Last month, after 33 consecutive months of the same format of my Detailed Financial Reports, I decided to shake things up, starting with report #34 (October 2017 Financial Report). However, the introduction will still repeat from month to month, because 50% of my readers are new every month, and I want to offer them all the content in my initial intro. That said, I will still plan to modify the intro periodically when appropriate. If you’re a regular reader and only want to read the new content then feel free to just skip the intro (no harm, no foul).

Intro

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

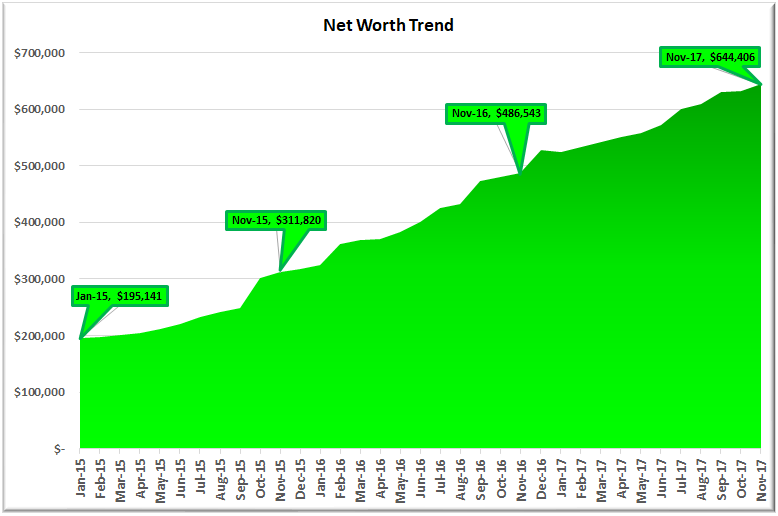

For those of you new around this corner of the internet, these monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of my financial details public, but it’s also a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141, and our gross income was on pace to hit $178,000 that year.

Fast forward three years: our net worth is on pace to finish the year at ~$655,000 with a gross income of $370,000.

- That’s a 3.4X increase in net worth due to a compound annual growth rate of 50% for the past three years.

- At the same time, income has increased 2.1X, which translates to a compound annual growth rate of 28%.

I honestly don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will need to share our results with my readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle, to only then have the means to check off bucket-list items, when my body is no longer physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for The Man before you have the option to retire. I think that 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two vital components of a good recipe for the 10 year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not that many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page.

Net Worth

Yay! We realized an increase to net worth of $12,239 or 1.9%. Net worth finished the month of November at $644,202.

November Net Worth $644,202 (up +22.1% for 2017 YTD)

- Previous month: $632,168

- Difference: +$12,239

There were many contributing factors:

(1) The most obvious is that we spent less then we earned (the most important fundamental to building wealth). This includes automated investments that go to my 401K, HSA, Rich Uncles, and TD Ameritrade account.

(2) The stock market continued to make new highs (The DJIA hit 24,328 and the S&P 500 hit 2,658). Last month our AT&T stock position had fallen significantly, leaving us with a $3,000 paper loss. However, after falling from the high in October of $39.80, then hitting a low in November of $32.55, it has recovered over 50% of its loss. This alone reduced our paper loss by about 60% since our original purchase price was approximately $39/share. We are actually now at breakeven because I was able to buy back calls I sold against the position (via a covered call) for about 30% of what I had sold them for near the November lows. So I cashed in on the profit from the options and got 1:1 recovery in the stock price.

(3) I received $3,200 in expense reimbursements for work-related travel, lodging, and food.

(4) I received my Q3 401K match.

(5) We cashed out $950 from our latest credit card hack with the Citi Prestige card (this was offset by a $450 annual fee paid back in September, but we also received a $250 statement credit for travel-related expenses, so it really was offset by a $200 expense).

(6) And finally, we counted all the interest and dividends received from our various investments with PeerStreet, Rich Uncles, TD Ameritrade, 401K, and CD’s.

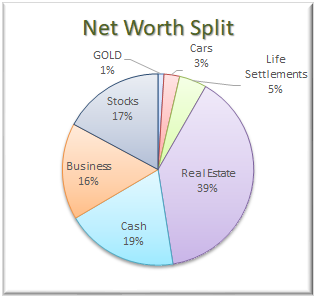

Net Worth Break Down:

– Last month I combined the P2P category into cash since it will now all be converted to cash over the next 12 months as I wind down my investment in this asset class.

{kind=link}

– This month I added a new slice to represent our newest investment in Life Settlements.

– Cash declined from 27% in October to 19% in November (we are still holding a large stash of $122,680). This is due to two major cash deployments: (1) We invested $30,000 into Life Settlements mentioned above, and (2) we paid down an additional $24,000 in principal on our home mortgage to stay on track to hit our goal of being mortgage-free by 2021.

– Due to the above, the Real Estate category increased from 36% to 39%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($10,000), and our hard money loans through the PeerStreet ($80,000) platform.

– As a clarification for newer readers, the Business category represents the ownership I have in the private company that I work for. Earlier this year I wrote my largest check ever ($105,000) to take advantage of what I think will end up being a tremendous financial opportunity.

– The Stocks category represents the cumulative value of our retirement accounts that are invested in stocks. However, it is not all of our retirement money as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $73,000).

– We have not added to our Gold position in some time. I’m still contemplating whether gold should have a place in our overall portfolio mix or not. I probably won’t liquidate what we have, but it is unlikely that we will be adding to this position in future.

– That leaves the Cars category. I include our cars because the goal is to keep the value of our cars as a percentage of the overall net worth pie as small as possible. By including them, it keeps me conscious of the opportunity cost of sinking too much capital into the machines that are only meant to get us from point A to point B. The combined value for our cars is currently being held at $17,000 and will get revalued at the end of the year. I suspect the value will drop by at least $3,000.

Gross Income

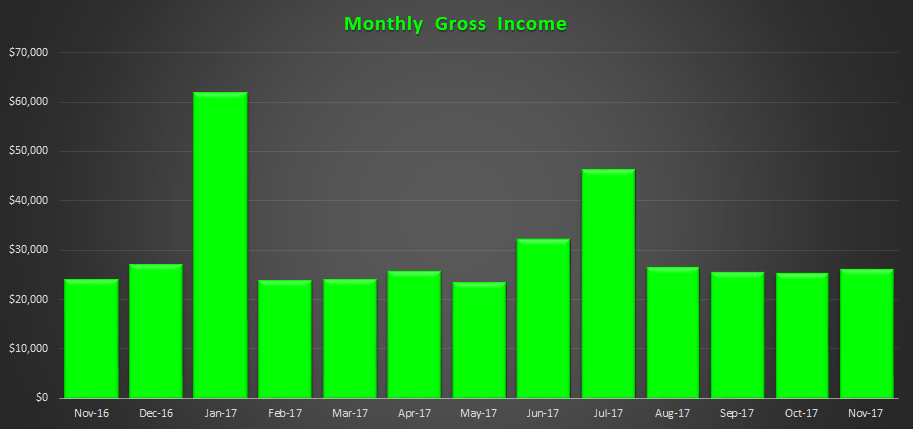

As you can see from the chart below, our income has been somewhat flat the past four months (averaging about $26,000/month). In December we will see a nice spike due to this month’s three-period pay cycle in the bi-weekly pay schedule I am on (we experience two months a year with three pay periods). I expect our December income to hit about $31,000.

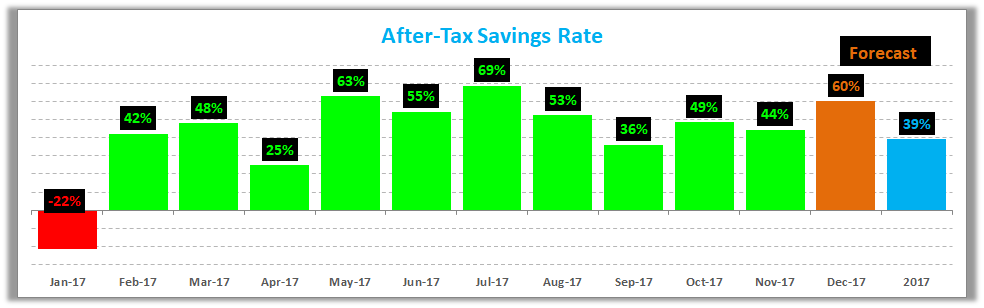

Savings Rate

Below is how we did vs. our goal of saving 50% of our after-tax income.

We are currently on track to miss our goal of saving 50% due primarily to the decision I made to carry the $33,000 we paid to put my brother through rehab as an expense. However, if you back that out, our “adjusted” savings rate is actually on track to hit 52%. Unfortunately, the “it doesn’t count bucket” doesn’t exist. This is technically a loan, but since we are not sure if/when we will be paid back, we are not carrying it in our net worth figure as an asset. That said, I have decided that it probably doesn’t belong in our expenses either (but I am not going to go back and change it. It will just fall off when we start 2018 fresh). If we do eventually get paid back, then this will provide a surprise boost to net worth. Regardless, this is an investment in the life of someone who is well worth it, and my emotional and spiritual net worth has increased for having done it.

I promise you will stop hearing me mention this once 2017 is behind us.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

You can read about our strategy to pay off our mortgage in seven years (and three months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $294,864.

Our primary residence is currently sitting at 25.6% of our net worth. We would like to see this closer to 20% in the short term and far less in the long term (like less than 10% over the next ten years). Nonetheless, from revenue captured at the sale of the condo, we still decided to divert about $24,000 to pay down additional principal in order to stay on track for our seven year goal of paying off the mortgage (we had previously already paid down an extra $4,800, so this got us to the target of $28,400 for year three).

Woot, woot! We paid down an additional 7% of our mortgage balance, which puts our goal progress at 23.9% paid vs. 16.9% in October.

The original philosophy of this plan was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. I decided that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. We have used the cumulative increases thus far to execute this goal flawlessly. Since setting this goal in January of 2015, we have since paid down an additional $57,600 (Year 1 = $9,600, Year 2 = $19,200, Year 3 = $28,800).

At the end of 2018, we are planning to pay down an additional $38,400 according to the plan. Until then we will use most of 2018 to dilute our net worth concentration in our home equity. Soon I will also be writing about how we plan to leverage this idle capital sitting to our advantage.

Closing Thoughts

We don’t have any other significant money moves scheduled for the remainder of 2017. I tend to only talk about the money moves we are making to strengthen our financial future but I thought it would be nice to share some things that we are currently spending on to enjoy our enrich our current day to day lives:

(1) We recently put down a deposit to rent a condo up in Tahoe, where we plan to spend a week. We have invited my aunt and uncle to spend a few days with us, which we are very much looking forward to. We will be bringing our dogs, and we are excited to see them frolic in the snow. My old boss and mentor is going to be up there during part of our trip, so we will get to spend some time with him. And of course, we will be hitting the slopes a few of the days.

(2) I hired a personal trainer at $420/month to kick my butt back in shape. I have completely failed at my fitness goals the past two years (insert excuse here) because I frankly did not make it a priority. This is my way of forcing compliance. It’s been three weeks, and I love it. I will share more when I publish my 2018 goals.

(3) Being the busy professionals that Mrs. GYFG and I are, we have found ourselves with less and less time to prepare healthy meals during the week. So, we end up eating out a lot. Not always fast food, but still (speaking for myself), often overeating. That said, we just signed up for a meal delivery service. We are starting off dipping our toes in the water by only ordering enough food for lunch Monday through Friday. Everything is prepared with quality ingredients (grass-fed beef, pasture-raised poultry, wild-caught fish, seasonal organic veggies). All meals are cooked, portioned, and delivered on Sundays and Wednesdays to ensure freshness. If all goes well, we will likely add in breakfast, and potentially a few dinners. We will leave dinners open on the weekends and a few nights a week.

These are just a few ways that we are enjoying the money that we work so hard for. I am currently putting the final touches on my 2018 goals, which I will plan to share with the GYFG community in the next couple of weeks.

I am looking forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

4 Responses

I actually got in right around $33/share for AT&T stock, it was the perfect oversold situation from a technical perspective on this blue-chip stock. Short turnaround and quick profit. I sold have of my position but think it will still go higher.

Thanks for sharing your report, I enjoyed it! Keep up with the good work!

Awesome, Mao!

Wow your net worth really has increased by a lot from 2015 to present! Way to go, and keep up the good work!