GYFG here checking in for the July monthly financial report. If you have been reading these reports for a while you will notice that I have the same intro month after month. I do this for two reasons; a) for the newbies to the site (which make up about 50% of the site’s traffic), and b) to remind everyone what these reports are all about. By all means, if you have read the intro at least once, then please feel free to skip down to the “Summary of July 2017” section where the new content begins.

For those of you that are new around this corner of the internet, I wanted to fill you in as to what these reports are all about. These monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of your financial details public, but it’s also a very motivating one. It’s not just the post, but the process of putting this post together that really benefits me.

My sincere hope is that my transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if they are willing to do things differently. If you earn an average salary and have an average savings rate, then you can expect an average result! That means you will likely have to work at a job you may or may not enjoy until you’re 65 and then maybe you can retire IF you‘re lucky.

Hey, there is nothing wrong with average. If you’re happy with average, then, by all means, keep doing what everyone else is doing. Not sure how you feel about that, but I have no interest in living an average life. I want EXTRAORDINARY.

Most people don’t want to live below their means in order to reach FINANCIAL FREEDOM because that’s painful. They think it involves cutting out all the joy in life. You know what I’m talking about, those financial gurus that tell you that in order to get rich you need to cut out the $5 lattes and stop going out to eat. Then after 40 years of diligent and above average savings and super low spending, you will be a millionaire. Basically, you have to live like a college student and suppress all the things you want to do in life and then when you’re old you will be rich.

Okay, that doesn’t sound like the plan for me either.

The good news is there is another way. This site and these reports are here to show you the OTHER path to financial freedom. There is a way where you can have your cake and eat it too. I believe and hope that over time I will be able to convince you of the following:

In order to reach financial freedom you can choose to live below your means by cutting expenses to the bone and living in a state of scarcity or you can expand your means and live in a state of abundance by increasing your income and enjoying the $5 latte or other indulgences of your choice.

Not only that but if you’re diligent you can reach financial freedom a lot sooner than anyone has ever led you to believe.

Our Mission Statement:

To Humanize Finance, Build Wealth, and Reach Financial Freedom.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (because not that many finance blogs or people giving financial advice do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page (as well as annual trends and a few other financial metrics not found in this report). In these monthly reports, the plan is to give you a month over month update on Gross Income, Assets, Liabilities, Net Worth, Expenses, Contributions, Savings Rate, and progress on the mortgage pay down goal.

Summary of July 2017

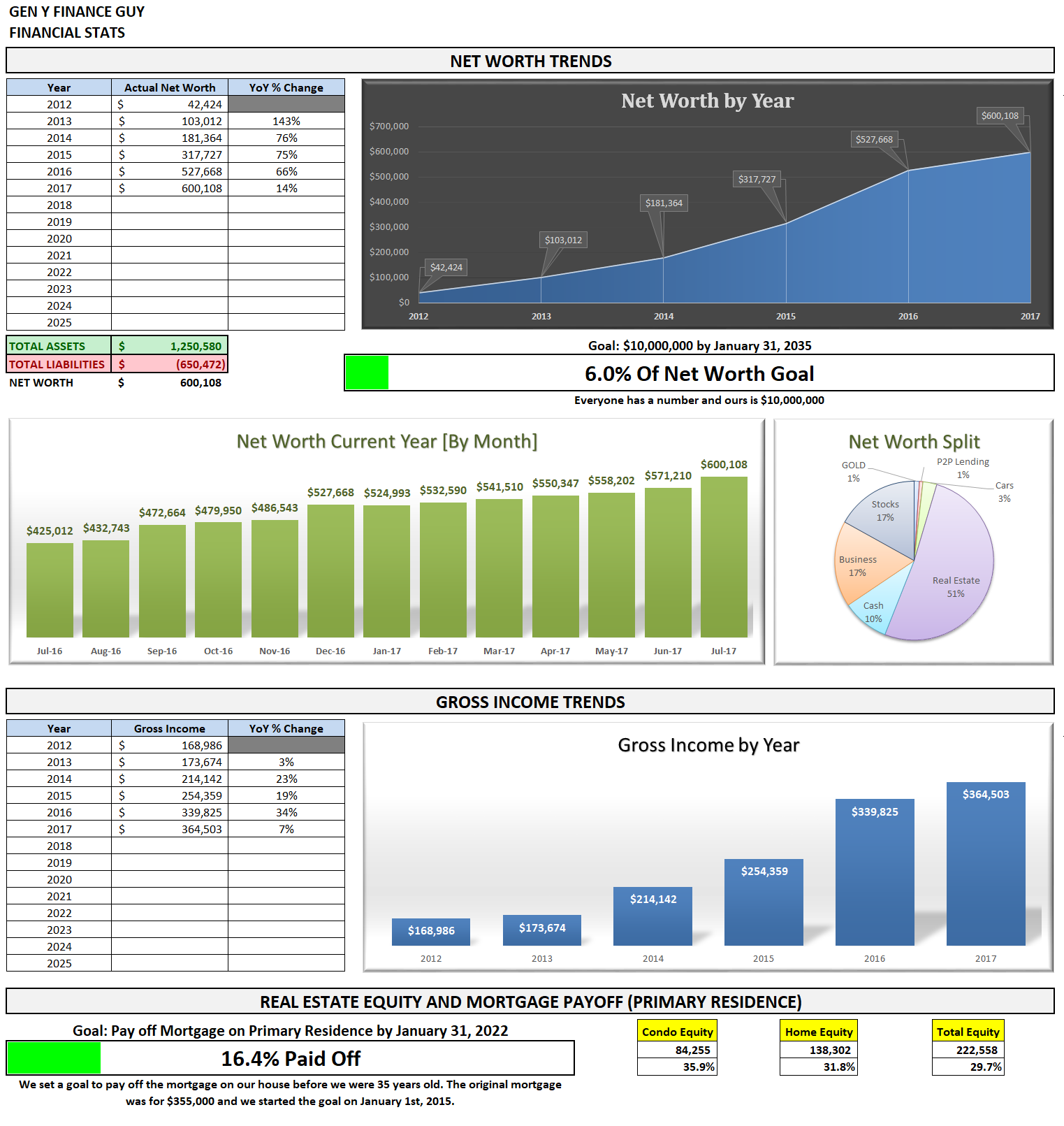

I love that we hit a nice round 6% of our $10M goal! Only 94% more to go, just have to tackle it $100,000 at a time. We should be able to land somewhere in the $650K to $700K range by the end of the year (YoY growth of 23-33%; vs. the 14% YTD).

Wonder how I pull all this information together every month?

We use Personal Capital to aggregate and consolidate our transactions from across all of our financial accounts (checking, savings, retirement, credit cards, mortgages, HSA, and other investment accounts). At the end of the month, I export that information into my financial stats spreadsheet in order to produce this (beautiful) monthly report.

Tracking your finances is, in my opinion, the best way to stay on top of your finances. You can’t optimize what you don’t measure. You can’t make informed decisions if you don’t know what you having coming in vs. what’s going out. Without a holistic view of how much you spend every month, there’s no way to set savings, debt repayment, or investment goals. It’s a financial freedom must!

If you don’t already have a FREE account with Personal Capital, stop reading and go sign up for your account right now! (Seriously, this financial update will be here when you’re done. There’s no time like the present to take action. You will thank me later!)

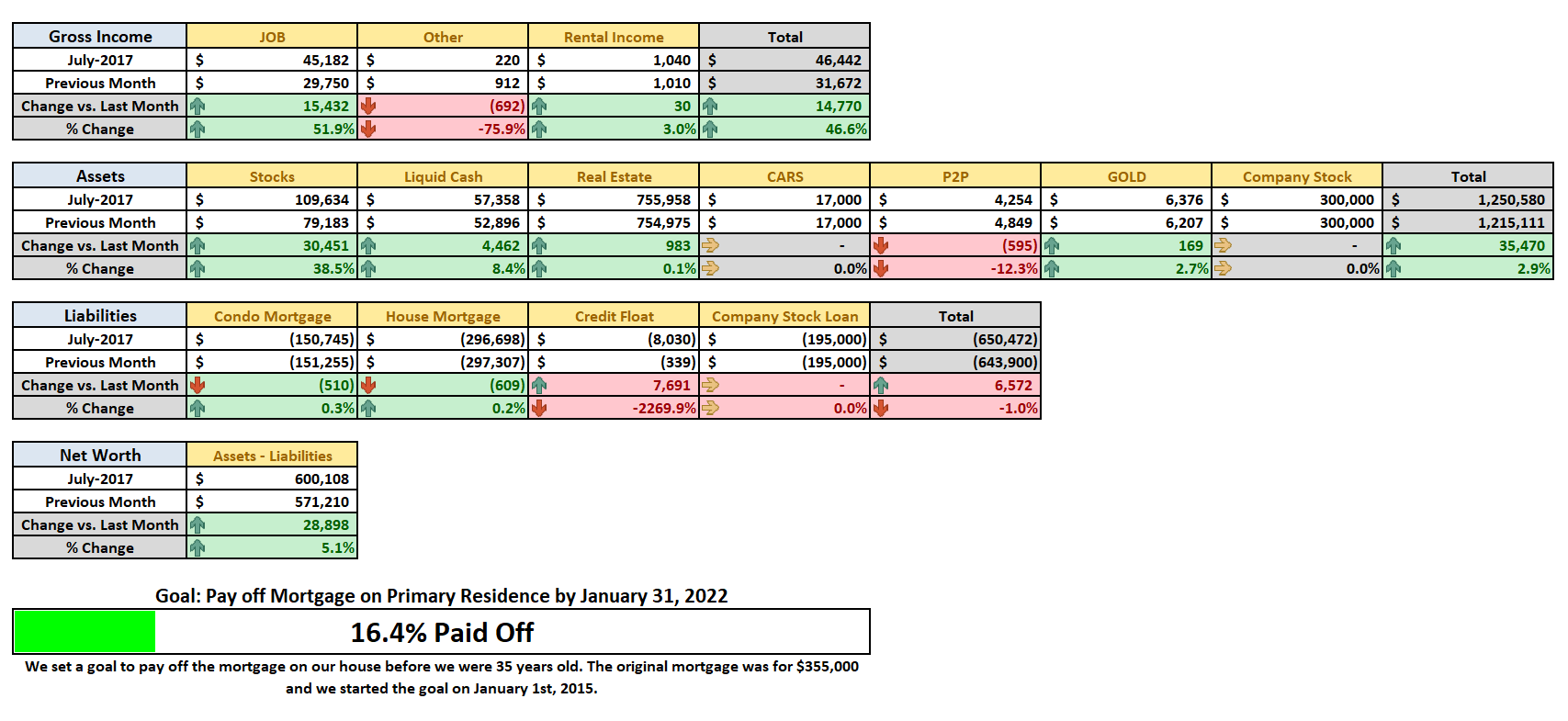

Month Over Month Financial Summary

Just three things to point out in case you missed it:

- Income for the month was up $14,770 or 46.6% vs. June, primarily a result of my mid-year bonus payout.

- Our stocks bucket was up $30,451 or 38.5%. I paid back my 401K loan as expected, contributed more due to mid-year bonus, and also received my quarterly match.

- Overall net worth grew by $28,898 or 5.1% for the month.

INCOME; What went down in July?

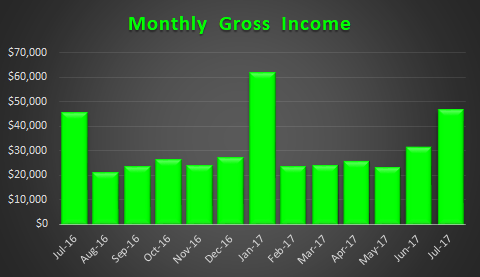

July Income = $46,442

- Previous Month: $31,672

- Difference: $14,770

There is really not much excitement left on the income front for the rest of this year. I will have one more spike in December due to a 3 pay period month, but other than that I expect income to average about $24,000/month through November, and then hit about $31K in December.

The only X-factor that could move the dial is Mrs. GYFG, since a large part of her compensation is commission based.

I will get into this more below, but we could potentially lose about $1,350/month, because we are in the process of listing our investment condo for sale, but it won’t likely be on the market until the middle of September.

Here is a look at the trend for the last 13 months:

You can see in the chart below that income for July is only up marginally vs. July of last year (only up about $700).

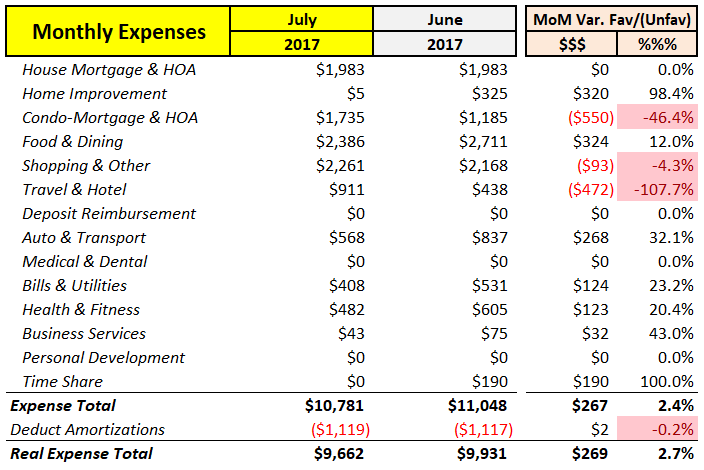

Now, where did all that money go?

I have come to the realization that there are always going to be unplanned expenses. Our goal is to save 50% of our income and live off and enjoy the difference guilt free. With that type of rule governing our financial life, it’s a free pass to inflate our lifestyle, but only proportional to our income. You can see prior financial reports here. We do however try to line up expenses with expected income as much as possible.

We had a spike in the “Condo-Mortgage & HOA” expense line due to some plumbing work we are having done as we prepare our condo for sale. And the spike MoM in “Travel & Hotel” is really a timing issue, as I will get reimbursed for the rest of my expenses next month.

Here is the trend for the last 13 months:

Note: I have now changed the chart to reflect the add-back of loan amortizations to reflect what I call “real spending” above. This is done because amortizations are really just a balance sheet transfer from cash to pay down liabilities, it has no impact on net worth.

It now looks like my expenses are giving me the middle finger.

CALL OUT: It is crazy how slippery money can be. Because of this I totally recommend you automate as much of your finances as possible, especially the saving and investing piece. We set our financial goals at the beginning of the year and then automate the process of reaching them.

Examples:

Our mortgage payment is automatically set up to pay $1,600 in additional principal.This is on hold. Trying to work down net worth concentration to something closer to 20%.- My 401K contribution is automatically deducted at a rate that will ensure I max out by year end ($18,000)

- My HSA contribution is automatically deducted at a rate that will ensure I max out by year end ($6,750)

- We are now sending $500/month to our Rich Uncles investment account. Looking to increase the account balance to $11,000 by year end (currently at $5,500)

We are now sending $2,000/month to ourPeerStreetinvestment account.We now have $77,000 invested here and are on hold from new monthly investments. This is generating about $6,000 of income annually.- In July I added a new automatic investment to an after-tax brokerage account for $1,000/month.

All of these things take priority over any spending that we do in a given month. We monitor expenses but don’t really manage them. Instead, we manage savings and investments and let the expenses work themselves out.

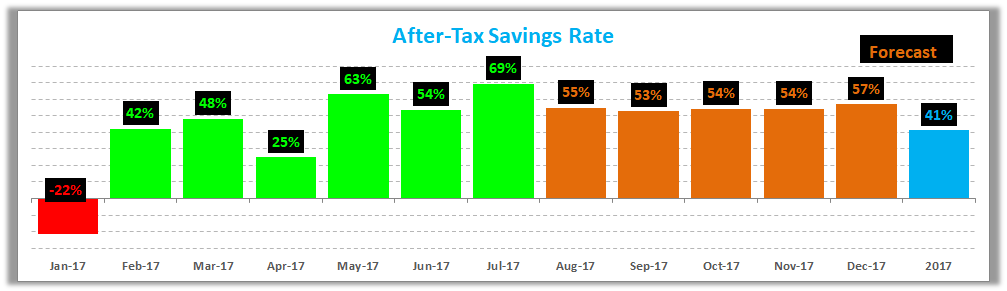

Savings Rate

Below is how we did vs. our goal of saving 50% of our after tax income.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Net Worth and Mortgage Pay Down Update

My ultimate goal is to build up a Net Worth of $10M returning 6% a year or $50,000/month in gross income. Don’t freak out, this is only about $5.5M in today’s dollars when you take into account a 3% inflation rate. If you want to see how I plan to get there you can read all about it here.

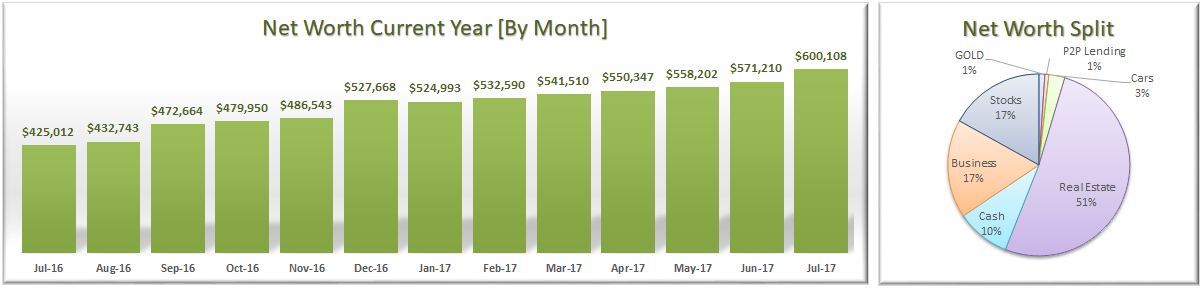

July Net Worth $600,108 (up +13.7% for 2017 YTD)

- Previous month: $571,210

- Difference: +$28,898

Net Worth is up 1,315% since 2012!

Net Worth Break Down:

The P2P category is slowing getting eliminated as I prefer the risk profile and returns of investing in real estate backed debt through PeerStreet. I have been and will continue to withdraw cash as it becomes available. As we pull out of our P2P loans on Prosper and Lending Club, I am considering to use those funds to double our GOLD position.

Note: I think people tend to glaze over the fact that the savings rate plays a much bigger role in increasing your net worth than the rate of return on your investments (in the early days of your journey). In the short term, your savings rate has a bigger impact on net worth. The goal is to eventually build a big enough asset base that the gains from compounding will eventually outpace the gains from savings. Actually, check out the post I recently wrote: Savings Rate – The Most Important Variable to Wealth Building [and the math to prove it]

Progress On Our Mortgage Payoff Goal

You can read about our strategy to pay off our mortgage in 7 years (and 3 months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $297,307. It is nice to see it go under $300K.

Our primary residence is currently sitting at 23.0% of our net worth, still higher than we would like, which is why we have not made any additional mortgage payments this year. We would like to see this closer to 20% in the short term and far less in the longer term (like less than 10% over the next 10 years). That is not to say that we don’t still plan to stick to our 7-year goal to have it paid off, we just feel more comfortable stacking up the cash in our bank account.

Based on the original 7-year plan, our mortgage balance at July-2017 should be $285,422, but is currently at $296,698. Doing the easy math, this says we are currently $11,276 behind goal. Based on the pending sale of our Condo, I think we will take a portion of the proceeds to catch us up to the goal for 2017, which would mean paying down the mortgage by $23,276 by December 31, 2017.

The End

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for the man before you have the option to retire. I personally think that 15-20 years is really all you need, and for the folks that are more aggressive (i.e. extremely frugal, not us) or very high earners you can probably reach financial independence in 10 years or less (maybe us, it’s yet to be seen but income is our focus vs. expenses).

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

One last thing before we go. If you are new or even if you’re not new and you have been wanting a more guided tour of the blog, I finally launched a “Start Here” page. I highly recommend you check it out.

Cheers!

– Gen Y Finance Guy

16 Responses

Hi Dom,

Great work this month. A few questions for you:

1. How do you enjoy Personal Capital with regards to real estate?

2. I see you have “after-tax” savings being shown, curious to get your thoughts on pre and post tax savings rate.

3. Maybe I’ve missed in the post or an earlier post, but What’s going on with the condo that you are putting it up for sale?

Thanks again for all the great detail, helps me look at my own NW with different glasses on.

Hey Church,

I just happen to have a few answers for you:

1. I assume you are talking about physical real estate and not PeerStreet investments. At first, when I first started using PC back in 2015, I loved the fact that it was linked up to Zillow to price the asset in real time, but over time I realized that there was wild swings and price did not always reflect comps. So, sometime in 2016, I unchecked the link to Zillow option and now only update the value of our real estate once every 6-12 months based on comps of similar properties in the neighborhood. Not really a PC problem, more a problem that it’s really hard to price an illiquid asset on a real time basis.

2. On savings rates, I publish the after-tax one, but I do track both. I choose to publish the after-tax rate because we all have different tax situations, so I thought as a metric that is relatable it would be the best to share. However, I like to track the pre-tax rate as well, especially to see how tax-efficient or really how tax-inefficient my earnings are. We are working on the tax efficiency longer term.

3. The builders of the condo complex that we bought had a lawsuit that was brought on by the association due to many building defects. Defects that are starting to cost a lot of money to fix, and will cost a lot more in the near future. We had planned to hold onto the property if the builder was held accountable to come in and fix them, but that was not the case, so we have decided to sell the condo. My wife sat on the board, and if the builder was not held accountable, there were going to have to be lots of special assessments to the owners to fix the roof, plumbing, and HVAC issues (among other things).

Cheers,

Dom

Yes, I was referring to your physical real estate on Personal Capital and not PeerStreet. I signed up for PC awhile back and my IRA manager doesn’t link to PC nor does my life insurance which make up two very large portions of my NW.

Agreed on the post-tax savings rate. I always figured the pre-tax savings rate was lower and conservatively decided to show that. I go back and forth on it all the time.

Sorry to hear about your condo complex. I had a similar issues in 2015 on a condo I owned in Philly, PA. Decided it was time to move on and get out of the physical real estate market to focus on other things.

Thanks for the insight. And, again, great job this past month.

SIX HUNDIE!!!

That’s big! Enjoy the feeling, you and Mrs. GYFG have done the work and sacrifice on the other end. Nicely done, Good Sir!

Hey JayCeezy!

We got there, but just barely 🙂

It’s crazy to think that when I first started these reports 31 months ago, we were only at $181,361. The fact that we were able to 3.3X our net worth in less than 3 years is still mind boggling to me.

Thanks for the support as always.

Dom

Nice job on 600k! Looks like we are clocking in right around $630k. I am hoping/aiming for $750k by year end, but there’s a lot of work to be done, and will need a gentle market. That being said, a market correction will only speed up my movement to the ultimate goal of $8-10M. It’s a win-win situation!

Cheers,

Sean

Hey Sean – Dude, we would be at parity if I included the $33K I spent to put my brother in rehab. Technically it is a loan, but I am not sure if I will get paid back or not, so that is why I am not carrying it in my net worth. I would rather it just flow in over time if/when it does get paid back.

$750K is a good goal to finish the year with. That’s my goal by end of January 2018 🙂

I would not mind a market correction myself.

Going to send you an email about a question I have for you.

Cheers,

Dom

Yes that’s true, we would be at parity! It’s all irrelevant though because your and your wife are a stampede I’ve seen in my rearview mirror for quite some time. I knew the point of parity and raging past me was already a foregone conclusion, I just did my best to drag it out as long as possible 😀

Hey amigo

Just found the site and loving it 🙂

What’s the “business” slice of the net worth pie? Listed at 17%?

I don’t see it listed/explained elsewhere… unless I missed something.

Thanks!

Caleb

Hey Caleb,

Welcome to the GYFG community. I guess I only explained the business slice in the first report that had it show up earlier this year.

This “business” slice represents the ownership that I have in the private company that I work for.

Cheers,

Dom

Thanks Dom…

So is that the same as the “company stock” line item in the “Month Over Month Financial Summary”?

Yes, but netted against the “Company Stock Loan” in the liabilities section.

Essentially I have $300K worth of stock, with an outstanding loan of $195K with the company at essentially 0% interest, for a net worth of $105K (this is whats represented in the pie chart).

Cheers

Oh I see. Cool man, thanks for the explanation!

I just discovered your site via PoF, and I have a PC question for you. I’ve just started using personal capital last month. Is exporting out to a spreadsheet an option on there I am missing or are you doing that by hand?

Hey Figerguyr1,

Welcome to the GYFG community! Yes, you can export all your transactions to a CSV file that will open in Excel nicely. Here are the steps:

(1) Navigate to “Overview” drop-down menu and then “Transactions”

(2) Once on the transaction page, in the upper right corner, you can choose your date range of data.

(3) Then next to the “search transactions” you will find a little icon that says “CSV”, by clicking this it will download all the transactions to a spreadsheet based on your selected date range.

Hope that helps.

Cheers

Hi Gen Y Finance Guy, I recently created a new passive income website. http://www.passiveincomewiz.com

I have admired your site and content and would appreciate any feedback. Your site inspired me to create my own. Thanks, TJ Mitch

thepassiveincomewiz@gmail.com