If you blinked, you missed January, as it was gone in a blink of an eye (at least for me). I hope that 2018 is off to a good start for each and every one of my readers. I also hope that you have already been taking steps to improve your financial future (I outlined 12 ideas here). Here, January was a mix of work, play, and much-needed relaxation. The busiest time of year for us starts mid-October and runs through mid-January. It was nice to end the last half of January in South Lake Tahoe.

We rented a condo and made an eight-hour drive to it with our dogs in tow for ten glorious days of downtime. As is typical, we lugged what seemed like an entire library of books, as both Mrs. GYFG and I are avid readers. I was able to finish reading one book from cover to cover and get about 25% deep into three others (my max is four books at a time). I should finish up the other three books I started over the rest of February (I try to read three – five books a month).

Unfortunately, I did not get to snowboard or ski because I am recovering from a bulging disc (with nerve impingement) in my lower lumbar spine. I also had a few really bad days where walking was very difficult and painful. That said, I ordered an inversion table before I left on vacation, have been using it multiple times a day since it arrived, and have since experienced much improvement. I am supplementing the inversion table with cryotherapy, massage therapy, stretching, icing, and weight loss. This injury actually stems back to March of 2016 during my Crossfit days. The good news is that after months, I finally feel like I am healing.

I had to take a break from the personal training for the entire month of January but will be back at it mid-February. However, I will be avoiding free weights and running (need low impact until the disc is healed). This year my health and fitness are moving up to the top of my priority list.

Inspired by a personal development book I’m reading, 2018 is the year that I master the art of having it all across body, being, balance, and business. This is a part of a $1,000 program I paid for back in early 2017, which was supposed to be “the year,” but better late than never. I hope you will join me on your own incredible journey of daily personal growth in 2018 and beyond.

If you’re a regular reader and only want to read the new content then feel free to just skip the intro below (no harm, no foul). If you are new or haven’t read many of these reports, I encourage you to take two minutes to read the intro below, which will change periodically.

Intro

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

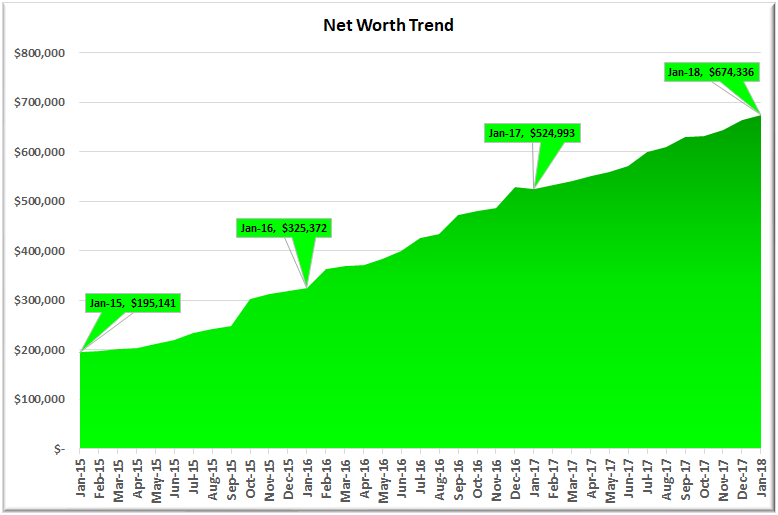

For those of you new around this corner of the internet, these monthly reports are about full transparency. They are just as much for me as they are for you. It was a hard decision to make all of my financial details public, but it has a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141, and our gross income was on pace to hit $178,000 that year.

Fast forward three years: our net worth finished 2017 at $664,391 with a gross income of $372,477.

- That’s a 3.4X increase in net worth due to a compound annual growth rate of 50% for the past three years.

- At the same time, income has increased 2.1X, which translates to a compound annual growth rate of 28%.

I honestly don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will need to share our results with my readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle to only then have the means to check off bucket-list items when my body might no longer be physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for The Man before you have the option to retire. I think that 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two vital components of a good recipe for the 10 year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not that many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page.

Net Worth

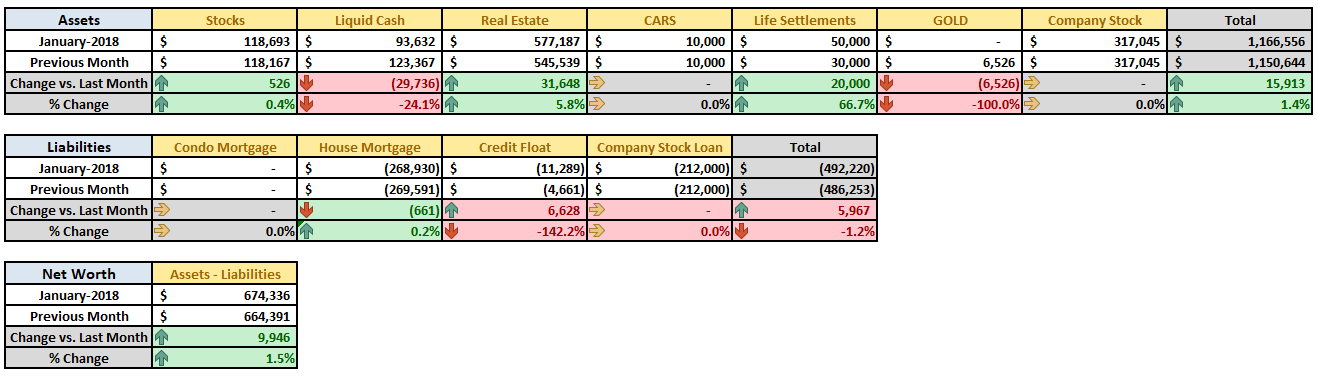

Our net worth was up just shy of $10,000 in January vs. December. February should be a great month due to my year-end bonus payout and my new rate of compensation kicking in. I’m currently projecting an increase in the neighborhood of $40,000 in February.

January Net Worth $674,336 (up +1.5% for 2018)

- Previous month: $664,391

- Difference: +$9,946

A few highlights include:

(1) The Real Estate bucket increased $31,648 or 5.8%. Besides some interest and dividend payments that hit, most of the increase was a result of contributions to two sources:

(a) I doubled our investment at Rich Uncles by investing an additional $13,000 in January. Our total account balance here is now $26,140. The plan is to contribute another $24,000 to bring this up to $50,000 by the end of Q2. We also have an automated investment of $1,000/month going here as well.

(b) We invested an additional $18,000 on the PeerStreet platform. This brings our total account value to $101,187 (now split 75% self-directed IRA account and 25% after-tax account).

(2) We invested in two additional life settlement policies, increasing our investment by $20,000 to $50,000.

(3) We sold our gold position as promised in the last Warren Buffet piece I published.

Net Worth Break Down:

– Due to the above, the Real Estate category increased from 42% to 46%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($26,140), and our hard money loans through the PeerStreet ($101,187) platform.

– Due to the above, the Real Estate category increased from 42% to 46%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($26,140), and our hard money loans through the PeerStreet ($101,187) platform.

– Cash decreased due to deployments to Rich Uncles, Peer Street, and additional life settlement policies. We are currently holding $82,343 in cold hard cash (what I like to call dry powder). This should increase to over $120,000 in February due to my yearend bonus being paid out.

{kind=link}

– As a clarification for newer readers, the Business category represents the ownership I have in the private company that I work for.

– In November I added a new slice to represent our newest investment in Life Settlements. We invested an additional $20,000 into two additional policies. I would like to build this up to $100,000 before 2018 is up.

– The Stocks category represents the cumulative value of our brokerage accounts (retirement accounts and after-tax account) that are invested in stocks. However, it is not all of our retirement money as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $73,000).

– That leaves the Cars category. I include our cars because the goal is to keep the value of our cars as a percentage of the overall net worth pie as small as possible. By including them, it keeps me conscious of the opportunity cost of sinking too much capital into the machines that are only meant to get us from point A to point B. The combined value for our cars is currently being held at $10,000 based on current Kelly Blue Book. However, now that our cars make up a minuscule portion of our net worth, I am seriously considering removing it from net worth altogether. If I do follow through with this, it will likely happen in Q1 of 2018.

Gross Income

I had planned to include income from dividends and interest but ran out of time this month. So, this is still not included, which means income shown here is shy about $750 for the month of January (and slightly lower amounts in months prior to January). We did manage to bring in $26,935 in January from all other sources (or approx. $27,700 if you include dividends and interest). I expect February to set a new record with income projected at $70,000.

Savings Rate

Below is how we actually did vs. our goal of saving 50% of our after-tax income.

We finished shy of 50% for January, but 45% is really good! If we don’t have too many surprises in 2018, we are on track to hit a record 60% savings rate.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than your compound return? If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

You can read about our strategy to pay off our mortgage in seven years (and three months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $268,930.

![]()

Our primary residence is currently sitting at 26.9% of our net worth. We would like to see this closer to 20% in the short term and far less in the long term (like less than 10% over the next ten years). The reason I watch this closely is for two reasons:

(1) Concentration Risk – Although I am confident we will accomplish this goal on time, you never know what may happen unexpectedly. What if we both lost our jobs and couldn’t make our mortgage payment? The bank is going to foreclose on a house with 50% equity a lot faster than one with 5% equity. Until we have the house completely paid off, this will always be a concern and risk to manage.

(2) Diversification – We don’t want our entire net worth tied up in our house. That would be poor risk management.

The original philosophy of this plan was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. I decided that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. We have used the cumulative increases thus far to execute this goal flawlessly. Since setting this goal in January of 2015, we have since paid down an additional $57,600 (Year 1 = $9,600, Year 2 = $19,200, Year 3 = $28,800).

At the end of 2018, we are planning to pay down an additional $38,400 according to the plan. Until then we will use most of 2018 to dilute our net worth concentration in our home equity. Soon I will also be writing about how we plan to leverage this idle capital sitting to our advantage.

RELATED: Our Mortgage Will Be Gone In Four More Years

Closing Thoughts

The books are officially closed for 2017 and now it’s time to begin writing living the narrative for 2018. This blog is all about real life experience!

My focus is aimed towards those 2018 goals I shared. A theme for 2018 is to regain some balance. I want to play as hard as I work, and right now the lines between my work and play are very blurred. I’ve mastered the work-life blend a little too well, meaning…the mixture has been a little work-rich. Now I need to course correct. I have a new hire starting this week, so that will have a huge impact after about three months of ramp-up time. I am also in the process of assembling a team to grow and manage the GYFG blog. I have recently brought on the following people:

– Lin: She is the Chief Editing Officer and the one responsible for the polish you have probably noticed on my posts these past few months. I’m grateful for her help and involvement in the GYFG project. [Leaping run-on sentences in a single bound, defending the sanctity of grammar wielding semi-colons and commas as weapons of mass correction, I am humbly at your service, GYFG community! Lin]

– Brandon & Kyle: Co-Chief Growth Officers, their mission is to grow the site’s traffic, as well as our email subscribers, revenue, and social media followers.

Assembling this team is going to help me work towards the bigger vision I have for the GYFG blog and community. Please stay tuned in, as this vision unfolds in the months to come.

After three years as a one man band, it is time to level up. This is true for the blog, my day job, and personal life. As I mentioned above, I have hired help at work and will be shedding a decent amount of work over the next three to six months. As I have shared previously, I have also hired a personal trainer, personal development coach (program mentioned above), and chef (food prep service). Don’t worry, I’m not getting soft, I’m just evolving and laying the foundation for the next leg of this incredible journey.

I’m determined to master the art of having it all across body, being, balance, and business!

I look forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

p.s. I recently had the opportunity to be interviewed by Erik from The Mastermind Within. The conversation we had was fun, informative, and filled with some great nuggets of wisdom. It was deeply gratifying that Erik reached out to have me on the podcast, as the greatest compliment I could ever receive is knowing that I’ve had a positive impact on someone else. Plus, revisiting The Slight Edge is always great – it’s the book that’s had the most impact on my life!

9 Responses

Hey, I just wanted to let you know that I really enjoy your writing, and thank you for writing. Please keep it up.

I always enjoy your updates. I Started reading your blog over two years ago and its inspired me to hop over into the faster lane of increasing income. It is nice to have another young guy blogging with similar thoughts and process oriented thinking as well as the financial numbers.

I predict you will zoom past me by the end of this year in the fast lane on the net worth train and I’ll never catch up. Not going to be disappointed at all.

Once thing I was curious about:

Your equities pie slice seems awfully low compared to the other slices.

Its seem that your income is doing all the heavy lifting where the equities could be there lightening the load and increasing your NW much faster.

Jason –

First, thank you for following along for the past two years.

Second, kudos for jumping on the income fast lane.

Your observation is not wrong. The equity pie slice is small compared to the other slices and is a result of a few things:

(1) In March/April of last year, I liquidated about $70,000 in an old roll-over IRA (that was invested in stocks), opened a self-directed IRA, so that I could invest in hard money loans through PeerStreet.

(2) I also took a $25,000 loan from my 401K to help with a cash flow issue, when I decided to put my brother through rehab. I had already committed about $120,000 to other investments and didn’t want to be left with a zero balance in our checking account (but we paid it back last summer).

(3) I have been severely under-invested for the past few years as I waited for a correction to put idle cash to work. However, I am changing that going forward.

(4) But don’t be fooled, we have also been putting plenty of money to work outside of equities: Commercial Real Estate, Life Settlements, Private Companies, Hard Money Lending, etc.

Cheers,

Dom

Your growth plans sound very exciting. I’m looking forward to seeing how the hires impact the site. Great recap of January and I’m focusing on health some more too. Weirdly enough that means cutting back on lifting and doing cardio instead since I’ve been feeling sore in my upper body. To health and wealth and in that order!

Thanks, SMM!

I like your priorities, we are aligned in 2018!

My advice for achieving body, being, balance, and business is to try and put rest, recovery and sustainability at the heart of what you do.

Trick is to go hard but don’t burn out:

Body – Train right to the edge, stretch, sauna, alternate body parts that are getting a work out.

Being – Don’t be afraid of a bit of introspection, have a think about what’s driving you and how best to use that self-knowledge.

Balance – Not too much work, not too much play, try and keep everything in moderation.

Business – I think you have that one down all ready, as you were ;-P

HH

The inversion table is a terrific idea. It works! I have two bulging disks dating back 20 years ago (deadlifts, awful!) I have a suggestion for your herniated disk. Buy the DVD set from http://www.ddpyoga.com

This yoga DVD system is GREAT, it will heal your back and will improve your overall health. Warning, it’ll get strenuous as your progress!