Financial Independence!!!

We officially hit our Financial Independence number this month as defined by the Five Major Milestones of FI that I wrote three years ago. The goal was to achieve a net worth of $3M with the ability to spend $120,000 per the 4% rule. That said, I’m the kind of person that never wants to touch the principal and only live off the income, so although the 4% rule says that we could spend $120,000 a year, there are a couple of things we have to be careful to adjust for. First, not all $3M of our current net worth is as liquid and easily spendable as it would be if it were entirely in stocks. Since I never intend to touch the principal I don’t adjust our net worth to exclude our primary residence. That is where the other adjustment to this rule for the GYFG household comes in – we’ve deployed approximately $1M in various cash-flowing real estate investments that will produce $171,000 in annual income – this is currently split as $120,000 from after-tax investments and $51,000 in a retirement account. There is also a small amount of income from dividends but it is only about $5,000 per year at this point.

![]()

This is a HUGE milestone to celebrate but we are still only 30% to our ultimate goal of Financial Freedom – a $10M net worth. The good news is that we continue to stay far ahead of our original projections on both income and net worth. We originally didn’t project hitting a $10M net worth until we were 48 in 2035 but we are now projecting that in 2027 (as shown in the above graphic). And this is before accounting for a likely liquidity event in the near future that would allow us to realize a good portion of the phantom net worth I’m carrying below.

With that, let’s dive into the financial update, and go through the details of what allows the GYFG family to live well and give well.

Financial Dashboard

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, six years later, we are 30% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust 25.4% CAGR. Even more mind-blowing is that our net worth has been compounding at a 65.1% CAGR during that same time period.

Note: I’ve finally got the confidence to forecast an income in 2021 that will be higher than what we earned in 2020. That is even after accounting for the large $415,000 capital gain we had in February of 2020. A large part of this increase is coming from Mrs. GYFG who is absolutely killing it in Real Estate. The other is based on a little more visibility that I’ve gained in the performance of my business through the end of the year. Nothing is guaranteed but I have a strong level of confidence that we can hit this forecast income figure.

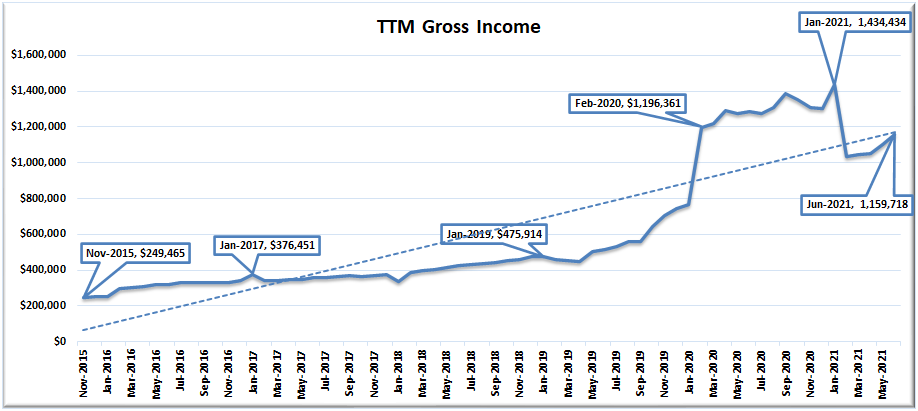

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. After falling off a cliff in February we continue to climb towards our previous peak in January of 2021. Our income continues to climb towards the previous peak and we are tracking to not only exceed our 2020 annual income but also to surpass our all-time high set in January of this year.

Net Worth

Current Net Worth: $3,001,550 (up $622,109 or +26.1% for 2021)

Previous month: $2,870,284

Difference: +$131,266

A fairly large portion of our net worth only gets re-valued periodically and I currently think our net worth is understated, which means we will periodically have large and lumpy changes to it. One of the drivers for the larger increase this month was moving up the value of our primary residence to be more reflective of market prices as we think about listing our home for sale in the near future (that accounted for $50,000 of the increase this month).

Note: I’m still not holding a value for my business in my net worth. As I’ve spent more time shopping my business around to potential suitors I’ve decided to move back to a 5X multiple as this is the high probability multiple for us (confirmed by an offer in hand). As much as I and my partners were hopeful for a larger multiple, there is a reason I held a 5X multiple internally and this is because of the deals I’ve personally been involved in during my Corporate days. I’m hesitant to hold a value in my net worth for this until we achieve a liquidity event. That being said, I’m holding a “Potential Net Worth” figure as I think we will likely achieve a liquidity event in the next 6 months (down from the 12-18 months I previously estimated).

Potential Net Worth: $6,001,550

^This values the business at 5X EBITDA implying a value of $5M in total Economic Value (EV). I then multiplied the EV by my fully diluted ownership stake of 60%, which potentially adds $3,000,000 to our net worth.

Net Worth Break Down:

Real Estate (48%) – This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (11%) – I decided to split this out on its own because it is something I do want to manage separately from our overall holdings in Real Estate. Our primary residence currently makes up 11% of our total net worth (down from 23% in September 2020) due to a cash-out refinance (locking in 2.8675% for 30 years) that put a mortgage back on the property. I expect the concentration to continue its downward trend until we move into our new house in January of 2022.

Net Cash (17%) – We currently have $519,000 in cash vs. $506,000 last month.

Alternatives/Other (16%) – This is a catch-all category that captures our investments in the following: life settlements, a special purpose acquisition company (SPAC), a private investment in the Robinhood trading platform, Bitcoin, and the newest addition of Bowery Farming – a vertical farming company that recently closed a $300M in a Series C funding round that I was lucky enough to participate in.

Stocks (7%) – Our 401K accounts are maxed out and we don’t have any new investment planned here for the year. The only thing that could tick this up is when we get the shares from a SPAC that we participated in that currently sits in the alternatives bucket above.

Total Capital Deployed in 2021:

This month we deployed an additional $62,941 into acquiring additional BTC during its continued decline. This currently makes up 6.67% of our net worth and we are comfortable with an allocation of up to 10%. That’s the only capital we deployed in June but we did commit another $50,000 for July deployment for another industrial real estate deal with projected 18% CoC returns.

There are a number of liquidity events that I’m expecting later this year:

(1) $75,000 hard money loan at 10%. The original loan was for $150,000 and was made back in November of 2019. Half of it was paid back six months ago and I expect the remainder sometime in the next couple of months as the last property securing the loan is currently being listed for sale.

(2) Robinhood Investment. I invested in a round led by Sequoia Capital at a $8.3B valuation back in July of 2020. The last round they raised in August 2020 was at an 11.2B valuation. They announced that they would be filing for an IPO in 2021 and some of the chatter is that it could go public at a $40B valuation. I’m not going to make F-U Money but my $10,000 could turn into $40,000+. Only time will tell.

(3) Life Settlement Policies. I invested $70,000 across seven policies in late 2017 and early 2018. Four of those policies are now past the expected maturity date. I’ve had to make several capital calls to keep the policy active as the insureds have lived past the expected life spans. If all four policies payout this year, I will receive $59,300 on an original investment of $40,000.

(4) $38,000 in maturing hard money loans made on the PeerStreet platform. The volume has been significantly less since the Pandemic hit and of the new loans being added to the platform, not many have been matching my criteria of a max 60% LTV and 8% interest rate. Therefore, I have been transferring money out of the two accounts with PeerStreet as the notes mature. On top of that, the majority of my remaining notes are in some form of default.

I could see a continued deployment of capital in the range of $25,000 to $50,000 per month for the remainder of the year (mostly real estate and/or alternatives). That said, it also depends on the timing of our remodel and its cash needs, while maintaining a comfortable cash cushion.

Closing Thoughts

First, I can’t believe it is already July. I’m excited and very nervous for the future months ahead with so many important events on the horizon:

(1) We get to welcome our daughter into the world sometime in early September.

(2) If all goes according to plan we should be realizing massive liquidity from selling some equity in my business.

(3) We’ve officially started remodeling the new house to prepare it for moving in some time between 10/2021 and 1/2022.

(4) Once we have better visibility on #3 above, we will be preparing to list and sell our current home.

(5) I turn 35 this year – WTF?!?

My goal is to not rush through the summer even though my innate thought process is “I can’t wait to get through September and then things will settle down.” Do things ever really settle down? M Maybe I just don’t know how to settle down. Until recently that was probably because I wasn’t ready for a different pace of life. I was consumed with achievement but this year will mark a HUGE inflection point for me and my family. I believe 2021 is shaping up to be the climax for the last decade-plus of head down focus and dedication. We’ve already started loosening the purse strings and now it’s time to make a significant shift in how we spend our time.

I’m excited to really evolve into the person I wrote about becoming in the last letter I wrote to myself from ten years in the future.

– Gen Y Finance Guy

23 Responses

What about taxes on your $3M equity stack? Doesn’t seem accurate to directly add this to your net worth.

Fellow Entrepreneur,

Good question. Last month I wrote about the monetized installment sale, which is going to allow me to defer the taxable event for 30 years, so that’s why I’m not carrying taxes on it.

GYFG, congrats on hitting the $3mm milestone, both for the impressive hard number and your Financial Independence goal.

1) A thought on your primary residence within your Net Worth, is you can extrapolate an equivalent rent/housing expense. The fact that you no longer pay a mortgage, and own an appreciating asset, is worth something. You are keeping both figures anyway, so whichever one you choose will be the right choice.

2) Just read and enjoyed James Altucher’s new book, “Skip The Line.” You might like it, not only because you are truly ‘skipping the line’, but it is a fun read that updates Altucher’s interesting life. I actually was exposed to James Altucher through you (and Adam Chudy) and am happy to absorb-and-apply his ‘Choose Yourself’ philosophy. If you get around to watching his Amazon limited series, I would be interested in your thoughts. He’s doing stand-up now, a field in which both his ego and humility are serving him well.

3) Along the lines of you writing to yourself 10 years in the future, I like to write letters to myself 10 years ago. Not to sound smug, but every letter is some version of ‘you were dopey, and by the way, “I told you so!”‘ Don’t learn anything, but it is fun to devolve for a minute!

4) Nice work scheduling your new family addition to last third of the year, keeping expenses low while still gaining the full tax deduction. Shrewd.

Good thoughts for your continued improving health, and Happy Independence Day to you and all readers!

Thanks, JayCeezy!

1) You may have missed it but we decided to put a mortgage back on the house last year when rates were so low that I couldn’t help but take what felt like free money – 2.875% for 30 years. That said, we are contemplating being mortgage free again when we move into the new house later this year. I’ll keep this idea top of mind to re-visit.

2) I’ve added Skip the Line to my wishlist. I did watch the series after you recommended it. All my wife could say is “this guys an idiot” paired with “how does someone make and lose so much money multiple times.” I think it’s part of his schtick. I found it entertaining but I would never want to follow his path. Luckily we all get the opportunity to follow a unique path to each of us.

3)I’d love to read an example of one of your letters if you want to share.

4)That is two in a row now as baby #1 came in late October.

Happy 4th of July Weekend!

re: #3 – Note to self…

Hang on to all that fear and regret you feel, every day. Not because it is doing you any good. But because it is consuming your time and energy, which you would only waste if you expended it on improving yourself and helping others. So marinate in it. Every day. Look at your face in the mirror. This is 50, and you are never going to be any better looking. This is the best it is going to get. Don’t bother trying to lose that 15 lbs., even if you do it will just come back and your effort will be wasted. Say this out loud to yourself as you look in the mirror. The wrinkles, the lines, the face looks like an accordion and could hold three days rain. The hair is getting thinner. In fact, you are losing so much hair that the cat is now allergic to you. You should invest in Bitcoin. Right now, don’t wait. But you won’t. You are too smart to ‘fall for it’, you are always the ‘smartest guy in the room.’ Now is a good time to tell you, after all these years. That isn’t a compliment.

Okay JayCeezy at 50, best of luck to you in the coming 10 years. I’ll write again when I’m 70, and you are turning 60. Until then, you are on your own!

P.S. – watch the self-talk!

Thanks for sharing, JayCeezy. I’m much nicer to myself in my head 🙂

FYI – I think you asked somewhere about seeing the % split of contributions vs. investment gains and I wanted to let you know that I plan to do an update at the end of the year of the post I did at the end of 2018 that showed like 66% of net worth coming from contributions and 34% from gains at the end of 2018 when net worth was ~$1M. I expect that relationship to have completely flipped by year’s end – big contributors are my exit from my prior employer and the pending sale of a substantial stake in my business.

Prior post (that was inspired when you asked this the first time: 4 Years into Our 20 Year Journey to a $10,000,000 Net Worth

I’ve read multiple times how well your wife is doing in Real estate.

I almost feel like it could use its own post.

Last I read some time ago she was as an on site property manager?

With real estate being so hot it would be cool to deep dive what she does to bring in a lot of income

After all we can thank our spouses for at least half our success.

Hey Jay – it’s been a while. And if you remember when my wife was doing property management than it’s been longer than a while. Property management was only a side hustle for her. Her main hustle is Escrow, which I know isn’t something every state has but in California, Escrow sits in the middle of every real estate transaction.

Congrats Dom on the huge milestone. Did you have a post on how you secured the private investment in Robinhood? The 100X money is in those moonshots 🙂

Thanks, Financial Freedom Countdown!

I did not have a separate post on the Robinhood investment, but I can share that I’m part of a private investor circle that gets lots of these types of opportunities. The group participated in Coinbase back in 2018 and I just passed on Block FI. There have been many others.

Booyah! Congrats on the $3M milestone, Dom.

There will be a day in the not-so-distant future when I forsee you hitting the $50M mark.

Thanks, Michael.

$50M seems feasible in 30-40 years…but the near future???

Near future is all relative… haha. More importantly, I think you may continue surprising yourself. Enjoy the ride (I know you are)!

As Mr. 1500 would say, welcome to the triple double comma club. I don’t know if I will ever get there but you’re a good example of what someone can achieve if they work their butts off and willing to put in the hours to succeed.

Can’t wait to see you reach your big hairy audacious goal.

You reminded me of Mr. 1500 and I hadn’t been to his blog in a while. It’s great to see him hit $4M in such a short period of time.

I’m right there with you on hitting $10M. After I finish this transaction to sell a piece of my business, it feels pretty inevitable that we will not only hit the goal but on a much shorter time frame than originally projected back in 2015.

Thank you for your post, what platform do you use to participate in Pre-IPOs, and what is the minimun capital required, thanks

Hey Jerry – those “pre-IPO” investments are not from a platform but a private investor circle I belong too. The minimums very from 50,000 to 250,000. The benefit of the group besides access to the deal flow is that if there is interest and an individual doesn’t want to invest the minimum we form a LLC to get to the minimum collectively.

Incredible Work Dom! You’re well on your way to that $10MM goal. RE crowdfunding is an interesting avenue that not many older/traditional investors are used to. Going to explore some more on here on how you came about those opportunities as well as private placements, and how to discern that with REITs and other options.

Thanks, Gary.

Congratulations Dom!

Hey Simon – long time!

Thanks for stopping by – hope all is well.

Hi guys,

Kudos for the achievement.

You invest. I get this.

Yet, I have a precise question.

Could you give more detail(s) about the ratio amount invested/yield (per month and per year)

This would be really helpful. Everything is really just a bunch of figure(s) with very limiting meaning.

I.E

I invest X $ in Y (crypto/real estate….) last year (i.e 2020) and I got Z % yield .

I.E just for clarification (fake number)

I invest 20.000 $ in equities Y last year and I got 2.5 % (dividend) + 10% appreciation (if equity Y has gone from 20.000 $ to 22.000$ valuation)

If you could give that kind information when it comes to your portfolio, this is what really matters. Everything else is for newbies 101. I say that because you like to give figure(s), yet not all figures matter.

++

Hey Tom,

Thanks for the comment. I do go into this sort of detail from time to time (mostly on our real estate holdings). But to be honest, my focus is on asset accumulation, tax minimization, and income maximization. I honestly don’t track the return of individual investments that much. You can also see the amount of money invested across different assets in the capital deployment section of the report.

I share the figures that matter to me at this point in my journey. I’m sorry if you don’t find them that useful.

All the best,

Dom