I have a lot of little things I’d like to share but none that seem worthy of a full dedicated post. Therefore, I’ve decided to group all those little things into this post with a handful of “bite-size thought-snacks.” They are thoughts I want to document and maybe even drive up some discussion in the comments if anyone has anything thoughts or insights to add.

Let’s jump in!

Mortgage Rates

I think the table below speaks for itself. As I shared last month, rates had become so low that even I couldn’t resist putting a mortgage back on our primary residence.

I was born in the 1980s and can’t imagine paying almost 13% or 4X the prevailing interest rate we see today. Rates are so low the money almost feels like it’s free. I wouldn’t want be on the other side of the trade holding a 30-year note for less than 3% interest! If we get the inflation I think we will over the next decade the real return in terms of buying power of investors holding these mortgages will end up being negative – this happens if inflation runs higher than the 2-3% we have seen for as long as I can remember.

Could rates go lower?

At this point anything is possible. I found this table from back in 2016 that shows mortgage rates under 2% in some countries around the world:

Is anyone else concerned about and/or preparing for much higher inflation in the future? If so, what kind of moves are you making? What sectors do you believe will benefit from an inflationary environment? Or, do you think it will be more of the same we’ve seen since the 2008/2009 Great Financial Recession?

I’m personally positioning the GYFG household to be long hard assets, which is why 72% of our net worth is currently allocated to some form of real estate. I’m also short the dollar via mortgage debt – thus the 2.865% mortgage we decided to take out. I’ll get into this more in the “Dream House” section below, but we will also be converting our $385,000 PIK loan with a 4% interest rate to an equity position.

I know that there are plenty of people gravitating to gold and cryptocurrency but without a cashflow attached it’s hard for me to get behind it…if you know what I mean (remember my Warren Buffett post that discusses this).

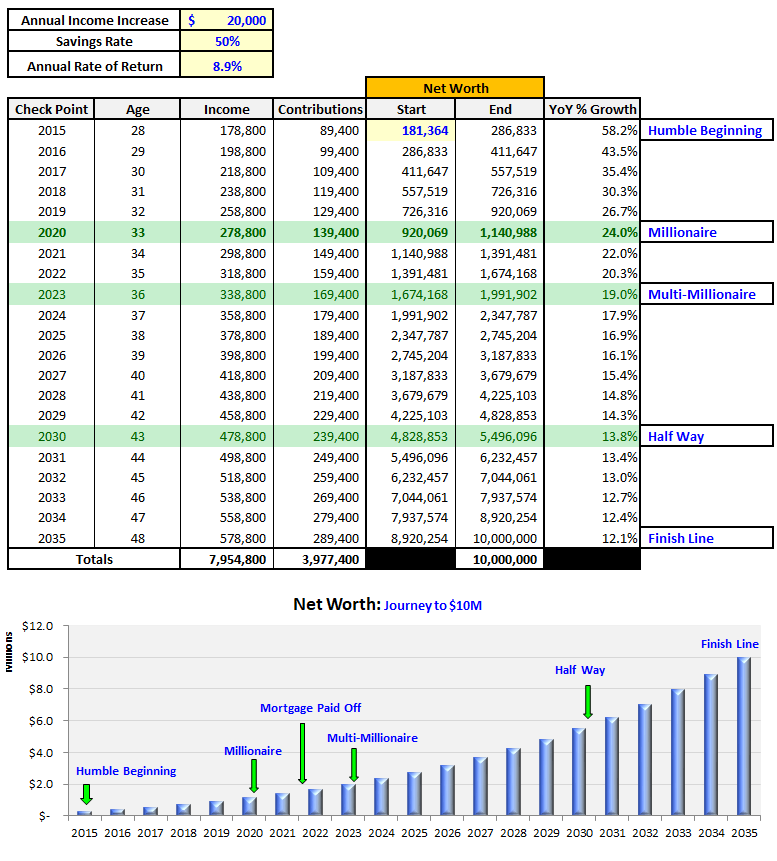

CAGRs to Reach $10M Goal

It’s been a few years since I updated my progress towards the 20-year plan I shared at the beginning of 2015. The last update I shared was in early 2019 shortly after we officially hit $1M in net worth. A common theme in my life has been accelerating timelines and that has been especially true with respect to our progress towards the original blueprint (screenshot below).

This plan was based on three major assumptions:

(1) Achieving a gross savings rate of 50%. (we have done this or better most years)

(2) Increasing our gross income by $20,000 every year. (we have done much better than this – like six-figure increases on average)

(3) Earning an 8.9% compound return. (this one is harder to measure and I’m too lazy to try to calculate it)

We have exceeded all income projections through 2035. Our income hit the 20-year target in 2019 with a year-end finish of $745,208. We are currently projecting an income of $1,104,395 for 2020. It’s obvious that income is the engine that fuels our net worth, along with some nice gains on investments.

As you might imagine, outpacing our income goals has helped us stay ahead of our net worth goals. Based on the plan, we projected to officially exceed $1,000,000 for the first time at the end of this year (2020). We actually achieved that two years early, at the end of 2018. Currently we are on pace to finish 2020 with a net worth of $2,400,000!

This puts us about four years ahead of schedule on the net worth front, so I’ve been playing around in a spreadsheet to see what it would take to accelerate our goal and move the finish line to age 40 instead of 48. In the table below you can see that to make that happen I need to increase net worth by 27% every year for the next six years (assumes we hit $2.4M with a 44% growth rate in 2020). The percentage doesn’t look crazy but the absolute dollar increases do look intimidating especially in the final year, which would require $2.1M in increases.

That said, I don’t think it is out of the realm of possibilities and I’m now going to try to start working towards this new target. The real x-factor that could help me hit and potentially beat this new target date is the eventual sale of my company, which I’m hoping to cash out of for multiple millions (if I can hit my targets). Since I can’t predict when our net worth might eventually take a hit from market conditions out of our controls I don’t try to bake those into our equation. My hypothesis is that as a whole we all will recover and either get back on track or be delayed a few years. I’m prepared for the downside but I don’t plan for it in this type of projection that I’m just trying to understand directionally.

Does anyone have any ideas to help me hit this aggressive target? Do you think I’m crazy yet? (Mrs. GYFG knows I’m crazy!)

Dream Home

The Mrs. and I have always intended to move up one more time. I can’t say it will be a forever home but it will be the home we raise our kids in for the next 20 years. Yes, I said kids, we are officially trying for baby #2. Our son will be two in October, so if our timing works out they should be about two years apart, plus or minus a few months.

You may recall me sharing back in March that we had made an investment of $385,000 in a ‘paid in kind’ (PIK) loan with a 4% interest rate.

Since last summer (2019) we have been discussing the idea of buying my wife’s parents’ house. My father-in-law built the house about 30 years ago and Mrs. GYFG has very fond memories growing up there. It is in the middle of the wine country in Southern California – right where we have always wanted to end up. We extended the loan to help my in-laws out regardless of whether we decided to buy their house or not. However, we did agree ahead of time that if we decided to buy the house that we would convert the note plus accumulated interest into an equity position. We also agreed to assume their first mortgage if we decided to move forward with the purchase.

We took the time to think about it and to look at other properties in the surrounding area. Every place we looked at was compared to their property. They have one of the most incredible views of the valley…definitely a multi-million dollar view. We also developed a list of concerns we had with such an arrangement with family and recently sat down with Mrs. GYFG’s parents to discuss those concerns and iron out the details.

The house is 5,000 square feet on five acres. It has a 3,000 square foot shop, an RV garage, a pool, 100+ avocado trees, citrus trees, apple trees, and a 1,100 square foot guest house. I should mention that as a part of our arrangement my in-laws will be downsizing to live in the guest house when they are not at their houseboat or traveling during their golden years. I know this would be a non-starter for some but we are very keen on the arrangement, especially since we have discussed all the sensitive issues upfront.

I won’t go into details with the specific financial arrangement but I will say we are aligned and on the same page. We have identified about $200,000 worth of improvements that we want to make before we move in and the best part is that my father-in-law is a contractor and designer who has agreed to do the work (the quality of his work is amazing – you’ll see in future photos). As far as timing, we plan to move into the “big” house by January of 2022 or about 17 months from now. This also aligns with my mother-in-law’s official retirement (her husband is already retired but takes on side projects for fun).

Our plan is to start making the improvements now so that we are not living through a remodel. The biggest project on the list to complete before moving in is a complete kitchen remodel and replacement of the AC throughout the house (the AC unit is 30 years old and doesn’t work well). We also plan to install solar on the house. The other big project that we will tackle once we live there is to remodel the pool area, which we don’t mind living through since it will be outdoors.

The plan is to turn our current house into a rental. We estimate that we should be able to gross $3,000 per month and net about $1,000 after expenses.

Income (Earned, Passive, Phantom, and Future)

This has become something I’m obsessing about. We’ve all read that the average millionaire has at least seven sources of income and I’ve been working hard these past few years to diversify our income streams from being solely reliant on W-2 income. Below is a tally of all of our income streams based on year to date values.

Earned Income

- $15,261/month in W-2 Income from my business

- $12,343/month in W-2 Income from Mrs. GYFG

Sub-Total = $28,604/month

Passive Income

- $25,694/month in profit distributions from my business (up from $12,186/month in 2019)

- $1,250/month from a $150,000 hard money loan at 10%

- $1,000/month from notary services (Mrs. GYFG’s side hustle)

- $586/month from a Commercial REIT that pays a 7% dividend (although due to COVID-19 this has been cut to 5% and I’ve taken a 30% haircut on valuation)

- $600/month from hard money lending (through PeerStreet – the majority of this is in a self-directed IRA)

- $500/month from selling tradelines

- $200/month from my blog

- $150/month from CDs and High Yield Savings Accounts

- $100/month from dividends (all in a 401K)

Sub-Total = $30,080

Phantom Income

- $1,285/month from $385,000 interest-only note at 4%

- $300/month because of solar investment that paid back our original investment about 18 months ago.

Sub-Total = $1,585

Current Total = $60,269 (Annually = $723,228)

Note: this only includes recurring income and does not include the gain we realized this year from liquidating my investment in my previous employer.

Looking ahead there are a few more income streams that we can look forward to.

Future Income

- $5,852/month from $280,916 Industrial Real Estate Investment (anticipated to start distributions in summer of 2021)

- $2,083/month in an after-tax account

- $3,769/month in a self-directed IRA

- $1,000/month from renting out our current primary residence

Sub-Total = $6,852/month

Future Total = $67,121 (Annually = $805,452)

I would like to get total income from recurring sources to a total of $100,000/month or $1,200,000 annually by the end of 2021. That means I need to generate an additional $32,879/month in income. If the business keeps growing the way it has to date, I can see a large portion of that delta coming from that, but I also know that I’m going to need to continue putting money to work as well.

#BIGGOALS

That’s the extent of this smorgasbord of my “bite-size thought snacks.” What about you? What are you noodling on these days? Thoughts on any of the above?

15 Responses

It’s pretty incredible if you are able to accelerate your $10 million net worth goal almost a decade early than initially budgeted while still enjoying your life and living in a dream house.

Your choice to go into business for yourself is certainly paying off.

Thanks, Rich!

Although we have realized acceleration against the original plan, we still have to prove out if we can accelerate it by a decade…big difference in the extra 4 years. I do agree that the business has been a great x-factor in this wealth-building journey.

At what age did you hit $10M in your own net worth (i.e we hit $1M at age 30 and $10M at age 40)? What were the big accelerators for your household? I’m just curious as I find modeling others to be extremely helpful.

Dom

I got there in my late 30’s (maybe around 37/38). It was a period of time when I didn’t track my NW as closely.

The big accelerator is just the law of large numbers and the nice run up across a number of asset classes including listed stocks.

S&P 500 Total Return For Past 10 Years:

Dec. 31, 2019 31.49%

Dec. 31, 2018 -4.38%

Dec. 31, 2017 21.83%

Dec. 31, 2016 11.96%

Dec. 31, 2015 1.38%

Dec. 31, 2014 13.69%

Dec. 31, 2013 32.39%

Dec. 31, 2012 16.00%

Dec. 31, 2011 2.11%

Dec. 31, 2010 15.06%

Imagine entering the start of 2013 with $3 million invested in the stock market. You get an extra $1 million by year end just due to stock appreciation.

Your NW will start compounding quickly and will result in larger and larger dollar changes.

Congratulations on hitting your milestones early. I agree that the sale of your company can propel you much further than your $10M target.

Personally, this year has been spending more time with my family; especially my parents given that I’m not traveling as much. And Coronavirus puts everything in perspective.

Booked my over water bungalow in Maldives for early next year to ring in 2021

Thanks, FFC!

I hope I can sell the company and cash out millions – that’s the plan I’m marching towards, but I have to get it to a big enough scale that it doesn’t require me…as in I can’t “be the business” otherwise the value will be significantly less valuable to a potential buyer.

I’m glad you have been able to spend more time with your family. Your vacation in 2021 sounds very fun!!!

Cheers,

Dom

Particularly interesting that the passive income exceeds the ‘W-2’ income (I think that’s what you call employment income in the US).

Big dreams, a lot of hustle, a plan and careful execution yield exceptional results.

Winning at life!

HH

Hey HH,

Yes, the W-2 income is income as an employee. I too found it very interesting that our “passive income” has exceeded our earned income. Although the passive income isn’t 100% passive, most income sources rarely are.

I’m trying to win and hustle for as long as I have the energy. These days I’m trying to work smarter and not longer hours 🙂

Dom

GYFG, have you heard of “Biflation”? The term is fairly new to me, at first I thought it was one of those Intersectional ‘Woke’ terms for someone using dolls. Turns out, it is when both Inflation and Deflation happen at the same time. The highest mortgage rate I paid was 12.5% in 1989, so I’m feeling you on the Mortgage rate confusion.

Coincidentally, the payment on a 12.5% mortgage would be twice the payment on a 2.85% mortgage.

Deflation, these things would have to happen: 1) demand decrease; 2) surplus of goods-and-services; 3) fall in money supply; 4) output increase; decrease in employment

Inflation, these things would have to happen: 1) demand increase; 2) scarcity of goods-and-services; 3) increase in money supply; 4) output decrease; 5) increase in employment

A decline in confidence and/or a recession could cause Deflation. I’m seeing the intentional increase in money supply to be an ‘encouragement’ of Inflation. The Deflationary pressures are hiding the negative impact of the federal deficit tripling in 15 years, to $26 trillion. People notice food prices are rising, but food is less than 5% of household budget. Gasoline was $2.50/gallon in 2005 and is about that now. There are years worth of light crude floating in supertankers, and demand has been decreasing. It doesn’t seem to matter. Hmm.

Am loving that the GYFG household keeps stacking money, that is the only surefire way to increase NW. You already have a great family home, but your In-Laws home sounds awesome! Looking forward to hearing your progress on that eventual transaction.

“Embrace the Grind!” – Daniel Cormier

Hey JayCeezy,

That’s the first I’ve heard the term “biflation” – it’ll be interesting to see how it unfolds over the next few years.

We are already lining up some improvements to the new house even though our move in date is 17 months away. We need to replace the AC system that is 30 years old and hanging on by a string. We also are in the process of getting solar added. And some Tim early next year we will start a kitchen remodel.

Dom

I love it, Dom! And thanks for the refi referral. I ended up going with Sebonic @ 2.875 with $474 in lender fees. I can’t complain about that (well, unless you look a today’s rates… haha). They’re a bit slow, and the loan officer is a bit of an a$$, but it’s coming along. Still can’t believe sub 3%!

The house sounds awesome. And 5 acres to do whatever you want with – incredible. I’d do it for the avocado and fruit trees alone! 😉

Keep up the momentum. You’re crushing it!

Thanks, Michael!

I’m glad Sebonic worked out for you.u wife is in the escrow business and lenders are so overwhelmed with the refi volume that they are all moving slower than normal. We are supposed to close on 9/15.

We both got locked right before Freddie and Fannie announces an increase of half a point in all refis effective 9/1.

Dom

Thanks for the transparency on your income! It really helps people see what the possibilities are to increase income and put the money to work. I’m always looking for possibilities. My husband’s consulting has certainly helped us grow our NW and several other smaller income streams. Inflation certainly helped us get to our current x,000,000 status, as well, after 2008. Looking now to get into hard assets, but so is everybody else, inflating prices for rentals in which to invest. Warren Buffett says to be greedy when everyone is fearful and fearful when everyone else is greedy . . . .Trying to see how that applies to us and hope we figure it out before opportunity passes us by! Thanks for the transparency!

Money That!

I like the name. I’m glad my transparency is helpful. I know seeing and talking about real numbers has certainly helped to open my eyes to the opportunity and potential out there.

Cheers,

Dom

Yikes, living on the same piece of land with in-laws, hiring an in-law as a contractor, buying a house from in-laws. Maybe you should go for broke and take up hang gliding too? You obviously have a thing for high risk and extreme danger!

Steveark,

Hang gliding actually sounds fun to me…maybe I am a risk junky and didn’t realize it until now – LOL!

I know what we are doing is not common but I have special in-laws. And after 15 years of being a part of their family I still really enjoy spending time with them. The same house would be crossing the line though. Worst case it all blows up and you get to read about it here first on the blog.

I hope you’re well!

Dom