GYFG here checking in for the May monthly financial report. For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you are happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living and average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte if you choose.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities. Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, and progress on the mortgage pay down goal.

Can I ask you for one small favor before you continue reading? Could you use one of the icons to the right of this post to share it on your favorite social media channel to help spread the word?

Thank you, thank you, thank you soooooo much!!!!

Shall we begin?

Summary of May 2015

What went down in May

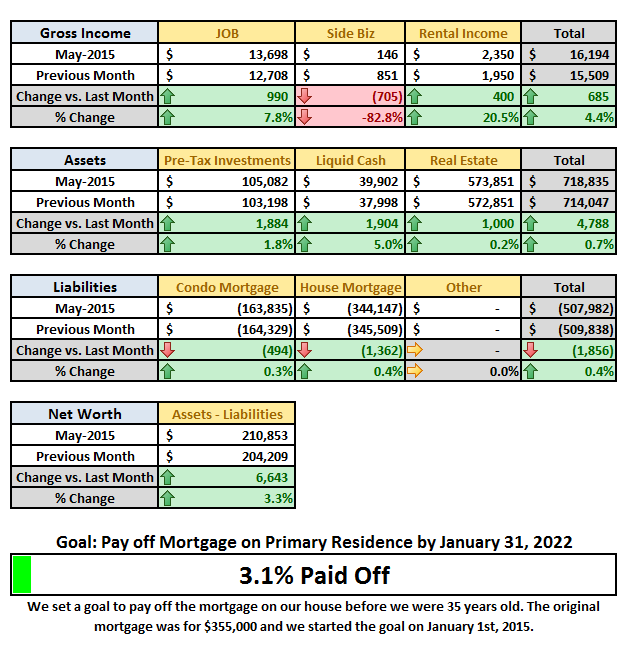

During the month of May gross income was up 4.4%. This past month my wife was kicking ass and taking names. She earned an extra $1,000 as she continues to grow her book of business. The hard work and business coaching is really starting to pay off. I am so proud of her. The other item of note that contributed to the increase in income was an extra $400 in rental income that resulted from renting out another room in our house for a month. However, this was partially offset by a $700 decrease in side biz income (which is really anything that is not JOB income or rental income).

May’s income does include $133 of income that was paid in May. Since monetizing in March, the blog has produced $341.67 in revenue. But don’t worry, I will be detailing all that and more in a separate blog update where transparency will still be the name of the game. I am sure you guys have seen a lot changing and I want to share the results with you all – especially those that are currently blogging or those that are thinking about blogging. You can learn from my successes and my failures. Let me be your blogging and financial guinea pig.

On that same note I am in the process of writing that EPIC blog post and an expanded eBook on “How to launch, grow, and monetize a blog.” The post will probably land somewhere around 5,000 words and the eBook will be 20,000 to 30,000 when complete. Both will be very detailed and full of screenshots and visuals. I am going to be giving a bunch of copies away for free, but you have to be on my email list to participate.

So it is probably a good time to take a break and join the email list real quick to make sure you get a shot at getting your free copy.

May Income = $16,194

- Previous Month: $15,509

- Difference: +$685

In July I anticipate a nice spike in income due to semi-annual bonus payments and a 3-period pay cycle (I get paid on a bi-weekly schedule). We could see income jump to as high as $22,000 in July.

Now where did all that money go?

The last four months have been very high with regard to expenses due to some planned and some unplanned expenses. I THINK I can finally say that our “one-time expenses” are behind us. If you want to see what I mean you can go look at the prior four reports here: January, February, March, and April.

Home Mortgage & HOA $3,233 The normal payment is $2,215/month for the mortgage and $84 for the HOA. However, as a part of our 7-year mortgage pay off plan, we started adding an extra $800/month towards principle. May was the first month that includes a higher amount to cover property taxes. For the next 12 months, or until my wife is able to contest the new appraised value on the tax roll, we will be paying an extra $134/month to our escrow account. Next year I will probably request to get rid of the escrow account and take care of property taxes on our own instead of prepaying them.

- Previous Month: $3,099

- Difference: -$134

Condo Mortgage & HOA $1,138 This is the payment on our rental condo and includes the mortgage of $888 and HOA of $250. We currently rent this place out for $1,350/month, as seen in the summary table above. In April we had to pay property taxes of $1,125 (thus the savings in May), since we don’t have an impound account set up to collect this on a monthly basis (we prefer it this way).

- Previous Month: $2,263

- Difference: +$1,125

Timeshare $0 My grandparents left me their timeshare before they passed away. This is a quarterly installment of the annual maintenance expense. I typically just rent it out for enough to cover the annual maintenance fees. I haven’t placed it with the property management company yet, but this reminds me that I should probably get on that soon. It’s not likely that we will use it this year. I really only hold onto it because I can cover the cost by renting it out and it’s in Vegas on the main strip between the Bellagio and the Cosmopolitan. My bet is at some point one of those hotels is going to offer a buy out to tear the thing down.

- Previous Month: $190

- Difference: +$190

Home Improvement $785 We don’t have any other big projects planned this year (February was the big one with the cabinets in the garage and my wife painting the interior of the house), which will be good for our savings plans. However, we had more spending than I expected here. We spent $270 for drought resistant plants for the backyard, $320 at Lowe’s & Home Depot mostly for new fixtures around the house, and $195 between Home Goods and World Market for a new place setting on our formal dining room table.

- Previous Month: $262

- Difference: -$523

Food & Dining $1,651 This amount includes money we spend at the grocery store, dining out, drinking out, and dog food/treats (our two dogs eat well). In the month of March we spent $781 on groceries, $56 on dog food, and $814 on eating out at restaurants. This is an expense that tends to get a little out of control for us. Last year we spent $14,000 on eating out or almost $1,200/month on average. The goal for 2015 is to keep this combined expense at or below $1,200/month; $500 for eating out and $700 for groceries. It’s evident in our restaurants category, but thought I would point out that we did get to try a few new places this month 🙂

- Previous month: $1,085

- Difference: -$566

Shopping & Other $1,537 I could break this out into other categories, but in all honesty I am lazy and don’t really want more than what I currently have broken out. But here are the big expenses: $80 wedding gift, $240 for our dogs (annual registration, shots, and toys), my wife got her hair colored $150, dry cleaning $28, my wife got her first pair of cowboy boots $200, house warming gift $260, skin care products for the wife $223, Costco $83, and misc. entertainment $273.

- Previous month: $401

- Difference: -$1,136

Travel & Hotel $500 I have a friends bachelor party coming up in July. We are staying in a house on the beach and had to book it early to secure our reservation. This was my portion of the rental and dinner out one night.

- Previous month: $0

- Difference: -$500

Auto and Transport $636 This includes fuel, car insurance on two cars, and toll roads. This month I have a few more services that I need to get done on my car that will likely inflate this expense next month, but you need to keep up with the routine maintenance so you don’t end up spending more than you need to by letting things break.

- Previous month: $1,186

- Difference: +$550

Personal Development $0 Not much else planned here for the rest of the year. This will likely fall off the report next month or I will leave it as a zero.

- Previous month: $2,250

- Difference: +$2,250

Bills & Utilities $468 This includes our monthly utilities like gas, electric, water, internet, and cell phones. Our internet did increase by $20/month since we are our of the promotional period. I may try and call to see if they will lower it if I threaten to switch providers. Otherwise not much to say here.

- Previous month: $412

- Difference: -$56

Health & Fitness $223 This includes a monthly massage subscription, monthly dues to remain an active member of Team Beachbody to ensure my discounts on supplements like Shakeology and Results and Recovery Formula. And a new order of Shakeology that should be here any day.

- Previous month: $164

- Difference: -$59

Business Services -$43 I actually got a credit this month as a result of switching my hosting services. I had previously prepaid 3 years up front, so I was refunded a prorated portion of this since I switched hosting companies. There will be an entire post on this 🙂

- Previous month: 65

- Difference: +$107

Total Expenses $10,128

- Previous month: $11,477

- Difference: -$1,349

Expenses came in a bit higher than I expected, but so did income, so they basically cancel themselves out. Although our spending was down by $1,349 vs. last month, we still spent about $1,900 more than I had expected. You know what they say “easy come, easy go.”

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

- Our mortgage payment is automatically set up to pay $800 in additional principal.

- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- We have an auto investment of $500/month into my wife’s IRA to make sure we max it out by year end ($5,500)

- At the beginning of the month I have been sending $1,000/month to a REIT investment.

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

What were Investments and Contributions?

I currently work for an employer that offers a 401K with matching. For years now, I have taken advantage of maxing out my 410K for both the tax benefit and company match. This works out to be about 16% of my income off the top before I ever even see my paycheck.

My wife happens to work in a family business and unfortunately they are not able to offer a retirement plan, let alone matching. So starting in 2014 we opened up an IRA for her that we plan to max out with $5,500 every year. Starting with February of 2015, we have set up an automatic contribution of $500/month.

I also have an IRA due to a 401K rollover from a previous employer. I personally wish I could have all my retirement money in my TD Ameritrade IRA account because of the unlimited investment choices and the ability to invest in many different asset classes, including options.

Now lets take a look at what activity went down this month:

- Contributed $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $500

- Difference: $0

- Contributed $1,169 Into my 401K. The normal contribution will average 16% for the year, but I do play around with the percentage occasionally.

- Previous month: $1,169

- Difference: $0

- Prosper Lending $0 We will probably make another $500 to $1,000 deposit here in June or July.

- Previous month: $0

- Difference: $0

- Rich Uncles REIT $1,000

- Previous month: $500 (I missed this last month)

- Difference: +$500

- Increase in Savings $1,904 This includes checking, savings, and CD’s. Almost back up to the $40K mark (where we like to be cash wise).

- Previous month: $0

- Difference: +$1,904

Total Investments & Contributions $4,573

- Previous month: $2,169

- Difference: +$2,404

Summing it all up against the Gross Income

Benjamin Franklin famously said, “that everything has a place and that everything should be put in its place.” With that, let’s summarize where the total gross income for the month of May went.

Gross Income $16,194

(Less) Expenses* $10,128

(Less) Investments & Contributions $4,573

Sub-Total $1,493

(less) Taxes & Benefits $1,493

Total = ZERO

Everything is accounted for (phew!).

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income. Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate. If you want to see how I plan to get there you can read all about it here.

May Net Worth $210,853 (with five months down in 2015, this puts us up $29,489 or 16.3% vs. 2014 so far and we still have 7 months to go)

- Previous month: $204,209

- Difference: +$6,643

With a year to date net worth gain of $29,489, that puts us slightly ahead of target. Recently I published a post where I outlined our goal to increase our net worth by $69,000 in 2015. We are officially 42% through the year and have reached 43% of our goal.

One of the other huge goals that I announced on the blog was the strategy to pay off our mortgage in 7 years. When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 2.7%, which means we picked up another 40 basis points in May. At this rate we will be 5.9% complete with this goal at the end of 2015 (assuming no extra lump sum payments).

The End

Both expenses and income came in higher than I expected. Last month I said, “we should see savings increase and net worth should be increasing by about $6,000/month or more (starting in May that is).” At the end of the day net worth is the ONE METRIC THAT MATTERS, and we had an increase of almost $7K in May. I am totally happy with that.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 20-25 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list below or at the top of the page and I will send you a copy.

- Mint.com (free) – Mint is great for setting up budgets and automating the tracking of your actual spending habits vs. the budgets you set.

- PersonalCapital.com (free) – This is like Mint, but is geared towards investments and net worth tracking.

24 Responses

Nice job in May! Always great to see the income side of the puzzle going up!

Thanks FF.

Indeed, it is always refreshing to see income climb. I think the next couple months should be pretty solid. If we can just keep spending in check, we should see some nice gains in NW.

Hope you had a great May!

Well done GYFG and wife! Your income growth has definitely been impressive. Do to my goals, side hustling would be really advantageous for me to start right now. However, my most lucrative skill is not my favorite to practice, so I’m trying to think of ways to monetize secondary skills.

Hey Hannah,

So excited to see my wife kick ass and take names.

What is your most lucrative skill that you prefer not to utilize?

And of the secondary skills, what ideas are you kicking around?

Cheers!

My most monetizable skill is building predictive analytics into software applications (an oddly specific and not that fun of a skill). I could probably earn $100/hr gross using oDesk or eLance. If I could come up with my own concept and I properly marketed it, I really think the market cap is so high that it makes $100/hr seem like pimping for pennies.

That said, the business I would really prefer to build is a quantitative marketing consulting business. Helping small businesses integrate reporting and analytics and website design into their processes to generate higher quality sales leads- I think you did something similar actually. I just have a few skills gaps in that area.

Sounds like you have some pretty awesome skills and I think the parlay of your skill set sounds like a very profitable one. Data driven marketeers are very much in demand.

Cheers!

Dude, nice job in May! Any month where my net worth goes up 3% is a good month!

Glad to hear you have the same plan as me for mortgage pay-off by age 35. I can only imagine how cool it’s going to be to have all that extra money to play with or invest with a young family.

Heck, just investing that mortgage payment (at 10%) for the next 25 years after pay-off gets you $2.4M of your $10M goal.

Keep up the good work and keep us posted!

Thanks Kevin!

If everything goes well we should see 2-4% gains throughout the rest of summer in Net Worth.

Yep, marching forward on the mortgage payoff before we are 35. The conservative plan is 7-years, but my stretch goal is 5 years. The trick though is to keep equity from the primary residence at less than 25% of total net worth. That is not a problem this year, but based on the planned I outlined in a previous post it could become more difficult: https://genyfinanceguy.com/2015/01/16/the-mortgage-snowball-strategy-to-pay-your-mortgage-off-in-5-7-years

Cheers!

Hey GYFG,

Great numbers for the month of May.

It is great that the MS; her jobs starts to work. It adds some nice income.

The mortgage is going good as well. You will beat me to paying it back (I decided to keep it at 9,5 years, due to tax reasons).

It is amzing that next to the job, family, investments and blog, you still find time to have bachelor parties. Enjoy the party

Thanks Amber Tree!

May was a good month for sure. Stoked that my lady is starting to see growth in her business. It is awesome to see her excitement as a result of her success.

Luckily the bachelor party is local and with a pretty mellow crowd. We will be renting a house by the beach. This is actually a bachelor party I am looking forward too 🙂

Cheers!

Hello!

My fiance and I are also trying to make our way through FI and I just started on my monthly breakdown (albeit on pen & paper)

Maybe I’ll get the courage to actually post it in a blog!

Keep your posts coming! I always love reading about how other people make FI work.. at the rate we’re saving, it looks like I can reach FI when I’m 46 (eeep, a bit late in the game, as I also started late :S)

Right on Ruby. I always tell people that you can’t optimize what you don’t measure. And there is a saying floating around there somewhere that says, “the thing that gets measured is the thing that gets managed.”

46 is still young. Keep us posted 🙂

That was a pretty good month!

I hope you manage to get those food costs down a bit! It is amazing how once nice meal out can get pricey when you add wine and apps to it.

Looking forward to the update about monetizing to see what has worked for you so far.

Yes, it was a good month overall. Still was a bit surprised on some of the spending.

The food budget does have a tendency to get a little out of hand for us. I think it should be under check this month, and hopefully balance out for the year around $1,200/month in total for groceries and dining out.

The material is taking me a while to write. Mostly because I am also writing an eBook to release with the post I have mentioned in the last two financial reports.

In short the following are working:

1 – Affiliate sales through Personal Capital & Amazon Associates

2 – Ad Revenue – currently using 3 different networks and making them compete for space on my site.

I am not getting rich by any stretch of the imagination. But the blog is more than paying for itself and I am looking forward to growing and integrating further strategies into the mix.

If you ever have any specific questions don’t hesitate to reach out: mrgenyfinanceguy@gmail.com

GYFG,

I love watching you build that empire. Way to kick ass last month! I am eagerly awaiting for you to blow through 20k in a month. You’re getting close.

MDP

Thanks MDP!

But I can’t take all the credit, the wife is kicking some ass as well on the income front.

Cheers!

Man, love the way you think about finances, especially on the earning more income.. I must say that I like doing offense & defense financially although I spend consciously where I can on stuff that I enjoy i.e. holidays etc

Liking your journey here & enjoying the value and different perspectives you’re adding out there!

Hey Jef – I think you have to do a bit of both. My stick is really to just follow the 80/20 rule. I spend 80% of my efforts trying to focus on increasing income and the other 20% on keeping expenses in check. However, I will be the first to admit that the Mrs and I do live a pretty good life and to spend a bit of money on the things we enjoy.

Agreed man! It’s all about what works & I feel I’m quite similar to you 🙂

What’s the point of reaching the top of the mountain if you have no-one to enjoy the view with right..