The year is officially 25% complete. I can honestly say this is the post I get most excited about writing each and every month.

These reports are a way for me to track my progress and stay accountable to my goals. But it’s also one of the many ways I try to humanize finance for all of you reading this blog. By the way, in case you missed it, we do have a mission statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs do this). I publish all of my financial details not to brag, but instead to show you what is working, as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities. Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, and progress on the mortgage pay down goal.

Shall we begin?

Summary of March 2015

What went down in March

During the month of March there was another downtick in income. This is almost entirely due to the final payment ($720 received in February) related to the side hustle I recently shut down in order to focus my efforts on this blog. It was a great year-long project that brought in $18,000 in extra income over the course of 12 months. I effectively earned about $100/hour and essentially got paid to learn a valuable skill set that I plan to leverage in growing this blog.

March Income = $15,057

- Previous Month: $15,711

- Difference: -$654

Going forward, gross income should come in around $15,000 a month from April through June. In July I anticipate a nice spike in income due to semi-annual bonus payments and a 3-period pay cycle (I get paid on a bi-weekly schedule).

Now where did all that money go?

Something to keep in mind as you read through the expense portion of this report is that although we have a high income, we are not extremely frugal. We try not to waste money on things that do not bring us joy, but we definitely don’t try to live like college students. A lot of blogs in the personal finance space are very expense focused, where I tend to put more energy and focus on the income side of the equation. This blog is definitely not a blog about frugality. If you are looking for that you should checkout Mr. Money Mustache and The Frugalwoods, they cover this topic very well, and they are very good examples of what it means to be truly frugal.

At the end of the day we try to spend less than we make. This happens most months, but there are a few months of the year where it doesn’t. We try to balance living in the present while planning for the future. As long as we hit our financial goals we do not feel guilty for the money we spend. This year the goal is to increase our net worth by $70K (as you will see below we have already increased it by about $20K so far this year)

Sorry!! I felt like I needed to make that extremely clear, now we can continue as usual.

Home Improvement $245 We don’t have any other projects planned this year (February was the big one with the cabinets in the garage and my wife painting the interior of the house), which will be good for our savings plans. However, there will always be small projects that hit now and then. All of this expense was related to expenses that were charged on our Home Depot and Lowe’s credit card that I missed last month (which reminds me, I need to go link those up in my Personal Capital account, okay I’m back).

- Previous Month: $4,796 (one-time expense in 2015)

- Difference: -$4,551

Home Mortgage $3,015 The normal payment is $2,215/month. However, as a part of our 7-year mortgage pay off plan, we started adding an extra $800/month towards principle. I actually just got notice from our lender that our payment will be increasing because our escrow account is underfunded. So in order for the bank to catch up, the payment has to increase by $134 starting in May. This will make our new “normal” payment over the next 12 months $2,348.76 and then it will drop down to $2,276.80. This means in order to continue paying an extra $800 towards principle I will be increasing this payment in May to $3,149. At some point we should probably remove the impound account and just pay this ourselves.

- No change vs. previous month.

Condo Mortgage & HOA $1,138 This is the payment on our rental condo that is just 10 miles from our house. We currently rent this place out for $1,350/month, so we have a small but nice positive cash flow of $117/month after our $95/month property management fee.

- No change vs. previous month

Note: I had previously stated that both mortgage payments were inclusive of property taxes, but after my wife read the February report she reminded me that the condo payment does not include the property taxes and that we will be paying $1,200 in April (dang it). Property taxes run $583/month on the home mortgage and $200/month on the condo.

Update 4-6-15: Hannah made a good point in the comments below. I had previously calculated the positive cash flow based on the assumption that property taxes were included. However, since being corrected this actually puts us at a slight negative monthly cash flow of $83/month. That be said, we still have a tenant that is amortizing our loan by almost $500/month, and the tax benefits of the property that still make it a good hold in my opinion. I would love for it to be better, but our timing on buying was not the best.

Lastly, as I explained to Hannah below, we look at this as our plan B if we absolutely fail at life we at least have a cheap option for housing in the Condo.

Food & Dining $1,361 This amount includes money we spend at the grocery store, dining out, drinking out, and dog food. In the month of March we spent $679 on groceries, $134 dog food, and $548 on eating out at restaurants. This is an expense that tends to get a little out of control for us. Last year we spent $14,000 on eating out or almost $1,200/month on average. The goal for 2015 is to keep this combined expense at or below $1,200/month; $500 for eating out and $700 for groceries.

- Previous month: $1,151

- Difference: +$210 (I am okay with the increase, we are within range)

We didn’t move closer to $1,000 in this category like I thought was a possibility in February’s report. But it is within range, so I am not worried about it.

Shopping & Other $499 I paid for a workout program for my mother in-law ($60), my wife got her hair colored ($120), we bought some stuff for the house ($100), I bought a few books (Choose Yourself, The One-Page Financial Plan) and a newsletter ($40), Target ($60) for a gift, some camping gear ($32), and other misc. ($87).

- Previous month: $1,356

- Difference: -$857

No membership payments this month (we only have two remaining, after canceling the others last month). As expected we saw a huge decline in spending in the general shopping category this month.

Travel & Hotel $0

- Previous month: $0

- Difference: -$0

Auto and Transport $459 This includes fuel, car insurance on two cars, and toll roads.

- Previous month: $593

- Difference: -$134

Personal Development $2,250 You may remember that last month I mentioned that my wife would be starting some business coaching that was going to be a total cost of $4,500 for 6 months’ worth of coaching. We are paying it in two installments, with the first installment paid in March and the final installment in April. This is an investment in my wife and her career. We are more than happy to make investments in ourselves. It saved us $300 to make two payments, instead of making monthly payments of $800/month.

- Previous month: $0

- Difference: -$2,250

Bills & Utilities $481 This includes our monthly utilities like gas, electric, water, internet, and cell phones. Not much to say here.

- Previous month: $400

- Difference: +$81

Health & Fitness $167 We made some cuts as planned from last month’s report. This is mostly for massages, but also includes monthly dues to remain an active member of Team Beachbody to ensure my discounts on supplements like Shakeology and Results and Recovery Formula.

- Previous month: $180

- Difference: -$13

Business Services $0

- Previous month: 0

- Difference: $0

Total Expenses $9,615 (I projected $10,000 in last month’s report)

- Previous month: $13,222

- Difference: -$3,607 (better than the $3,250 I thought we would be down when I wrote February’s report)

We saw expenses come down substantially during the month of March, which was nice to see.

However, we are not out of the woods yet. Next month will see one more spike in expenses before our cash outflow decreases significantly. We will have the final coaching payment of $2,250.

As I have mentioned on this blog before, my wife is in a family business that she intends to grow and one day take over. So this is an investment in her professional development, our future, and the future of the business. We are big fans of making investments in ourselves-the ROI is huge!

We also have both income taxes ($2,200) and property taxes on the condo ($1,200) that are due in April.

After factoring in the taxes I mentioned above, we can expect an increase to spending of about $3,400 in April vs. our March spending. I am projecting spending to come in right around $13,000 in April.

May will be the month where we really reign in the spending and crank up the savings. Not exactly what I want to be reporting, but it’s the reality. I would like to see savings of $2K to $3K a month starting in May (in after tax savings that is). The pre-tax savings happens no matter what!

What were Investments and Contributions?

I currently work for an employer that offers a 401K with matching. For years now, I have taken advantage of maxing out my 410K for both the tax benefit and company match. This works out to be about 16% of my income off the top before I ever even see my paycheck.

My wife happens to work in a family business and unfortunately they are not able to offer a retirement plan, let alone matching. So starting in 2014 we opened up an IRA for her that we plan to max out with $5,500 every year. Starting with February, we have set up an automatic contribution of $500/month.

I also have an IRA due to a 401K rollover from a previous employer. I personally wish I could have all my retirement money in my TD Ameritrade IRA account because of the unlimited investment choices and the ability to invest in many different asset classes, including options.

Now lets take a look at what activity went down this month:

- Contributed $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $500

- Difference: $0

- Contributed $1,169 Into my 401K. The normal contribution will average 16% for the year, but I do play around with the percentage occasionally.

- Previous month: $1,215

- Difference: -$46

- Prosper Lending $0 I was supposed to start contributing capital here this month, but put it off until April (which has been done before this post goes live)

- Previous month: $0

- Difference: $0

- Increase in Savings $300 This includes checking, savings, and CD’s. This is where I want to see the increase of $2K to $3K a month I mentioned above.

- Previous month: $1,592

- Difference: -$1,592

Total Investments & Contributions $1,969

- Previous month: $1,715

- Difference: +$254

Summing it all up against the Gross Income

Benjamin Franklin famously said, “that everything has a place and that everything should be put in its place.” With that, let’s summarize where the total gross income for the month of March went.

Gross Income $15,057

(Less) Expenses* $9,615

(Less) Investments & Contributions $1,969

Sub-Total $3,473

(less) Taxes & Benefits $3,473

Total = ZERO

Everything is accounted for (phew!).

* I will point out in case it wasn’t clear in the expense section above; the expenses include an additional principal payment of $800 on our primary residence.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income. Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate. If you want to see how I plan to get there you can read all about it here. However, March is a new milestone as we cross over $200K for the first time.

March Net Worth $201,054 (with three months down in 2015, this puts us up $19,690 or 10.9% vs. 2014 so far and we still have 9 months to go)

- Previous month: $196,990

- Difference: +$4,064

With a year to date net worth gain of $19,690, that puts us ahead of target. I have a post that is scheduled to go live in a couple of weeks where I outline our goal to increase our net worth by $69,000 in 2015. We are officially 25% through the year and have reached almost 29% of our goal (I just jumped up and down in excitement).

(Mr. CEO here – when he says “jumped up and down in excitement,” I want you to also know he’s taking selfies while he’s doing this)

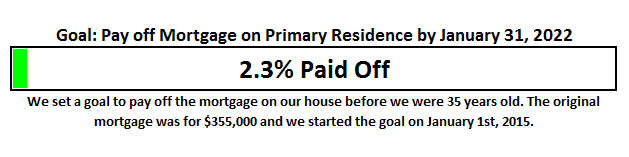

One of the other huge goals that I announced on the blog recently, was the strategy to pay off our mortgage in 7 years. When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 1.9%, which means we picked up another 40 basis points in March. At this rate we will be 5.9% complete with this goal at the end of 2015 (assuming no extra lump sum payments).

The End

March was a better month than February overall. April is shaping up to be a lot like February. May is the magical month. We should see savings increase and net worth should be increasing by about $6,000/month or more (starting in May that is).

Every month you get to see that I am not superhuman and have my own financial hurdles to work through. I don’t particularly like spending more in a given month than I bring in. Although our income is high, I still think that our spending has room for improvement. We’re not going to make these changes over night.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 20-25 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less.

I am looking forward to chatting with you all in the comments below. Anything I should elaborate on? What can I add that would help you take action? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

TD Ameritrade – They are hands down the best broker for the retail investor. TD Ameritrade provides a number of investing platforms that are more robust than any other platform I have ever used. My particular favorite is the “Think or Swim” platform. Oh and did I mention that they have over 100 ETFs that you can trade commission free?

They also provide a ton of educational resources that are again all free to you. You will also have access to stocks, options, futures, and forex all on a single platform. And if that wasn’t enough, they will let you invest commission free for 60 days while you test drive the platform and they will give you up to $600 for rolling over your other accounts.

My special offer to you: If you sign up for an account using the links I provided on this post, I will send you a video that gives you an over view of the Think or Swim investing platform and I will even show you how easy it is to execute your first covered call. All you need to do is sign up using the banner below or the TD Ameritrade link above, then send me an email at mrgenyfinanceguy@gmail.com

38 Responses

Man your not playing around on those personal development costs. I’ll be curious if you decide the outcome was worth it.

It is certainly a serious investment. Maybe I will be able to convince my wife to write a post once she completes the 6-months worth of coaching.

But I can honestly say that I am already seeing a difference in her mindset and attitude towards her ability to take over the family business.

She is working with a respected real estate professional with 20 years in the business.

The escrow business is very much a relationship business and I think this is exactly what she needed to get her through the dip. Meaning it takes time to build relationships before deals start happening.

I have no doubt that the investment will pay off in both the short and long term. The short term benefit will be harder to measure in terms of ROI. But longer-term it will prove money well spent.

Cheers!

I think the word is already out that you are not Mr Frugality! I agree with your paragrpah addressing that though. There is a spectrum of frugality levels with MMM, ERE, etc on one end and the general public on the other. I prefer, like you, to be somewhere in the middle. That let’s us accelerate retirement, but still do things we enjoy. Not everything has to be a competition for how low the expense can go.

Are you going to get the wife’s IRA maxed once the one-time expenses are out of the way? I know you will max either way, but do you like to front load when possible?

Hey Vawt,

I know it was probably pretty obvious from my financial reports alone, but I just wanted to be sure to clear the error in case there was any doubt. Plus it was also a great opportunity to promote other great blogs doing a great job in leading the people interested in Extreme Frugality.

Personally, I find extreme frugality to be as sustainable as extreme dieting. I don’t know anyone including myself that has ever gone on a very restrictive diet only to binge at some point. That doesn’t mean those people don’t exist of course. Maybe I just don’t have the kind of discipline it takes. Or I am not willing to make the sacrifices. Or maybe I just don’t have the will power.

Luckily for guys like us in the middle there is still a path.

I haven’t given much thought to front loading my wife’s IRA. But since you pose the question…I probably will just keep it at $500/month to max out by the end of the year. The only thing that would cause me to deviate from this plan would be a 10% correction in the market place. I have a hard time front loading with the market at all-time highs. Maybe I think I am clever 🙂

Plus I just added another automatic transfer of $500/month in order to dust off my old Prosper account that I opened back in 2010, but have not used in a couple of years (in terms of new capital).

Cheers!

If your condo is netting $95/month and you haven’t accounted for $1200 in taxes, then you are slightly cash flow negative. Are you considering selling the unit and deploying the capital elsewhere?

We had a unit that was making us about $100/mo, but then our HOA increased, and we had a few small maintenance tasks come up, and we realized that we would be much better off with intentional real estate. Since that time, our $100 has become $650 a month.

Good point Hannah! When I was calculating the positive cash-flow of $117/month I had thought it included the property taxes that just jumped up from about $160/month to $200/month based on a reassessed value by the county. So that does put us at a slight negative of about $83/month.

However, we still have a tenant that is amortizing our loan by almost $500/month and a nice tax benefit with the depreciation of the property. We also look at this property as our plan B. If we absolutely fail at life, we are very confident that we can afford a $1,000/month mortgage.

One thing we have discussed though is to refinance the property to improve the cash-flow. But so far we haven’t pulled the trigger either way.

Glad you guys were able to redeploy capital and improve the cash-flow. Good work!

Cheers

GYFG,

With your income it is inconsequential whether you have $100 positive or $100 negative cash flow. Eventually your rent will increase over time so I personally would take the same path you are taking with the primary residence. Make an extra $500-$1000 in payments on your rental and treat the outflow no different than investing in your 401k. Now instead of a couple of hundred dollars passive income 10 year from now all the rent would be bankable.

Just my $.02

MDP

Agreed MDP!

We are not going to get rid of it.

Its funny you mention this because my wife just suggested the same thing. We are actually considering paying extra money over here as well. But I think I would like to refinance it to improve the cash flow but then continue amortizing it at an accelerated rate. That way if something happens to our income and we need to stop making extra payments, we are at least cash flow positive and can use the positive income if needed.

Thanks for your input. It is much appreciated and valued.

Cheers!

Thank you for sharing your monthly expenses. Your food budget is impressive. Here’s a thought cut it down to $600 and put the savings on your mortgage. It would speed up your pay off plan.

Hi Sue,

Thanks for the idea. However, the idea behind the accelerated mortgage pay down is what I call the “Pay More Later” strategy. The idea was to focus on increasing our income instead of decreasing our expenses. Or put another way we wanted to have our cake and eat it too. At this point in time we don’t want to throw any more than the extra $800/month at the mortgage. At least not until January of 2016 when it will jump to $1,600/month extra.

We love our food way too much to basically but out our entire budget for dining out and hosting people over at our house.

But no doubt if we were willing to make a few more sacrifices we could definitely speed up the pay off of the mortgage.

Thanks for stopping by.

Cheers!

Don’t worry GYFG, even though you are a spendy-pants, I’ll still read your blog! 🙂 That’s what’s great about this community is there are blogs which focus on income taxes, frugality, side-hustles, etc. The variety is the best part, and everyone is free to steal the ideas from each that work best for them. Congrats on the $200k club!

Thanks FF!

We are definitely “spendy-pants”. But I will be honest, I am looking forward to May where I can still be a spendy-pants and grow the net worth by $6,000/month on average.

I am glad my spending habits have not stirred you away from the blog. I look forward to your comments and your contribution to the conversation.

Totally agree that the community of PF bloggers is like an all you can eat buffet. You get to go around the different blogs and pick and choose what defines your journey. A little bit of savings here. A little extra income there. Top that off with some maxed out tax-advantaged accounts….etc.

Cheers!

I meant to ask. Why don’t you fund a Roth IRA for yourself (I know we’ve discussed your wife’s traditional in the past). Thanks.

In all honesty I haven’t given it much thought. I know you can always pull the contributions back out without penalty and the gains are tax free at retirement age. Can you give me some good arguments as to why I should be considering it? Besides it being a hedge on higher taxes in the future?

In all honesty I’m trying to figure it out myself. Reading Go Curry Cracker and jlcollinsnh has me thinking the benefits don’t really make it worth it. I currently max out my 401k and HSA, and unfortunately I cannot contribute to a traditional IRA. So basically I’m looking for other tax-advantaged accounts to put my money instead of my after-tax brokerage account. I maxed out my Roth for 2014, but haven’t pulled the trigger yet on 2015.

Well if you find a good reason, please do share!

Great month! In the spreadsheet it shows $1950/month in rental income, and you mentioned the condo renting for $1350. Are you also renting out a spare room in your primary? Sorry if I missed this somewhere.

Yep we rent out a room for $600/month.

Yes, you are correct FI Fighter, He has a room for rent at his primary.

Looking at your expenses, I did not realize how similar our real estate investments were. We have the rental in FL and the rental in CHI that we also live in, do you think you would do another investment property once the condo is paid off? You mentioned the $600 above where do you apply those funds specifically?

Hey man,

We are actually considering another rental property sometime in the next 6-12 months.

The $600 is in the rental income bucket. So if you look at the summary table above you will see $1,950 listed as rental income. $1,350 is what we collect for the condo and $600 for the room we rent.

How are your rentals doing?

Cheers!

I’m glad to find someone else interesting in paying down the mortgage. Most sentiments say to pay the ‘low cost’ debt to increase savings. We find (future) solace in owing money to NO ONE. So we proudly march towards that goal.

We do try to keep spending low to make progress towards our targets. I’m wrapping up the month. We spent more than we budgeted for – But update coming soon!

It is always nice not to owe someone else money.

Looking forward to your update Mr. Maroon.

Cheers!

Congrats on hitting $200k! That’s a huge amount for someone who’s just 28. I also read your about page. You have an awesome story . . . very inspiring.

Can’t wait to see you hit $300k!

Thanks Professor!

I hope to see you around.

Cheers

I’m a big fan of Tony Horton. His P90X2 is what got me in shape for the first time in my life. Great guy and solid program.

Hey Simon,

Tony Horton is awesome. I did P90X for the first time back in 2011 and went from 240 lbs with 28% body fat down to 187 lbs with 8.5% body fat in about 256 days. I did P90X, Insanity, P90X/Insanity Hybrid, and P90X-2. I have been hooked ever since. I just finished a round of classic P90X last month. Now I am doing P90X3, only 30 minute workouts that allow me extra time to work on the blog 🙂

Glad we have another fan in the house.

Have you done any other programs?

Cheers!

I just started reading some of your articles and I’m quite impressed!

I own two rental properties along with the home I live in with my family and I’m continuously torn between paying off the mortgage of the cheapest rental (mortgage is $566 and rental income is $850, and I “only” owe $76000) or maxing out my 401K to $18,000.

My other rental rents for $1050 while the mortgage is $800, however, I still owe about $156,000. Ideally, I would love to pay off the cheapest rental first, and use the income to pay off the second, and so on…

What would you recommend?

(By the way, you’ve given me a TON of motivation to start writing again in my own blog. Thanks!)

Hey Budget Nerd!

Glad you found the site and have enjoyed some of the posts. Love the name by the way.

Maxing out the 401K would be higher on my priority list. I make sure I max that out before I do anything else.

Next its the IRA for my wife. If she had a 401K we would take advantage of the higher contribution limit and max that out as well.

Then after pre-tax accounts are maxed out, and you still have extra money you are not sure what to do with, that is when I would start considering paying down the mortgage on one of your properties.

Now I will say that I am not paying down my mortgage on my primary residence because I am against debt per se. It just happens to be the best option for my money at the moment. And I only like to have so much leverage.

You rental properties sound like they are doing pretty well on a cash flow basis.

If I understand correctly you have two rentals and a primary residence? Is your primary residence already paid off?

I look at paying down my mortgage as a bond allocation that is paying me a guaranteed 3.675% return. I would touch government bonds with a ten foot pole as I think there is a lot of capital risk. Plus the 30 year is paying something like 3% the last time I looked. Eventually rates will go higher and bonds will fall in price.

The stock market is at an all time high so I really don’t feel compelled to invest the extra money until we have a decent correction.

Starting in May I will start having an additional $2K to $3K available that I will need to figure out what to do with. One way I will be deploying some of that capital is putting more money in my Prosper account. I am thinking something like $500/month.

Then sometime over the next 6-12 months we may look at picking up another investment property. We are not dead set on this, but it is a consideration.

Not sure I really gave you any advice or at least not the advice you were looking for. I would have to know a bit more about you personal goals and situation before I could be more concrete in my advice.

Otherwise I can just share my thinking and what I am doing and why.

Hope to see you around.

Cheers!

p.s glad I could spark the writing engine for you.

Hey thanks for the response! To answer your question, I have two rentals that have a positive cash flow, and I own my personal residence that has not been paid off. To be honest, we only plan on living here for about 5-6 more years as it’ll be a bit too small for our growing family. You gave me some great ideas, and I really appreciate it!

I’m working on maxing out my 401K, and once I accomplish that, my goal is to definitely set up an IRA for my wife. (who do you go through to do that, anyways?) I usually allocate a portion of my check to a savings account for each of my kids (I’m not too sure about a 529c), and I pay 10% of all my income to my religious organization.

We have some existing debt, but nothing crazy like high interest credit card debt. Any debt accrued we always ensure that it’s at a low interest rate. Sometimes we go back and forth on whether it’s more productive to pay off debt first, and then invest, or to max out investments first while employing the “snowball effect” on current liabilities.

Again, thanks for the response!

I use TD Ameritrade for all my investment accounts outside of my work 401K. That’s why I have them linked up in the side bar. Let me know if you decide to go with them and have any questions.

Your asset is growing and liability is decreasing. That 2% of growth is great considering the market’s downturn last month. Thanks for sharing your post and keep up the great work.

Cheers,

BeSmartRich

Hey BeSmartRich,

I totally agree. I am very happy to see my assets continue to move up and to the right on a chart. And its always good to see the liability of the equation move lower.

Hope your doing well. Thanks for stopping by.

Cheers!

Hey Gen Y Finance Guy,

Love the very detailed monthly review you’ve put together, as well as the clear enthusiasm you have for sharing it and working towards your goals alongside other bloggers! Very motivating.

My perspective towards finance seems reasonably similar to yours – I have a lifestyle I really value and am grateful for, but personally don’t want to change it and take the frugality path to get to FI. I’ve just taken a new role with a good increase in salary, but am also really keen to get some ‘side biz’ income going to support it.

Looking forward to following your journey and see you make huge bounds towards those ambitious goals of yours!

Cheers,

Jason

Hi Jason,

Glad you enjoy the detail and transparency. It was a decision I made early on before I ever launched the blog. I didn’t see a lot of blogs out there that showed how the sausage was made if you will 🙂

The community has been great and I have connected with so many awesome people.

Sounds like you may be a brother from a different mother. I totally get you about lifestyle. That is something else I have noticed over the past 7-months, is the over-abundance of frugal blogs. It’s awesome that they can live so cheaply, but like you I like certain things that cost more than the average frugal blogger is willing to pay. That is the great thing about personal finance, is that there are many paths to the end goal.

I imagine the spectrum like this:

Spending<<<<<<<<<<<>>>>>>>>Income

I tend to find myself leaning right towards the income side of the equation. But I still manage expenses as to not waste money.

Thanks for the comment.

Cheers!

– GYFG