It’s hard for me to believe that everything is just going to go back to normal overnight. Or even that we’ve seen all the pain we are going to see during this pandemic. But I also acknowledge that I could be wrong – either in my timing or hypothesis of what is likely to happen next. There is no doubt many businesses have or will fail due to the blow of this pandemic (and the resulting restrictions to “business as usual”). On the other side of the coin, there are going to be other companies that thrive in the “new world.” My business (software consulting) is one of those businesses that is not only surviving but thriving in this environment (after the initial shock of the pandemic had worn off).

I took my protective measures in the event this got worse, which is in the eye of the beholder. For me, “getting worse” means that it hit home by impacting my family’s income and threatening our livelihoods. To date, those measures have proven not necessary, but I don’t regret taking them and would do the same without hesitation.

The GYFG family has been living a more “normal” life in that we have been doing some fun things that are not limited to the confines of our own house. Eating out. Renting a house by the beach (thank you to my business for financing that for my family, my team, and their families). A lake trip. Going to the gym. You know…things we did pre-pandemic. This also means letting go of the white knuckle grip I had the family purse. This loosening of the purse strings is driven by several factors:

(1) The easing of government restrictions on what we can and can’t do.

(2) Seeing my income not only remain stable but increase during this pandemic. The same has happened for Mrs. GYFG, who is in Real Estate, as her business has posted record revenue figures for the past several months.

(3) Having taken certain precautions to hedge the downside:

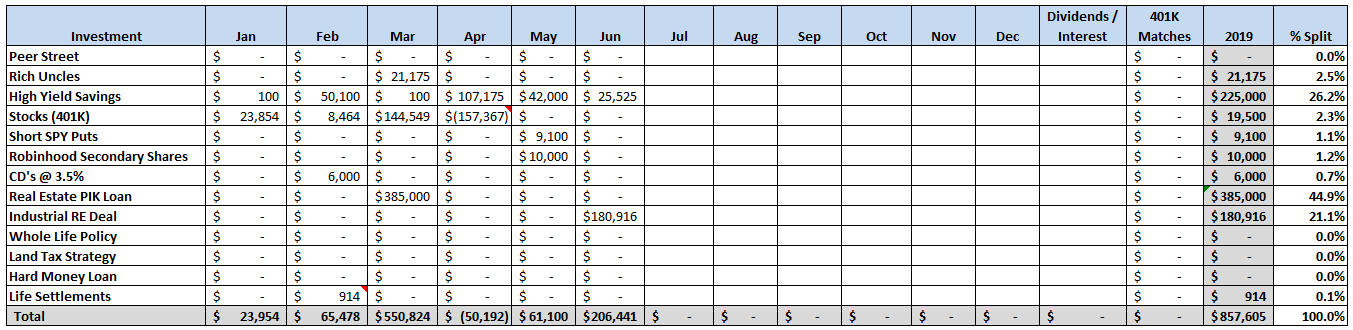

a. First, we’ve only got 6% of our net worth tied up in stocks. I liquidated all but Mrs. GYFG’s 401k account after buying pretty damn close to the pandemic lows.

b. We’ve built up a massive cash hoard. Although down from ~$570,000 last month, it’s still sitting at ~$449,000 this month.

c. Purchasing a plethora of put options on the S&P 500 (an article I still owe you guys – soon!). The way I look at it is I’m willing to risk up to $10,000 annually and if I’m wrong that means my business is doing very well and so are all my other investments. If I’m right, it could pay 50-100X, hopefully enough to offset any damage to my business and other pieces of the GYFG family net worth.

d. Deploying capital into assets that should do well with inflation, particularly real estate. I’m avoiding commercial real estate that focuses on office space, gyms, and retail. Instead I’m focusing on another sub-category of commercial real estate – industrial real estate (property that is used for manufacturing, processing, or warehousing). I’ll talk about one such deal later on in this post.

e. Deploying capital into other interesting investments with built-in downside protection. For example, I will be participating in a SPAC focused in the media/entertainment space, and it comes with full capital protection over the next 18-months should the management team not be able to deliver. I’ll provide more details in July’s post after the deal has been funded.

All this has me feeling much better about the future regardless of the outcomes in the short term because I feel like we are covered..by being prepared. That is the one thing I promised myself after being unprepared and unable to really participate during the financial crisis in 2008/2009. I’m still willing to take risks in pursuit of compensating rewards, I’m just not willing to do it without the right risk management plan in place. I never want to put my family’s lifestyle unnecessarily at risk.

In the next section, I’m going to start sharing my financial dashboard in full detail (again) and provide commentary below on certain key areas.

Financial Dashboard

Net Worth:

Current Net Worth: $2,008,444 (up +20.2% for 2020)

Previous month: $1,945,625

Difference: +$62,818

We finally hit the $2,000,000 mark, which is the goal we set at the beginning of the year, to exceed $2,000,000 in net worth by the end of June. I’m still not holding a value for my business in my net worth and depending on the multiple you use, that could add anywhere from $300,000 (1X) to $1,400,000 (5X).

Net Worth Break Down:

Real Estate (67%) – This category includes the equity in our primary residence, a hard money loan at a 10% interest rate, our investment in the Rich Uncles commercial REIT, and our hard money loans through the PeerStreet platform. This also includes a 4% PIK loan. This month we did see an increase here after making an investment into a industrial real estate deal that I’ll detail in the deployment section below.

Net Cash (22%) – This is still a large position but we did see our cash position drop about $115,000 vs. last month.

{kind=link}

Life Settlements (5%) – Flat vs. last month. We currently have investments in seven policies. They are accreting in value by about $1,000 per month. For anyone familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with this fixed return you are amortizing (realizing) that value with the passing of time. Two of these policies have required capital calls as the insured has lived past the estimated life expectancy (which eats into the expected return). I started investing in these policies in late 2017 and have yet to see a return of capital or a return on capital. I have another year before another two policies are expected to mature and if they don’t I will be required to make annual capital calls to those as well to keep the policies in force.

Stocks (6%) – This is flat.

Total Projected Income in 2020: We are currently on pace to earn $1,031,408. Keep in mind that ~$415,000 of that is from a realized gain from selling the stock I owned in my previous employer.

Total Capital Deployed in 2020:

Last month I said:

“We are currently sitting on about $570,000 in cash and I believe I have found a home for another $181,000 (the amount sitting in an IRA that I rolled over after leaving my employer). I’m currently in the process of rolling this into my self-directed IRA as I am going to be participating in an Industrial Real Estate deal – specifics to come once I make the investment. The sponsor has negotiated a property with about 450,000 square feet of space at $20/sqft. The replacement cost to build the same is about $120/sqft. It is a fire sale deal by a very large public company that isn’t in the business of real estate and just wants it off their books (they got it through an acquisition). More details to come.”

I did in fact complete that rollover of funds to my self-directed IRA and funded the deal mentioned above. Although the sponsor has negotiated the purchase of the entire 450,000 square feet of space only about a third of the property has actually been acquired. They are pre-leasing each building before funding each part of the deal. I really like the margin of safety built into the deal based on the following three factors:

(1) We are getting this deal for significantly under replacement costs.

(2) We are pre-leasing the space with 15-year leases: “The 450,000 SF building will be leased immediately upon close to 3 tenants at 150,000 SF each, at $1.00 per/SF/month, with a 9-month deferred rent payment and 6 months reduced rent structured into the lease contract. This will generate a gross revenue of $427,500 per month or a 25.63% cash on cash (net) without the use of debt.”

(3) It is an all-cash deal, which provides a lot of flexibility if things don’t go exactly as planned. We won’t have creditors breathing down our neck. And because of the economics of the deal it is still expected to produce mouth-watering cash on cash returns.

The projected timeline is to close on the remainder of the property by the end of July. One thing I didn’t mention was that it is also located in an opportunity zone, which comes with a lot of tax benefits if you have capital gains to shelter. I didn’t mention it initially because I was investing through my self-directed IRA and since that money can’t benefit from the opportunity zone it went into one of the two LLC’s that isn’t set up to take advantage of this.

However, since I have ~$415,000 in capital gains from selling my stake in my previous employer, I have decided I will deploy an additional $100,000 into the second LLC to defer the taxes on some of those gains. This sponsor would normally plan to exit an investment like this within three to five years, but because of the opportunity zone, the plan is to hold for ten years, because if you hold for ten years your tax basis will step up significantly reducing the deferred taxes. And…if held for 10 years the appreciation from the investment above and beyond the capital gain rolled over will not be taxable at all.

You only have 180 days from realizing the gain to deploy the capital in an opportunity zone, which means I need to fund this by early August. It’s a lot like doing a 1031 exchange based on the timeline you have.

Expenses

Well, this section only lasted a couple of months before I got bored with it. I stopped tracking our expenses for a reason and I was reminded of that reason when I sat down to write this month’s report. I stopped tracking because we spent the past five years building a habit of saving at least 50% of our income and we do it naturally without thinking about it. I still think it is a good exercise to review spending at least every 6-12 months to make sure you’re not spending unnecessarily. As long as income is stable I don’t see expenses becoming an issue.

Savings Rate

This is still a very important metric but I think it has run its course on this monthly financial update. I will still track this but as long as it stays at 50% or higher, I will no longer be thinking about it much.

Net Worth Conversion Ratio

Definition: The Net Worth Conversion Ratio measures an earner’s ability to convert earned income into wealth or net worth. It excludes passive income since passive income is dependent on the earner’s decision of putting earned income to work or spending on consumption.

This is a new metric I want to start tracking monthly moving forward. Now that “the machine” is in full production, it is time to not only bring back the net worth conversion metric but to make it a star of the show. I once wrote that financial nirvana is reached once hitting 100%. Next month will be the first month I will be sharing this new metric in these monthly updates. When I first calculated this back in early 2016 the GYFG ratio clocked in at 25.3%. Since then we have significantly increased our savings rate and the gravitational pull alone should have moved it much closer to 50% these past few years. We’ll see next month…

Closing Thoughts

The last few months have been very transformative for me in many different aspects. I’ve been very focused on clawing back a lot more of my time in order to spend it with my family and on my own fitness. I’m also working hard to make sure I don’t become a slave to my business. I have learned that what got me to where I was prior to starting the business was not going to be what got me to where I wanted to go. I’m done with 70-80 work weeks on the regular, those now become the rare exception. I’ve put strict restrictions around my time, only allowing 40 hours a week for running the business and another 10 hours for writing this blog and managing my family’s net worth. The rest is being spent spending time with my family, working on my fitness, reading, and more leisure than I’ve historically had in my life.

I’m currently hard at work laying the groundwork for the next level of growth and scale in my business. The goal of all of this is to put the right systems and people in place to allow me to start taking half days on Friday when my son turns two in October. I will be spending that extra time making memories with my son. I’ve already been taking way more vacation than I ever did when I was employed for someone else. Now I’m working on condensing my work week from 40 down to 30 hours a week over the next 15 months and going down to a half-day on Fridays will be a nice step in that direction.

I’m allocating more focus on managing the time fortune that was bestowed upon me.

– Gen Y Finance Guy

8 Responses

Hi Dom – I like how you are not afraid to deploy capital with risk management in place.

I would also like some downside protection in my investment portfolio. Are you able to share what put options did you buy to try to hedge out downside equity risk?

Any chance the industrial warehouse sponsor is looking for more investors? 🙂 25 percent cash on cash is tremendous.

Hey Rich,

The put option I’ve purchased (and traded around) are the Jan ‘21 $100 strike puts on the SPY ETF.

They are deep out of the money but they also get extreme leverage with big spikes in volatility. I’ve traded around my core position on days with big volatility spies and have already taken my risk capital off the table.

I have a post I’m working on that shows how these puts perform with respect to volatility as measured by the VIX.

I’ve historically only sold options but now find this interesting given the uncertainty we live in.

If you have a platform that allows you to view historical option prices check these out and see how they have moved in relation to both the underlying and volatility.

BTW – I made an introduction between you and the sponsor. Let me know if you participate.

Thank you for your response and your introduction to the sponsor.

GYFG! Congrats on hitting the $2mm milestone! Kind of a big deal! My sincerest hope for you, speaking as someone who hit that milestone 3x, is that the GYFG household continues up-and-to-the-right! Happy to learn that you are taking vacation/personal time as a form of compensation.

Knowing that you have read Tim Ferriss’ “4 Hour Workweek” per your previous posts and discussion, I would be interested to know if there were an specific ‘hacks’ you incorporated to switch your mindset from the 50-70 hour work weeks to your current level of efficiency. The last few years of my worklife, my time was my own and I resented the intrusions (phone, e-mail, requests for info, repeated raising of issues that had been put to bed, etc.) by people who were ‘paid to look busy’. I cut my phone and in-person interaction to the bone, and that was massive.

Continued success to you, happy you have cracked the code to thrive in this uncertainty!

Thanks, JayCeezy! I too hope that we can continue up and to the right in terms of our net worth trajectory. You know that one of my personal goals is to get a little richer every day (on average). The only way I know to try and manage that is to keep growing the income side of the equation to try and outrun the inflection point where the % movement in our net worth is out-matched by the savings due to an ever-increasing income.

I think the biggest shift for me is to learn to delegate more – only spending time on the 5% of things that are the highest and best use of my time. I’m slowly learning to use leverage – not financial leverage – but leveraging systems and other people’s time and talent.

I also have less interest in working those long hours…I honestly didn’t mind them earlier on…but I also knew that that wouldn’t be the case forever.

Hi Dom,

Love what you are doing here.. I recently found your blog and I have learned a lot! I will continue search for opportunities that will eventually help me eliminate my 9-5 job and become financially free. I am slowly getting there! I did have a question with peerstreet. With the current COVID scenario, we are seeing more deals go into default. I diversified into about 15 projects a year to two years ago, and 5 of the projects are late on payment and 3 of the properties have issued Notice of Defaults. One of the deals finally paid me back (with interest) almost a year after maturity. Do you still think P2P loans are sustainable or are funds a safer route like Fundrise/RichUncles?

Thanks again for all you do

Hey Jon – Thanks for reading along. I’m glad you’ve gotten something out of the blog.

In terms of P2P, I do still like PeerStreet but I have completely pulled out of Prosper and Lending Club where the rates got so compressed the unsecured nature of it become uninteresting to me as the risk/reward profile changed. I like PeerStreet because the loans are at least backed by the Real Estate. The majority of my activity here is in a self-directed IRA and as long as I eventually get paid I don’t really care if the loan is late or falls into default. The average LTV across my portfolio is 67% so there is a significant equity cushion to protect my capital from losses.

These days I only invest in loans with a max LTV of 60% and a minimum interest rate of 8%. My bigger concern here is the cash drag as the deals flowing through the platform has significantly slowed.

I’m also an investor in Rich Uncles and I don’t think it’s any safer and not really comparable as you are investing in a different part of the capital stack – equity vs. debt. Due to COVID my Rich Uncles investment took a 30% haircut so it is not immune.