GYFG here checking in for the March monthly financial report. If you have been reading these reports for a while you will notice that I introduce each month with the same intro month after month. I do this for two reasons; a) for the newbies to the site (which make up about 50% of the sites traffic); and b) to remind everyone what these reports are all about. By all means if you have read the intro at least once, then please feel free to skip down to the “Summary of March 2017” section where the new content begins.

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgence of your choice.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

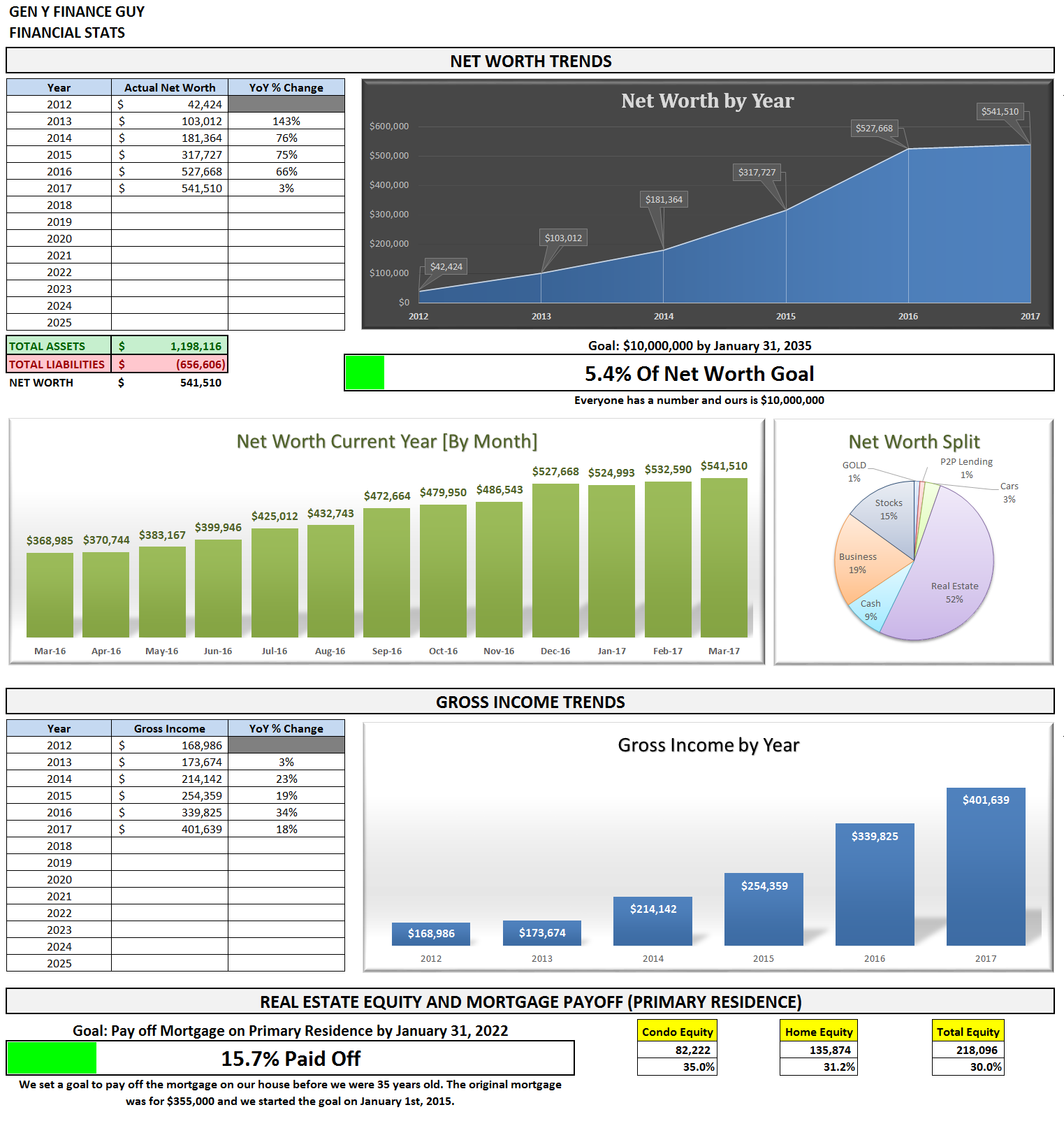

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate, and progress on the mortgage pay down goal.

Summary of March 2017

Wonder how I pull all this information together every month?

Note: You may be wondering why I don’t use a bunch of screenshots from personal capital in these reports, and that is a fantastic question. As many of the other bloggers out there who use personal capital, post nothing but the graphics from within the application. I personally only use it as an aggregation that feeds into my own database that creates all the graphics you see in this post. The tool is fantastic, but I personally think the graphics are a bit limited, and prefer my visualizations.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I export that information into my financial stats spreadsheet in order to produce this (beautiful) monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must!

If you don’t already have a FREE account with Personal Capital, stop reading and go sign up for your account right now! (Seriously, this financial update will be here when your done. There’s no time like the present to take action. You will thank me later!)

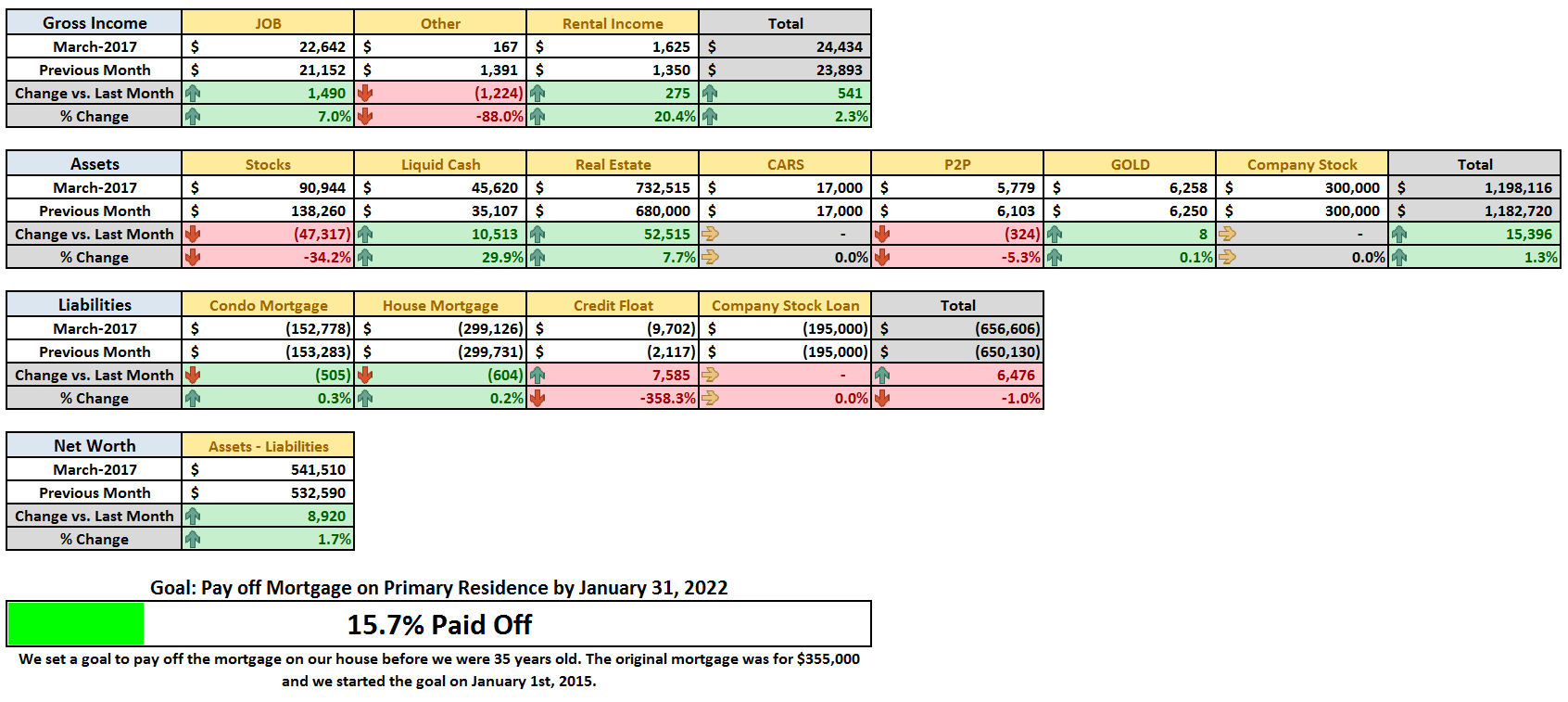

Month Over Month Financial Summary

Just three things to point out in case you missed it:

- I renamed the Pre-Tax investment column in the assets section to “Stocks”. It’s down $47,317 because of a transfer to a SD IRA investment account (the transfer was $50,000 so that I could put more money to work at PeerStreet).

- Due to 1 above, my real estate holdings increased by $52,515, $50,000 due to the transfer, and the rest due to additional investments made.

- Cash is up $10,513 or +29.9%, but a big piece of this is due to timing of paying our credit cards, which we pay in full when due. Between now and the end of summer, the goal is to save as much cash as possible, and to pay of the $27,000 401K loan I took out.

INCOME; What went down in March?

March Income = $24,434

- Previous Month: $23,893

- Difference: +$541

The GYFG household started 2017 strong with a new record high for income in a month of January (due to my year end bonus, which hit in February of last year). I don’t have another big bonus month until July, so I suspect income to be between $23,000 to $27,000 for March through May (range is due to uncertainty of Mrs. GYFG’s monthly commissions), but then jump in June due to a extra pay period.

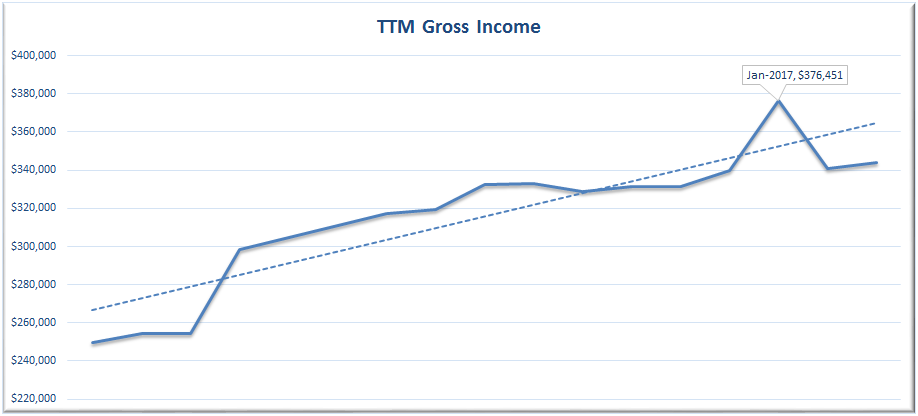

Here is a look at the trend for the last 13 months:

For those of you not familiar with the TTM acronym, it is short for ‘Trailing Twelve Months’. The all-time high remains $376,451. The big falloff in February was due to February-2016 falling out of the TTM aggregation time frame, which was almost a $60,000 month last year.

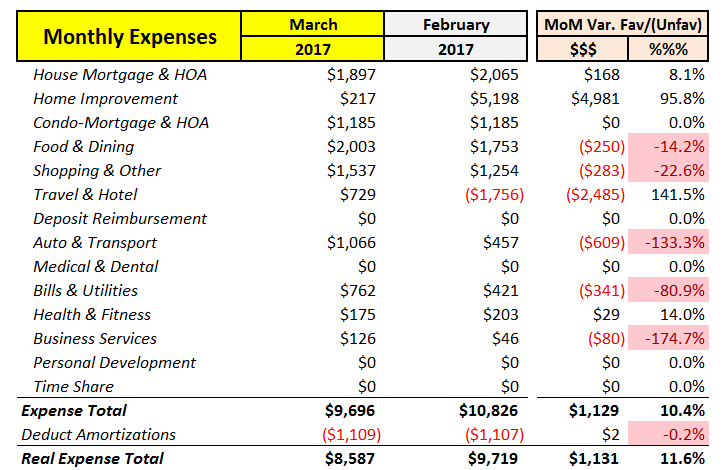

Now where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it is a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here. We do however try to line up expenses with expected income as much as possible.

Last month I wrote “I do expect March spending to drop below the $9,000 level and remain below $9,000 through May (maybe even through the rest of the year)”. As expected, we did see our real expense (after adjusting for amortizations) drop to $8,587 for the month of March.

We do have a few larger expenses hitting in April, but I still have us forecasted at around $8,100 for the month.

Here is the trend for the last 13 months:

Note: I have now changed the chart to reflect the add-back of loan amortizations to reflect what I call “real spending” above. This is done because amortizations are really just a balance sheet transfer from cash to pay down liabilities, it has no impact to net worth.

That spike is going to haunt me for the next 12 months, but it is also going to be a constant reminder to keep spending in check for the remainder of the year in order to achieve our savings and net worth goals. It really makes our spending look small in context of the big spike 🙂 . We are currently projecting our spending at $133,000 for the year vs. our original budget of $112,000 (and vs. 2016 at $121,000).

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

Our mortgage payment is automatically set up to pay $1,600 in additional principal.This is on hold until at least June 2017. Trying to work down concentration to something closer to 20%.- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- My HSA contribution is automatically deducted at a rate that will ensure I max out by year end ($6,750)

- We are now sending $500/month to our Rich Uncles investment account. Looking to increase the account balance to $11,000 by year end (currently at $5,500)

- We are now sending $2,000/month to our PeerStreet investment account. Looking to increase the account balance to at least $25,000 by year end (currently at $7,000).

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

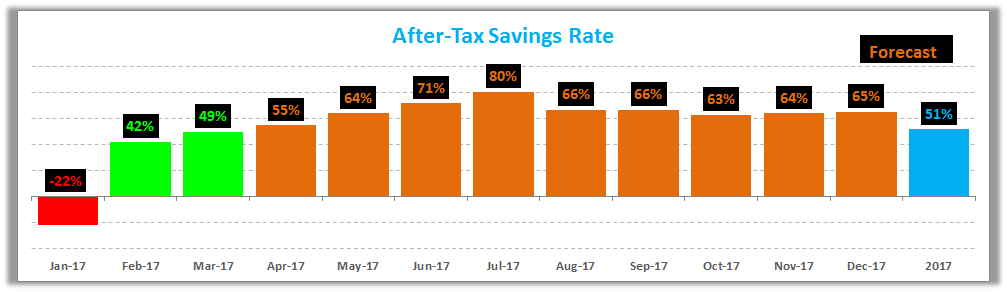

Savings Rate

Below is how we did vs. our goal of saving 50% of our after tax income.

You can see that although our goal for the year is 50%, we bounce all over the place on a monthly basis.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income. Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate. If you want to see how I plan to get there you can read all about it here.

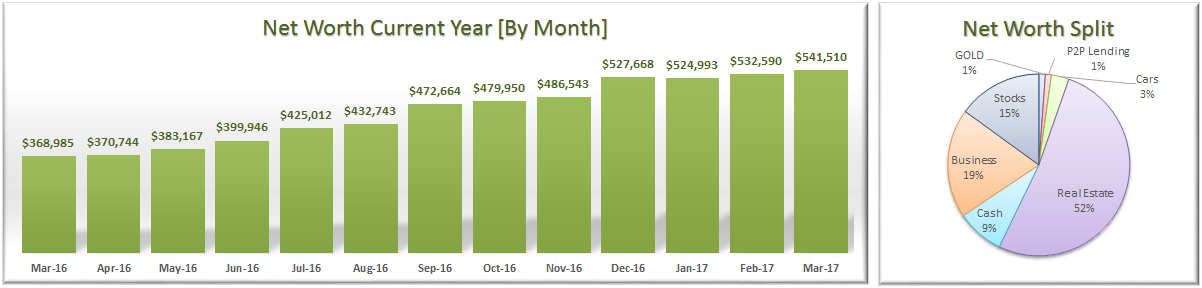

We are back in the black and set another new net worth high in March.

March Net Worth $541,510 (up +2.6% for 2017 YTD)

- Previous month: $532,590

- Difference: +$8,920

Net Worth is up 1,176% since 2012!

Net Worth Component Break Down:

In January, I added a new “Business” category that reflects our recent $105K equity investment.

You will also notice that I consolidated the split out of our primary residence and just lumped it all into the “Real Estate” category. However, we are still tracking this, I just wanted to keep the pie chart clean and easy to read. Our primary residence is currently sitting at 25.1% of our net worth.

The real estate category also now includes $57,000 I invested in hard money loans through PeerStreet. Only $7,000 of this sits in an after-tax account, while the remaining amount is sitting in a newly created self-directed IRA. Since I don’t need the cashflow right now, I figured it would be best keep the majority of my investment in a tax-sheltered account, especially since the gains are taxed at ordinary income rates.

And in case I have not spelled it out previously, the real estate category is also where our investments in commercial real estate (through Rich Uncles) live.

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote: Savings Rate – The Most Important Variable to Wealth Building [and the math to prove it]

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $299,126. It is nice to see it go under $300K.

The progress chart above shows how much of our goal we have completed. As noted above, we have put this on hold until at least June of 2017. However, we also want to work down our concentration risk, as our home equity position currently makes up 25.1% of our net worth. We would like to see this closer to 20% in the short term and far less in the longer term.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

10 Responses

Hey Dom,

The new layout looks really slick. I really like it – moving the menu to the top has opened some nice real estate for the content to spread out more.

Thanks for sharing this – I look forward to seeing how you are doing each month.

Erik

Thanks Erik!

We are still fine tuning, but I am really pleased with how the first phase has turned out. But yes, moving the menu to the top instead of fixed to the left side definitely opened up a lot of screen real estate. I originally did that menu structure because it was different from 99.9% of all the blogs I had ever come across. That with my cartoon helped me stand out early on.

When we pushed through the redesign I still wanted something different, which is why we have the post feed on top of the menu bar.

I am excited to see the site evolve to the next iteration after two years of its previous design.

Thanks for stopping by!!!

Another successful month in the books!

For simplicity in an asset pie chart it makes sense to lump primary residence with rentals. You are a financial wiz, so I don’t worry that you will start thinking of them as the same thing, but others might.

One is an expense (your home) and one is an investment (your rentals). Your home is not an investment, even if it does have a forced savings account (paying down the mortgage) and potential for appreciation. You pay for it every single month. With rentals done right, the tenant is paying every month.

But on the balance sheet, equity is equity!

Brian – It’s been a good run with 26 out of 27 months with positive gains to net worth since I started reporting it on the blog in January of 2015.

Maybe one day we will have a 3rd property in the real estate portion of the pie chart, but for now we are content with the single rental and investing through online real estate platforms like PeerStreet (Hard Money Lending) and Rich Uncles (Commercial REIT).

New layout is looking excellent! Keep up the good work 🙂

“Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.”

I don’t really believe in this too. I think I’m kind of in the middle. Don’t go crazy and wild on a shopping spree every weekend, but at the same time I don’t deprive myself if I want or need something. I do search for deals though. For example, I needed a new pair of jeans and my wife had a gift card with some money left over so I went to that store, and specifically was lucky enough to find my size and a nice color in the clearance section! So I guess I bargain splurged, lol!

Congrats on the great month again. Are you winding down P2P lending? I heard that a lot of people had negative experiences with those companies.

Thanks Troy! Yes, I am winding down my investments in P2P from the unsecured consumer market. However, my investment in this space was only about $6,000 at the height, and earned about 5% on average for the past few years. That said, I have put $60,000 to work with PeerStreet, to take advantage of the desirable asset backed market. Post with details to come soon.

Nice update and great overall progress on 2017 so far. Our net worth is currently at $546k but something tells me you guys are about to leave us in the dust! We made combined $290k in 2016 but 2017 is looking like $260k. I am hoping 2017 will be our last yoy drop for the foreseeable future! But who knows with my industry.

Nice grabbing lunch yesterday!

Sean

Thanks Sean! It was nice to finally meet up in person, I appreciate you making the time.

So we are only $5K apart now, it’s neck and neck, but didn’t we get this close one time before? Then you shot up a huge amount and left me in the dust 🙂

My spreadsheet has us growing out net worth to about $10,000 to $15,000 a month for the remainder of the year before any sort of gains from investments. I figure we should be well over $700K by January of 2018, unless the market takes a dive, which it very well could. I am more than happy to see the market correct!