GYFG here checking in for the February monthly financial report. If you have been reading these reports for a while you will notice that I introduce each month with the same intro month after month. I do this for two reasons, a) for the newbies to the site (which make up about 50% of the sites traffic) and b) to remind everyone what these reports are all about. By all means if you have read the intro at least once, then please feel free to skip down to the “Summary of February 2016” section where the new content begins (click the orange link to be taken there automatically).

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgence of your choice.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate (NEW), and progress on the mortgage pay down goal.

Summary of February 2016

We use Personal Capital To Track Everything

I will continue to add screenshots of my Personal Capital account as another level of TRANSPARENCY in the numbers that I share. Ignore the big increase that happened around the 10th of February. It was due to a glitch that forced me to remove my brokerage accounts and then add them back in.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I then drop that information into my financial stats spreadsheet for this monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must, folks.

Personal Capital (which is free to use) is a great way for us to systematize our financial overviews since it links all of our accounts together and provides a comprehensive picture of our net worth. If you’re not tracking your expenses in an organized fashion, give Personal Capital a try.

Month Over Month Financial Summary

Just three things to point out in case you missed it:

- We added precious metals to our asset side of the equation. We purchased two 1 oz maple leaf 24k gold coins.

- My annual bonus hit in February, which is largely the driver for the huge 11.4% increase in Net Worth this month.

- Our credit card float is the highest it has ever been as we have pre-paid for some larger expenses. A bit $6,400 chunk will fall off during the first week in March.

What went down in February?

At the time of publishing the December 2015 financial report I thought that January was going to be a huge record setting month. Since my bonus was paid out later than normal February ended up setting an all-time record with income at $59,495 for the month. That is a 278% increase YoY and a 135% increase vs. January.

Based on our current forecast I expect income to take a significant dip and maintain around $18,200/month, with the exception of July, which is currently forecast at $43,400 due to my mid-year bonus. There are several factors that could help us exceed expectations:

- Mrs. GYFG is still killing it. The last two months she has brought in an additional $5,500/month above and beyond her salary from monthly bonus payouts and notaries.

- There is the potential for a mid-year promotion to VP that I am working towards. This could lead to a substantial increase in both my base and bonus compensation.

Here is a look at the trend for the last 13 months:

For 2015 we realized $254,359 in gross income, over the weekend I updated the 2016 forecast, and it’s now forecasting gross income of $287,373 for 2016 (based on new information, and I think we will actually come in closer to $300K or more). If you’ve read my blueprint for how I plan to reach $10M, you will notice that we have jumped about 6 years ahead of schedule on the income front.

I didn’t have us at this earning level until 2021 in the original blueprint…which will obviously need to be updated (post to come probably late February).

The Juicy Details

- Previous Month: $25,346

- Difference: +$34,149

Income in February was up 134.7%.

Now where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it is a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here.

Note: The format of this section of the report has been changed to show a better view of month over month expenses and to help reduce the time it takes to put this part of the report together every month. Let me know what you think in the comments below.

Expenses were rather flat month over month with increases in the Home Improvement category offset by decreases in Travel & Hotel, Business Services, and Health & Fitness. The negative amount for business services was due to a refund I received for my hosting service.

Expenses were down 0.2% this month vs. last month. This month I have added two additional lines below “Expense Total” to add back amortizations since they are a balance sheet swap and not really an expense (accounting geek out moment…and I am not even an accountant). This will help give a more accurate picture of our expenses.

One of the other things I am thinking about adding is a YTD comparison vs. our 2016 budget/forecast that we put together. But still need to think about that one.

Here is the trend for the last 13 months:

I haven’t change the chart yet to reflect the add-back of loan amortizations.

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

- Our mortgage payment is automatically set up to pay $1,600 in additional principal.

- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- My HSA contribution is automatically deducted at a rate that will ensure I max out by year end ($6,750)

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

What were Investments and Contributions?

- Contributed $0 There is no longer any tax benefit for us to contribute to my wife’s IRA due to our income level in 2016.

- Previous month: $0

- Difference: -$0

- Contributed $4,662 Into my 401K.

- Previous month: $1,442

- Difference: +$3,220

- P2P Lending $1,000 We now have $6,000 invested here. We opened an account with Lending club last month. Trying to spread the love 🙂

- Previous month: $2,000

- Difference: -$1,000

- Rich Uncles REIT $0 This was from reinvested dividends. We currently have $5,255.

- Previous month: $97

- Difference: -$97

- Increase in Savings $26,732 This includes checking, savings, and CD’s.

- Previous month: $2,141

- Difference: +$24,591

- HSA Contribution $669 This is set up to max out by the end of the year. We currently have $6,536 here (JUST SHY OF MAXING OUT).

- Previous month: $488

- Difference: -$181

Total Investments & Contributions $33,063

- Previous month: $6,349

- Difference: +$26,714

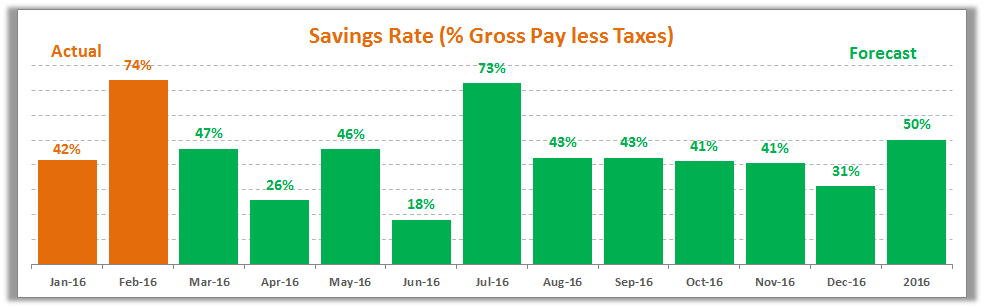

Savings Rate

Below is how we’re tracking to our goal of saving 50% of our after tax income.

You can see that although our goal for the year is 50%, we bounce all over the place on a monthly basis.

So far in 2016 we are on target to hit our goal of 50%.

Speaking of savings rate, have you checked out my recent post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Net Worth and Mortgage Pay Down Update

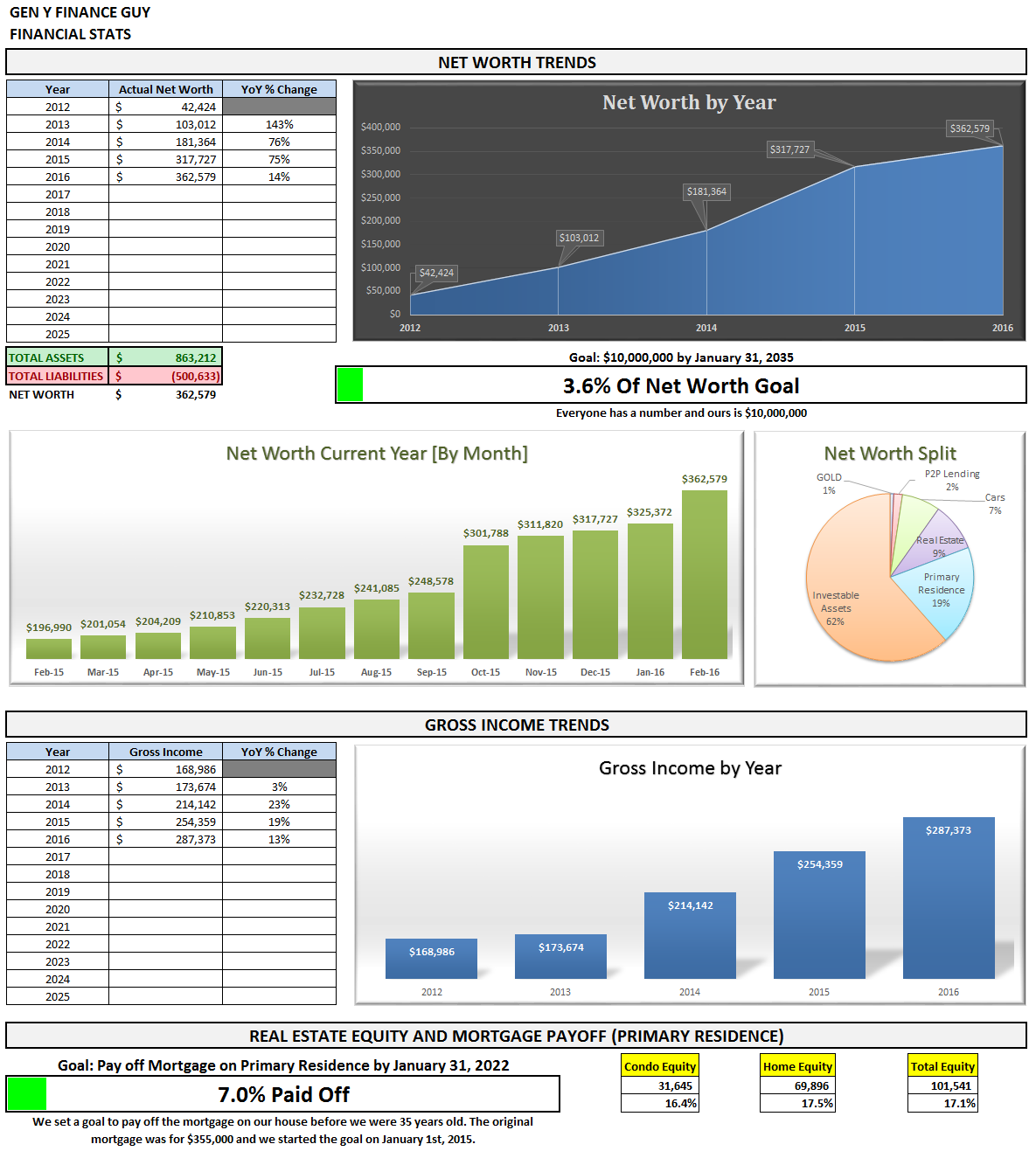

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income (at the end of February we are officially 3.6% there). Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate (just take a look in the side bar for growth at a glance). If you want to see how I plan to get there you can read all about it here (soon to be reviewed and updated in February of 2016).

February Net Worth $362,579 (this puts us up $48,853 or 14.1% vs. 2015 with 10 months to go)

- Previous month: $325,372

- Difference: +$37,207

Since publishing the first financial report we have been able to post 14 consecutive months of positive gains to Net Worth. Let’s see how long we can continue this trend. The larger the number becomes (and the more invested we become), the more difficult it will be to continue this trend.

Net Worth Component Break Down:

You will notice that in the second chart above that I have broken our net worth out into 6 categories: Primary Residence, Cars, Real Estate, P2P Lending, Gold, and Investable Assets. I want to continue to see our primary residence and cars make up a smaller and smaller piece of the overall pie. Gold is a new allocation and the plan is to work to build this up to about 5% of our Net Worth.

Something I have been thinking about and worth pointing out is that our net worth was actually negative to the tune of almost -$300K back in early 2009, so we have come a long way in a relative short period of time. Until now I had only reported our ending net worth from 2012. I am thinking up a post that would give the full story of how we started so negative right out of college and how we have improved it so dramatically in such a short period of time. I mention the first drag in this post about our investment condo.

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote: Savings Rate – The Most Important Variable to Wealth Building [and the math to prove it]

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 6.4%, which means we picked up another 60 basis points in February.

We are currently amortizing the loan at about $2,200 month in 2016.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

Oh, you’re still reading.

Do you want to help keep our lights on? You’re under no obligation, but if you were already thinking about it or were a little bit curious, why not help us out?

Here are a few ways you can help us out:

- Personal Capital – You know how big I am on tracking my finances, that’s why I totally recommend Personal Capital’s FREE software that helps you see all your financial accounts in one secure and convenient place (checking, savings, investments, and retirement accounts). Without a tool like Personal Capital, these reports would take 2-3 times as long to complete. You want to track your income? Your expenses? How about your Net Worth (who doesn’t like watching that bad boy climb). Just sign up and link your accounts today. Absolutely FREE to you!

- Prosper or Lending Club – Lending to consumers is a great industry that’s produced profits year after year for a handful of banks. Now with Prosper, you as the investor get unprecedented access to this market. My personal P2P portfolio is earning over 5%. Open a FREE investment account today!

- TD Ameritrade – They are hands down the best broker for the retail investor. TD Ameritrade provides a number of investing platforms that are more robust than any other platform I have ever used. My particular favorite is the “Think or Swim” platform. Oh, and did I mention that they have over 100 ETFs that you can trade commission FREE?

- Blue Host – Have we inspired you to create your own blog? Well let me save you some money. This is the hosting company that I use for this blog. It is stupid cheap and the customer service is amazing. The normal price is $5.99/month, but if you use this link you will get a 34% discount (only $3.99/month). It took me less than 5 minutes to buy my domain, install wordpress, and get the first version of this site up and running.

OR you can check out our Recommended Products and Resources page.

27 Responses

I like that chart for your projected savings rate by month. One of my big take-aways from your site is that I need to do more planning for savings. I’ve been in ‘survival’ mode for the last 4 years with expenses (get my business off the ground, engagement ring, wedding/honeymoon), so I need a savings rate goal when things return to normal in late 2016.

Hey Brian – We have all been there my friend. Planning definately makes these things top of mind. I have found that with anything I plan in my life, they seem to move in the direction I am after much quicker than just winging it.

Let us know what you land on for the savings rate goal.

Cheers!

The long-term planning to that degree is great for increasing the chances that you actually stick to the plan, it’s sort of like writing down your goals and placing them where you can see them. It provides that much needed reinforcement, and strong work on setting a personal best!

Congrats on the killer month of February! Looks like you are on a big roll on the income side!

Funny you mention the 1oz maple leaf. I really love these. Not as much as a investment asset class (I have paper gold for that).

Why did you add these to your asset class mix?

Hey AmberTree – It was a great income month for sure…but one that won’t be repeated for sometime (January 2017). However, I do expect to set a second best income month in July with mid-year bonuses.

The Maple Leaf coins are really a beauty to look at.

I added these in the asset class mix due to currency war/devaluations that are going on around the world. I am an optimist at heart, but this is just a way to hedge my bets in case this whole monetary experiment we are in fails. Talks of negative interest rates in the US are becoming more common place (espeically with so many other countries around the world already live with them).

We are living in interesting times.

It feels like the prudent thing to do.

Cheers,

Dom

Nice this is the report I was waiting for! 🙂 As of today, as my large bonus just hit as well, our NW is at $415k.

I will be very interested to see how you manage your cash position. I am deathly scared of cash and the way I operate our finances is I invest anything over 5k in a checking account, whether I invest that money conservatively or aggressively depends on the current market environment, but I feel there is ALWAYS a better option than cash.

Cash now makes up roughly 1/4th of your net worth which is clearly very high, unless you plan on purchasing a property or something of the like. Looking forward to hearing more about this!

Sean – Nice move in your personal Net Worth.

Over the next 90 days our cash position should come down by at least 40% due to the following:

1 – Taxes in April [$3,000 hit to cash] (we will be sending the IRS more money as usual)

2 – Credit Card Float going to Zero [$11,000 hit to cash] (you may notice in the screenshot above that the float has crept up to $11,000, mostly due to home improvement project, recent vacation, and prepaying future vacations). I have paid these down to zero and will plan to keep a very minimal float until we get two refinances we are working on out of the way.

3 – Condo refinance is on hold due to some complications (basically need to wait one year from February). This was going to be a $14,000 hit to cash, as we were going to need to bring money in to achieve a 25% equity stake.

4 – Since we could not move forward with #3 above we have decided to move forward with a refinance on our house [$25,000 hit to cash] to free up additional cashflow and expedite the pay off of our mortgage. The plan is to initate the loan application on 4/1/16. Based on comparable comps we would only need to bring in about $7,000 to achieve a 20% equity position in order to get the best rate our credit union is offering on a zero fee refinance for a 3/1 ARM at 2.25%. This will free up almost $500 a month.

We are also working with an agent to look at properties in a certain senior community where we live that have great cash flow potential but very little in the way of appreciation. More to come eventually on this.

Onward & Upward!

Dom

BlueHost customer service, in my opinion, is pretty terrible. Hold times are usually over 20 minutes and the advice is generally geared toward pushing tertiary products.

Not to mention my site often goes offline due to the host not being reached.

Gonna move to another host this summer.

Eric

Hey Eric – that is a bummer that you have not had great experience with Bluehost. I still think for the price you can’t beat them for those just starting out. If you want first class customer service I recommend WP-Engine or hosting from Themeco. I started with Bluehost until my traffic grew to a level that justified upgrading to a new hosting company. My first jump was to WP-Engine…and most recently I switched to Themeco as they also are the ones that developed my theme. Their hosting is optimized for both wordpress and my theme.

Yah, BlueHost is garbage. My site is down every few days (without making changes on the back end). And customer service is always at least a 22 minute wait for phone or chat.

For instance, my site is down right now for new reason…

Calling them to get a refund and will move to ASmallOrange.

Several blogger friends of mine are pretty unanimous that BlueHost is just about the worst host around. But because they offer such a nice referral fee, people pump them without a lot of thought.

Since you’re above the tax deduction phaseout levels, do you have any plans to contribute to a backdoor Roth IRA? I’m not sure exactly how much you have in the Traditional IRA you have for her, and I know that money would be subject to being taxed, but I was curious. If you don’t have a Traditional IRA for yourself, what about a backdoor Roth IRA for yourself?

On a side note, you made more in gross income for the month of February than I gross for the entire year. Kudos to you. Maybe I’ll be there some day.

It didn’t happen overnight and admittedly I do have help from Mrs. GYFG.

Do you have any side hustles going that can help boost your income?

Right now, I’m too busy with working full time (plus overtime as necessary) and doing online school full time to do any side hustles. I’m hoping for a career change within the next year or 2 that will increase my income as well as my income potential by a lot. Once school and my career change are complete, side hustles will be much easier to do.

Kevin – you are not the first person to ask that question. At this time we don’t have any plans to contribute to a back door roth. We both have traditional IRA’s due to rollovers from previous employer 401k accounts. So, the Roth conversion gets messy when commingling funds.

Not saying I won’t ever pursue that option, but its just not on the table right now.

Cheers,

Dom

Sorry to hear about your experience. My experience using them during my first year of blogging was much different.

I am going to submit a ticket with customer service sharing your feedback.

Has your experience always been this way? Or only as your site has grown in traffic?

Dom

Nice work! Great that majority of your expenses are going toward home / renovations which I suppose you could classify as more of an investment than an expense. Unlike my rental expense, which I’m trying to move away from. Keep up the good work.

Outstanding YoY monthly income increase. Congrats on this and best of luck with the potential VP promotion.

Thanks!

Way to go GYFG you’re killing it! Honestly, your net worth increase YoY is super impressive. To think its just going to start to snowball from here.

Good luck with your ambitions to become VP, hope it happens for you 🙂

Thanks Thomas!

Speaking of the VP role…I just got word yesterday that I will be starting our leadership program to prepare me for that new role. So, I think everything is on track 🙂

Dude, ya’ll are killing it! Your income reports are definitely inspirational, and I can’t wait for the post telling the whole backstory. I’ve been reading through your blog wondering what the h$ll ya’ll do, lol.

What I’m getting from your blog so far is just validating my decision to focus on income rather than just frugality. I was having some doubts recently, since I read a lot of frugality-focused blogs, but reading your blog inspired me to do some actual math (gasp!) and figure out that I’m on the right track.

– Pia

Hey Pia – The backstory is kind of spread throughout the blog. You can find out a bit of the backstory by subscribing to my email list. The short story is my wife and I graduated college in 2008 and she works in real estate and I work in corporate finance. From an income standpoint our combined income back then was about $65,000 and 7 years later were on track to earn over $300,000.

Frugality is a good characteristic to have. But I am a much bigger fan of relative frugality vs. extreme frugality…which you can see from our income/net worth reports. Meaning we are frugal relative to our income. The entire premise of frugality is living below your means. And to that end there are many ways to expand your means (income is one of those ways) in order to achieve frugality status.

Glad you find these inspirational. Regarding math, I am very fond of this quote “the path is all math,” not sure who said it.

Cheers,

Dom

Congrats on the bonus here Dom!

Looking forward to reading that you’re continuing to increase your income and get that VP position you’ve mentioned 🙂

***Spoiler Alert***

Jeff – you continue to make ground on the backlog. The VP role has actually been upgraded to a position in the C-Suite, which is actually supposed to get announced this week.

Cheers