It has been 13 months since devising our plan to pay our mortgage off in 7 years or less. I won’t rehash the entire post again, but let me give you a brief synopsis of how and why this goal came to be:

- We purchased our house for $370K in 2014 with an original loan of $355,000.

- As you would expect, one day I was doing some intermediate term planning, and in doing so was trying to estimate how much income we would earn over the next 5-7 years.

- At the time I expected our annual income for 2015 to be around $185,000 based on what I knew at the time. And I assumed that we would be able to increase our income by $10,000/year (which with hindsight was very conservative, we ended 2015 with a total gross income of $254,359)

- Based on the assumptions our 5 and 7 year gross income projections were the following:

- 5 Year: $1,075,000

- 7 Year: $1,575,000

- Based on the assumptions our 5 and 7 year gross income projections were the following:

- At the time I expected our annual income for 2015 to be around $185,000 based on what I knew at the time. And I assumed that we would be able to increase our income by $10,000/year (which with hindsight was very conservative, we ended 2015 with a total gross income of $254,359)

Then all of a sudden it just clicked for me. The remaining balance we owed on our mortgage was 33% and 22% or our 5 year and 7 year income projections, respectively. The next thought that popped into my head was “it would be irresponsible of us not to pay the mortgage off far earlier than the 30 year term.”

I know this goes against conventional wisdom. Many would ask “why pay off cheap debt when you can just invest the difference and make much higher returns?” In theory and to the finance nerd that lives deep inside my being, I typically would agree with this statement.

But the problem arises when theory and reality collide. The first reality is that most people love to say this but rarely do people follow through with investing the difference that they could’ve put towards paying off the mortgage early. Secondly the return from paying your mortgage down early is guaranteed, the stock market or other investments are not.

Thirdly, most of those financial gurus recommend a bond allocation in your portfolio, and a paid off mortgage can represent a bond substitute. And lastly, you have to question the source of the advice to never pay your mortgage off early (what do they have to gain/lose if you do/don’t?).

I am not suggesting that the people don’t have your best interest at heart when they’re steering you against paying off the mortgage. But think about it from their perspective. A financial adviser can’t collect a management fee on the funds you pre-pay to the mortgage. Likewise the banks misses out on interest on all of those pre-payments as well (that is their profit).

How many people do you know that have a free and clear house before they’re 35? Can you imagine the change in lifestyle this could afford you?

Being the rational person that Mrs. GYFG is, she was immediately on board once I presented the facts (i.e the numbers), well and I also did a little colorful painting about the options it would afford us being without a mortgage. Actually, she has really grown really fond of the strategy after watching our balance being aggressively paid down.

The linchpin of the strategy is based on a no austerity foundation. We wanted to accomplish this goal but suffer no loss to our current lifestyle. Yep, we’re determined to have our cake and eat it too.

The early payoff would be entirely financed through increases in our annual income. Remember that $10,000/year increase assumption from above? Each year we would use this to pay down the mortgage, and never get used to seeing that money. However, if increases were/are larger than $10,000/year we get to decide if we want to put it towards the mortgage, investments, or lifestyle inflation (yep, I said a naughty phrase).

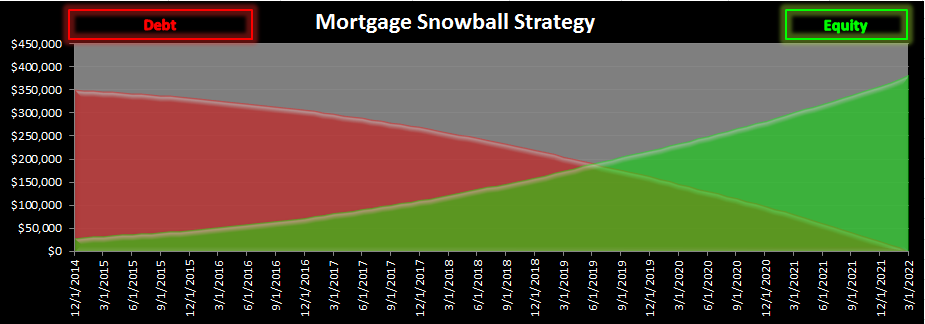

We are currently 13 months into this strategy (@ 3/5/16) and are currently paying an additional $1,600/month in principal (it was $800/month extra in 2015). This means we are currently amortizing our loan at a clip of $2,100/month.

Since putting the original income assumptions together we have experienced rapid growth that has far exceeded our income projections. We are now projecting our 5 year and 7 year income at the following:

5 Year Income = $1,471,794 (37% increase from previous projection)

7 Year Income = $2,200,511 (40% increase from previous projection)

This now puts the original value of our mortgage at 24% and 16% of our total 5 year and 7 year income, respectively. We could not be happier with how well things have worked out and there has definitely been absolutely no austerity.

Is It Time To Speed Things Up?

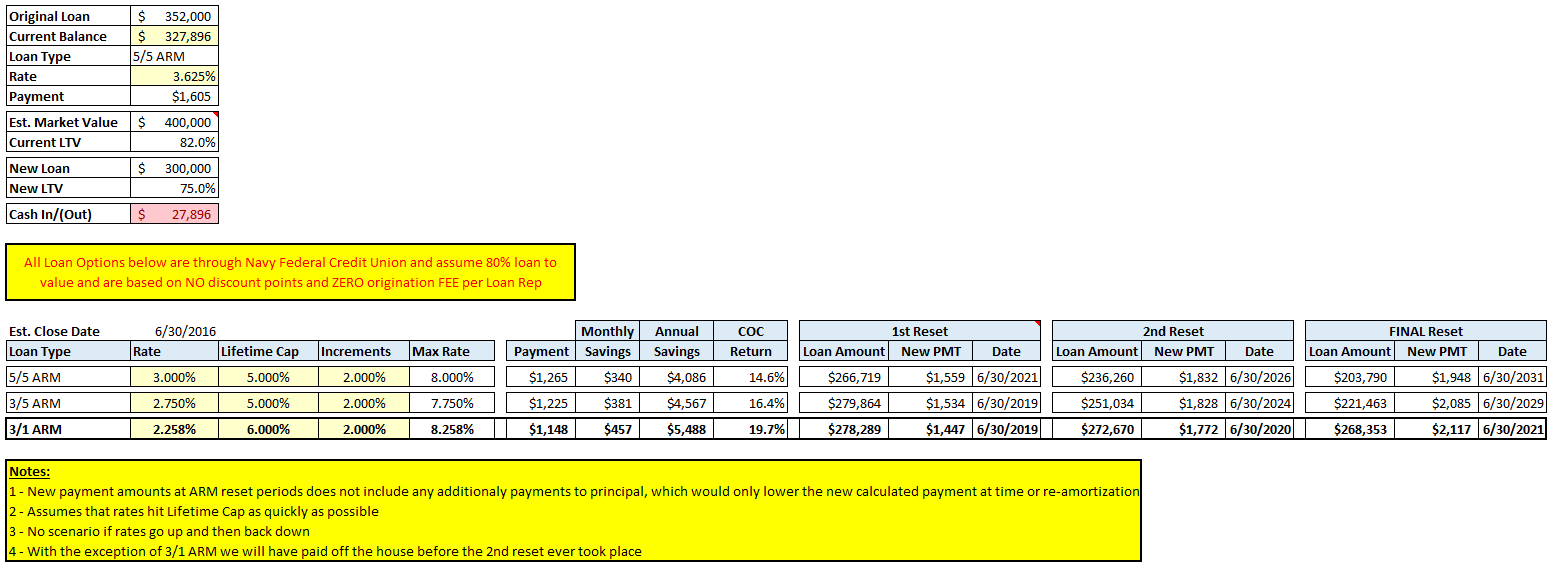

With things taking a quantum leap on the income side of the equation, our stretch goal of 5 years now seems very doable. The question I have been mulling over these past couple of months is what route do we take to speed things up. Do we flat out increase additional mortgage payment and leave the current loan in place (5/5 AMR @ 3.625%). Or do we refinance into a new ARM? Rates have come down since we closed on our current loan back in September of 2014.

Once I get an idea in my head, I become obsessive, and begin the research and necessary number crunching.

We currently have almost 20% equity in the property based on comparable sales in the area. When we first took the loan out we had 5.5% equity, part of the growth is from appreciation, but another part is from the additional payments and regular amortization.

Before we get into the possible loan refinance options that are under consideration (actually our minds are already made up on what we will pursue, it’s just a matter of timing), let’s me first provide a few opinions/beliefs that I have (that could be totally wrong, only time will tell):

- Interest Rates Will Stay Low: The fed may have raised rates by a token 25 basis points in December, but the probability of another increase this year or anytime in the next couple of years is very unlikely. With the rest of the world now experimenting with negative interest rates and the bull market getting long in the tooth, the fed will be hard pressed to not take rates back to zero, and there is a high likelihood of the US going negative. Although, I think the US will be the last county to do so.

- Our Mortgage is a Substitute for a Bond allocation: You can choose to lock your money up in bonds at historically low rates, where a bubble may or may not be preparing to burst, or you can skip the bond allocation and treat your mortgage as your bond allocation. The 30 year treasury yield as I write this is around 2.6%, I would rather pay down my 3.625% mortgage early and earn a full 100 basis points higher.

- No plans to keep a 30 year mortgage to maturity: It is very obvious from this post that we have no intention to keep our 30 year mortgage until maturity. Yes, with an ARM comes the potential risk of interest rates going up. But as you will see in the analysis below, we will have long paid off our mortgage before that comes a reality as long as everything goes as planned. On the flip side, even in the worst case scenario where interest rates rise and our interest rate increases by the lifetime cap as quickly as the loan contract allows, it is still a very small % relative to our income.

- ARM Mortgages should not be used for affordability purposes: We have not and will not use an ARM mortgage in order to afford our home. This is where people get in trouble. Instead we strategically choose to use ARMS for the lowest possible interest rate in order to maximize our ability to amortize the loan rapidly to pay the mortgage off. The key to using an ARM is to by a house that is far less than you can afford.

- It’s best to ignore convention and instead be contrarian: I truly believe that if you follow conventional wisdom and heard mentality the best you can hope to achieve is average results. I am skeptical of any advice that comes out of the mouth of someone that has the potential to make money from you following that advice. I am not saying they don’t “think” they have your best interest at heart, but they also have bills to pay. If you’re willing to live your life like most won’t for a few years, then you will be able to live the rest of your life like most can’t. You don’t get extraordinary results by doing what most people do.

- Theory rarely translates into reality: Everything in theory sounds great until you get kicked in the nuts…yeah, that one wasn’t in the text book was it? In theory you should take on as much cheap debt as possible and invest it at higher rates. That is a no brainer right? Leverage is a double edged sword. It can help you build wealth much more quickly during market expansions, but it also multiplies losses when the market contracts. What happens when reality hits and you can no longer service your debts and you have to file for bankruptcy? That is what you call a sucker punch from the theory camp. I am not against the use of leverage, just the abusive and irresponsible use of it.

- The market return from stocks and real estate will be virtually zero over next 5-7 years: I believe that the financial markets are mean reverting and we have had an incredible run since the 2009 lows in the depth of the financial crisis. From the low in 2009 to the high in 2015, the S&P 500 compounded at about 21% before dividends (back of napkin math). The average bull market lasts 7 years and the longest on record was 10 years. At some point we will go into recession if we are not already in one as I type this. During a recession the market falls 20-40% based on history. I think we are going to witness a period in time where market returns are much closer to 0% then they are to 10% over the next 5-7 years.

- If I am wrong I still win: Even if I am wrong about the market and interest rates I still win. At the end of the day my mortgage will be free an clear. Let’s say the market returns 8% per year instead of 0% or worse. I will have only earned 3.635% (interest rate on my mortgage). But I also still have money in stocks, real estate, P2P lending, etc. In addition to the additional principal we are still investing/saving thousands every month. If the economy remains strong, it is likely the company I work for will do very well, which in turn will mean I do very well since a large part of my compensation is dependent on the bottom line performance of the company.

I could go on, but I will stop there. Let’s move into the different refinance options we have to help us speed up the elimination of our mortgage from 7 years to 5 years. We explored the following 3 ARM options with our credit union: 5/5 ARM, 3/5 ARM, and the 3/1 ARM.

All three of the loan options assume an 80% LTV (loan to value), come with zero discount points, and zero origination fees. The only thing we would be responsible to pay for would be appraisal, title, and escrow. And actually since my wife is in the industry we don’t have to pay anything for escrow. Total fees would be about $850.

In addition to the refinance we’re also looking to bring an additional $27,896 in to pay the mortgage down to $300,000. The reality is that we have way too much cash sitting idly in the bank and are not interested in putting it to work in the financial markets right now.

If you look at the 5/5 ARM option you can see that the new rate we could refinance into is about 63 basis points lower than our current rate and would save us about $340/month or $4,086/year. This would provide a cash on cash return of 14.6% during the first 5 years of the fixed rate period. You can see that in the worst case scenario where interest rates rise and our loan increases by the max 2% per reset period, has a lifetime cap increase of 5% (max interest rate of 8%), which means our payment could go from $1,265 to $1,948. However, this would only effect us if we held the mortgage for longer than 5 years, and even in the worst case scenario $1,948 is less than 10% of our gross monthly income as of today.

In all cases, we would use the monthly savings to throw right back at the principal.

Let’s skip the 3/5 ARM as we won’t be pursuing this option and I don’t want to rehash what I wrote above for the 5/5 ARM. You can look at the table and see the differences.

Chosen Path: 3/1 ARM @ 2.258% and Cash-in of $27,896

Recently I wrote about another refinance we are pursuing with our investment condo. Like that refinance we are looking to bring cash into this deal. The cash on cash returns are even better with this deal at 19.7% for the 3/1 ARM @ 2.258%.

So, am I really missing out on market returns? This is a return worthy of the Oracle of Omaha himself (watch out Warren Buffet, there is a new kid on the block).

By refinancing into the 3/1 ARM loan, bringing in the $27,896 to pay down the mortgage during refinance, applying the savings from the refinance towards the principal, and staying the course with our existing plan to pay off the mortgage. This now puts us on track to murder the mortgage in 5 years.

Our previous target date was January 31, 2022. The new target date is January 31, 2020.

Note: I wrote this post several months ago. And have since finished the refinance at 2.25%. The refinance required us to bring in a bit less cash in order to close (ended up with a new loan amount of $305,000). So, although it has now been 16 months since putting the plan together, we are actually at the 28 month milestone based on the additional cash we brought in to increase our equity position to qualify for the best loan terms and avoid any costs associated with the origination of the loan. Our cash on cash return actually increased to 23% due bringing in $5,000 less and the slight decrease in the final interest rate. We have since put additional payments on hold while we dilute our net worth concentration here.

What would you do? Do you plan to pay off your mortgage early or keep it until maturity? What arguments would you make for against this strategy? Do you think I am completely nuts? Partially nuts?

– Gen Y Finance Guy

Is it time for you to consider a refinance?

21 Responses

Totally paying mine off earlier. My parents were mortgage free I think in their 40s and it’s allowed a lot of financial flexibility. We can only lock in interest rates here for a few years at a time as well so that’s another consideration.

Thanks for sharing NZ Muse!

Where about in the world are you located? You mention you can only lock in rates for a few years, so that leads me to believe you are not in the United States.

Cheers

Great job with the refi! That definitely helps accelerate your plan to pay off the mortgage.

We don’t have a mortgage so it’s hard to say for sure what we’d do. I typically agree with the wisdom of enjoying cheap debt while you can and taking advantage of stock market returns. However, you make some great points for this strategy. Like you, I think we’re more likely to endure a recession in the near future than a period of great returns.

Happy Independence Day!

Thanks Believe Fire!

Hope you enjoyed the 4th of July weekend!

That’s great stuff! Congrats on putting that sideline money to work and getting a terrific return.

I think your comment at the end is worth digging into further: “We have since put additional payments on hold why we dilute our net worth concentration here.” You compare it to a bond, and young people don’t usually want much of their net worth in bonds. So the net worth allocation is very important: how much of your net worth should be in your home? If you live in a natural disaster area (earthquakes, hurricanes, etc) – does that change the allocation? More people need to consider this than just taking standard advice to either pay down their mortgage faster or not.

Thanks Brian!

You call out a very good point (BTW, I also corrected “why” to “while”).

I think the conventional wisdom in a Stock/Bond allocation split is 100 minus your age (if you are 30 then it would mean your portfolio should be composed of 70% stocks and 30% bonds). But I am not big on conventional wisdom, it should be customized for each individuals goals and risk tolerances. It also doesn’t really contemplate any other holdings.

I got the image below from an email newsletter that I am on that shows the average person (the bottom 90%) has almost 60% of their wealth tied up in their homes vs. the top 10% (the wealthy) have between 10% and 30%:

Personally, 25% is my upper limit when managing our goal to pay our mortgage completely off. Over a longer period of time the value of our house should trend much closer to 10% or less (at least that is the goal).

Interesting graphic. The poor have a tough time saving and owning a house is an excellent forced savings plan (if they can afford it).

Your long-term plan sounds like you’ll be squarely in the top 10%

Great post and particularly interesting to me given my position –

I am now 10 days away from the 1 year anniversary of our condo purchase and have a ton of different thoughts flowing through my head.

we purchased our condo for $660,000 with only putting 10% down, final note being $600,000. Typically I wouldn’t have made this purchase without 20% down, but this condo was in our perfect neighborhood and was well under market value. At the time the condo was probably worth $740,000 or so. I was able to talk the seller down because I was currently living in the condo as a renter. My thought process for him was several months in rent would be gone while fixing the place up, would have to drop $30k or so to get it up to par that the buyers in this market would want to see, and not using a realtor. Ultimately we agreed on my first offer I gave him and shook hands over dinner.

Fast forward 355 days and the value of this condo is now worth $920k on Zillow and probably $950k if I were to actually try and sell it. You may have heard about how hot bay area real estate is at the moment, but news articles just don’t do it justice. It’s absolutely insane what’s going on up here.

We now owe about $585,000 which based off Zillow value gives us ~36% equity. For the longest time there was 1 option, do a cash out refinance and pull the $150k that I can deploy in other avenues as I see fit. While this is still my top option, I have recently started thinking about just selling the place and renting for several years. While I think this option would be the best financial outcome, it goes against everything I believe in that no one can time the market, stock or real estate. Ultimately I will still probably do the cash out refinance and pull $150k, but have strongly been considering selling and renting for a bit.

One interesting thought I had, while I would never do it, with this $150k I could literally stash it in a bank and use it to pay my mortgage for the next 37.5 months. Roughly 3 years of not paying a mortgage. While a cool thought, it’s obviously terrible use of money and interest rates and something I’d never do. I will most certainly deploy the bulk of this money – $110k+ in the stock market, but it will remain dry powder until the market offers better values. The other 30-40k will go towards remodeling our place a bit.

Sean – That is just insane how much appreciation you have experienced in such a short time. I have an idea, sell your condo and then move down to my neck of the woods and you could pay cash for a 3,300 sqft house on a quarter acre 🙂

Will be interest to see what you decide to do. You know what they say “no one ever went poor taking a profit.”

However, it might be advantageous (assuming Bay Area Real Estate holds up) to stay one more year and sell and avoid any capital gains taxes on up to $500K in profits since you are married. Now that is what I call having your cake and eating it too!

i didnt know you could get such low rates 2.25%? what do you think is the best rates for a 5 year ARM with 750 plus fico score now days?

Andy – Just to be clear the 2.25% rate is for a 3/1 ARM. I know Sam over at Financial Samurai just refinanced at 2.625% on a 5/1 ARM.

i know those are super low apr, do you usually call different banks? I never done one but planning to. I guess you would never get the same deal with your current bank, as the others are more competitive.

I am a member of Navy Federal Credit Union, so I just go through them. Credit Unions, especially Navy Federal seem to have the most competitive rates.

Congrats on your progress! Are you planning on purchasing more investment properties in the future?

Thanks Pia!

We are planning to try and find and buy a 3rd property before the year is up. We will be getting back the $50,000 we loaned out via a hard money loan this month, and it’s mid-year bonus month, so that should give us lots of cushion to deploy $50,000 to $60,000 to acquire another property.

When we do you will hear all about it on the blog 🙂

Cheers

Very thorough analysis and presentation of your position; thanks for your transparency.

Financial Samurai just posted his thoughts on ARMs today. You two have gotten me thinking about my options.

I am in the process of refinancing to a 3.25% 30 year fixed. I chose not to ARM to keep flexible in case Fed raises rates (if they go negative I will probably lose my mind). But there’s a decent chance I pay it off in 7-10 years, especially if I hit AMT and can’t use it for deduction anyway.

You’re not crazy. I would have done the same thing with our house if we knew we’d be in the area long term. I eventually want to move back to the east coast and plan to pay that mortgage off aggressively if not buy in cash.

Great rate! With your income and your mortgage size, I think paying it off early is a no-brainer. It’ll feel great, and you can conquer a new goal after.

S

If it is that relatively low percentage of your income have at it, it makes perfect sense in your situation. As is typical there is a lot of variation between situations. For my particular situation it doesn’t make much sense… at the moment. While not having a mortgage would be awesome, if I put all my focus on paying it off it would unbalance my asset sheet (since homes are a non-liquid asset that historically underperforms other asset classes, I don’t want to have much more than 25% of my net worth locked up in it). Heck to keep that number right between principle paydown and asset appreciation it takes a lot of cash going into other investment accounts.