In my last post, I conducted an analysis of my family’s spending in order to ready it for some drastic reductions in response to the unprecedented times that we find ourselves in today with the COVID-19 pandemic. Besides getting a better understanding of my household’s historical spending, the goal of that exercise was to first get our spending below $100,000 per year and then to also figure out our Minimum Monthly Spend (MMS). In doing so, we found that we could easily reduce our spending to below six figures – in fact, almost overnight (our first level of cutting landed us at an annual spend of $96,814 or $8,068 per month). And if things got really tough, we can easily drop our spending to $58,623 per year or $4,885 per month.

We’ve taken action immediately and pulled the “quick release” valve to let out the inflation that had crept into our spending over the past five years. Don’t get me wrong, that lifestyle was by design and even encouraged under the law of 50/50, which allowed us to spend up to 50% of our after-tax income guilt-free as long as we saved the remaining 50%.

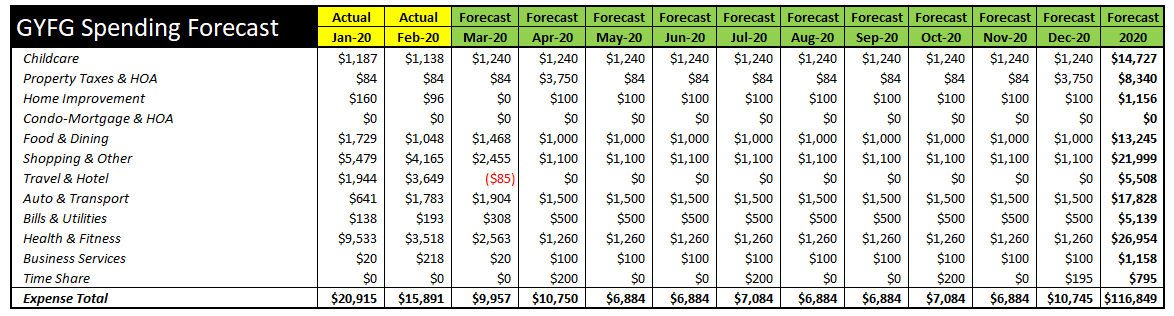

If you’ve run through a similar exercise to prepare your own family’s household for potentially challenging months ahead, I wanted to introduce the next step. It’s one thing to come up with a fixed monthly and annual spending number, but that isn’t nearly as useful as putting together a monthly expense forecast whereby you figure out when you will be spending money by month. Below I will share that for the GYFG household based on our new level of spending at $96,814 per year. I know I typically spend much more time talking about the income side of the equation, but since I currently have a lot less visibility in what that may look like through the rest of 2020, the next prudent thing to do is manage the expenses until there is less uncertainty around our household’s income.

Since most of Q1 was already in the rearview mirror at the time I created this, January through March are what they are (FYI – March is a forecast based on our spending through 3/27 per Personal Capital). You can see that our spending in the first few months of January and February was very high. They were higher than “normal” because we had some large expenses related to a functional health program we are currently going through as well as a getaway that my wife and I took to celebrate our eighth wedding anniversary.

You can see in March that the “shelter in place” order naturally helped reduce our spending. After accounting for the money that has already been spent, you can see that our new annual spend of $96,814 is a bit lower than what our actual spend for 2020 will be since we really only have nine months of spending remaining this year that we can impact (because it hasn’t happened yet). Over the next nine months, April and December will be peak spending months as this is when our property tax installments are due.

We feel very comfortable with this spending level at least through June as that is when my current backlog of business will be exhausted. Luckily I have already pre-collected all of the revenue upfront, so I don’t have to worry about that evaporating as companies pull back spending. My wife also feels confident that her income is safe for at least the next few months. (Side note: I have significantly reduced our income projection for 2020 – slashing it by 40% from previous projections)

Although the government has officially passed a $2T relief bill, the US is still on lockdown as we move through the “eye of the storm” and wait for this virus to slow its roll. It’s a waiting game for us all to see what happens next. I’m sure families and businesses are feeling less anxious knowing that help is on the way. But we are all left wondering what life looks like on the other side of this virus. Some are speculating a v-shaped recovery. Personally, I have absolutely no clue how long it will take for us to resuscitate the economy after the viral storm has passed. I do think that life is going to be different as we all adjust to what will likely be a new normal, at least for a long while. And just like those who survived the global challenges of their generations, I’m sure that none of us will ever forget this!

Stay Healthy!

– Gen Y Finance Guy

p.s. here is a link that defines the eligibility to receive the one-time direct payment. The maximum a family can receive is $7,500. The income limits are $75,000 for an individual and $150,000 for a couple (with phase-outs up to $99,000 and $199,000 respectively). If you find yourself in hard times this might help you.

p.p.s. and for businesses check out SBA 7(a) Paycheck Protection Program Loan. We are looking into this for my business and have already submitted the initial application. I also recommend you read the piece that the team and Permanent Equity put out here that summarizes the specifics.

3 Responses