2018 is quickly coming to an end! The weather is cooling down as we shift from summer to fall and the holidays are just around the corner. I like to get a head start on planning for the next year by starting that process at the beginning of November and finishing by Thanksgiving. I’m not quite ready to share my goals just yet but there are a few things that I do want to share. My goals will be mixed, but this post will be dedicated exclusively to the GYFG financial arm.

I’m currently in the process of laying the groundwork for our finances in 2019. I’m programming “the machine” so that most things will happen automatically. That’s right – I’m replacing myself with robots – no need for me to push any buttons or pull any levers. I highly recommend that you pre-plan and automate as much of your financial life as you can. It’s the only way for you to ensure that you “pay yourself first” and it builds in a level of discipline that you might not have with a manual process.

Let’s jump in.

Putting the 401Ks On Autopilot

Did you know that the 401K contribution limit is increasing in 2019? If not, now you do! The new limit for 2019 is $19,000, which is up from $18,500 in 2018. Actually, the limits for many pre-tax accounts are increasing in 2019 (<<<The Wall Street Physician gave a nice run down).

The GYFG household has two 401Ks that we have the privilege to contribute to. We plan to max out both of these accounts, where we are allowed to invest $3,166.67/month or a total of $39,000 for the year. Last year we front-loaded our contributions but in 2019 we plan to spread them out evenly over the course of the year.

I have set my contributions at 7% and Mrs. GYFG’s at 20%. Both of these percentages are based on earning less than what we earned in 2018. My contribution rate of 7% assumes that I only earn $271,429 of my total $300,000 compensation package (salary + bonus). Since Mrs. GYFG will still be on maternity leave and is not sure exactly when she will be coming back to work full time (rough estimate is sometime in February), I have assumed she will only earn 80% of her 2018 earnings.

We will re-evaluate these contribution percentages sometime in August and adjust as necessary to ensure we take advantage of the full $39,000 contribution limit between our two 401ks.

Action: I recommend every reader to evaluate their own situation and work towards increasing their contributions to maximize any company match at the very least, but ideally maxing out your contributions to defer taxes on as much income as you can. Let the powerful flywheel of compounding work for you at maximum capacity, and for the maximum time, uninterrupted. If you don’t already have an automated deduction from your paycheck please go set that up ASAP. And for those of you that may not have a 401K available to you (about 45% of the US), I encourage you to go to TD Ameritrade and set up an IRA so you can also use a tax-sheltered vehicle to start saving towards your retirement. Reminder: these contributions come off the top of your taxable income: you save, and you also save!

What About The Health Savings Account (HSA)?

Yes, the HSA contribution limits are also increasing from $6,900 in 2018 to $7,000 in 2019. I can’t make the change yet, but I plan to update my contribution to realize the full $7,000 pre-tax benefit. Unfortunately, 2018 is the last year that my company will be making contributions on my behalf (it’s been about $800/year). I will be setting myself a calendar reminder to increase my monthly contributions to $583/month before the first payroll in January of 2019.

Action: This account has been called “The Ultimate Retirement” account. This is because it is the only pre-tax account that is not subject to federal, state or FICA taxes. The Mad Fientist has one of the best articles explaining why and how this can become “The Ultimate Retirement” account. Go read it here.

Finish Paying Off Mortgage

About three years ago the GYFG household set a goal to pay our mortgage off in seven years (by January of 2022).

The original philosophy of this plan to pay off the mortgage was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. In keeping with the GYFG emphasis on the income side of our financial equation, I decided that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. This has not only proved to be true but in terms of our income, it’s actually proved to be very conservative. To date, we have paid down the mortgage by $214,020 in less than four years (as of October 2018).

Our income has exceeded our wildest projections and is actually 11 years ahead of schedule. We either completely underestimated our ability to increase our earnings or we sandbagged this goal. I’m going to plead the fifth. Either way, we decided back in June that we would accelerate this goal and put the mortgage to bed by July of 2019 – only nine months away from when I’m writing this in early November of 2018.

As of November 5, 2018, we currently owe $140,980. This means we will be plowing $15,664/month towards the mortgage for the next nine months (seven of which land in 2019).

Action: Review your own situation. Does it make sense to work towards paying down your mortgage early? We look at our mortgage as a substitute for a bond allocation. Check out the original plan I laid out to pay off your mortgage in five to seven years.

GYFG 2019 Budget

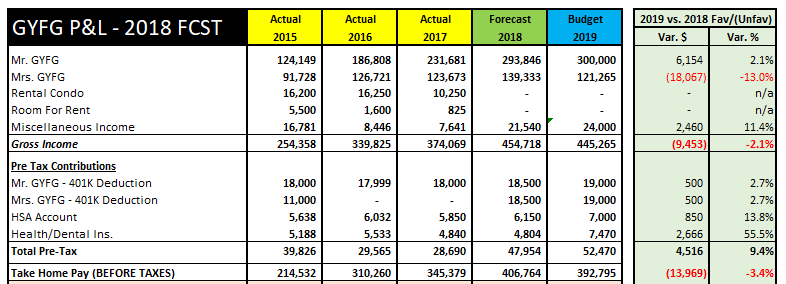

I’m going to break our budget down into two sections for easier readability and to split up my commentary. I’m including the GYFG historical P&L (profit and loss) statement back to 2015 in order to see how things have trended and to provide additional context and color.

Take note that 2015 through 2017 represent our actual final numbers, 2018 is a forecast comprised of ten months of actual plus two months of forecast, and 2019 is our projection based on everything we know today. What I think is interesting is that although we have lost certain income streams we have been able to more than offset those losses from either our day jobs or our side hustles. At their height, the rental income we were bringing in was $21,500 (in 2015) and in 2018 it’s $0.

We do not currently include any income received from interest and dividends from investments. If we did, this year this would represent an additional $12,000 or slightly more. Since all dividends and interest are set to auto-reinvest, we just let those gains flow through to net worth. At some point, they will get added to the P&L as their own income line item.

The miscellaneous income is derived from the following sources: the blog, selling tradelines, and an unexpected tax refund received in 2018 (for the 2017 tax year).

Overall, you can see that we are actually forecasting a drop in gross income in 2019. This is because our rockstar, Mrs. GYFG, is going to be out on maternity leave for part of the year and may initially go back to work part-time. The increase you see in my income has nothing to do with an anticipated raise; rather my increase for 2018 wasn’t effective until sometime in February, so 2019 is the first year I will realize the full impact of the increase. After increasing my income by $185,000 over the last three years, I’m not expecting to receive much if any increase in 2019. That said, I do have an interesting new project in the works, which could be an absolute game changer to the GYFG household if it takes off (will share more as it develops).

The last piece in the screenshot above that I’m sharing is all the money taken out of our pay before taxes are calculated. Mrs. GYFG didn’t have access to a retirement account for a couple of years because her work didn’t offer a qualified plan and our income was too high to qualify for any tax benefit via contributing to an IRA. It sure is nice to have a second 401K bucket to contribute to and shelter more income from the Tax Man.

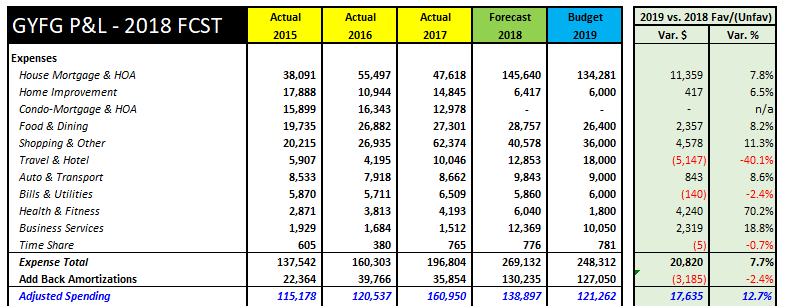

On to expenses…

I used to share our detailed expenses in my monthly financial reports but stopped sometime in 2017. The above needs some explaining between the difference in the “Expense Total” line and the “Adjusted Spending” line. First, the Adjusted Spending line is what I look at as our real spending. The big adjustment I make is that I add back amortizations (money that paid down principal on our mortgage) since this is a balance sheet transfer and is thus net worth neutral – cash declined and our mortgage liability declined by the same amount. This ensures that only the true expense of a mortgage is included (i.e., interest, insurance, and property taxes). The rest goes towards building equity and is forced savings.

Our adjusted spending peaked in 2017 (the year we helped my brother get the help he needed) and looks like it will be returning closer to 2016 levels as we head into 2019. We believe that our spending “sweet spot” longterm is somewhere around $120,000 per year. We feel pretty confident about this as our mortgage will be completely paid off in 2019, eliminating about $6,500 a year in interest, and we are very close to being done with all the home improvement projects on our list. In 2020, this will represent an additional $10,000 we can allocate elsewhere and still be in the $120,000 range.

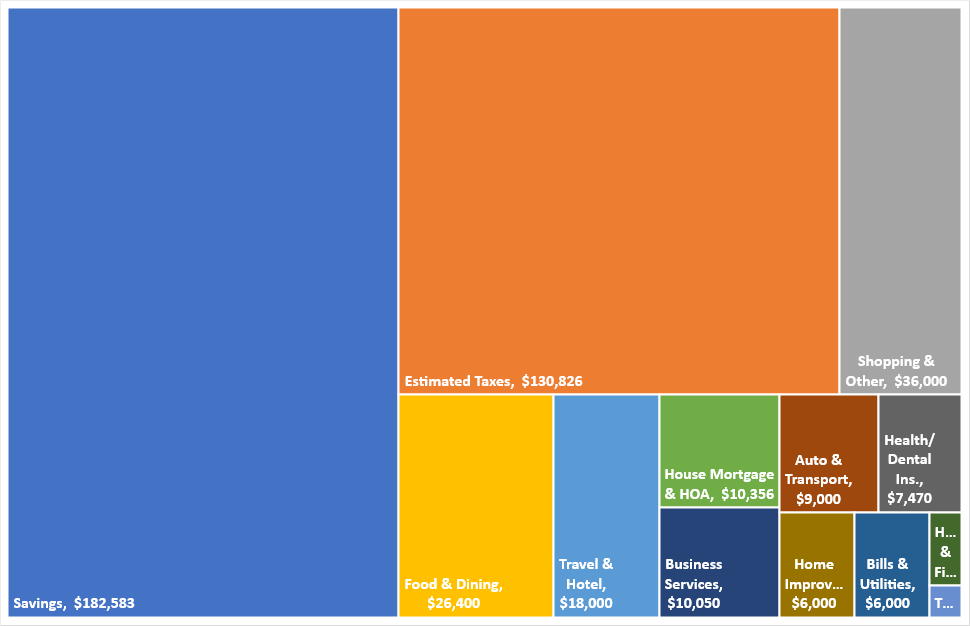

Here is an interesting way to visualize where all of our income from 2019 is projected to go:

A few things to note on the $182,583 in projected savings:

(1) $127,050 of this is committed to paying off the mortgage.

(2) $45,000 of this is committed to maxing out our 401Ks and HSA account.

(3) This leaves only $10,533 to apply toward other investments in 2019. Most of this will likely be sent to Rich Uncles as we work that investment up to a round $100,000.

(4) Without the pretax savings, this would be significantly lower as we would be giving up more to Uncle Sam.

(5) Our taxes are only estimated and could potentially be more, which would obviously eat into this number.

(6) This currently gives us a projected savings rate of 59% for 2019.

When all is said and done, this breaks down to about 40% savings, 30% taxes, and 30% spending (as a percent of gross income). I really like that our savings is greater than both our spending and our estimated taxes. I do, however, wish we had more than the $10,533 of discretionary investment money. I guess I’m going to have to figure out how to increase our income even further 🙂

Action: Put a budget together for your own household. Decide whether the allocation or control based approach is best to fit your unique situation. Don’t have a budget template? Head over to this page to download the GYFG FI Toolkit, which includes a: budget template, financial dashboard, savings rate calculator, and more.

That’s a Wrap!

I feel solid about how 2019 is shaping up. There is a plan in place, most of which is automated, so it’s really a “set it and forget it” approach. There will of course be twists and turns along the way as one can never plan or prepare for every possible outcome, but this will be the blueprint that guides us through 2019. It will take minimal bandwidth to manage the financial arm of our lives, leaving much more time to focus on our new family and other priorities.

Onward & Upward!

Gen Y Finance Guy

9 Responses

Good stuff all around. Thanks for putting this good content out there, it’s always a nice kick in the but to get my 2019 planning in order.

Good luck with the new endeavor! I hope it works out for you!

Thanks, Chris!

can you share how to calculate the mortgage amortization to add back in? I’d like to start doing this as well. Thanks. 2019 will be very different for you now with kid, expect some unpredictability! Cheers

JD – the easiest way to figure out how much of your monthly mortgage payment is going to principal vs. interest is to look at your mortgage statement. For example, take a look at the screenshot from our monthly mortgage statement that gives you a breakdown of what our monthly payment is comprised of:

Notice that our total regular payment is $1,932.80 and that $934.32 is going to the principal (i.e. reducing your outstanding loan amount), this is the piece you would add back since it is only a balance sheet transfer. I hope that helps.

Dom

Hey Gen Y, long time reader here. You state that your wife will go back to work after her mat leave but I do not see any anticipated child care costs in your 2019

expenses. Also, are you sure you’ve properly accounted for baby Gen Y in all other categories? One thing I know for sure is that babies are expensive. Wishing you much success for the upcoming year. Cheers!

Hi Blessed,

Thanks for the comment. It’s always nice to hear from long-time readers who comment for the first time. You have a keen eye and you are correct I did not call out a separate line for childcare costs and Mrs. GYFG is indeed going back to work in February (four days a week). We actually recently interviewed and hired a nanny to start with us full time in February (10 hours a day for four days a week). This is going to cost us $2,400 per month. Mrs. GYFG and I have decided that this will be funded from other categories (particularly the “Shopping & Other,” “Food & Dining,” and “Travel & Hotel” line items).

After six weeks, we have already noted a significant reduction in our spending patterns. We have been and plan to continue cooking at home a lot more. Take the food & dining category, for example, we typically had spent $2,500/month on average prior to baby GYFG, and since have been on pace to only spend about $1,400/month.

The punchline is that we think we are covered with the $121,262 adjusted spending budget. If not, 2019 will show us where we went wrong on our assumptions and we will adjust 2020 accordingly. But so far overall spending has declined significantly.