Most of the time when you hear about refinancing it is usually along the lines of locking in a lower rate and/or cashing out during the refinance. You don’t read or hear much about a cash-in refinance and how the returns could really be worth consideration.

My wife and I currently find ourselves about 10 years into the 5/1 ARM on our investment condo. It didn’t start out as an investment. Actually, it is an interesting story on how we even became the owners of the condo. My wife’s parents had bought it back in 2005 before the market went off a cliff during the depths of the financial crisis. They paid $257,500 for it and put about $50,000 down. They secured a 5/1 ARM at something like 5.65%.

Their thought process was that real estate was going to keep going up and they feared their daughter (Mrs. GYFG) would never be able to afford to buy a place when she finished school in 2008. So, they figured they would buy something now to lock in current prices (just in case). During the time that the Mrs and I were still in college they rented the place out.

The Financial Crisis

Fast forward to 2008 and we are in the middle of one of the worst financial meltdowns in history. Unfortunately my wife’s parent’s livelihood was/is heavily dependent on real estate performing well. My wife’s mom owns an escrow company and her dad is a designer/contractor.

As my future in-laws financial world got rocked, it was assumed (or maybe hoped) that we would move into and take over the mortgage on the condo. It was either we assume the place or they were going to fire sale it. They were panicking and not thinking rationally, especially given that they still had a tenant in the unit. We hadn’t necessarily decided we wanted to move back to our home town, but we thought this could turn out okay even though the condo was upside down. At the current mortgage payment of $1,190 we would had been hard-pressed to find anything we could rent for much cheaper.

We agreed to assume the mortgage and with that ownership of the condo. My wife had graduated in May of 2008 and I in December of 2008 (I actually walked with my class in May but had a few classes to finish up). I had already started working full time as a financial analyst for the oil company I had interned with. My wife actually moved back home and started looking for a job. Once she found a job we gave notice to the tenants. Once the tenants moved out in early 2009 we decided to do a full kitchen remodel and put in new flooring and granite counter tops throughout.

When we officially moved into the condo in 2009, similar units were selling for as low as $80,000. Oh, and the mortgage we had just assumed was around $195,000 with an interest rate of 5.65%. Luckily that remodel only cost us material and the labor was free (thank you father in-law). My wife and I laid the slate flooring ourselves.

So, to recap we had just assumed a mortgage on a condo that was worth about $125,000 less than what was owed on it (after you factor in the $10,000 we had just put into it to make it our own). Our view at the time was that we could help family from losing this thing and with a long enough time horizon we would actually come out ahead. We were going to have to pay rent somewhere anyways, right?

The Benefit of an ARM Mortgage During Times of Economic Instability

Don’t be fooled! I know I paint a very calm picture, because that is just how I roll. My wife (girlfriend at the time) on the other hand was freaking out. She felt burdened with this place, but also had mixed emotions, because she was stoked to make it her own. At the bottom of any fall, it is easy to eat what the media feeds you, and at the time everything was going to ZERO. Obviously that was a bit of an overreaction.

At the bottom of any steep decline the case that something is going to ZERO becomes very compelling, but isn’t always RATIONAL. By the time we assumed the place, it had already fallen almost 70% from its purchase price. It didn’t seem plausible that these would ever be free.

But I would be lying to you if I didn’t admit to second guessing our decision over and over…and over again.

Then the ultimate freak out moment came when my wife learned that the mortgage rate was adjustable and was set to reset in October of 2010. Not really understanding how the interest rate was set at the time, she had nightmares of the rate jumping to some ridiculous number…like 10.65%. She had learned that the rate could increase up to 5% above the current rate (thus the 10.65% number), but what she failed to realize at the time was the following:

1 – The rate could only increase by a maximum of 1% a year with a life time cap of 5%. So, even if it were to increase it would be at least 5 years before we hit the max rate

2 – The rate could adjust UP or Down depending on the state of interest rates.

But more importantly…

3 – The rate was based on a spread over the federal funds rate. The margin is 2.75%.

It took a while, but I was finally able to explain to her that the adjustable rate was actually going to work to our benefit given the weak economy and historically low rates. The FED had recently just cut the federal funds rate to a range of 0.00% 0.25% (December of 2008), which implied a new rate of 2.75% to 3.0% when the mortgage rate finally reset.

I did the quick math and explained to Mrs. GYFG that our new rate was actually going to go down by about 3% and with that our payment was going to decrease $290/month (going from $1,190 to $897/month).

It has now been 62 months since the rate began its annual reset every October. That first reset took the original rate of 5.65% down to 2.875%, where it stayed for a few years, until recently jumping to….wait for it….3%.

The savings from the adjustable rate mortgage over the past 62 months has amounted to approximately $17,980.

Values Were Also Reset For Property Tax Purposes

During this time the assessed values that determined your property tax bill were also revised much lower to reflect the true market value. This has saved us thousands of dollars over the past 5 years as well. I haven’t actually done the math.

As the market has recovered the assessed value has continued to increase. Sometimes ahead of the market. Luckily my wife has experience in appealing property tax values, which has ensured that our property taxes were a true reflection of the prevailing market price of the condo. Most people don’t even realize that you can appeal the value of the property that your tax bill is based on.

Where Are We Now?

Remember towards the beginning of the post when I explained that we assumed a condo that was worth $80,000 at the time with a $195,000 mortgage (and the $10,000 we had just put into it)? So, all told we were under water by about $125,000.

First of all, we lived in the condo for a little over two years before moving and renting it out (in July of 2011). As a rental it has essentially been breakeven (after the Mortgage, HOA, water bill, and Property Taxes). From an income tax perspective it has been slightly better than breakeven due to the ability to depreciate the value over 27.5 years.

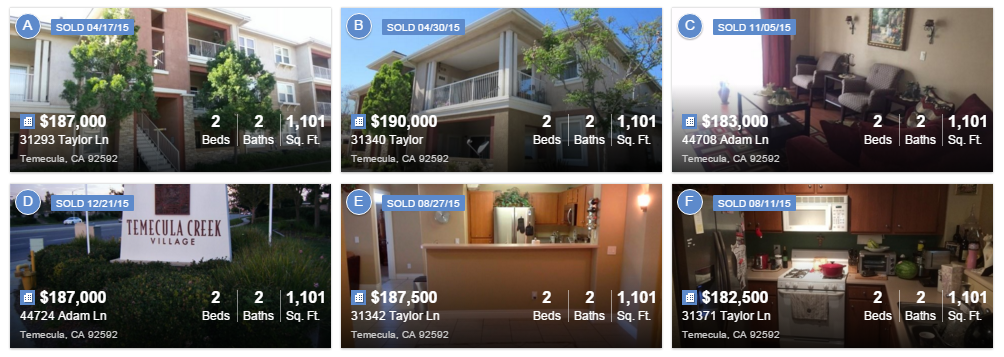

In 2015 there have been a number of units that have sold in the $183,000 to $190,000 range:

Redfin is currently estimating the value of our condo at $187,500:

At this point in time we owe $159,845. So, we are no longer underwater when comparing what we owe to the value of the property. However, the property is still $70,000 off its original purchase price of $257,500.

This currently puts our LTV (loan to value) at about 85%, leaving us with about 15% equity in the property.

We plan to hold this for the long term, but would like to improve the cash flow of this property. We are currently charging $1,350/month in rent, which is about $100 below the market, but we have a solid tenant in there. We don’t have plans to raise the rent on the current tenant in the near future, so the other option we are evaluating is a refinance.

A Cash-in Refinance [by the numbers]

Since this is an investment condo the only way we will be able to refinance would be to bring enough money in to move our equity in the property to 25%. Based on comparable sales and the upgrades we have made to the place we estimate the value to be between $190,000 and $200,000.

Let’s assume it is worth $195,000 for this exercise.

With that value the max loan on the property could be $146,250. This means in order to refinance we would need to bring $13,595 to the table to increase our equity stake to 25%. Because my wife works in the industry we won’t have much in the way of closing costs. The refinance we did on our primary residence 2 years ago cost us about $1,000 (basically appraisal and title, no origination fee or escrow fee).

Since we believe that rates will continue to remain at historic lows for much longer than anyone suspects (hello Japan) and due to the fact we don’t plan to keep the mortgage for a full 30 year term, we are interested in refinancing into a new 5/1 ARM.

Giving a quick look on the Internet I see that the rates are as low as 2.50%, and since this is an investment condo I will assume a 75 basis point premium at 3.25%.

The interest rate would be slightly higher than our current 3% rate, but by resetting the amortization schedule our new payment would be $696/month (at least for the first 5 years). This would represent a savings of $201/month or $2,412/year.

$2,412 is a 17.7% Cash on Cash Return on $13,595

After you factor in the $1,000 for closing costs, then we are looking at 16.5% Cash on Cash Returns.

If rates continue to fall or we are able to get a slightly more favorable valuation (meaning less money we have to bring in) then this cash on cash return could only get better. As I write this on 2/7/16, we are currently sitting on about $86,000 in cash and building. We don’t have anywhere else we could deploy cash and earn this kind of return.

So, over the next 60-90 days we will be moving forward to refinance the condo.

Have you ever considered a cash-in refinance? Did you think about it from this perspective?

-Gen Y Finance Guy

29 Responses

Dom,

Kudos to you and your wife for:

a) helping out family!

b) assuming a loan and servicing it with integrity (unlike most in that same situation during that time)

c) taking a long term investment perspective

Glad to hear the ARM worked in your favor!

Looking forward to hearing about the new one. I’ll take a 16.5% return on cash M-F all day long! 🙂

Thanks Micheal!

You said you would take the 16.5% return on cash “M-F all day long!”

What about Saturday & Sunday? 🙂

Haha, I knew you’d catch that. 😉

Sat & Sun are reserved for those blue moon deals or investments that yield 16.6% to infinity!

Nice!

Michael, I read the “M-F” as something other than “Monday thru Friday.” Sometimes I see what I want to see!

#beardlife Represent, GYFG!

Great story, sometimes not everything is measured in dollars. Your F-I-L’s help with the kitchen, and generous spirit of the original acquisition, is remarkable. You and Mrs. GYFG’s having their back and assuming the existing mortgage is also something that might be hard to justify on paper, but is the ‘right thing’ for your family. Always admire your posts, storytelling, and path. Continued success!

Thank you JayCeezy!

Enjoying the #beardlife for sure. It has been 2 months now.

You are right, on paper it looked horrible, but at the time we were able to help family out and in reality needed to live somewhere right?

It’s funny that this post just made me realize that there was a time in 2009 where our combined net worth was seriously negative by 6 figures when you consider the fact that I had student loans and my wife had just taken on a car loan at the time. Net Worth wasn’t even a consideration or thought back then.

Even if it were, I would had made the same decision.

Cheers,

Dom

What a story. It is good that you helped out your wife’s family and are able now to turn around this into a profitable rental condo.

The story for sure makes sense to me. We have had a similar move on our main house mortgage. We brought in cash when we financed to a 3/3 loan. It means the rate is fixed for 3 years and is then reviewed. We took this format as it was actually the cheapest formula around and has the lowest risk to the upside (There is a rule in Belgium that your rate can not double compared to the initial rate)

My lessons learned after 2 mortgages and 2 refinances: Always negotiate with multiple banks and look for the less regular formulas. There might be surprises there.

Thanks for sharing your own story AmberTree.

Sounds like the lending is probably a bit different in the US compared to Belgium.

That is incredible patience, congrats on waiting out the bad market. Definitely the mind of a smart investor, most would have panicked and run the other way!

Going with the ARM basically is a bet on the next 5 years – the rates can’t really go lower from here, so there is no way to adjust down after 5 years. Your access to low cost financing is unique, but I would recommend most investors towards fixed rate.

If mortgage rates go up 2% in 5 years, would it be better to get an ARM+refinance or lock in the lower rate now? What if it is 2% in 10 years? This sounds a lot like timing the market perfectly, which we know most investors are horrible at. But given your trading experience, you aren’t exactly the average investor!

Brian – when you are lot over leveraged patience is easy. The value was all paper at that point.

I would not recommend most to go down the road of getting an ARM. Although I don’t think rates are going to go up for years to come, this is not really a bet on interest rates. We don’t plan to have the mortgage for a full 30 year term, rather we plan to pay it off before that. I don’t mind using leverage but I have a 2-3X gross income rule on how much debt we can have outstanding. So, in order to use more leverage we have to be disciplined on paying it down quickly when times are good.

I think the biggest mistake most people make is getting an ARM in order to afford a place. For us, the ARM is just a way to reduce the amount of interest we pay while rapidly amortize the loan.

Cheers,

Dom

That’s true – if you pay back the loan in 5-10 years, the ARM will definitely provide a lower interest rate over that time.

I’m very much in the leveraging phase of building my rental property investments, but there will be a time when I need to decide I’ve had enough “good” debt (good because the tenant repays it, not me, but debt all the same). I’m curious – how did you come up with your 2-3x gross income rule?

Good question Brian!

It really started with a gut check. I tried to convey my thought process in this post: https://genyfinanceguy.com/2015/09/17/personal-leverage-ratio/

You may argue after reading it that we still have plenty of room for more leverage. Last year we earned about $250K which would imply a maximum borrowing capacity of $750K, yet we have a little less than $500K. This is by design based on where we are in the recovery. Also with interest rates so low we definitely could afford for productive debt than that, but don’t have the appetite for it.

By the end of this year, this number based on 2016 expected earnings will be around $900K…but it brings up something for me to think about. Should the number be based on a rolling 3 year average? Or just last years income? Or this years expected income?

At some point we will pull the trigger and take on more debt when we find the right property to add to our collection (evil laugh as I type this).

Would love your thoughts after you read that post (assuming you are interested in reading it).

Cheers,

Dom

$900k in expected earnings! Guess business is going well, congrats!

Read the post, interesting stuff. I guess the 2-3x is generally a rule of thumb so people don’t buy more house than they can afford. Yet the SF average is 9.1x so they didn’t get the memo (and why I will rent as long as I live here): http://www.economist.com/blogs/graphicdetail/2015/11/daily-chart-0

I think you need to separate the productive debts into 2 categories. Your home and college education can be productive debts – these are expenses that are worthwhile. Debts that directly lead to a return on investment are different. These are investment property mortgages and some business loans (a stable business that you can predict an accurate return on investment for).

In my mind these are different because one category has diminishing returns when taken to the extreme. For example, college education is good, but at some point around $100k you get way less for every dollar put in after that. It’s not like you can just keep collecting PhDs and expect the return to be there once you get a job.

Rental property mortgages you generally can expect to keep going. If you run the calculations, it will tell you: buy as many properties as possible with as much leverage as possible as long as the property is cash flow positive every month. If buying 1 property makes sense and you can get the same deal on 100 properties, do it!

Of course, that doesn’t sound quite right either, but in my mind there is a big difference between those types of debt. I could very easily feel comfortable with 5-8x income on investment mortgages. I’ll keep thinking about this over the years as I approach that number (right now I’m at 1x).

Brian – Sorry, I was not clear on the $900K…what I meant to say is based on expected earnings in 2016 that our maximum leverage we would be willing to carry would be $900K.

I can totally see the argument to create sub-categories for different types of debt. But I grouped them together because the reality is that every dollar in debt you already have reduces your borrowing capacity and your ability to service that debt.

In reality I would encourage most to get rid of the student loan debt before buying a house or investment property.

5-8x leverage scares me 🙂

That would mean up to $2.4M in leverage capacity for us. I totally get that there is cash flow and all that, but things get messy when theory and reality collide. Maybe I am just too conservative when it comes to financial leverage. But it also means you have the potential to create a lot more wealth than me 🙁

“Things get messy when theory and reality collide”. That is a perfect way to sum it up!

I guess let me restate the 5-8x. I could see $1M in mortgage debt on $150k regular income, maybe spread across a portfolio of 20 homes with 50% equity average in each. So the price of those homes would be $2M, and I would expect a cash return (rental income minus expenses) on that of >$50k per year, mostly tax free. I suppose this bring it at or under 5x.

Is that taking things too far? Maybe yes, maybe no.

I think it is all in the eye of the beholder. I don’t think there is anything wrong with your approach, we all have different tolerances.

With your scenario I would call it 5x.

Looking forward to following your build up.

Luckily there is plenty of time for me to think about it. Even if I am fairly aggressive with it, it will take years to get there.

ARM fan and a proponent of cash-in refinancing as well if you plan to hold for a long time. Those numbers make it a no brainer!

Bigger numbers might be a little trickier due to liquidity component e.g. need $100,000 to get LTV to 75% to refi is harder to stomach.

Where is this condo again?

Sam

Hey Sam – Yes, I have noticed that you are an ARM fan as well.

We do plan to hold the property foreverrrrrrr….

The condo is in Southern California in Temecula, which is about 1 hour north of San Diego.

Dom

Did you end up doing this cash in refinance? Have you researched to the tax implications of it? I did something similar and it seems highly unusual for investment properties, so I am having a hard time finding appropriate guidance for tax filing. If you did find that information, can you share any relevant IRS Publication numbers you found?

Justin – We did not end up doing a cash-in refinance with this property. We put it on hold until Jan/Feb of 2017 due to some complications that will remedy themselves by then. Instead we ended up completing a cash-in refinance on our primary residence.

There shouldn’t be any tax consequences though, besides your tax deductions going down potentially. You can’t be taxed on taking out a loan.