We have officially begun a new year and with that I have decided to start a new quarterly series. As many of you know that have been reading for any length of time, every month I put together a very detailed financial report that details out gross income, expenses, net worth, savings rate, and progress on the 7 year 3 month mortgage pay off goal. Since the report already pushes 3,000 – 4,000 words a month, I thought it would be more appropriate to provide details of the equity portfolio in an entirely separate post.

Also, I don’t really see the benefit of updating this on a monthly basis, quarterly should be just fine.

One of the guiding tenets of this blog is that of FULL TRANSPARENCY. This is another step in living up to the high standards we live by here at GYFG.

This will serve several purposes:

- It will force me to analyze the performance of my portfolio.

- It gives you a better view of what is under the hood.

- It will also provide some visibility around where the increases come from. Too many people overestimate their returns and forget about new money contributions, company matches, dividends, etc.

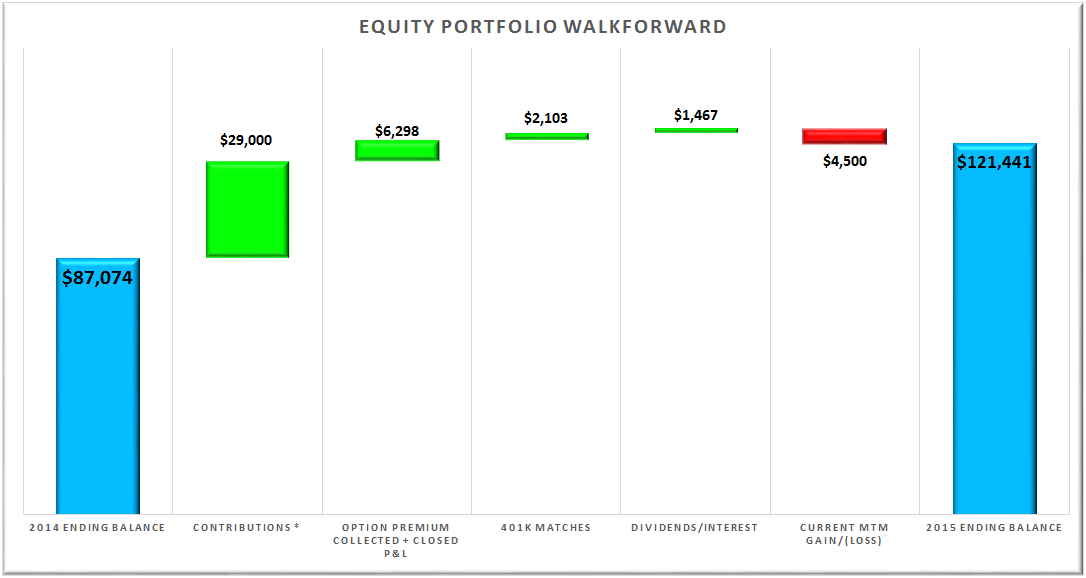

Breakdown of Portfolio Performance [12/31/15 vs. 12/31/14]

You may have noticed in the title of this post that the portfolio is up 39.5% in 2015, and I will be the first to admit that this is a bit misleading. But never fear, I will be breaking down the components of where the gains came from and will also be comparing the performance to the S&P 500 as my benchmark.

For many of you this will be your first time seeing a waterfall chart. If this is your first time I hope you like the visual of how the portfolio grew and what made up the gains.

Now let’s breakdown the buckets…

2014 Ending Balance = $87,074

[+ $29,000] Contributions – 2015 Contributions Include: Maxing out 401K for $18K [2015], Maxing out IRA for $5.5K [2015], and Maxing out IRA $5.5K [2014].

[+ $6,298] Option Premium Collected + Closed P&L – This is representative of the option premium I collected for selling cash secured puts, covered calls, other option selling strategies, and any other realized gains from closing stock positions.

[+ $2,103] 401K Matches – At this time I am the only one in the GYFG household that has a qualified retirement plan through work that offers contribution matches. Currently the company I work for offers 25% on up to 6% of your income. Next year this is increasing to a 50% match, but it will only be on up to 4%.

[+ $1,467] Dividends/Interest – One of the rules I use when selling covered calls or puts is to only do this on stable companies with a long history of paying dividends, and a dividend rate of 3% or greater. It is just another way I look to increase my margin of safety in the event that I am exercised and forced to take a stock position from short puts. Or it also helps to reduce cost basis on long covered call positions, until the stock is eventually called away. The interest is very minimal and comes from interest on cash sitting in my brokerage accounts.

[- $4,500] Current MTM Gain/(Loss) – I currently have $26,200 invested, which is for 5 covered call positions that I still have on. I will detail them later in the post. This is a little misleading by itself, because some of the premium from the $6,298 above offsets these open MTM losses.

2015 Ending Balance = $121,441 [+ $34,367 or + 39.5%]

Now that you can see the detailed breakdown you realize that a large part of the portfolio increases came from new contributions. When you back out the contributions you are left with the investment gains.

Note: I include the 401K match as an investment gain. It is not money I contributed and I don’t distinguish it from market gains.

This leaves a gain of $5,367 or 4.6%.

This compares to the return of the SPY (ETF representing the S&P 500) of -0.8% before dividends or 1.25% with dividends.

Note: the SPY gain was calculated taking the 2014 closing price of $203.87 and total return here.

In future updates I will also accompany this with screenshots from Personal Capital as another level of TRANSPARENCY. I haven’t included them here because I only set my own Personal Capital account in the middle of this year, so the history is incomplete.

What is the Current Make-up of the Portfolio?

First and foremost I should remind you that of the $121,441, only about $26,200 is actually invested. The rest is sitting in CASH as we close the year. This leaves me sitting with 78% of my investable assets, across my brokerage accounts, in CASH. Over the course of 2015, I was sitting on average of about 50%. This is very telling with respect to how I feel about current market valuations.

I started raising cash at the beginning of the year. I even detailed a post with a 4 tier system to deploy it should the market finally see a correction. That post was written back in April when I had about $63,000 in cash sitting in my brokerage accounts. Today that has grown to $95,221. In addition to this cash stash, we have also been building up our savings account that currently has about $70K in cash as I type this, and is about to surpass the $100K mark by the end of January.

We are preparing ourselves to take advantage of much better prices ahead. I don’t fear the erosion of inflation on the purchasing power of our dollars. I actually think that cash will be one of the best performing asset classes in 2016.

Current Open Positions and MTM Gain/(Loss)

- CAT [- $1,578] – $67.50 Covered Call

- OIH [- $700] – $31 Covered Call

- PG [- $742] – $77.50 Covered Call

- VZ [- $270] -$45 Covered Call

- WMT [- $1,210] – $65 Covered Call

Well there you have the first portfolio update. This may evolve over time, but for now this is likely the format that I will be using going forward. The next update will be comparing Q1 of 2016 vs. 2015. I may even consider including performance of my P2P investments, REIT’s, and Rental Real Estate. Or I may even create a separate post series. I have not decided yet…if you have an opinion, please let me know.

How did your portfolio do in 2015? What is your plan for 2016?

-Gen Y Finance Guy

8 Responses

Great looking analytic, GYFG. Now that you have this information, what does it say to you about your investment decisions and weighting? How does this analysis help your decision-making for future investment decisions and weighing risk/return? Did your investments (P2P, cash, covered calls, equities, etc.) perform to your expectations? How do you know? My thought is that unless you can compare your investment performance to a weighted benchmark(s), this is tough to use for action.

My portfolio is pretty simple, 91% cash instruments (3% MM, 88% CDs) and 9% equities. Total return, 2.5%. (slight neg on equities brought down the total from 2.72% on cash). Your outlook for market conditions, risk, valuations align with mine, and I have not been able to make sense of equity performance for several years. My strategy for 2016 is basically “white-knuckle”.

Hey JayCeezy:

Happy New Year!

Glad you like the visual.

What this tells me is that my thesis that the the S&P 500 had a higher probability of finishing the year negative than positive is what pushed me into over 50% cash earlier in the year and had me finish the year with almost 80% cash. When I look at the sources that accounted for the overall gains of the portfolio, I am reminded that I am still at the part of the financial journey where contributions have a much greater impact than actual returns.

I am not big on weightings instead I am a probability based trader that tries to use options to transfer risk (investor fear) to my portfolio from someone else in return for a premium (no different than that of an insurance company). I also knew and am reminded that in periods of low volatility there is way less opportunity to sell premium (insurance) in the market. To me this just means that my underwriting criteria need to remain stringent and not loosen to chase yield. Which ultimately means there will be less opportunity and potentially less reward.

That said I continue to believe that we are entering a period in time where we are going to experience reversion to the mean, while markets normalize and have a chance to digest the move over the past 7 years. In order for this too happen we will either see a large drop relatively quickly OR we will see many years of very low returns (think 0-2% compounded). So, for the average investor that is a less than exciting outlook. But I think for the premium sellers like myself, I believe this “many years of very low returns” will be partnered with much more volatility.

I don’t think I will have a problem outperforming the S&P 500 with my investment strategy. In a higher volatility environment I expect I will be able to deliver 8-12% returns selling options. Worst case I believe my strategy can consistently deliver 3-5% returns. These check-ins will be a way for me to measure that and hold myself accountable.

I totally agree on using a benchmark to compare performance. Mine is the S&P 500 as I mentioned in the post. But my goal is to not only outperform but to profit every year whether the market is up, down, or sideways. I don’t really call it a win when the S&P 500 is down -10% and I am down only -3%. The real goal is to beat the S&P 500 and produce positive returns every year.

P2P lending performed well, delivering 5.5% returns in 2015 with no write-offs. Albeit this is a much small part of our net worth, it is an area I plan to allocate some more capital too in 2016.

My non-listed REIT paid out a steady 7.5% dividend in 2015. Depending on if we pick up another property or not will determine if we put more money here.

CD’s delivered 3% returns…will likely renew these as they just matured this past week.

Overall I am happy with the performance. I will continue to make savings/contributions my primary focus and make will likely be relatively conservative with how I invest until another major reset (i.e opportunity of a lifetime) comes around.

Cheers,

Dom

hey GYFG,

It is especially your option premium that I find impressive. My personal goal for 2016 is 1000 EUR, so seeing making someone approx 6000 is really inspiring.

Next to that, I like the idea of stacking up cash until a major opportunity comes by again. For now, I lowered my monthly investment and put the rest aside in cash. I stay invested with the rest. I actually consider lowering even further to have more cash. Our cash is now about 10 pct of the portfolio.

AT

Hey AmberTree!

Hopefully 2016 will bring Volatility back in a big way so we can both double our premium sold.

Cheers!

Awesome! Yes I’m looking at my portfolio the same way and getting nervous about what that MTM will look like over the next year for me. Solid thinking of holding on to the cash…

The hard part for me is figuring out the best time to deploy it. Ideally it’s at the bottom of the market but who knows. Any idea when you will start buying? Shares are looking pretty bad already.

Also, another transparent measure I like to look at for myself is how my investment performance (i.e., shares only) compares to the SPY. If you take out that cash weighting, it gives you a better look at how your pure stock picks are performing, when you could have put that in the SPY. I’d like to see more of your portfolio, how much you’re investing in each company vs cash etc, as opposed to just the gains (i.e., where is the 121k sitting, what’s the return on your cash component).

We gotta be getting close to the bottom on gas prices? I’m thinking of investing some there — super risky… Also, I’m still excited about Netflix.

Hey Will,

When it comes to deploying capital, I believe you just have to develop a plan, pick some spots, and then execute the plan. I personally have a 4 tier system that is at -10%, -20%, -30%, and -40%. The first tier got triggered this past week when the SPY was officially 10% off its highs. My investing strategy and approach to the financial markets is a bit different than the main stream is is a little difficult to convey, due to the way that I utilize options…particularly selling them. I have a post coming out in a couple weeks detailing the way I invest in the market.

I hear you and will take note of the next level of transparency to show positions and size in relation to the MTM loss. If I was not clear in the post, at 12-31-15 my cash position was $121,441 minus the $26,200 I have invested in the 5 open positions I listed at the end (OIH, WMT, PG, VZ, and CAT), all of which I own 100 shares and have a short call sold against each position.

It becomes a bit difficult to show my gains on cash vs. invested assets, again because of options. I personally don’t ever see a reason to be fully invested. Without cash on hand you lack the resources to take advantage of deals. I tend to be much more opportunistic. Nonetheless I will continue to try and provide more transparency as time goes on.

Regarding Gas Prices – I assume you mean oil in particular, which has taken a really bad beating. I figured that oil would dip below $30/bbl before stabilizing. It is probably a decent time to start nibbling. The story at the bottom is really compelling for the bears that this thing is going to zero…but that is usually when the tide is about to turn. However, there are likely some smaller companies that will go bust in 2016 as their hedges expire and the price they get for their oil is less than they need to service their debt.

Only time will see my friend.

Nice job maxing out your 401k and those IRAs. You have quite an impressive company 401k plan. I haven’t heard of one so generous with matching before – that is sweet!

Thanks Sydney!

I think I have a pretty standard match program for the 401k plan. Not sure what you mean???

I only get matched on 25% of my contributions up to 6% of my income. That only amounted to $2,108 in 2015.