The mantra for the month of July was “Finish Strong!”

Once we cross over the halfway point of each year, I get this uncontrollable urge to finish and close as many loose ends as possible. This ranges from open house projects, investments, food in the house, books, blog posts, etc. Below are some of the things I was able to get across the finish line in July:

- I invested an additional $100,000 into the Industrial Real Estate deal that I wrote about last month. This time it was into a separate LLC that was created to take advantage of the Opportunity Zone tax benefits. I have ~$415,000 in gains from liquidating my equity position in my former employer and this investment will help me defer and reduce the taxes associated with the $100,000 I invested in July (a lot like a 1031 exchange).

- I funded a $50,000 investment I committed to in June. The investment is in the Vista Media Special Purpose Acquisition Company (SPAC).

- I completed a full branding exercise with a marketing professional for my business.

- I secured two strategic alliances with other consulting partners that do what my company does to gain access to flex resources.

- We completed our solar expansion project that took our original solar system installed in 2015 from 15 panels to 30 panels. This cost $12,000 out of pocket but I will be receiving the 26% federal tax credit when I do my 2020 taxes.

- We completed the installation of our two Tesla Battery Walls. The gross price of these was $27,400 but the state of CA will be sending us a rebate check within the next 60 days for $26,400, for a net $1,000 cost out of pocket (before the 26% federal tax credit when I do my taxes for 2020).

- Finally finished writing the blog post that outlines the hedging strategy that I’ve alluded to for the past several months: Low Probability + High Return Hedge Strategy

- I filed my taxes for 2019 and have already received the $45,000 refund (a combination of state and federal).

- I secured a beach house for the whole month of November for the family – it’s the same house we rented for my company’s retreat back in June. I negotiated a flat rate deal, and by extending our stay to 31 days (checking out December 1st) was able to get rid of all the taxes because on day 31 it is no longer considered a short term rental.

There are a few other big items I’m working to finish up by the end of August:

- We have decided to put a mortgage back on our house and have locked in a rate of 2.865% for a 30-year loan. We originally purchased our house for $370,000 in 2014. Conservatively, it is currently worth about $500,000 (I say “conservatively” because the lender we are working with took this stated estimate and waived an appraisal). We are pulling out $300,000 in cash. I’m hoping to close on this by the end of August but it may slip into September.

- In conjunction with the branding exercise I mentioned above, I’m also in the middle of a complete website redesign for my business. The target is to push that new site live this month.

Overall, July was a very productive but chaotic month. Mrs. GYFG and I were firing on all cylinders out of necessity due to the growth we are both seeing in our respective businesses. Funny…just last month I was talking about how balanced my schedule had become and then it all blew up in July. We are hoping for a less hectic month in August.

Financial Dashboard

Net Worth:

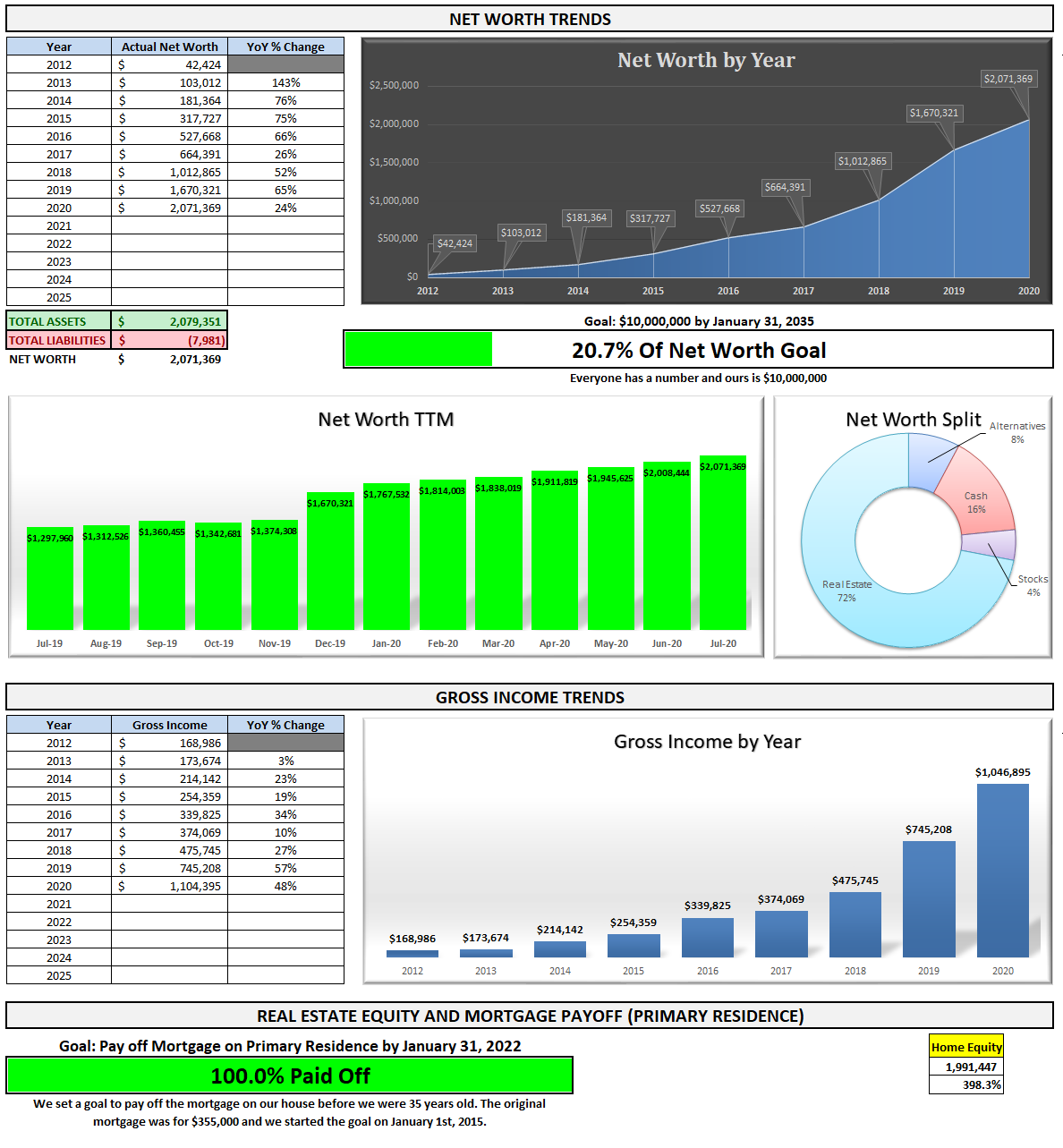

Current Net Worth: $2,071,369 (up +24% for 2020)

Previous month: $2,008,444

Difference: +$62,926

Note: I’m still not holding a value for my business in my net worth and depending on the multiple you use, that could add anywhere from $300,000 (1X) to $1,400,000 (5X).

Net Worth Break Down:

Real Estate (72%) – This category includes the equity in our primary residence, a hard money loan at a 10% interest rate, our investment in the Rich Uncles commercial REIT, and our hard money loans through the PeerStreet platform. This also includes a 4% PIK loan. This month we did see an increase here after making an additional investment into an industrial real estate deal that I’ll detail in the deployment section below. We will be reducing our concentration in the real estate category in the near future (see note below).

Net Cash (16%) – This is still a large position but our cash position did drop about $118,500 vs. last month. We plan to see an increase of $300,000 in cash in the next 30-45 days. That’s because, after being mortgage-free for 15 months, we have decided to put a mortgage back on our house with a cash-out refinance. This will help us reduce our concentration in the real estate category, while also taking advantage of the lowest mortgage rates in history. We were able to lock in 2.865% for a 30-year mortgage (more details below).

{kind=link}

Alternatives (8%) – This is a new catch-all category that captures our investments in the following: life settlements, a special purpose acquisition company (SPAC), and a private investment in the Robinhood trading platform.

Stocks (4%) – We have not been deploying new capital into stocks nor do we plan to in the near future.

Total Projected Income in 2020: We are currently on pace to earn $1,046,895. Keep in mind that ~$415,000 of that is from a realized gain from selling the stock I owned in my previous employer. I think our income does have upside potential to finish the year at $1,200,000 but I’m not counting those chickens before they hatch.

Total Capital Deployed in 2020:

The format of this table has changed to provide better clarity on net deployments because the table was misleading by not showing some of the liquidations that occurred to fund some of the new capital deployments. So, now you can see the gross deployments netted against the gross liquidations. I wanted to provide this view so I knew what the net new capital deployment was as some of the activity this year has been re-deployment of returned capital.

We’ve been busy the first seven months of the year and I don’t currently have much that’s new on the radar for the remaining five months…and honestly, I need to take a little breather anyway. Back to building up the cash war chest.

Net Worth Conversion Ratio

Definition: The Net Worth Conversion Ratio measures an earner’s ability to convert earned income into wealth (net worth). It excludes passive income since passive income is dependent on the earner’s decision of putting earned income to work or spending on consumption.

This is a new metric I will be updating and sharing monthly. Now that “the machine” is in full production, it is time to not only bring back the net worth conversion metric but to make it a star of the show. I once wrote that financial nirvana is reached once this metric exceeds 100%. When I first calculated this back in early 2016 the GYFG ratio clocked in at 25.3%. Since then we have significantly increased our savings rate and the gravitational pull of increasing both our savings rate and income helped us significantly improve the performance of this metric, which now clocks in at 65.8%.

You will notice that I have shared the metric based on ‘earned income’ and ‘all income’ but I’m most interested in the earned income calculation (per the definition above).

The goal the past five years since adopting this metric was to focus on increasing our earned income while simultaneously saving at least 50% of our after-tax income in order to create excess capital for investing. I should note that excluded from the earned income calculation is any income derived passively from investments and more recently profit distributions from my business (I do include the W-2 income I earn as an employee of the business).

The end goal is to get to a point where net worth is 100% or greater than earned income – bonus points if you can accomplish the same thing based on all income sources. I expect our net worth conversion to finish the year somewhere between 70% and 75%.

On No Longer Being Mortgage-Free

So many things have changed in the world and in our personal lives since setting the goal to be mortgage-free. The original goal was to be mortgage-free by January of 2022 and we did it by May of 2019. Our net worth has nearly doubled since paying off the mortgage and we have diversified our income away from being mostly W-2 income through both investments and by starting a business. I also wanted to be in a strong financial position to launch from when I found the right opportunity to go off on my own because entrepreneurship was always in my future. I didn’t want the pressure of a mortgage hanging over my head.

I don’t love debt but I have always believed there is a time and a place to use it responsibly. Still, I will always prefer a low debt profile over a high debt profile. I do this knowing that I’m leaving potential gains on the table. In return for a more conservative approach to debt we also have more optionality than those who are highly leveraged. I’ve shared this before but I’ll share it again and that is that we optimize for peace of mind over maximum financial return.

Once interest rates hit below 3% I couldn’t stop thinking about how cheap a 30-year mortgage would be and whether it was something the GYFG household should take advantage of. After weeks of contemplation I decided that we should move forward with putting a mortgage back on our primary residence for the following reasons:

(1) This may be the cheapest money we will ever see in our lifetimes. I couldn’t believe that I was able to lock in a 2.865% mortgage rate for 30 years. I would never want to be on the other side of that trade…I’m guessing most people are with me, which is why the Fed’s balance sheet is exploding. It feels like free money at this point.

(2) We don’t need the money now but the best time to borrow money is when you don’t need it. We plan to make one more move, and that is into our dream house, which is related to the $385,000 we deployed in March. This ‘paid in kind’ loan is on my in-laws’ property. Our intention is to convert it to equity in the next 18-24 months. There is currently a $400,000 loan on the property that we would assume (currently at a 3.6% interest rate), and the property is currently valued at ~$1.6M (conservatively). We know that we will need $200,000 to $300,000 to make improvements to the property to make it our own.

(3) We plan to convert our current home into a rental once we move into the dream house. We had always intended to put a mortgage on the property once we did that in order to not leave too much equity “lying around doing nothing.” With interest rates so low, we decided that it would be in our best interest to act now, in case rates significantly increased in the next couple of years. By pulling out $300,000 we are getting back most of the $370,000 original purchase price. Looking at comparables today we believe we could rent our house out for $3,000 per month with a net free cash flow of about $1,000 per month after covering the mortgage, HOA, taxes, and insurance.

(4) The risk of inflation. There has been a massive amount of money created out of thin air due to the federal government’s response to COVID-19. The Federal Reserve has also committed to doing whatever it takes to keep the economy from crashing…pledging trillions of dollars in liquidity to keep the credit markets from freezing up. Fixed-rate debt can act as a very nice hedge to higher inflation as the debt becomes less expensive to service when inflation rises (assuming your income is rising as well).

(5) We want to reduce concentration risk in both our primary residence and real estate generally. As you saw above, we are currently very concentrated in real estate, with 72% of our net worth tied up here. This refinance will help us bring that concentration down by approximately 15%, reducing our exposure to 57% of total net worth in the real estate category. So, you could also look at this as a rebalancing of the portfolio. Once the cash-out refinance is completed, our primary residence will only be 10% of our net worth – down from 25% as I type.

(6) More dry powder to deploy in investment opportunities that arise from the COVID-19 mess. I think there could be “once in a lifetime” buying opportunities in the next 6-18 months.

(7) We now have more than enough passive income to pay for the mortgage. We have one long term hard money loan ($150,000 note) that pays 10% ($1,250), which alone covers the new mortgage payment we are taking on. I’ve passed on several similar deals with this same associate that could triple this monthly income by deploying up to the full $300,000. I don’t mind borrowing at 2.865% and earning 8-10%. My business also generates a significant amount of passive income.

(8) We could use a little leverage in our life. Even with $300,000 in debt, our assets are 8X larger (at ~$2,400,000).

Closing Thoughts

The one thing I have learned from the past six years in sharing my thoughts here on the blog is that thinking can and should evolve as circumstances change (and as the world changes). In February of this year, I shared a reflection on the things I believed to be true in terms of the principals that guide you towards achieving financial independence and I’ve remained very consistent in my philosophy with tweaks along the way. Until now, a part of my strategy the past six years has been to be mortgage-free and it made sense for us at the time…and it no longer makes as much sense for us right now.

Although I do think it necessary to adopt a set of wealth-building fundamentals (like the ones I linked to above), I won’t be afraid to change my mind on the tactics or strategies I deploy within the framework of those fundamentals. The GYFG household has 11 such guiding principals (originally shared as the Tenacious Ten – we added one this year) that we have followed religiously these past six years, with the intention to continue following them for the indefinite future.

We still have a couple of loose ends to close up over the next month or two but there are two things I’m very much looking forward to in the near future:

(1) I’ll be going down to a four and a half-day work schedule in October in order to spend more quality time with my son. The plan is to pick him up around 11 am from daycare, get lunch together, and then put him down for his nap. I’ll work for a couple of hours while he naps and then we will do something in the afternoon when he wakes up. It could be jumping in the car and heading to the beach for a couple of hours. Going to the wild animal park. Going on a bike ride. Going over to Grandma and Grandpa’s for pool time. That is just to name a few of the ideas I have for us.

(2) In November we have a beach house booked for the entire month. This is all a part of our ideal 3-6-3 lifestyle, whereby we spend three months living by the beach, six months living at a home base, and three months traveling (could international or domestic). This is a lifestyle that we have been growing into and this will give us a total of six weeks by the beach for 2020. We will temporarily relocate there for the month. Mrs. GYFG and I will still be working for part of the month on a modified work schedule and then will be completely off for half the month.

I hope you and your family are staying healthy and making the best of summer.

Onward & Upward!

– Gen Y Finance Guy

14 Responses

Hey Dom,

Long time reader. Funny enough I recognize the place you are renting for a month. I rented this very place with my in 2018. The picture on the wall above the kitchen gave it away. Awesome place to enjoy. There is a great Healthy eating place that is walking distance that has great coffee and food. I don’t want to say too much here since this is public and all.

If you want the name email me and I will give it to you

Enjoy,

Hey Randy,

It’s a small world! We rented the unit below in June for my company’s retreat and are excited to enjoy the view again for a whole month. I will email you for the name of the food recommendation.

Dom

I want the name of the place so I can rent it at some point. It’s seems like it’s THE place to rent.

Would love a beach house for a month. We did two weeks and it was wonderful. Maybe next year we’ll try for a month.

Great job consistently growing your net worth. We are in similar, albeit different shape.

I reduced hours as well to spend more time with our kids and have no regrets. Losing my consulting income hasn’t hurt our ability to save and grow our net worth yet.

Thanks for sharing, TPM!

I’m looking forward to a reduced schedule later this year to spend more time with my boy.

“Fortis Fortuna Adiuvat,” – Latin proverb, also one of John Wick’s tattoos.

Awesome moves, GYFG. Am loving the return of the consolidated dashboard. That chartreuse really pops! Tasty way to end the day for you and Mrs. GYFG, too, can recommend. Maybe you’ll enjoy it at the beach house, with a sunset, breeze, and dirty blues soundtrack playing just under the sound of the waves.

Hey JayCeezy,

I love the Latin prover you shared. It reminds me of another one I picked up after reading The Endurance that tells the amazing story of Ernest Shackelton and his leadership ability to lead he and his crew to safety after shipwreck in Antarctica. His family moto was “Fortitudine Vincimus,” which translates to “by endurance we conquer.”

I’ll add those ZZ Top songs to the beach house playlist.

Dom

Awesome view from the beach house! I’m jealous of your November abode.

I’m also a big fan of taking advantage of the cheap mortgage rates now available. The 30 year fixed rate is at a historic low and nice to see that you were able to take advantage of it.

Yes, me too!

One of my employees just locked 2.625% last week on a 30-year mortgage with no points and closing costs will be about $2,000 (mind blowing!!!).

Hi Dom, glad to see you continue to do so well. Your Opportunity Zone investment piqued my interest, is it through a sponsor you know personally? You stated that you put $100k out of $415k in capital gains into this investment. Any plans for sheltering the remainder? The taxes are gonna be high, especially with the added Obamacare tax and being in California…

Hey Joe,

It’s nice to hear from you, it’s been a while. Were you ever able to dig up any of that old content?

I think about your x-factor comment a lot these days.

Yes, I did invest $100,000 into an Industrial Real Estate deal located in an opportunity zone. I had already invested $190,000 a couple months back through my self-directed IRA (not into the LLC that is set up to take advantage of the Opp zone) while I waited to get some capital returned.

I know the sponsor through a friend in a private investment group I belong too. I would love to shelter more but don’t want to put it all in one basket. Of the $415,000 gain, approximately $120,000 of it will be taxed at ordinary income since it was from selling options, leaving an additional $200,000 to possibly shelter – ideas?