Based on the short amount of time I’ve been writing, you may have gotten the wrong message. Yes, I am working diligently to pay off the mortgage early on my primary residence. However, this does not mean I think all debt is bad or evil.

Consumer debt is pure evil when you are the borrower! If you are the investor/credit extender it can be very profitable (check out Prosper if you would like to get a piece of this action). If you have consumer debt, pay it off as fast as humanly possible, and never look back.

When it comes to non-consumer debt or what I like to call productive debt, I am totally for it. Before we talk about what your leverage ratio should be as an individual, let’s first define the characteristics of productive debt.

What is productive debt?

- It is money borrowed to finance your primary residence. This is a step above renting in that it gives you a tax write off and the ability to build equity in an asset. It also allows you to turn your housing into a fixed expense that is not subject to annual increases like rent is (except for property taxes).

- It is money borrowed to finance an investment property. In my opinion it needs to be cash-flow positive from the beginning if it is a rental. Or at the very least it needs to give you more benefit than its costing you (i.e. on your taxes). Just make sure the numbers pencil out.

- It is money borrowed to finance a business. But with today’s technology it is highly probable that you can avoid borrowing to start a business and bootstrap your new venture unless it is some sort of brick and mortar type of business.

- It is borrowed money in your brokerage account in the form of margin. I know people that do this very successfully, but I wouldn’t recommend it for everyone.

- It is borrowed money to fund your college education. I contemplated whether I wanted to include this in the list or not. Studies show that a college educated person is going to make more money than someone without a degree. Of course there are exceptions to the rule, but most of us are not the exception. Just make sure you have a positive mathematical expectancy (i.e positive ROI).

These are really the only forms of debt that make sense to carry on your personal balance sheet in my opinion. These could all be argued, but that is not what this post is about.

How much should you be leveraged?

Ah, that is the $64M dollar question.

Leverage is a double edged sword as they say.

When things go your way, leverage will magnify your gains. When things go against you, leverage will magnify your losses.

When borrowing for a house, you should not borrow more than 2-3 times your annual salary. This keeps monthly payments low relative to your monthly gross income. This rule of thumb gives you a chance of paying off your mortgage way ahead of schedule if you so desire. It also ensures that you are not “house rich” and “cash poor.”

However, we are not just talking about how much to borrow for a house. We are talking about your total leverage on all productive debt (as defined above).

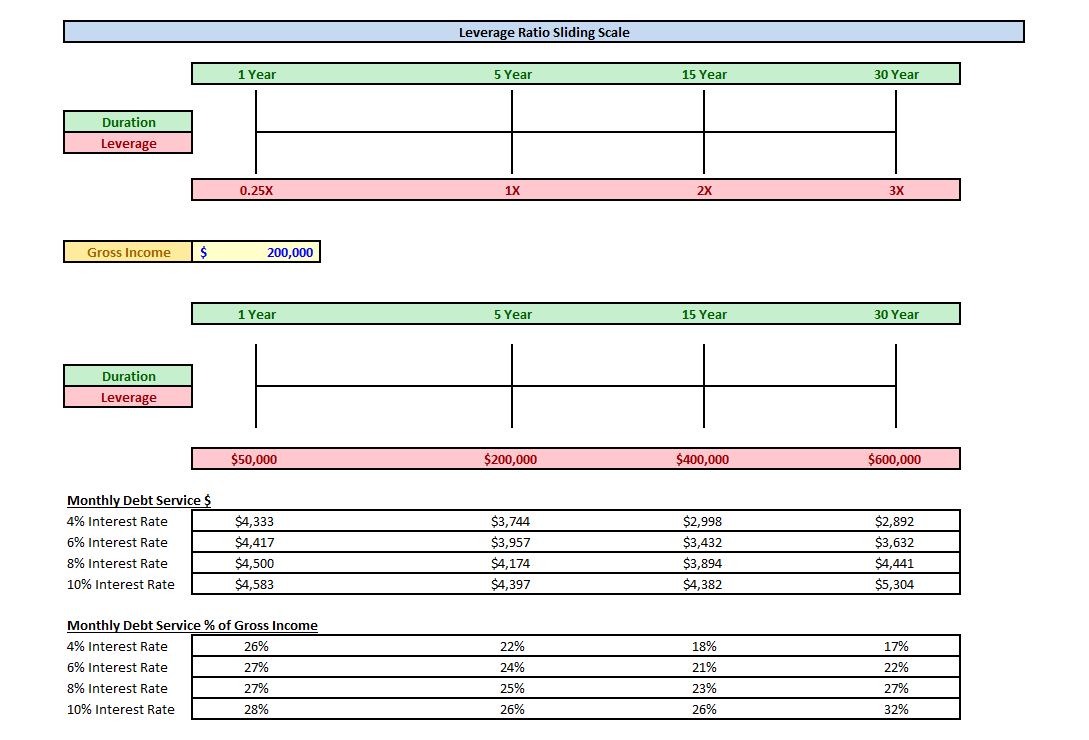

Leverage Ratio = Total Debt/Gross Income

Your leverage ratio should really operate on a spectrum from ‘0 X Gross Income‘ to ‘3 X Gross Income.‘ The longer the duration the more leverage you can responsibly manage. The payments will be lower since they are spread out over a longer period of time.

Shorter duration comes with higher payments when you keep borrowing amounts the same. Meaning that a monthly payment on a 5 year loan for $100K is going to be much higher than the payment for the same amount over 30 years.

This sliding scale (below) is just to get a good rule of thumb when determining how much leverage you can personally take on. Once you figure out where you are on the scale by using your gross income and the duration of the debt, then you should take that number and look at the minimum debt service as a percentage of your gross income. I personally don’t want debt service to exceed 35% of gross income. I currently have two mortgages totaling $500K with a minimum monthly debt service of $2,600/month, which amounts to about 14% of gross income for us.

4 Factors to consider when determining your leverage ratio

- Duration – How long is the borrowing period?

- Rate – What is the interest rate on the debt?

- Income – What is your monthly gross income in relation to debt service?

- Liquidity – How many months could your liquid assets cover your monthly debt payments?

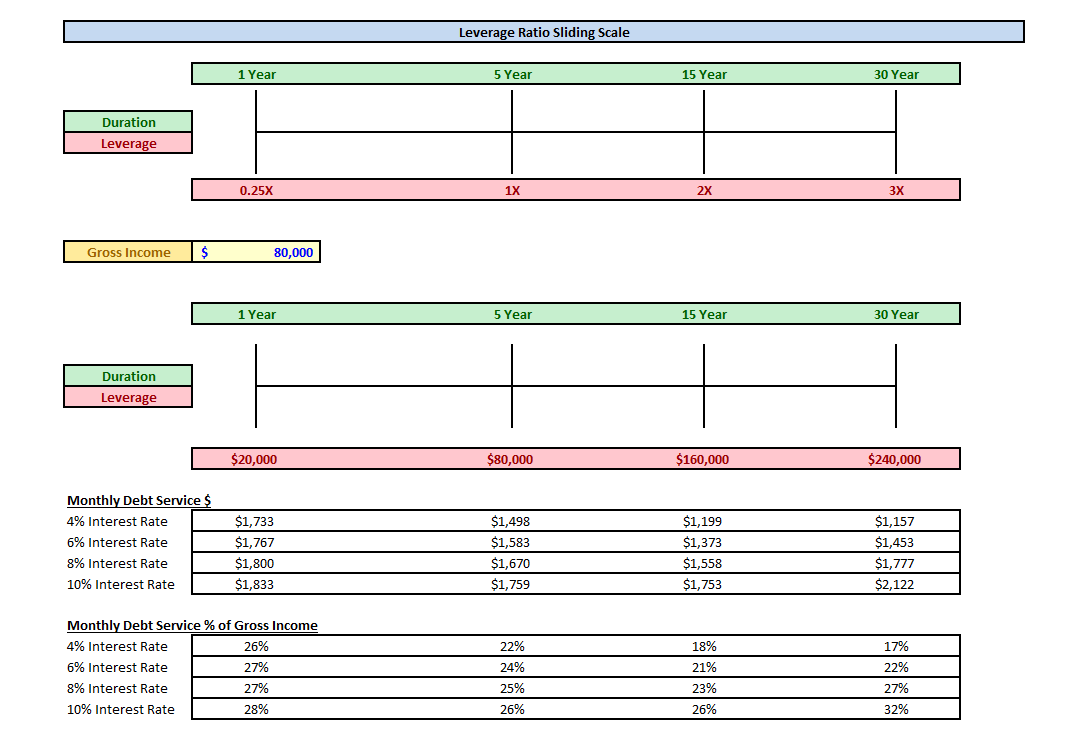

Debt service should be no more than 50% of your gross income (as I pointed out above, I personally don’t want to see it be more than 35%), and I would recommend that you have at least 6-months in reserves in case something happens to your income. Let’s go through an example using the above sliding scale of someone with a $80K gross Income (we will call him Jimmy).

Assumptions:

- Gross Income = $80K ($6,666 Monthly)

- Interest Rate = 4%

- Liquid Cash = $50,000

Initially the sliding scale would indicate that Jimmy would be okay borrowing up to $240K based on a 30 year duration and a 4% interest rate. His monthly debt service payment to amortize the loan would be $1,157/month, which only represents 17% of monthly gross income.

With $50,000 in the bank, Jimmy has a little more than 43 months’ worth of reserves to cover the debt in the event something happens to his income stream.

Jimmy has my stamp of approval to go to his max of 3 X his net worth in leverage.

Note: Technically Jimmy could leverage up even more because of such a low interest rate. At a 4% interest rate, Jimmy could probably take out a loan for $720K. This would put his leverage ratio at 9:1 and his monthly payment at $3,471 (or 52%). But after 25% for taxes, Jimmy would be looking at just 23% of his income for living expenses and savings/investments. I wouldn’t recommend it.

Conclusion

I know its a very simplistic model. But sometimes its good to just keep it simple. I probably don’t have the same appetite that some have for leverage, only because I have seen people first hand get destroyed by using too much of it. It is also worth pointing out that the interest rate has a very heavy influence on how much leverage you can take, especially the further out in duration that you go.

I am confident that this personal leverage model will keep me out of trouble. It may be conservative, but that is completely fine with me. I would rather be conservative on the debt front and aggressive on the income front. Plus it is good to keep in mind that this is only one form of leverage and they call it OPM or Other Peoples Money.

Do you want to download the model to use yourself? You can do it here >> Personal Leverage Ratio

What do you think? Would you make any changes? How does this model fit your personal risk profile when it comes to leverage?

– Gen Y Finance Guy

2 Responses

I agree, people need to pay attention to leverage no matter if they are risk averse or very aggressive. I am more aggressive with keeping low cash reserves, but I also have low debt.