I’M A DAD!

We weren’t expecting our son to make his debut until early November but he had other plans and came about three weeks early. I guess he got the memo that the theme for October was “finish,” so he decided to finish the gestation process and hit the eject button. Mrs. GYFG and I are completely infatuated with the little man. Yes, he looks like a little man. The good news is that he did give us enough time to complete the nursery and our office project so there were no loose ends even though he arrived early.

Last month I promised some photos of the completed nursery and home office project:

The only item left on my list to finish before the year is up is a book that I’m in the middle of reading (Tribe of Mentors

Although there was plenty of drama in the markets, we were pretty distracted by the excitement of welcoming our son into the world to take much notice. It wasn’t until I went to write this monthly update that I noticed that the extent of the recent market turbulence almost caused a decline in our net worth. The good news is that our 50% savings commitment still has the power to offset losses from the market and keep us in a position of continued growth. This marks the 45th month of growth out of the 46 I have published on this blog. Amazing!

If you’re a regular reader and only want to read the new content, feel free to just skip the intro below, and head to Net Worth. If you are new or haven’t read many of these reports, I encourage you to take two minutes to read the intro below, which will change periodically.

Intro

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

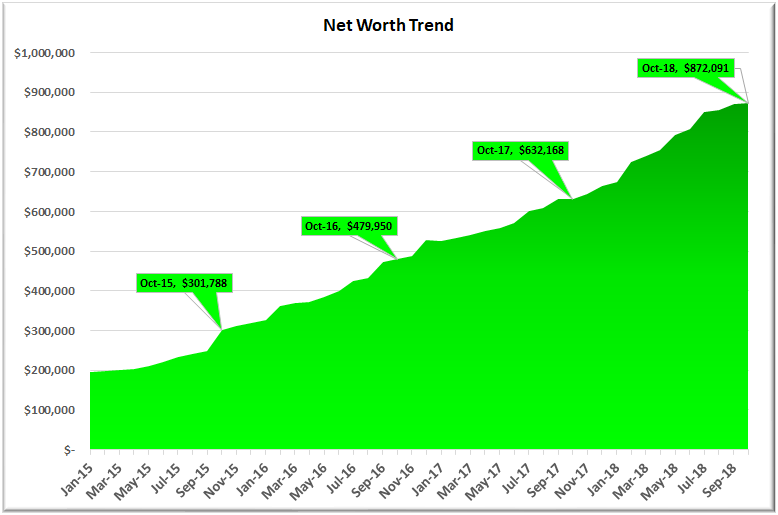

For those of you new around this corner of the internet, these monthly reports are about full transparency. They are just as much for me as they are for you. It was a hard decision to make all of my financial details public, but it has proved to be a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141, and our gross income was on pace to hit $178,000 that year.

Less than four years later, our net worth currently clocks in at $872,091 with a gross income over the trailing twelve months of $452,392.

- That’s a 4.4X increase in net worth due to a compound annual growth rate of nearly 50% for the past four years.

- At the same time, income has increased 2.4X, which translates to a compound annual growth rate of 28%.

Honestly, I don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will share our results with my readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle to only then have the means to check off bucket-list items when my body might no longer be physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. Choose to spend on what is meaningful to you. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. Keep this famous Jim Rohn quote in mind:

“If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!”

You must be intentional with your finances if you ever want a fighting chance to make it to financial freedom. But it does not have to take 40-50 years of slaving away for The Man before you have the option to retire. I think 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two of the vital components of a good recipe for the 10-year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not so many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, and I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere, so I have always intended to share my own.

You can find all my previous reports on the Financial Stats page.

Net Worth

Our net worth was up $1,935 in October vs. September. Compared to last October, our net worth is up $239,923 year-over-year (or +38%). An increase of less than $2K is not a rock star month but growth is still growth. And that’s after stocks took a bloodbath, declining 7% for the month of October. There will come a day when we reach an inflection point such that our ability to earn and save won’t be enough to fend off declines in net worth due to market moves of this magnitude but until that day comes we are going to milk this for all it’s worth.

We are still making a run towards a $1,000,000 net worth by the end of the year which will depend on two factors: 1. how the market performs during the last quarter of 2018; and 2. how the company that I work for and own stock in performs (I only revalue that position once per year).

October Net Worth $872,091 (up $207,700 or +31% for 2018)

- Previous month: $870,156

- Difference: +$1,935

Net Worth Break Down:

It’s back! Again. Below is a more granular look at the nuts and bolts of our net worth – a peek inside the sausage factory!

Fun Fact: I was curious to know what percentage of our net worth was after-tax vs. pre-tax. I did the math and found that about 30% of our net worth is tied up in pre-tax (or tax-favored retirement accounts) and that the remaining 70% is all after-tax.

The Real Estate category increased to 54% from 52%. This category includes the equity in our primary residence ($309,020), our investment in the Rich Uncles commercial REIT ($60,704), and our hard money loans through the PeerStreet ($104,331) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000.

The Real Estate category increased to 54% from 52%. This category includes the equity in our primary residence ($309,020), our investment in the Rich Uncles commercial REIT ($60,704), and our hard money loans through the PeerStreet ($104,331) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000.

Cash remained flat at 4%. We are currently holding $36,395 in cash. This is net of our credit card balances of $2,993 (finally down after an all-time high of almost $20K in August), which we pay in full every month based on the statement due date.

{kind=link}

As a clarification for newer readers, the Business category (at 13%) represents the ownership I have in the private company that I work for. I anticipate this increasing significantly by the time I update the value at 12/31/18. I expect the value of this will increase by at least $100,000.

Life Settlements remained flat at 9%. We currently have investments in seven policies at $10,000 each. They are accreting in value by about $1,000 per month. For anyone that is familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with a fixed return, you are amortizing (realizing) that value with the passing of time.

The Stocks category decreased from 19% to 18% and represents the cumulative value of our brokerage accounts (retirement accounts and after-tax account) that are invested in stocks. However, this is not all of our retirement money, as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $78,000 and are counted in the Real Estate category of the pie chart).

The Cars category remained flat at 2%.

Note: I include our cars because the goal is to keep the value of our cars as a percentage of the overall net worth pie as small as possible. By including them, it keeps me conscious of the opportunity cost of sinking too much capital into the machines that are only meant to get us from point A to point B.

Total Capital Deployed in 2018 (YTD):

One item not captured in the table below is the capital deployed due to automatic reinvestment of dividends and interest, but I do plan to include that total at the end of the year. I had originally estimated that we would deploy somewhere between $250,000 and $300,000 in capital this year. I recently revised my projection to $350,000 and we surpassed that this month. All I can say now, with any confidence, is that it will be less than $400K by the end of the year.

We deployed an additional $28,375 in the month of October, bringing the YTD total to $356,298. I played a bit of catch up on paying down the mortgage this month according to the plan I devised back in June to have it paid off by July 2019. We are currently $4,500 ahead of plan and are on schedule to be mortgage free in nine months!

I know I said I didn’t notice the market decline much but it did catch my attention long enough to put an extra $5,000 of idle capital to work, bringing the total deployed to stocks up to $10,000. We only have $10,000 left sitting in cash (in my 401K), which will be fully invested by the end of the year.

Through the end of the year I anticipate the following deployments on a monthly basis:

– $5,000 to Stocks (still have $10,000 left of $80,000 cash in a 401K to deploy, which I do monthly)

– $1,000 to Rich Uncles (working towards a $100,000 balance)

– $5,000 to $10,000 towards paying down the mortgage (we may defer this for a few months while we build up our cash balance)

So, we are looking at a minimum of $6,000 and a maximum of $16,000 of capital deployed for each of the remaining three months of the year. Mrs. GYFG is officially on maternity leave, which will impact our cash flow through January. We will adjust as necessary.

Gross Income

October income was down -9.2% at $32,672 vs. September of $35,981. With Mrs. GYFG going on maternity leave her income is going to drop by about 50% for the next three months. The good news in November is that it is a three pay period month for me, so we should see income remain above the $30,000 level. I see income dropping to around $25,000 in December.

In the second chart above, I also track our income on a trailing twelve months, and we set another record in October at $452,392 (that’s ten consecutive months of record highs). I think we can manage at least two more records this year but I do anticipate a dip sometime in Q1 of 2019. I currently have our income projected to finish 2018 at $454,718 (up slightly from last month).

Savings Rate

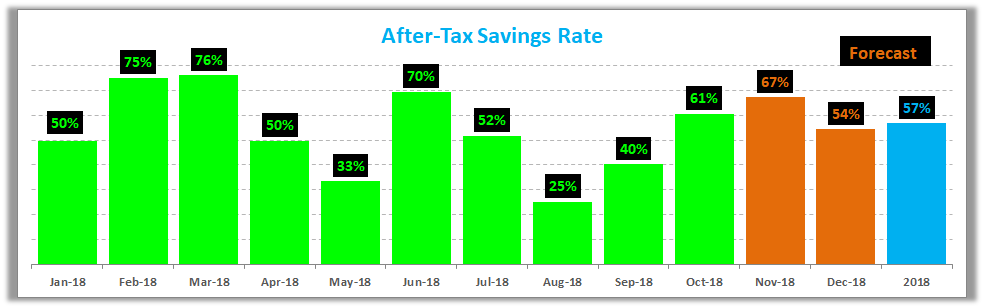

Below is how we actually did vs. our goal of saving 50% of our after-tax income.

I’ve updated the forecast through the end of the year and we are now tracking to a 57% savings rate – still above our 50% target. It was the combination of our high savings rate and diversification across asset classes that allowed us to deliver another month of positive net worth growth.

Speaking of savings rate, go check out my post where I mathematically prove the importance of your savings rate as a higher priority in achieving financial independence than your compound return! If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

After several refinances our mortgage is a 3/1 ARM at 2.25% and we currently owe $140,980. We had originally set a goal to pay it off in seven years and three months but recently accelerated that timeline by a few years. In the progress bar below you will notice that we were originally working towards a goal completion date of 1/31/2022, but are now aiming to have this goal completed by 7/31/19.

For the past few years, I have been writing about the desire to avoid concentration risk and ensure diversification, and therefore not rush to pay off our mortgage. But in June 2018 we decided to go after this goal hard and fast. Why the change of heart? The first major driver is the fact that our income has grown far faster than we had ever imagined in our wildest dreams. Based on the 20-year plan I shared on the blog back in 2015, our income wasn’t projected to hit current levels until 2029 – that puts us 11 years ahead of schedule.

Prior to the 2018 tax reform, the tax benefit we received from being able to deduct the interest and property taxes was already minimal. Under the new reform, there is zero tax benefit (due to SALT limit and the increased standard deduction to $24,000 for a married couple which is greater than our itemized deductions). I still don’t understand why anyone could be dogmatic about keeping a mortgage for the tax deduction, which is worthless under the new tax reform for most households across the USA.

Additionally, why would you spend a dollar on interest to get thirty cents back? Why not pay zero interest and keep 70 cents out of each dollar that you don’t have to pay towards interest? Our lightbulb moment came when we realized that we could get this accomplished in about a year, which became very motivating in light of Baby GYFG’s imminent arrival (the sweet boy is here). We feel this gives us a very strong financial foundation from which to spring into our next phase of life and wealth building.

This acceleration means that the equity value in our home will be growing rapidly over the next nine months, as will the percentage of our net worth concentration tied up in this asset. It currently makes up 35.4% of our net worth, and I anticipate it will make up as much as 40-50% of our net worth between now and July of 2019.

ONLY NINE MONTHS TO GO!!!

The original philosophy of this plan to pay off the mortgage was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. In keeping with the GYFG emphasis on the income side of our financial equation, I decided that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. This has not only proved to be true but it’s proved to be very conservative. To date, we have paid down the mortgage by $214,020 in less than four years.

This goal is now 60.3% complete (vs. 55.4% in September)!

Closing Thoughts

I will continue to leave the financial cruise control on through the end of the year. My focus has shifted to our son, and I plan to prioritize enjoying our first Thanksgiving, Christmas, and the New Year with him and Mrs. GYFG. November is also the month that I begin to think about my goals for the new year. Ideas have been percolating the past few weeks and I’ve finally landed on a theme for 2019. As I’ve done in years past, I plan to have my goals set by Thanksgiving, and this year I’m setting them around the five major F’s:

- Family

- Fitness

- Finance

- Food

- Fun

I will create one goal for each category and in the order of priority listed above.

Onward & Upward!

– Gen Y Finance Guy

8 Responses

Congratulations for becoming a dad! Our boy is the best thing ever. So much joy. But it is also so hard if you plan to be a stay at home dad.

In ER room right now bc he is sick.

Gotta roll with the punches!

Sam

Thanks, Sam!

He has changed our lives in so many ways (for the good). We can’t wait to show him the world (being the foodies that we are we can’t wait to help him taste his way through the world). We are only three weeks in but we are loving every minute of it. Unfortunately, I’m not quite to the point where I’m ready to be a stay at home dad, but a very involved one a part of my plan. I still have some financial goals to slay for the family. We have reached a point where work can be optional for Mrs. GYFG but she is not ready to close the door on her career just yet (she is next in line to take over the family business as the third generation). She plans to take three months and then go back to work four days per week for most of 2019.

The good news is that we have been grinding for years preparing for this day. We have much more autonomy in our schedules today and a lot more financial means to enjoy the many experiences we want to do as a family.

That said, we will continue to march towards our $10M goal by 48 (the year 2035). The good news is that our income is 11 years ahead of schedule based on the 20-year plan I shared in 2015 and our net worth should finish this year about two years ahead of schedule. No one can predict the future but if a few x-factors work in our favor we will hit our goal before 48. We will have our house paid off in another nine months and the investment engine will really be stoked with tons of cash.

I hope your boy gets well soon!

Thanks for stopping by.

Dom

Long time reader/lurker. Congrats Dom! Becoming and being a father is an incredible experience and journey!

Thanks, Jon! I appreciate you coming out from behind the darkness to leave your kind comment.

Such great news! So glad you have finished your office! It looks great! I know that flooring very well, and it will look that great for 30 years or more. Bookshelves are populated well already, with lots of room for pictures, trophies, maybe even a few aspirational objects for you and Mrs. GYFG to behold as you pass by. Not that you need suggestions, but you could do worse than a bottle of 1986 Chateau Lafitte Rothschild for you and the Mrs., and a 2018 to share with your boy Eduardo Ricardo Gerardo Leonardo in 2039. Also, congratulations on him, too!;-)

P.S. – spoiler alert: my takeaway from ‘Tribe of Mentors’, at 600+ pages and over 2 lbs., is the ‘weighted blanket’ and ‘binaural beats’ for sleep hygiene. You will have to tell us yours!

Hi JayCeezy!

The office really turned out great. I actually just hung up that Slight Edge poster you might have noticed in the background (as well as our framed degrees from our respective alma maters).

You’re right there is plenty of room in the bookshelves for more books and other items you mention. I like the idea of aspirational objects. I will for sure get something to share with our boy (I LOL’d out loud when you brought up your suggested name from earlier in the year – hate to say it but it didn’t make the cut 🙁 ).

Re: Tribe of Mentors

I will try to remember to share my takeaways but I have a feeling you will hold me accountable. I will say I have added a lot of books to my Amazon reading list. I also have a fun post about this book coming up in the next couple of months, probably the perfect place to include my takeaway(s).

Congrats on becoming a father Dom! It must be such an exciting time. I remember when I brought home my newborn son- it changed my life forever. Can’t believe he’ll be entering high school in a couple of years. Your net worth is coming along nicely. Hope you can join the double comma club this year. The service is better and the drinks are stronger;)

Thanks, Millionaire Doc! We are still trying to soak it all in. We still have to pinch ourselves to check that ensure we’re not dreaming. We are absolutely smitten with the little man.

I hope to become a card-carrying member of the double comma club in December – save me a seat at the bar!

Dom