolio would have withstood the different periods of time throughout history. If your retirement strategy would have withstood the worst ravages of inflation, the Great Depression, and every other financial calamity the US has seen since 1871, then it is likely to withstand whatever might happen between now and the day you no longer have any need for your retirement funds.

After entering a topical $1M portfolio withdrawing 4% annually (following the Trinity study) FIREcalc looked at the 116 possible 30 year periods in the available data and concluded that for a 100% equity portfolio, the lowest and highest portfolio balance at the end of the periods was $-931,017 to $8,509,297, with an average at the end of $2,686,348. It found only 8 cycles that failed, for a total success rate of 93.1%.

With a 90% equity portfolio, the lowest and highest portfolio balance at the end of the 30-year periods was $-676,978 to $6,924,916, with an average at the end of $2,337,419. The success rate slightly increased with only 6 cycles failed and a success rate of 94.8%.

For a more conservative portfolio of 65% equity, (35% bonds is about the “riskiest” allocation most financial advisers would suggest to clients, some go as far as 50% in more conservative cases) the lowest and highest portfolio balance at the end was $-301,852 to $4,921,485, with an average at the end of $1,543,147. FIREcalc found only 5 cycles failed, for a success rate of 95.7%.

With this data, you can clearly see the astronomical opportunity cost of “security”. Going from no bonds to 10% in bonds would have cost you $1,584,381 in the best period for only 1.7% more chance of success! Choosing a 35% bond allocation would have cost you a crazy $3,587,812 just for 2.6% more chance of success, or in other words, almost $1,4M per percentage points 🙂

Retirement

If you are like me and still have years before retirement, a large bond allocation might not be ideal for your portfolio. The main advantage I see in bonds is the stability they could offer if I would be withdrawing from my portfolio. During my whole accumulation phase, I prefer opting for better long-term returns of equity. If we look at the S&P 500 over the past 70 holding periods of 20 years, starting with 1926 to 1945 and going forward in 20-periods, not a single term has posted a loss.

I would argue going 100% stocks is more risky in the short-term but is actually safer in the long-term. Such an allocation would optimize your returns and might allow you for an earlier financial independence.

Now, once you retire, bonds might serve a purpose. If you would need to withdraw from your portfolio each year and encounter a recession in the first few year of retirement, your success rate would drop considerably. Starting a withdraw phase in 1929 or 1930 would have been devastating and you would then need to go back to work, or considerably reduce your spending. In the exercise above, the few failed scenarios in FIREcalc where all periods starting in the worst market conditions in history. Having bonds allows you to withdraw that portion of your portfolio first before selling off any stocks. For that reason, changing your allocation might be suitable in the first few years of your retirement.

Allocation

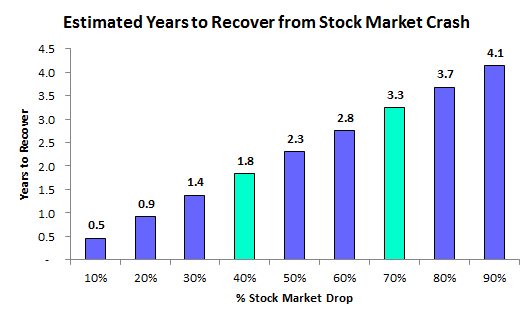

To determine how much you need to allocate to bonds, I suggest thinking about the amount you would need to live through a recession. As shown below, market crashes historically recovered quite rapidly. For a 40% drop like we have seen in the 2008 crash, it’s estimated to recover in only 1.8 years.

Data: NYTimes Chart Credit: FlannelGuyROI

Me, I used 1 full year of living expenses, this would allow me enough time to liquidate some positions and greatly increases my rate of success in early retirement. If you feel comfortable with the market swings and are investing for the long haul, you can have a 100% equity portfolio until you approach your retirement target. Then you can allocate your desired amount to bonds but I would not look at in terms of percentage of your portfolio.

Diversify

The one thing I need to underline when suggesting that a 100% equity portfolio is that you need to stay diversified. I would not recommend this allocation to someone who picks individual stocks and only has a hand full of companies in his portfolio. I suggest investing in index funds such as the Vanguard Total Stock Market (VTSAX) given it’s broad diversification. If you can choose an index fund, keep in mind the most important factors of a good fund:

- It should hold at least 1500 individual stocks

- It should have a low management fee (0.05% to 0.30%)

- It should be easy to buy and sell at no or very low cost

Once you are invested in a properly diversified, your allocation should outpace over the long-term if we compare to historical data. Of course, past performance does not guarantee future results so I will let you get to your own conclusions after the data and arguments I presented.

What About Me?

If you read my Open Book Series, you can see that I currently have a 95% equity portfolio. After research, I concluded that I am too young to hold any bonds at all and that I should optimize my long-term potential return by opting for a 100% equity portfolio. However, I started investing in bonds at the beginning of my accumulation phase and now I do have this small amount idling in my registered account (401K). I currently invest all my new contribution all in equities and don’t intend to increase my bond allocation before retirement.

I hope this gave you a little idea about the possible asset allocations, don’t be shy to comment below if you have anything to add or any questions on the subject.

Be Happy, Xyz.

14 Responses

I currently keep 10% of my retirement portfolio in bonds, although I debate whether that makes sense. I also have a 60/40 bond and stock split for my “emergency fund” which suits me just fine as I’d like to see some modest growth there and am willing to stomach a ~20% drop in the value of that account.

Yes, for an emergency fund it makes sense. I currently hold my emergency fund in a 1.95% savings account.

A lot of people think bonds are safer than stocks but Nick Murray in Simple Wealth, Inevitable Wealth makes a very good argument that bonds are actually more risky – the risk being that inflation will eat up portfolio value and you are more likely to outlive your investments. (I also wrote a blog recently on the topic).

The popular (il)logic of using your age to determine your bond mix is dangerous. Really the only reason to have bonds – IMO – should be based on your personal risk tolerance if you just don’t think you could hold steady through a downturn.

Yeah, I would understand holding bonds if you knew a downturn is coming but again; who can time the market? 🙂

Ya bonds aren’t doing so hot and aren’t projected to do much better.

I consider rental properties as creating my own bonds, but with several advantages. If you were to buy all cash, it would be fairly similar to a bond, with much better numbers. But I recommend using leverage on properties in boring markets.

I like that idea, for example, paying off a 3% mortgage is like a guaranteed 3% bond (which is pretty good!)

Xyz – the paid off mortgage is the only thing remotely close to a bond that I am willing to jump into. Especially given the interest rate environment. I think people fail to remember the inverse relationship that bond prices and interest rates have…there is potentially a lot of capital risk for people locking up money in longer duration bonds. When interest rates go up, bond prices go down.

I prefer to treat the mortgage on my primary residence as my bond allocation. It is sitting around 23% of my total net worth at the moment, but overtime I plan to dilute that to 10% or less.

Thanks again for the guest post.

Cheers,

Dom

I have 90% equity and 10% bond portfolio in my 401k. I’ve been reading that bonds have almost a 1 correlation with equity so if there’s that much correlation it’s hard to justify that bonds are much safer than equity. It’s good to see from a quantitative standpoint exactly how much we could be paying for safety. Great analysis and post!

Thanks for the compliments, you can head on to my blog for more 😛

I’m currently at 100% equity, but considering whether to do 10% bonds, so this is timely. Your breakdown by phase makes logical sense, but shouldn’t you be comparing total returns, not just yield, which doesn’t include the dividends? Looking at the total returns for the Vanguard Total Bond tracker (VBMFX) is much less bleak at 5.9% for the year and 4.94% for 10 years.

Agreed, more research would need to go into that. Thanks