GYFG here checking in for the October monthly financial report. If you have been reading these reports for a while you will notice that I introduce each month with the same intro month after month. I do this for two reasons, a) for the newbies to the site (which make up about 50% of the sites traffic) and b) to remind everyone what these reports are all about. By all means if you have read the intro at least once, then please feel free to skip down to the “Summary of October 2015” section where the new content begins (click the orange link to be taken there automatically).

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom, if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you’re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then by all means keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM, because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgence of your choice.

Not only that, but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found on this report). In these monthly reports the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate (NEW), and progress on the mortgage pay down goal.

Summary of October 2015

I think October went by faster than any other month this year. This perception really is a direct result of my busy season kicking in at the day job. We are knee deep in 2016 financial planning, and I am also involved in our long term planning out to 2021. The company I work for is growing very rapidly and it’s really an exciting time for me. Especially with the new role, I am more involved in strategic planning than ever before. It is great to be challenged again.

As many of you likely read on my 100th post (celebrating 1 year of blogging), I have to slow down the publishing schedule a bit on the blog to once a week, at least through the end of the year. This will allow me the bandwidth I need to focus on the day job and a few other things I am working on to continue to grow this blogs reach. What you also may have noticed is that I have still been publishing 2 posts a week since that announcement. This was really a matter of posts that were already scheduled to go live through October. November is the official change in frequency, at least my personal commitment to the frequency.

There could be weeks that I publish two articles, I am just not promising to do so.

Let’s get this show on the road and see how October went…

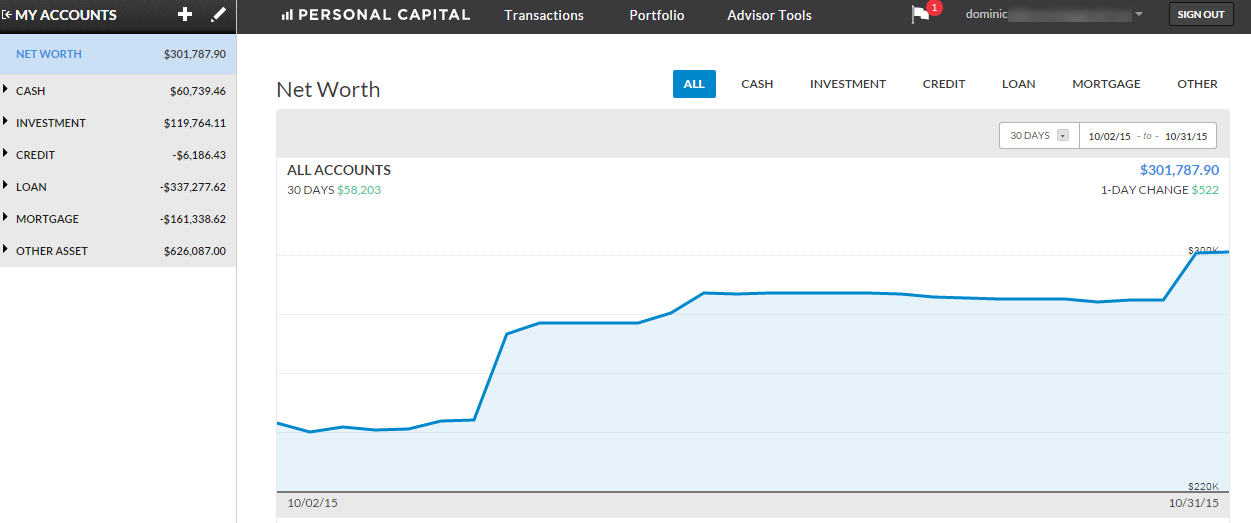

We use Personal Capital To Track Everything

This month I am adding a screenshot of my own Personal Capital account as another level of transparency for you. I recently had a email conversation with Sam over at Financial Samurai around bloggers who share financial information. One of the questions that came up in my head during that conversation, was how you all would be able to confirm, that what I was sharing was real. This is just another way to keep me honest.

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month I then drop that information into my financial stats spreadsheet for this monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must, folks.

Personal Capital (which is free to use) is a great way for us to systematize our financial overviews since it links all of our accounts together and provides a comprehensive picture of our net worth. If you’re not tracking your expenses in an organized fashion, give Personal Capital a try.

Month Over Month Financial Summary

Notice in the below screenshot that I blew out the assets section.

What went down in October?

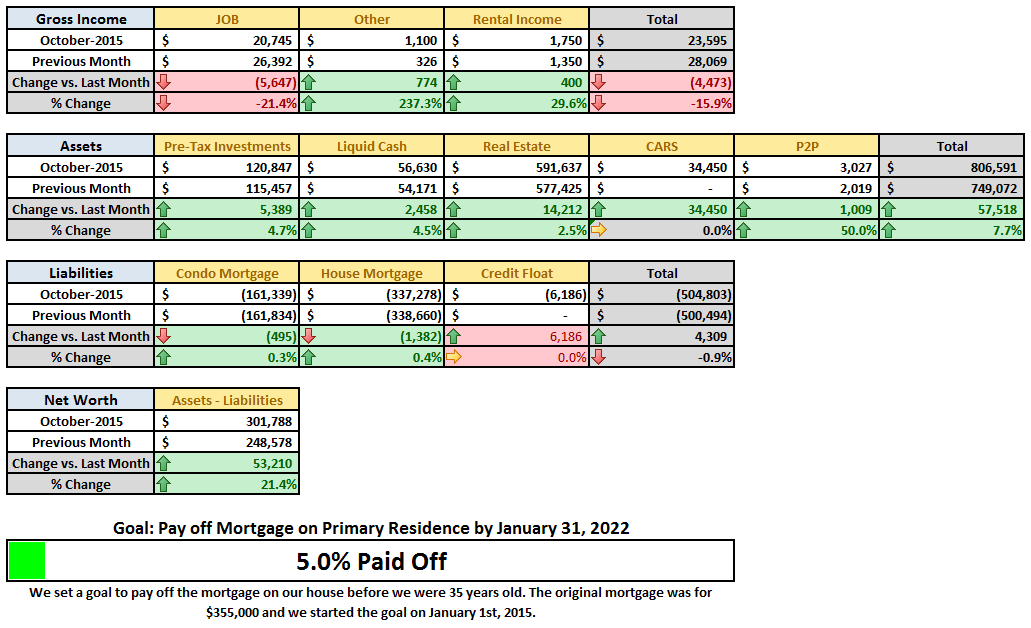

This month came in much higher than I had anticipated on the income side of the equation. However, it was down 15.9% vs. last month. Mrs. GYFG killed it again this month bringing in an additional $7,100 above and beyond her regular pay. Part of this was from a monthly commission and the other part was from her notary business. I was able to bill an extra $1,000 for some side consulting work (I mentioned this last month). Finally the blog received a $100 commission check.

Last month I raddled on about how I thought income would be in the $15,000 to $17,000 range, but I actually think it is going to be higher now. Mrs. GYFG just had another killer month end at work and will likely be getting an even bigger commission check in November for October revenue.

Here is a look at the trend for the last 11 months:

So far this year we have produced $211,661 in gross revenue (January through October).

The Juicy Details

- Previous Month: $28,069

- Difference: -$4,473

Now where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it is a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here: January, February, March, April, May, June, July, August, and September.

Home Mortgage & HOA $3,317 The NEW normal payment is $2,349/month for the mortgage and $84 for the HOA (got hit with two HOA payments this month). However, as a part of our 7-year mortgage pay off plan, we started adding an extra $800/month towards principle in January of 2015.

- Previous Month: $3,233

- Difference: –$84

Condo Mortgage & HOA $1,150 This is the payment on our rental condo and includes the mortgage of $888 and HOA of $250. We currently rent this place out for $1,350/month, as seen in the summary table above. Our interest rate adjusted up from 2.875% to 3%.

- Previous Month: $1,150

- Difference: –$0

Timeshare $0

- Previous Month: $0

- Difference: +$0

Home Improvement $470 This should be around $200/month through the end of the year.

- Previous Month: $170

- Difference: +300

Food & Dining $1,907 We had another dinner at Maestro’s where we picked up the tab for us and my sister and law and her fiancé. Also had a lot of dining out this month. As I have mentioned before, our long term target is $1,200/month (to date we have averaged $1,560).

- Previous month: $1,570

- Difference: -$337

Shopping & Entertainment $1,558 This category covers any discretionary shopping and entertainment expenses.

- Previous month: $1,041

- Difference: -$517

Travel & Hotel $1,575 This was to pay for our flights to Kansas City for Thanksgiving with friends.

- Previous month: $248

- Difference: -$1,327

Auto and Transport $438 This includes fuel, car insurance on two cars, and toll roads. It was my wife’s car this month that need all kinds of preventative maintenance. The only thing we have left is her breaks, which will likely happen in January.

- Previous month: $972

- Difference: +$534

Personal Development $0 We do buy books on a regular basis but that would fall in the shopping category above. This is just for some of the larger investments we make in ourselves.

- Previous month: $0

- Difference: +$0

Bills & Utilities $535 This includes our monthly utilities like gas, electric, water, internet, and cell phones. Sometimes this also includes a cleaning lady and our monthly lawn service.

- Previous month: $505

- Difference: -$30

Health & Fitness $312 This includes a monthly massage subscription (on pause, while I change locations), monthly dues to remain an active member of Team Beachbody to ensure my discounts on supplements like Shakeology and Results and Recovery Formula.

- Previous month: $31

- Difference: -$281

Business Services $99 This covers hosting with WP Engine for $49/month and MailChimp email service $10/month (for those emails I have been sending everyone on my list). I have now upgraded to SumoMe Pro for an additional $40/month. Will look to convert these to annual subscriptions in 2016 to save 20-30%.

- Previous month: $59

- Difference: -$40

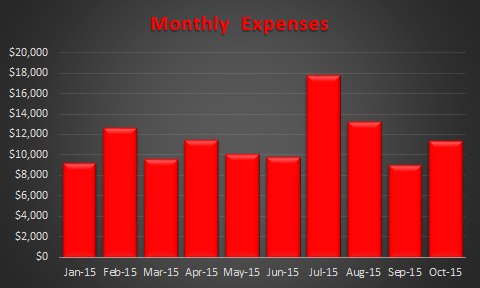

Total Expenses $11,361

- Previous month: $8,978

- Difference: -$2,383

Expenses were up 26.5%% this month vs. last month.

Here is the trend so far this year:

What is great about all this detailed tracking that I started this year, is that that it is allowing me to plan for 2016.

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

- Our mortgage payment is automatically set up to pay $800 in additional principal.

- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- We have an auto investment of $500/month into my wife’s IRA to make sure we max it out by year end ($5,500)

- At the beginning of the month I have been sending $1,000/month to a REIT investment or to Prosper.

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead we manage savings and investments and let the expenses work themselves out.

What were Investments and Contributions?

- Contributed $500 to the wife’s IRA for the 2015 tax year.

- Previous month: $500

- Difference: $0

- Contributed $1,058 Into my 401K.

- Previous month: $3,138

- Difference: -$2,080

- Prosper Lending $1,000 We have deposited $3,000 so far this year.

- Previous month: $1,000

- Difference: +$0

- Rich Uncles REIT $0 We currently have $5,158

- Previous month: $0

- Difference: $0

- Increase in Savings $2,458 This includes checking, savings, and CD’s.

- Previous month: $1,056

- Difference: +$1,402

- HSA Contribution $1,000 This is set up to max out by the end of the year. We currently have $4,110 here.

- Previous month: $1,000

- Difference: $0

Total Investments & Contributions $6,016

- Previous month: $6,694

- Difference: -$678

Savings Rate

Last month we added a new section to track our monthly savings rate. Since publishing our goal of saving 50% of our after tax income, I thought it would be a good idea to keep track of it in these reports going forward.

In the above chart you will see the trend of our savings rate by month. You can see that although our goal for the year is 50%, we bounce all over the place on a monthly basis. I still have us forecasted to miss our 50% goal, but we did improve to 46% (vs. 44% last month).

This year has largely been a foundational year, where I finally formalized the financial philosophies that drive our finances. It will be very interesting to see what we can do in 2016, going in with such a solid foundation.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income (this month we officially reached 3% of our goal). Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate.

I am not anywhere close to a 7-figure net worth yet (or what some refer to as the double comma club). However, it is growing at a very respectable rate (just take a look in the side bar for growth at a glance). If you want to see how I plan to get there you can read all about it here (soon to be reviewed and updated in 2016).

October Net Worth $301,788 (with ten months down in 2015, this puts us up $120,424 or 66.4% vs. 2014 so far and we still have 2 months to go)

- Previous month: $248,578

- Difference: +$53,210

This month’s increases include some onetime adjustments. It is very rare that we will experience these kinds of jump in our net worth. Here are the three major adjustments that took place in October:

- We now have included our cars in our Net Worth Calculation. This accounts for a one-time increase of $34,450 (for 2 cars). This will be a value that continues to decline overtime as the cars lose value. I added this in order to have the net worth that I report match the screen shot from Personal Capital (shared above). This will also incentive me to make sure we keep our cars for as long as possible, in order to use capital in a more efficient manner (i.e. on investments and not on new cars that lose their value over time).

- I added our credit card float to liabilities. We do pay our credit cards off every month. However, we also take advantage of the free float that the credit card companies offer. This is now accounted for the way it should be.

- We updated the market value of our primary residence. It has been 8 months since we last changed the market value of our home. Mostly because I have been waiting for a comparable property to sale on our street. Until now we had been carrying the value at $378,800, the most recent house that sold on our street in September, went for $393,000. This is now where we are carrying the value of the house. Although we have a lot that is about 40% larger and more upgrades, we are not going to factor those in…We are not appraisers. See sale below:

In light of the recent changes, I also thought it was time to include more detail around the components that make up Net Worth in the Pie Chart below.

You will notice that in the second chart above that I have broken our net worth out into 5 categories: Primary Residence, Cars, Real Estate, P2P Lending, and Investable Assets. I want to continue to see our primary residence and our cars to make up a smaller and smaller piece of the overall pie. Over time I can see myself adding two more categories to represent insurance (post coming early 2016), and stock options (in the company I currently work for).

You will notice that in the second chart above that I have broken our net worth out into 5 categories: Primary Residence, Cars, Real Estate, P2P Lending, and Investable Assets. I want to continue to see our primary residence and our cars to make up a smaller and smaller piece of the overall pie. Over time I can see myself adding two more categories to represent insurance (post coming early 2016), and stock options (in the company I currently work for).

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote for GenFKD covering this very topic: Rapid Wealth Building: Savings Rate vs. Compound Return.

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (although the execution of this is going to change up a bit in 2016, details to come). When you break it down and follow the 3 simple rules, it’s not as hard as it sounds. We bought our house in February of 2014 and then refinanced it into a 5/5 ARM in September of 2014 to remove PMI and free up cash-flow to put towards the principal and keep us on track to pay the mortgage off at an accelerated pace.

The progress chart above shows how much of our goal we have completed. Last month we were at 4.6%, which means we picked up another 40 basis points in October. Those monthly 40 basis point improvements have really started to add up.

I am still working out our plan for the slight change in the execution of the mortgage payoff goal. If you don’t know what I am talking about, you can go to the August report to read about my concerns around tying up to much capital in the property before it’s paid off and it becoming too large a percent of our net worth here (You will find it in the same section).

I have decided what I am going to do with the extra money earmarked for paying off the mortgage every month. I found what I believe to be the perfect financial vehicle for these extra payments. All I can tell you is that it involves the very controversial Whole Life Insurance. But before you judge, wait to read the posts I have coming out in 2016. I am not saying this is right for everyone, but it seems to be the right fit for us right now. I have been researching this product for the past year and have been working with an agent that specializes in a special use of these that reduces the front loaded fees significantly and maximizes the cash value of the policy. That is all I can tell you for now.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

PS: Here are my favorite ways to track this stuff:

- The “Financial Stats” spreadsheet – a simple Excel template I created to provide the tables and charts you see in this post as well as on the Financial Stats Page. If you would like a copy of this spreadsheet, sign up for my email list (sign up form in the right side bar) and I will send you a copy.

- PersonalCapital.com (free) – I track everything in Personal Capital and then enter into my custom Excel template. Check out my Personal Capital Review to see if its right for you.

23 Responses

Im digging your mortgage payoff strategy! Bc I didn’t have a discipline one, I ended up paying off my mortgage in 12.5 years instead of my goal of 10.

Congrats on your huge increase in income!

Thanks Sam!

I like it and designed the mortgage payoff strategy based on the concept of “no austerity.” It is all based on incremental revenue every year. So it doesn’t effect our lifestyle.

Income growth has been much greater than I expected this year. In fact when the year started, I thought that our income was actually going down about $35K, but it is actually on track to be $35K higher (so a $70K swing vs. expected).

That is some great progress. You are tracking to almost double your net worth in 2015! That is awesome. With all the income increases, you should see solid 6 figure increases every year even if the market goes mostly sideways. Congrats.

Vawt –

This year has been much better than I planed for. It certainly helps making progress. At some point I expect that my wife’s income will take a significant hit when real estate goes through another cycle, since about half of her income is based on monthly commission.

The goal is to continue to increase my income from the day job, side hustles, and passive income streams to offset an eventual decrease.

I would be very happy to increase net worth by 6 figures every year.

Great momentum Dom! You’ll be in the double comma club in no time. Props to Mrs. GYFG. 😉

Thanks Michael! We are making solid progress on our way to the double comma club. We have the wind at our backs at the moment. Trying to take advantage of the momentum as much as we can right now.

Woah big jump!! nice job. I also don’t count my car in my net worth, on the contrary our car loans are currently hurting out net worth, with the cars being valued at $0 towards our net worth. Not done by design, I’ve just never gotten around to adding the value of our cars in personal capital.

Keep up the good work.

Sean – it was a big jump. But keep in mind it was largely the cars and the increase in the value of our primary residence. I am much more interested in seeing the “investable” portion of net worth increasing. But I am happy to have my offline tracking now matching what I have in Personal Capital.

I don’t think you should include cars as part of your net worth. They provide no financial value in retirement and they throw the numbers off in your bar chart with a sudden increase when the asset was already there. They majke October look much better than it really was. You would probably get some money for the cars if you had to sell them but in reality if you hold them for a long time they will just go down to zero real value and once you sold them you would need to replace them with another car. In my mind net worth should only include investment assets such as cash, bonds, stocks, and real estate. In fact for retirement projection purposes I might consider removing my primary residence from my net worth summary since you can’t easily access the equity from real estate and you need to live somewhere. Don’t get me wrong I do think that a primary residence should be part of the net worth summary but you should consider leaving it out when doing retirement projections. All other consumer goods (cars, boats, furniture, clothes, etc.) should not be part of the net worth summary in my opinion.

Hey Nickr – I can totally see where you are coming from. I know that by throwing in the cars that the month of October looks a bit skewed, but it was easier than going back in time and restating the starting point. It’s a onetime adjustment that I specifically called out so everyone knows I am not playing any funny games.

Now whether it should/shouldn’t be included is really a matter of personal preference. But I agree that the focus point should be on real estate and investable assets. That is why I started breaking out the components of net worth in October as well.

The truth of the matter is that I am trying to treat my personal finances like a business…and a business would not leave any asset off their balance sheet just because it was/is going to depreciate. But it also brings up a good point, because where do you draw the line. If I was going to really be true to that I would also include all of our personal possessions, which I am not going to do.

But the Cars make up a big enough chunk that I want to include them so that I watch them. When they were knew they were worth $65K, so they have lost about 50% of their value. And as you alluded to they will continue to lose value over time. I will probably only update the values every 6-12 months like I do on our real estate holdings.

By including them here, it gives me extra motivations to continue to hold on to them so they continue to shrink as an overall % of Net Worth.

Thanks for your thoughts and comment.

Cheers

Man, that’s a crazy pace you a building wealth at. Keep that savings rate towards 50%, you are killing it!

MrZ

The 50% savings rate is the linchpin to rapid wealth building in my opinion.

Wow, that was very extensive post. Great job on growing your net wort and achieving 300K mark. Truly amazing!

Cheers!

BSR

Thanks BeSmartRich!

Onward & Upward

Love the adding cars into net worth. Never dawned on me until a soccer mom totaled my car last year, and I negotiated a higher valuation on it and was left with a decision of what to buy with the proceeds. Sure felt like a part of my net worth then. Also hammers home the proposition of owning a car vs. leasing when you think about it in Personal Capital terms.

Nicely done Funancially Savvy.

Congrats on 300k! Just crossed that mark myself this month, although my new worth is made up of 100% investments and cash. I don’t have much exposure to real estate, other than REITs .

Congrats right back at you!

Yeah Dom! Hitting that $300k mark. Keep up the great work, loved the extensive analysis this month and glad to see Mrs. GYFG rockin it!

Refreshing to see spending similar to my own! Congrats on the 300k mark!! Looking forward to reading more of the blog.

Thanks MB! I recently just finished a piece on reviewing our total spending in 2015 that comes out next week (spoiler alert, we spent $137,000 in 2015).

Looking forward to seeing you around the blog.

Cheers