Happy New Year!

And just like that, 2017 is now completely behind us. It’s hard to comprehend that the entire year can now only be viewed from the rearview mirror. How did the year pass by so quickly? From an achievement standpoint, it was another GREAT year, but it was one of the more challenging years that I can recall. I’m not one to get anxious or overly stressed, but I admit that 2017 pushed all the right buttons to test my resolve.

In the end, I emerged a stronger and more resilient person. It is through adversity that we come to appreciate our blessings and success in the short time we have on this amazing planet. It’s a reminder that sometimes the sweet comes paired with a healthy helping of bitter to ensure we remain humble and filled with gratitude. I wouldn’t have it any other way and neither should you.

Readers of this blog know that I exude optimism and an unbreakable positive outlook. Sure, I have my dark days, but that is something we all share as humans. I can’t help but stay focused on what’s going well because channeling too much energy to the negative is fruitless and a waste of our precious time (our most valuable resource).

All this to say, I am extremely satisfied with 2017 and can exit the year with no regrets, but with many lessons learned.

If you’re a regular reader and only want to read the new content then feel free to just skip the intro below (no harm, no foul). If you are new or haven’t read many of these reports, I encourage you to take two minutes to read the intro below, which will change periodically.

Intro

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

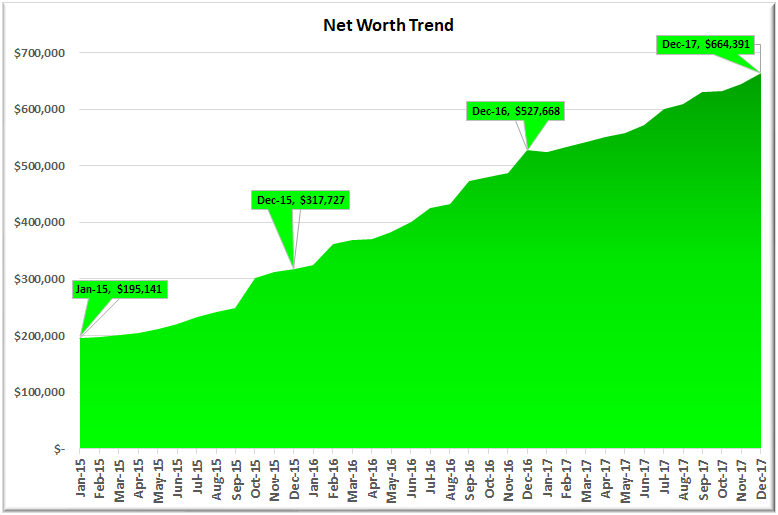

For those of you new around this corner of the internet, these monthly reports are about full transparency. They are just as much for me as they are for you. It’s a hard decision to make all of my financial details public, but it’s also a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141, and our gross income was on pace to hit $178,000 that year.

Fast forward three years: our net worth finished 2017 at $664,391 with a gross income of $372,477.

- That’s a 3.4X increase in net worth due to a compound annual growth rate of 50% for the past three years.

- At the same time, income has increased 2.1X, which translates to a compound annual growth rate of 28%.

I honestly don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will need to share our results with my readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle to only then have the means to check off bucket-list items when my body might no longer be physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. There is a famous Jim Rohn quote that I think everyone should keep in mind:

If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!

You have to be intentional with your finances if you ever want a fighting chance to make it to financial freedom. It doesn’t have to take 40-50 years of slaving away for The Man before you have the option to retire. I think that 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two vital components of a good recipe for the 10 year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not that many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, but I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere.

As always, you can find all my previous reports on the Financial Stats page.

Net Worth

We finished the year strong with an increase to net worth of $19,985.

December Net Worth $664,391 (up +25.9% for 2017)

- Previous month: $644,406

- Difference: +$19,985

A few highlights include:

(1) I increased the value of our home from $435,000 to $450,000. It had been 15 months since I last updated the value, which is based on comparable sales and listings in our neighborhood. I’m still referencing it at less than both Redfin and Zillow estimate the value to be, but they tend to either be too high or too low in their values anyways. This does increase our net worth concentration in our home to 27.2%, so we have some work to do in diluting this in the coming months.

(2) I decreased the value of our two cars from $17,000 to $10,000. It had been 11 months since the last update. I am very pleased that the value of our cars now makes up only 1% of our net worth.

(3) I purchased an additional $17,000 worth of company stock in response to a capital raise for an acquisition we will have closed by the time this post goes to press.

(4) I received my Q4 401K matching contribution of about $1,350.

(5) Since this was a three-pay period month for me, I found myself with excess capital to put to work. So, I sent $4,000 to our after-tax PeerStreet account, and an extra $2,000 to RichUncles (the commercial REIT we invest in monthly). I also increased our monthly contribution to RichUncles from $500/month to $1,000/month.

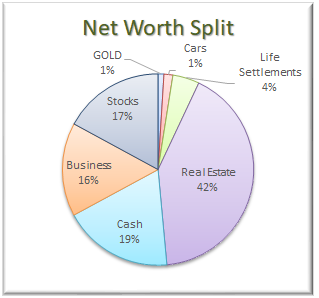

Net Worth Break Down:

– Due to the above, the Real Estate category increased from 39% to 42%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($13,000), and our hard money loans through the PeerStreet ($83,000) platform.

– Due to the above, the Real Estate category increased from 39% to 42%. Keep in mind that this category includes the equity in our primary residence, our investment in the Rich Uncles commercial REIT ($13,000), and our hard money loans through the PeerStreet ($83,000) platform.

– Cash remained the second largest allocation. We are currently holding $123,367 in cold hard cash (what I like to call dry powder).

{kind=link}

– As a clarification for newer readers, the Business category represents the ownership I have in the private company that I work for. Earlier this year I wrote my largest check ever ($105,000) to take advantage of what I think will end up being a tremendous financial opportunity. As I mentioned above, I did acquire an additional $17,000 in stock. Unfortunately, we didn’t experience any increase in valuation in 2017, but the silver lining is that we didn’t lose any value either.

– In November I added a new slice to represent our newest investment in Life Settlements. The plan is to invest an additional $20,000 to $30,000 into additional policies sometime in Q1 of 2018.

– The Stocks category represents the cumulative value of our brokerage accounts (retirement accounts and after-tax account) that are invested in stocks. However, it is not all of our retirement money as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $73,000).

– We have not added to our Gold position in some time. I’m still contemplating whether gold should have a place in our overall portfolio mix or not. I probably won’t liquidate what we have, but it is unlikely that we will be adding to this position in future.

– That leaves the Cars category. I include our cars because the goal is to keep the value of our cars as a percentage of the overall net worth pie as small as possible. By including them, it keeps me conscious of the opportunity cost of sinking too much capital into the machines that are only meant to get us from point A to point B. The combined value for our cars is currently being held at $10,000 based on current Kelly Blue Book.

Now that our cars make up a minuscule portion of our net worth, I am seriously considering removing it from net worth altogether. If I do follow through with this, it will likely happen in Q1 of 2018.

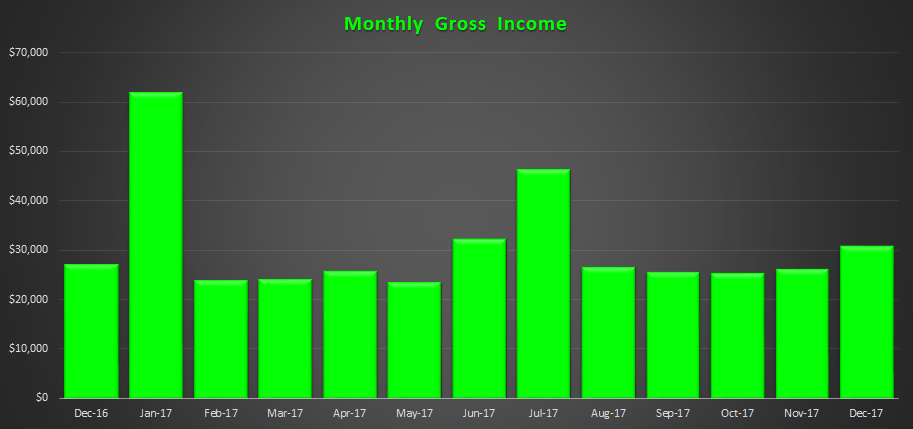

Gross Income

We finished the year with $372,447 in gross income for 2017 (income in December was $30,771). This is up $32,652 or 9.6% vs. 2016. Since I started producing these monthly reports, I have yet to include income from dividends or interest. Although the value does get picked up in the net worth figure, it has so far been excluded from income. Now that it has grown to a decent amount, I will start including it in 2018.

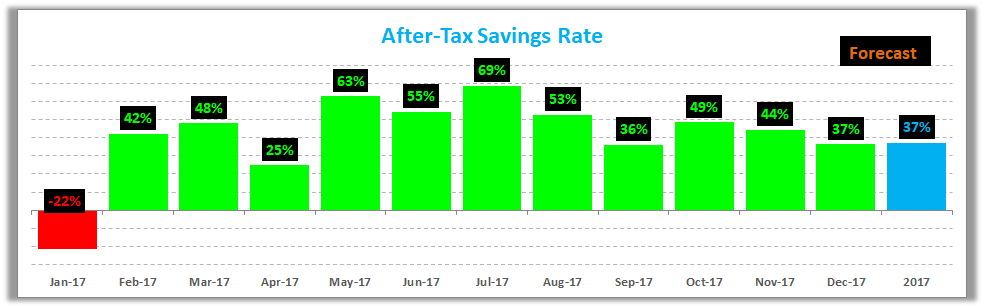

Savings Rate

Below is how we actually did vs. our goal of saving 50% of our after-tax income.

We missed our goal of saving 50% due primarily to the decision I made to carry the $33,000 we paid to put my brother through rehab as an expense. However, if you back that out, our “adjusted” savings rate is 50%. Unfortunately, the “it doesn’t count bucket” doesn’t exist. This is technically a loan, but since we are not sure if/when we will be paid back, we are not carrying it in our net worth figure as an asset. That said, I have decided that it probably doesn’t belong in our expenses either (but I am not going to go back and change it. It will just fall off when we start 2018 fresh). If we do eventually get paid back, then this will provide a surprise boost to net worth. Regardless, this is an investment in the life of someone who is well worth it, and my emotional and spiritual net worth has increased for having done it.

I promise you will stop hearing me mention this once 2017 is behind us.

Speaking of savings rate, have you checked out my post where I mathematically prove the importance of your savings rate as a higher priority than the compound return? If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

You can read about our strategy to pay off our mortgage in seven years (and three months). After several refinances we currently have a 3/1 ARM at 2.25% and we currently owe $294,864.

Our primary residence is currently sitting at 27.2% of our net worth. We would like to see this closer to 20% in the short term and far less in the long term (like less than 10% over the next ten years). The reason I watch this closely is for two reasons:

(1) Concentration Risk – Although I am confident we will accomplish this goal on time, you never know what may happen unexpectedly. What if we both lost our jobs and can’t make our mortgage payment? The bank is going to foreclose on a house with 50% equity a lot faster than one with 5% equity. Until we have the house completely paid off, this will always be a concern and risk to manage.

(2) Diversification – We don’t want our entire net worth tied up in our house. That would be poor risk management.

The original philosophy of this plan was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. I decided that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. We have used the cumulative increases thus far to execute this goal flawlessly. Since setting this goal in January of 2015, we have since paid down an additional $57,600 (Year 1 = $9,600, Year 2 = $19,200, Year 3 = $28,800).

At the end of 2018, we are planning to pay down an additional $38,400 according to the plan. Until then we will use most of 2018 to dilute our net worth concentration in our home equity. Soon I will also be writing about how we plan to leverage this idle capital sitting to our advantage.

RELATED: Our Mortgage Will Be Gone In Four More Years

Closing Thoughts

The books are officially closed for 2017 and now it’s time to begin writing living the narrative for 2018. This blog is all about real life experience!

It’s time to start aggressively working towards those goals I shared two weeks ago. I am excited to announce that I have already crossed off one out of five of the goals:

(5) Negotiate $25,000 to $75,000 pay raise.

– I ended up negotiating a $75,000 increase for 2018 that will be effective 2/1/2018. That’s the good news! The bad news is that this will likely be the last increase I see in compensation (salary + bonus) for a couple of years. I agreed to freeze my total compensation at 2018 levels and that all additional gains will come from stock and option grants (more on this later in the year). Yes, part of my negotiation was to also make stock and/or options a part of my annual compensation (what they call stock-based incentive compensation).

– I have had a good run these past three years, increasing my total compensation by $210,000 from my starting compensation of $90,000.

– I now believe that much more net worth will be created by taking all future gains in compensation in the form of stock and options.

I look forward to chatting with you all in the comments below. How was your month? Also, if you have a blog, I encourage you to write a monthly financial report and come back here and share the link. I would love to be part of your support and accountability.

Cheers!

– Gen Y Finance Guy

15 Responses

Your income is insane. If you stay focused and fairly frugal then your net worth should skyrocket over the next 2-3 years.

Dividends With Children – Thanks for stopping by. I have to pinch myself every once in a while to make sure I am actually awake and not dreaming. The level of income has even exceeded my own expectations, in that I have gotten there much faster than I had originally envisioned. But I guess that shows how powerful intention can be.

Onward & Upward!

Dom, Your net worth is absolutely nuts! Your hard work and dedication is driving this thing through the roof.

Keep doing you! Good Luck in 2018!

-MH

Thanks, MH!

It’s one foot in front of the other…

I think we have seen all the excitement we are going to see on the income side of the equation when it comes to 2018. The focus will be on net worth and investments.

Unbelievable 2017! As mentioned by all, your income is incredible. Even here in the valley working with executives, not many see the income you’re at, at 20 years older, so kudos there! I’m excited for you guys and sounds like you’re looking to make an addition, we probably won’t start that in 2018 but maybe 2019.

2017 was off to a rocky start for me. I lost 80k in income and was leaving my previous partners. All said, I was able to increase my income throughout the year to where I only dropped 20k yoy income. More importantly, we grew our net worth from 480k to 730k during 2017, which far exceeded my expectations. With a little bit of luck and a lot of hard work, I’m going to give everything I’ve got at becoming a millionaire in 2018.

Let me know next time you’re in the SF area, would love to grab lunch again.

Sean

Thanks, Sean!

In the midst of all your changes, it sounds like you did a great job to minimize the income loss. I hope that 2018 will be even more prosperous for you. Great job on the Net Worth front!!! I don’t have us forecasted to hit $730K until March of this year, but then you will probably be further along…you just keep dangling that carrot out there.

The seven-figure club is a stretch goal for us as well in 2018. Fingers crossed and if all the stars align we can both do it.

I will be in SF on 2/1 and 2/2. Let me know if you have time to try and get together (shoot me an email).

Cheers,

Dom

Congrats Dom. That is a very nice salary and I hope it grows some more. If I count my primary home, real estate composes a hefty portion of my net worth too. I need to continue to work on passive income. Happy new year.

Thanks, Millionaire Doc!

Happy New Year!!!

It looks like it will take a pretty significant downturn to stop you from hitting the $1M mark sometime this year.

When I project our current income and savings I think we’ll hit $10M around the same time you’re projected to – sometime in our mid to late 40’s.

I really only give the $1M target a 30% chance in 2018 but would welcome it with no complaints.

Based on the 20-year plan I put together back in 2015, I project us to hit the $10M mark by 48 years old. I hope to hit it earlier due to my conservative forecasting nature 😉

Your income is mind-blowing. You just got a raise that’s almost as much as I make in an entire year. What is your income breakdown now? Base salary, bonus, stocks, options, etc.

I’m hoping to see $150k/year within the next 5-7 years. I have a plan for it, but it’s going to take a lot of work and having no life to finish school and certs while working full time. At least I’m maxing out my 401k, Roth IRA, and HSA for now.

Hi Kevin!

It’s been a while. I still can’t believe the speed at which I have been able to increase my income, I’m still in a bit of shock myself. In a little over two years, I have increased my salary from $90,000 to $250,000. On top of this, I have a fixed $50,000 bonus (based on financial results). It’s hard to value what my stock/options package will be worth, but I have negotiated 5,000/shares per year. These can be taken as options or as stock. If I take them as stock then I have to put up the capital.

I hope you can reach your $150K goal faster than you expect.

Cheers,

Dom

I have read many blog’s income reports but it’s something different and oh! man you gave the consolidated chart of 2Yrs which is really really motivating and inspiring.

Your growth is really unimaginable compared to others. I have a blog and making some money out of it, but after seeing your growth, I have decided to put all my damn efforts to triple my blog income in short future.

Thanks for inspiring me.