A while back a fellow blogger and friend of mine, Mr. 1500 or 1500days.com, wrote a piece on whether you should pay your mortgage off early or not. I don’t disagree with his logic as it makes perfect sense. However, like many things in personal finance, I have a hard time with absolutes. Instead “it depends” is a much better answer. Today I am going to make the case for paying off your mortgage early, given the right circumstances are in place. Depending on your own personal goals and circumstances, this may be a viable option for you to consider.

Usually the argument goes that you should keep your mortgage, especially given the historically low interest rates. The thought process, which I don’t disagree with, is that if you can borrow at say 3.75% for a 30 year mortgage, and invest at say an 8% return by investing in a broad based index fund like the SPY (tracks to S&P 500). In theory you should do this all day long every day. There is also the argument for liquidity. It’s true you have faster access to cash by liquidating your investments than you do in tapping the equity in your house (unless you have a home equity line of credit).

On the other hand paying extra principal on your mortgage to pay it off early is getting you a guaranteed return equal to that of your interest rate. But maybe that is not enough to entice you, you say “I am willing to take the risk for closer to market returns.” What if I told you that it’s possible to engineer better than market returns through strategic refinancing and accelerated repayment? Again, this does not apply to everyone, but this is an example based on my own personal experience.

The Back Story

My wife and I were in the market to buy a house as we were tired of paying the ridiculous $3,100/month in rent. No doubt we were living the high life (literally in a high rise) and in luxury. The affluence in our high rise apartments was crazy. We ended up here after giving up on our original house hunt in early 2013. House prices in Orange County were ridiculously high, and we didn’t love anything we were seeing. We also were not very fond of signing up for a $750,000 mortgage either, after PMI & Taxes, we would have had a payment of $5,100/month. So, we opted to live in luxury (a sort of limbo if you will) while we reevaluated our options.

After a year of living the baller lifestyle, we decided to do a little domestic geo-arbitrage and move about an hour inland in order to get access to a housing market that was way less expensive. Where houses were going for half the price and were 4-5X the size.

We wanted to buy a house so that we could stop throwing money down the drain and start building some equity. But we also wanted to save a substantial amount from what we were currently paying in rent.

Mortgage #1

We found the house for us on our first outing with our real estate agent. Actually we had been looking for a few months online and narrowed our list down to the top 3 to see in person. Number 2 would be the lucky winner. We paid $370,000 and financed $355,000 of that purchase price. Since we only put about 4% down, we ended up with an FHA loan that cost us $6,000. We didn’t have much in the way of closing costs since our agent was a family friend and did the deal pro bono, and my wife is in the escrow business. After everything was said and done we were responsible for about $1,500 in closing costs on top of the $6,000 for the FHA loan.

Total Investment = $22,500

Free Cash Flow* = $895.28/month or $10,743/year

Annual Cash on Cash Return = 47.7%

*Free Cash flow was calculated by taking the difference of $3,100 in rent vs. new mortgage payment of $2,710.77 (includes property taxes, HOA, and PMI). The initial savings between these two was $389.23. Because interest and property taxes are tax deductible, we need to add $506.06 in monthly tax savings (based on 30% tax rate, which is conservative) for a total of $895.28/month in total savings.

**The loan we took out was a 30 year FHA loan at 3.75% with 1.35% PMI for the life of the loan.

This was a no brainer for us. I couldn’t invest in anything that I know of for this sort of guaranteed return. And to put things into perspective further, in order to earn the same $10,743 by investing for an 8% return, one would have to invest $134,288 (or about 6X our total investment). Or, if you wanted a to earn the same from a safe CD, at 2% you would have to lock up $537,150.

Refinance #1 [Mortgage #2]

As much as we hated to go with an FHA loan, it was really the only option we had based on what we were willing to put as a down payment at the time. However, the plan was always to refinance out of the FHA loan as quickly as possible, if to only save the 1.35% we would have to pay in PMI for the life of the loan (these requirements have since changed).

Within 8 months of taking out the first loan we found the opportunity we had been looking for to refinance our loan to remove PMI without 20% down. We joined a credit union that was offering a 5/5 option ARM at 3.625% with zero origination fees and zero points. We would be able to get this refinance done for about $1,000.

Incremental Investment = $1,000

Free Cash Flow* = $438.13/month or $5,257.56/year

Annual Cash on Cash Return = 526%

Total Return Profile after 1st Refinance [Cumulative]

Total Investment = ($22,500 + $1,000) = $23,500

Free Cash Flow* = $1,333.41/month or $16,000.92/year

Annual Cash on Cash Return = 68%

A whopping 68% return, again I have no idea where you can get these types of returns, if you are aware of them, please let me know. Also, in order to achieve the same $16,000 in cash flow from investing at 8%, one would have to invest $200,011. Or $800,000 in a CD earning 2%.

*Keep in mind that investment is what could had been invested in the market, but instead was put towards the mortgage.

About 4 months into the new 5/5 ARM, we had finalized our plan to pay the mortgage off early. One of the major hypotheses was that the the market would return much less than historical returns and that there was a high probability that we would soon be entering a recession. In plain English we believed and continue to believe that the imputed 3.625% that we would be earning by making extra payments to the mortgage would be better than what would be earned in the markets over the next 5-7 years.

If we are wrong, the worst that would happen is that we under-perform the market (or would we???), but would still have a house that was free and clear earning the equivalent of 3.625%. Now I should also add that this was not in lieu of investing, it was in addition. We also do not allocate any of our funds to bonds, as we look at a paid off mortgage as a bond substitute.

So over the last 19 months we have systematically paid an additional $16,000 in principal on top of the normal loan amortizations (this was as of April 2016).

We realize that this dilutes our annual cash on cash return.

Incremental Investment = $16,000 @ 3.625%

Annual Cash on Cash Return = 3.625% [equivalent]

Weighted Average Return (before refinance #2)

Total Investment = ($23,500 + $16,000) = $39,500

Annual Cash on Cash Return = [($16,000 * 3.625%) + ($23,500 * 68%)] / $39,500 = 42% [weighted]

*Keep in mind that investment is what could had been invested in the market, but instead was put towards the mortgage.

Refinance #2 [Mortgage #3]

We were not really looking to refinance per say, but with market volatility heating up and rates dropping, it got us curious. At first we considered refinancing our investment condo, but found out that we could not for various reasons that I will not go into here. Then we wondered what a refinance would look like on our house. Specifically a cash-in refinance. Since we didn’t yet have an 80% loan to value (LTV), we would need to bring money into the deal.

This time we decided to go with a 3/1 ARM that again was through the same credit union and the cost would be $1,000. The loan itself was zero origination and zero points with a starting interest rate of 2.25%. This time it was going to require that we bring in $21,000 in order to get the 80% LTV.

Incremental Investment = $22,000

Free Cash Flow* = $382.11/month or $4,585.36/year

Annual Cash on Cash Return = 21%

So, the question that is probably going through your head, or that should be going through your head, is “what will the blended return be over the life.”

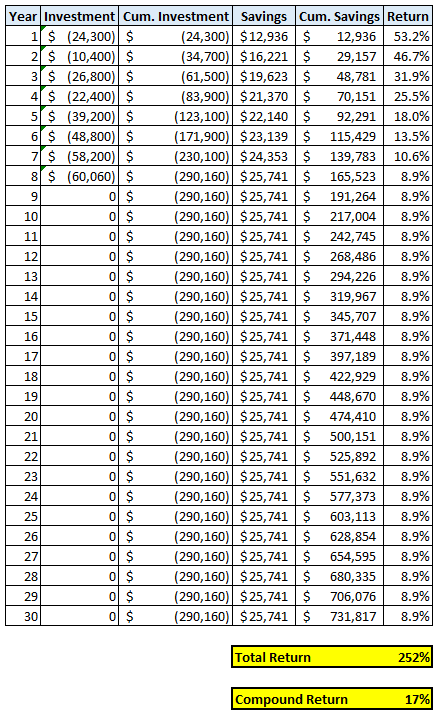

In order to calculate the annual return on investment, we have to cash flow the savings and investment by month, so that we can get annual figures. These figures are going to vary a bit from the numbers mentioned above, as they are cash flowed based on actual savings and investments.

Now that we have the table built out with the timing of investment vs. savings, we can go ahead and figure out what the annual return profile is looking like.

Remember that a dollar saved is equivalent to a dollar earned.

Actually it could even be argued that a dollar saved is greater than a dollar earned, as it has already been taxed, so you get to keep 100% of the savings. The alternative is you have to give X% of every additional dollar you earn to the government. Look at those returns created in the first 4 years…they make me very happy 🙂

It’s amazing that we have already saved almost $50K since buying our house (we will complete YR 3 in February 2017).

Update: I should point out that the returns you see in the above table are not compounded returns. The compounded return over the 30 year duration would be 4.3%. If you want the quick easy math for converting a total return over a certain time period into a compounded annual return visit this link.

In the table above you can see that I continued the annual savings of $25,741/year through 30 years in order to calculate the total savings over the life of the typical mortgage length. We never intended to keep our mortgage for 30 years, but we did plan to enjoy the savings we financially engineered over the full length of the mortgage. If you really think about it, once you have a paid off mortgage, you have essentially created a synthetic dividend for life.

Wow! Looks like you can synthetically create a better than “market” return using your own mortgage combined with a little strategic refinancing and through financial engineering, voila. This is just another way to answer the question of “should I pay my mortgage off early.”

What do you think? Is this math surprising to you? I don’t think I have seen this done anywhere else online. Again the circumstances have to be right, this won’t work out the same for everyone. Also in the post that Mr. 1500 did that I linked to in the beginning of this post, he was contemplating paying cash for his house vs. investing…same question, but different variables. The point of this post is really to show you that there are rarely absolutes, and many permutations to what may seem like the same question.

– Gen Y Finance Guy

10 Responses

GYFG,

Brother every time I read your posts, I feel like a C algebra student in an MIT physics class. Your shit is definitely on another level.

In all seriousness, I think most will probably do what allows them to sleep best at night. In my case is was simply paying that bitch off as soon as possible and keeping it paid off.

MDP

Hey MDP – I couldn’t help but picture you in a physics class studying to be a rocket scientist. The math angle to this whole personal finance journey is really fun for me…if that wasn’t already totally apparent.

But your right, it can be as simple as doing what helps you sleep at night.

Looking forward to joining you in the mortgage free club.

Cheers

First of all I commend Gen Y with sharing his path to home ownership and the financing along with the refinancing of his mortgage on his new house. This is very good information when buying and refinancing your primary residence.

However, there are significant hidden costs when purchasing a new home especially after renting. There is one thing for sure when buy your new home. Home ownership is expensive! Plain and simple. Let me explain and I will give some examples.

Moving Cost – Unless Gen Y was able to talk his college buddies, relatives, co-workers into hauling his refrigerator, washer and dryer, beds, and tons of boxes moving cost can run $3500 when moving within Southern California. $12,000 or more if moving across the country. Maybe he got lucky and was able to spend less than $100 on burgers, hot dogs, and beer for everyone who helped out. I use to think it was fun moving my friends around after college thirty years ago. Don’t ask me anymore because I don’t enjoy lifting, pushing, and stacking boxes at my age. Let’s say $3500 moving cost.

Furniture- Do you really think son’s Johnny and Steve want to use their bunk beds from when they were 4 and 6 years old now that they have their own rooms and pushing middle school. Do you think the wife wants that old and dilapidated couch from Aunt Emma or the old kitchen table that the kids used permanent markers to doodle and write their names. If you’re moving from a 2 bedroom apartment to a 2400 square foot 4 bedroom house furniture cost can add up quickly. Patio furniture, barbecue… Let’s say $4000.00

Repair Cost- Hey is great when you rent… if the toilet is backed up, electrical outlet shorts out, window is cracked you just run to the manager on site or landlord. Not so when you’re a home owner. Hope you are a (DIY) do it yourself like me. A good handy man can cost you $75-$100 an hour plus material. Home Depot and Lowes loves me. As always I can never get out of the store without buying something else. Garage door, springs, openers, kitchen faucets, electrical, plumbing… this stuff can add up quickly. If you have a pool and Jacuzzi leaks, heaters, and new tile can run into the thousands. $2000 a year.

Homeowner fees, Association fess, and Melarose tax.- Gen Y maybe lucky and not have to pay any of these in an old neighborhood, but most new neighborhoods in So Cal you will have to pay. I pay $235.00 a month for maintenance and lighting. No common pool or Jacuzzi! Let’s say $2400 a year.

Lawn care- Oh yes the lawn grass does grow. I maintained my lawn and property (plants, shrubs, trees) for 14 years. I remember in the So Cal heat I would be drenched in sweat mowing the grass and my neighbors would come out of their air conditioned house get into their air conditioned car. Then they would smile, honk, and wave to me as they drove buy. Gardeners $1200 per year.

Maintenance Cost- Need a new roof, drive way, house paint, fence is starting to sag. Pool and Jacuzzi maintenance can run $200-$300 a month. This can also add up quickly. $3500.00. Maintenance cost can be ongoing so you should also set aside some money.

Utilities- Use the air, water the grass more, 3-4 TV’s in the house, Wi-Fi, computers in every room, washer and dryer going. Have a pool and Jacuzzi. Guaranteed that your utilities will go up. My neighbor said his electricity cost were $500 a month. Of course his family set his thermostat at 62 degrees in the heat of summer. Extra $1200 dollars a year.

Pets- Why else would you get a house with a yard. Mommy, Johnny, and Steve brought home a cute little puppy. Well this little puppy does not come cheap. I have a yellow lab,… he’s chewed up my patio furniture, pulled the direct TV cable out where it goes into the house, came within centimeters from biting completely into the 220v line that goes the AC. Guess who picks up the po…p? Vet bills, food, shots, license.. can add up quickly. $1000 dollars a year.

Misc- Renovations can be a significant cost- redoing a kitchen, bathrooms, and bedrooms can run $20,000-$50,000 easily. An old co-worker of mine was always doing something to their house. Landscape the back yard, re-built the garage, and new roof. Last time I talked to her they were not happy with the house and decided to renovate the whole house. They bought the house 4 years ago and it was turnkey when they bought the house. I could go on and on.

If you are already a home owner you probably can relate to what I’m talking about. Given some of these costs are one-time, now the cash free cash flow of $10,743/yr and $16,092/yr don’t look so great any more. Not to take anything away from Gen Y’s great work, but home ownership should not be taken lightly. Do your homework with all the hidden costs? Be careful because your dream home can drain your wallet fast. It can become a bottomless pit. Try not to become house rich and cash poor. Good luck!

I try to make extra principal payments every few months or at least during months when I don’t invest in the markets. If I have extra cash flow, I’m happy to pay down debt. If only my mother had the same mentality. She just doesn’t seem to have any sense of urgency to get out of debt. Even if she had paid off her original mortgage when it was due and not made extra payments her financial situation would be so different today.

That is fantastic Sydney! It is always sad to see friends and family making poor financial decisions, but even tougher when it’s our own parents…they are the ones that are supposed to be passing down good financial habits right?

Great analysis and math here. I don’t own yet but I like to plan some tricks ahead of time.

So bottom line: you moved from the city paying $3100 for rent to being on track to owning your own home (but adding an hour commute for you and your wife) in 8 years, without changing your income or lifestyle (besides the longer commute)

A few questions:

1. Could you just have skipped Mortgage #1 and bought the house with Mortgage #2 if you had known about it?

2. Have you looked into using a HELOC, where you would minimize your average daily principle with your consistent income cash flow paid into it and also have a credit line available for emergencies?

Jason – one correction we actually don’t have a commute, in fact my wife got rid of here 45 min to 1 hour commute. We both work within 5 miles from home.

The short answers to #1 is yes.

And to #2 no. I think I have read about such a HELOC, but do you have more information or a link to how the mechanics of this work?

I first heard about it from a company that sold software to help you maximize your cash flow and told you when and how much to pay down the HELCO and mortgage. Recently I’ve seen new people online marketing a ebook and info and how to do it yourself replaceyourmortgage.com Also, there is one mortgage company that offers a HELCO type of mortgage that integrates your checking account with it http://www.aioloan.com/ More fun math for you to play with!

These programs I believe are designed for people that don’t have a ton of extra cash flow and already have 80% equity, whereas in your situation you have a lot of discretionary income. Not easy concepts to quickly gasp, but look I think you’ll find it really interesting. Let me know what you think. I’m getting married soon and doing my homework early.

Thanks Jason, I am looking forward to checking it out.