As I do from time to time, I like to pass along guest posts I’ve done for others. Below is a guest post that I wrote for “Max Your Freedom” about a year ago. However, as I type, it appears that the blog has been sold and the site has changed drastically (for the worse in my opinion). You can read about Max in the interview he did for my site before he stopped blogging himself here. I’m bummed that Max is no longer blogging as I enjoyed reading his content and his charting skills were superb.

It’s always interesting to re-read things from the past. I particularly enjoy reflecting back and being reminded of the progress that can be made in as little as a year. As you read through the post below, I will sprinkle it with update comments to compare where I am today vs. a year ago.

Enjoy!

Hey, I’m Dom – the man behind the cartoon (THE Gen Y Finance Guy).

Hey, I’m Dom – the man behind the cartoon (THE Gen Y Finance Guy).

I recently started a new interview series on my blog called Chasing FIRE and Max was kind enough to accept my invitation to participate. Max is someone I look up to and is someone who inspires and motivates me. I’m a big believer in Jim Rohn’s philosophy that says, “You are the average of the five people you spend the most time with.” If you want to level up, then you need to level up the people you spend time with, both physically and digitally.

Although I’ve never actually met Max, the internet has enabled me to get to know him and learn from his experience. I found him among the thousands of bloggers in the personal finance space, because I gravitate towards those written by high earners with net worths in excess of my own. I believe that reading and learning from those that already are where I want to be acts as a gravitational force that pulls me toward their higher level much faster than I could have traveled towards it on my own.

I’m grateful to be able to include Max in my circle of five!

Today Max is turning the tables and has asked me to answer my own interview questions, which he has been so generous to share on his blog with you fine readers.

Note: For those not aware of what FIRE stands for, it’s an acronym for Financial Independence Retire Early. At least that’s the traditional definition…but you will learn my alternative definition to that below.

OVERVIEW – Who are you?

In the digital realm of fellow bloggers, I like to think of myself as the Chief Freedom Officer of my little corner of the internet. In the real world, I’m a 30-something C-Suite executive (I’m 32 but “30-something” just sounds better). I’m married to the wonderful Mrs. GYFG. Until recently, we had been enjoying the benefits of the DINK lifestyle (Dual Income No Kids), which has had a massively positive impact on our careers and ability to build wealth rapidly. We recently welcomed our son into our lives in October of 2018 and I can’t even begin to describe how infatuated and lucky we are. Now we need a new acronym!

We live in the always-sunny Southern California, in Temecula, a city I describe to others as the “Napa of Southern California.”

I started life at the bottom, in extreme poverty, which in the US still isn’t that bad (the poor of the US have won the lottery compared to the poor in a lot of other places around the world). I grew up on welfare to drug-addicted parents but I haven’t let that get in my way and I don’t use it as a crutch or excuse. I believe that you can choose to be the victim or you can choose to be the victor in all circumstances. I choose to be the victor and used my starting point in life as fuel in my quest for FIRE (see what I just did there?). As you are about to discover, I live the truth of “It doesn’t matter where you start in life. What matters is how you play the hand you were dealt.”

We live in unprecedented times with more opportunity for success (and riches) than at any other time in history. To get your piece of the pie, you only have to decide if you are willing to do the work. If I can start where I did, and end up in the C-suite by age 30, you can set your own eyes on your own prize and achieve it. There is a quote by Les Brown that I absolutely believe in that says “Most people fail in life not because they aim too high and miss, but because they aim too low and hit.” I hope my story will allow you to aim higher in your own life, and to stop listening to any self-limiting beliefs you may have.

I knew from an early age that I wanted more than what I had been exposed to. More knowledge. More money. More opportunity. I lived vicariously through those I observed outside my own circle. I developed a knack for hustling early on. I mowed lawns, washed cars, accepted any paying gig I could find. In high school, I sold candy out of a shoebox, earning $60 to $80 a day. This was in addition to holding down a job as soon as I could get one. I intuitively knew that money provided optionality: more money = more options.

I didn’t know about the concept of FIRE back then; all I knew was that I wanted to be rich. When I first discovered the concept of FIRE I was really only interested in the FI part of the acronym. That was until I came up with an alternative meaning to the FIRE acronym – Financial Independence Recreational Employment. Some may want to retire early, while others just want to be in a position where work is optional, and still others want to pursue their calling regardless of the monetary compensation. I have no plans to ever stop working as long as I’m physically and mentally able, so once I reach my FI number, my employment becomes recreational.

There is another quote that I regularly revisit which pairs well with the Les Brown quote I shared above:

FINANCIAL – It’s all about the Benjamins!

It’s time for a little financial voyeurism. Don’t lie – you know that’s why you read personal finance blogs. Don’t feel guilty about it, because it’s a great way to level up your own financial game. Talking about money in the real world is so taboo but talking about it online is totally acceptable. Like Max, I’m a big believer in transparency so I’m not going to hold back on sharing real numbers. I believe that transparency provides context.

Before we dive in let me make it very clear that I’m not in this financial journey alone. Everything I share below is a result of the combined efforts by both my wife and me. Some refer to us as a power couple, but she is my WHY and a lot of my HOW. My driving force. My biggest cheerleader. I’m a better and more successful man because I have her in my life.

I think it’s appropriate to start with the earning side of the equation. It’s true that it takes money to make money. Please remember that income is not wealth; it is only potential wealth. No matter how much you earn there is one universal truth to building wealth: spend less than you earn and invest the difference wisely. With that said, I’ll provide a quick overview of our household’s earning history and then dive into how we have saved and invested that income to build wealth (net worth).

Since graduating college in 2008 I have worked for four companies over the last ten years:

#1 Public BioPharma Company (Financial Analyst): I had interned at an oil company for a year and a half while still in school but turned down their offer to join them full time when I graduated. Instead, I took a job offer that was in my hometown and closer to my girlfriend at the time (now wife – it worked out!). This job paid $52,000 per year but was short-lived. I only stayed for three months before realizing I had made a mistake by turning down the oil company. I wanted to work in finance and the job I took ended up being 85% accounting. I was outta there!!!

#2 Private Third Generation Family-Owned Oil Company (Financial Analyst): After three months at the job above I reached out to my old boss to see if his offer was still on the table. Fortunately for me, the offer was not only still on the table but the company was even willing to sweeten the pot. It was a win-win as both sides were known entities to one another. Originally, the offer was $58,500; the increased offer I accepted was $63,500. I wore the traditional FP&A hat (financial planning and analysis), but I was fortunate to participate in some mergers and acquisitions. After a few years, I transitioned into trading, where I helped run all the hedging activities for a private $3B oil company, and traded West Coast products (gasoline and diesel fuel) and options (on the NYMEX) for profit. If you count my intern time, I ended up being with that company for five years. I left with an $80,000 salary.

#3 Public Company in Action Sports (Senior Financial Analyst): A recruiter reached out to see if I might be interested in a Senior Financial Analyst role with a really cool company. I eventually left the oil industry and joined this public $2B company in action sports (think Quicksilver, Billabong, Hurley). After doing a small stint in FP&A again, I weaseled my way onto the eCommerce team, where I helped launch a global analytics team to support the fast-growing $100M eCommerce business. I am fascinated with the online world because of how measurable everything is. I joined this company with a starting salary of $80,000 and left eighteen months later with an $88,000 salary.

#4 Private Professional Services Company (Senior Financial Analyst | Director | C-Suite Executive): Presently I’m almost five years into my time working for a consulting company in the construction management space. I started at the company in 2014 as a Senior Financial Analyst earning $97,000 and today I hold a C-Suite title and earn $300,000, plus incentive stock/options.

[GYFG Here: Shortly after this post was published (about two months later – in February of 2019) I decided to start my own company. I dipped my toes into the entrepreneurial waters until I convinced myself to go all in. I gave my 6-month notice in June of 2019 and put the peddle to the metal in growing my new business. We have averaged about $70,000/month in revenue for the past three months and look to be on track to do over $1,000,000 in 2020. I hit an inflection point in July of 2019 where the income from the business started exceeding the income from my C-Suite job. The good news is that I negotiated a deal that allows me to enjoy both for the last six months of the year. Starting in January of 2020 I will continue on in a part-time advisory role for this company (up to 40 hours per month) for a very nice fee.]

We are all well aware of the power compounding can have on our investments but I also want you to know that effort and knowledge compound over time as well. My career is a direct result of the compounding force on the massive effort I have exerted and the increased knowledge I have continually sought out (and applied). I have taken the Jim Rohn quotation above to heart: I earn more because I have worked very hard to become more, adding value beyond my compensation to those who pay me.

Before we dive into our net worth and overall financial goals I can’t miss an opportunity to brag about my wife for a moment and give a brief rundown of her career.

My Wife: Also 32, currently being groomed to take over a family business (in real estate), where she will represent the third generation to run it.

[GYFG Here: We have both since turned 33.]

She started out working for a firm that specialized in reducing property taxes for large real estate holders. She started at $35,000 per year and by the time she left to work for the family business, she was earning about $75,000. She strategically took a pay cut to work for her mom at a base salary of $48,000 per year, but with added monthly bonus potential.

Today, she is earning a base of $72,000 and is on track to earn about $62,000 in bonuses ($134,000 total projected for 2018).

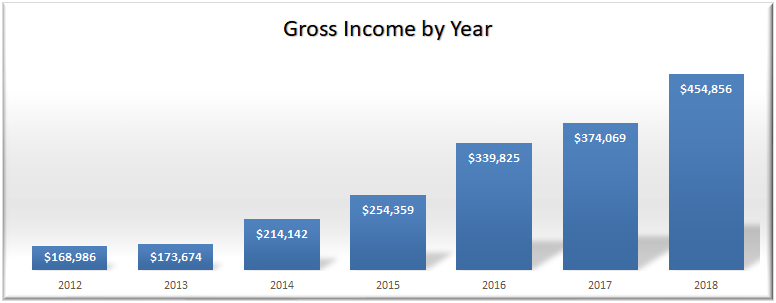

My wife has done extremely well, growing her annual income from $35,000 over ten years to $134,000 in 2018. I haven’t always been ahead of her in compensation and I wouldn’t be surprised if she surpasses me again in the future. Our success is a team effort, with the whole being greater than the sum of the parts. Below is a look at our household’s combined income over the past seven years (includes day job and any side hustles).

[GYFG Here: We actually ended 2018 with a final income of $475,745 and are currently on pace to earn $700,000+ in 2019.]

I believe that a high income is the first step towards financial nirvana. To that end, we have focused most of our energy since graduating college on increasing our income. You can see from the chart above that it has paid off handsomely. We believe in relative frugality and have no interest in living on a shoestring budget. “Extreme frugality” works for some but not us. We would much rather increase our income to a point where our expenses don’t matter. We accomplish this by following the law of 50/50, whereby we save 50% of our after-tax income and are free to spend the remaining 50% guilt-free. It’s a free pass to embrace lifestyle inflation – typically a BIG “no-no” in the PF space.

As I mentioned above, income is only potential wealth: you have to be intentional with your money and make sure you follow the “golden rule” to building wealth, which is to make sure you reserve a piece of the income pie for savings and investments. So, let’s take a look at how we have been able to take our income and convert it to wealth (net worth).

[GYFG Here: As I type, our Net Worth is currently sitting at $1,342,681 and has a high probability shot at hitting something north of $1,500,000 by the end of 2019.]

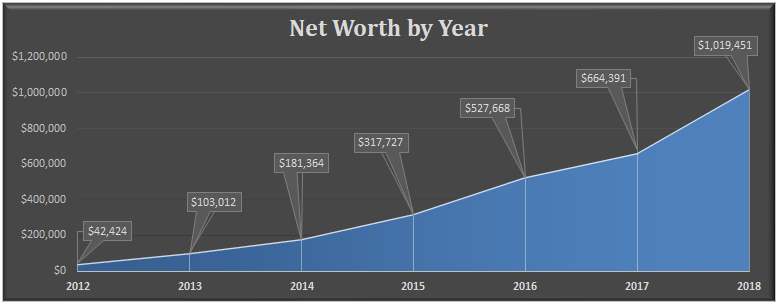

From 2012 to 2018 we have earned a cumulative $1,979,910 in pre-tax income. I don’t have the exact figures but let’s assume about 30% of that went to taxes ($593,973), leaving us with $1,385,937 to fund our lifestyle and wealth-building endeavors. Therefore, we have managed to convert about 74% of our after-tax earnings to net worth (about 50% of pre-tax income). That is a fantastic net worth conversion ratio. I define financial nirvana as the point where your net worth is greater than or equal to your pre-tax lifetime earnings – resulting in a NW conversion ratio of 100%+ (after-tax).

So, what’s our goal?

We have a big hairy audacious goal of achieving a $10M net worth by age 48 or earlier. We set this goal back in January of 2015 and so far we have been ahead of schedule in terms of the targets we set for both income and net worth. Based on the original plan (linked above) our net worth target for 2018 was $744,457 (actual = $1,019,451) and our income target was $238,800 (actual = $454,856). The growth in our income has been the primary driver in exceeding our net worth targets.

Note: When I say “we,” I’m referring to the “royal we,” as my wife thought I was nuts when I first set this goal. She has since converted to become a devout believer.

The other big goal we set for ourselves was to become mortgage-free by 35. It now looks like this will happen in about eight months while we are both still 32. Although this financial move will likely result in a lower net worth than had we invested this money, we prefer the peace of mind of being 100% debt-free. As they say, “a bird in the hand is worth two in the bush.”

[GYFG Here: We ended up paying off the mortgage in May of 2019 while we were both still 32.]

This year (2018) was a big year for us. We made it to the third of the five major milestones on our journey to financial independence. The third milestone is earning membership to the double comma club. I should point out that I differentiate between financial independence and financial freedom, with our FI number being $3,000,000, while our FF number is that $10m mentioned previously.

You may see “financial independence” (FI) and “financial freedom” (FF) used interchangeably across other blogs in the personal finance blogosphere, but to me they are not the same. Don’t get me wrong – reaching FI will provide you with a nice lifestyle, one of your own design, but it’s a life that you are now locked into for the rest of your days. Are you sure you will have the same wants and needs 10-30 years from now? My own wants and needs have changed a lot over the last three decades and I’m willing to bet they will drastically change again over the next three. Maybe I decide to pick up an expensive sport, or have to take care of a family member from time to time, or even indefinitely? How does that fit into my FI plan?

Shout out to Physician On FIRE, who writes:

Financial independence allows you to be self-insured against a financial catastrophe in the case of death or disability, saving you those monthly premiums. Financial Freedom allows you to be self-insured against the cost of unexpected expenses and lifestyle upgrades. [emphasis mine – GYFG] – PoF

Reaching Financial Freedom provides a margin of safety. I would argue that FF makes you that much more insulated from market crashes, like the Great Financial Crisis of 2008/2009, when many asset classes sank 50% or more.

Some of us prefer to set a Big Hairy Audacious “Financial Freedom” Goal, like reaching $10,000,000 in net worth – oh yeah, that’s mine. I chose this number because I want to leave a legacy for my family. I want my family to continue to be able to live well and give well into perpetuity. I want to make my world so big that anyone in it can have anything they desire. Most of all I aim for my version of FF and my $10M goal is where I reach a point where money is no object.

I want the FREEDOM to decide to live a bigger life. Give back more. And secretly, deep down I want F-U Money, which I define as enough to enable me to pivot away from any situation I choose, with my decision completely divorced from any financial need.

I can’t define Financial Freedom for you, as this number is very discretionary and limited by your own imagination, your own ambition, and your very personal vision of your own life.

RECREATION – What do you do for fun?

Wow! That is such a loaded question. Who came up with these???

In all seriousness, we enjoy traveling, and tasting our way through our travels. We are foodies and one of our favorite things is to incorporate food tours and food crawls into our travels. You’ve heard of a pub crawl, right? Well, we took that same concept and applied it to food (and booze). We first learned of food tours when we went to Seattle. If you’ve never done one before, be sure to add that to your list of things to try. It’s great because you get to try food from multiple places but also get a download of the local history and hot spots.

Longer term, we have a dream of living what I have dubbed the three-six-three lifestyle. The idea is that we will live three months at the beach, three months in a foreign country, and six months at a home base. One of the first international destinations we want to travel back to for an extended stay is Italy.

Other activities I enjoy include reading, writing, cooking, water skiing, snowboarding, and many fitness-related activities.

I also really enjoy creating new income streams whether they be from credit card churning, selling tradelines, blogging, starting a business, or through investments.

PARTING ADVICE & WHERE WE CAN FIND YOU

Before I conclude, I want to state strongly: It’s never too late! They say the best time to plant a tree is twenty years ago but the second best time is today. It doesn’t matter where you start; what matters is that you do get started. Your journey is not going to look like mine or Max’s because we each have our own unique paths, and so do you. Don’t compare your beginning to someone else’s middle or end. Instead, learn what you can from others to improve your own situation.

I have a few parting pieces of advice for people of all ages:

(1) Who you marry matters. I encourage you to not to make this decision impulsively, quickly, or dimensionally limited. You want to find someone that you are compatible with emotionally, intellectually, and physically. And please, make sure you are financially compatible and aligned. Financial friction is the #1 reason for divorce.

(2) Remember that FIRE is not about the money. It’s actually about the TIME! The optionality money provides in how you allocate your most precious resource – time – is what makes money valuable. The goal is not accumulation for accumulation’s sake, but rather about being able to live well and give well.

(3) Aim to save 50% of your after-tax income if you want to become financially independent in 10-20 years.

(4) Read The Slight Edge

(5) Never stop learning. Commit to being a student for the rest of your life. Remember the quote I shared above from Jim Rohn: “If you want more, you must become more.”

Thank you for giving me another opportunity to dive deeply into my own journey. I love hearing the stories of others, and I hope that you enjoyed mine.

Onward & Upward,

6 Responses

Dom, your story is truly inspirational. Glad to see your own company is doing great and super charging your net worth!

Thanks, FFC!

Keep it up Dom! I love seeing your progress.

Thanks, Keenan!

GYFG, I come for the content, but stay for the cartoons! Am loving this one with the Benjamin fan, total Baller!:-)

I’m here to entertain you…and I’ll be here all week!!!