First and most importantly: I was finally able to procure some toilet paper for the GYFG household!

I still don’t understand why people started hoarding TP as if it were gold but I’m glad we had enough on hand to get us through the initial panic phase of this pandemic. The news hasn’t gotten any better but we all seem to be adapting and moving past the shock of it all. There is still plenty of uncertainty on the horizon with respect to where we go from here…most of which plays out daily well beyond my control. That being said, I believe even more strongly in the importance of focusing on what I can control!

Like many, the GYFG household has been tackling a lot of deferred home cleanup and improvement projects since we have been “sheltering in place.” Below is a list of projects we have been able to tackle over the last six weeks:

(1) Built the table for the backyard that we’ve been wanting since upgrading our backyard last September. The base and the top are constructed of wood but the top was coated with a concrete finisher. We have wanted an oversized table for so long in the backyard. Our goal was a table large enough to fit eight comfortably as well as plenty of room down the center for the many dishes we plan to share with friends in the months and years ahead. Mrs. GYFG was the brains behind this operation and she got it built for a couple of hundred bucks.

(2) Finally fixed that faulty electrical outlet that went out years ago…better late than never! Below is a picture of the old one because I was too lazy to take a picture of the new one. It’s nice to be able to plug in a Sonos

(3) We’ve wanted to build planter boxes for a home garden since we moved into our home six years ago. Voila! They are finally built, and we planted them during the first weekend in May. We’ve planted several types of tomatoes, jalapeños, beets, carrots, basil, mint, rosemary, squash, and peppers.

(4) I bought the family some electric bikes for Christmas back in 2018 with the intention of family bike rides. However, we had to give it some time until baby GYFG was old enough to ride in the child seat I purchased. The recommendation we read said to wait until he was about a year old and had full control of his neck. At last, I installed the child seat on the rear of my bike and we have been enjoying family bike rides every week.

(5) We cleaned the garage as we do every year. In the process we finally mounted mirrors on the wall in our home gym workout area, converted from one of the three car spaces in our garage when we first moved in. The mirrors came from the closet doors in what is now my home office. We had removed them years ago and just leaned them against the garage wall with the intention of eventually removing the mirrors from the metal casing and actually mounting them to the wall. This project hit a few road bumps but we got through it. The mirrors ended up cracking in a few spots but we decided to live with it. Mrs. GYFG is going to help me neatly write the following two sayings on them: (1) Don’t let your workout break you, and (2) Don’t let perfection be the enemy of good enough!

We weren’t only productive in the home improvement category. The Mrs. and I have invested a significant amount of money in our health this year seeing a Functional doctor, and we began health protocols halfway through April to start optimizing our bodies – inside and out! We have been using this extra time under quarantine to get into the best shape of our lives. In addition to the plethora of different supplements we take on a daily basis, we are practicing intermittent fasting, daily activity/workout, naps, meditation, and eating a very clean diet. After only two weeks we are feeling so good! Our energy levels are high and stable throughout the day. I don’t know if you can feel vitality but it is stronger than ever in us and we can’t wait to see what the coming weeks and months have in store for us. I’ve personally lost 11 pounds in the past two weeks and I’m down to a weight I haven’t seen since April of 2018. Best of all, it hasn’t been very hard at all.

April was also a great month for securing the future of my business. We just finished our first full twelve months in business at the end of March and have big goals for the next twelve months. Below are the highlights since COVID-19 struck:

(1) We hired an additional full-time employee on April 1 as planned. This was a bit scary to follow through with in the midst of the pandemic unfolding but I was very honest and transparent with the current team and the “new guy” about the health of the business. I put “new guy” in quotations because although he is now a new full-time employee, he has been moonlighting with us since August of 2019. This new hire has really given me the ability to scale myself as I let go of certain items on my plate.

(2) We added about $700,000 in contracted work to the backlog. The year had been off to an amazing start and the pipeline of future work was overwhelming…but then COVID-19 hit and that all vanished overnight. It’s understandable that companies would pump the brakes on all spending given the current circumstances. But I would be lying if I didn’t admit being very worried about my team who rely on the business to fund their livelihoods. Before winning this new work I again was transparent with the team and let them know that they might want to tighten their spending and save as much money as they can over the next three months (April – June) as our current backlog at the time had enough work to keep everyone busy just until the end of June. Then this new business was added, and we all took a deep breath again.

(3) In response to the above, we got the opportunity to make an additional full-time hire, and that person officially starts May 4th.

Lastly, on the financial side we have continued to perform well, in spite of the challenging environment we find ourselves in. With that, let’s dig in!

If you’re a regular reader you know that I typically have a formula to this post, but for the next couple of months I feel the need to change it up. I realize that my family is in a fortunate financial position to weather a storm like this and I feel awkward going through the normal cadence of this report as if everything is hunky-dory. I want each reader to know that I am hesitant to continue sharing our financial statistics in light of the pain that many are feeling right now. At the same time, I pledged to continue publishing these reports every single month until I hit my BIG financial goal. It is also important for me to lead by example to continue responsibly managing my family’s finances – through both good times and bad. I think it’s important that transparency is maintained to see how finances are managed in both bull markets and bear markets. That said, I will be removing some elements so it is not as “in your face” when it comes to certain aspects of the normal report.

Net Worth

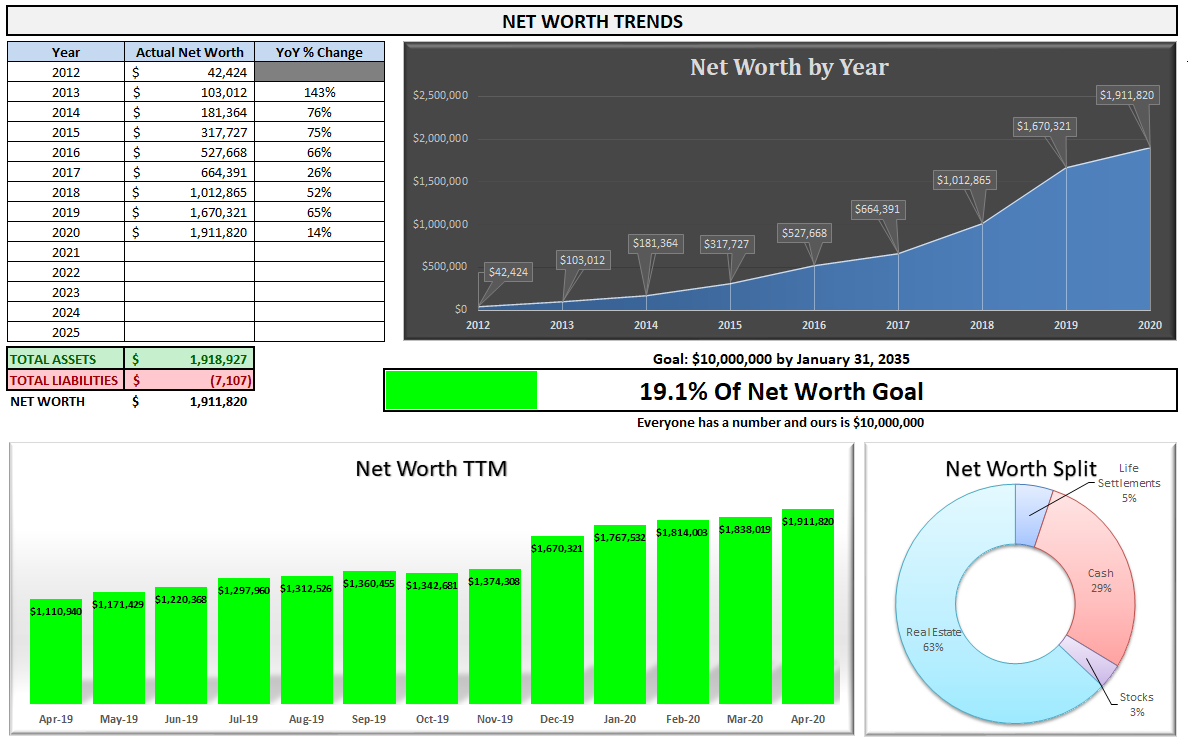

April Net Worth $1,911,820 (up +14.5% for 2020)

Previous month: $1,838,019

Difference: $73,801

Net Worth Break Down:

Real Estate (63%) – This is a decrease from the 66% figure last month. This category includes the equity in our primary residence, a hard money loan at a 10% interest rate, our investment in the Rich Uncles commercial REIT, and our hard money loans through the PeerStreet platform.

Net Cash (29%) – This is up from 14% last month. The primary driver was liquidating all the stock positions I put on in March.

{kind=link}

Life Settlements (5%) – Flat vs. last month. We currently have investments in seven policies. They are accreting in value by about $1,000 per month. For anyone familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with this fixed return you are amortizing (realizing) that value with the passing of time. Two of these policies have required capital calls as the insured has lived past the estimated life expectancy (which eats into the expected return). I started investing in these policies in late 2017 and have yet to see a return of capital or a return on capital. I have another year before another two policies are expected to mature and if they don’t I will be required to make annual capital calls to those as well to keep the policies in force.

Stocks (3%) – This is down from 15% last month. I ended up liquidating most of the positions I added during the lows in March (all of our purchases were made between 3/12 and 3/23 when the market – measured by the S&P 500 – was down 25-35%). I didn’t intend to hold these for such a short period of time but I also didn’t expect the market to bounce back as much or as fast as it did. Toward the end of April, the S&P 500 was only off its highs by 10%. Had I known I would be keeping these positions on for such a short period of time, I would have been better off not selling the calls against them – hindsight is always 20/20. I still made a very nice return (like 2x the average market return). I also was starting to feel very uncomfortable with how much capital I had deployed all at once and since I optimize for peace of mind, backing that down felt like the right move to make.

It feels like we dodged another bullet in April with our net worth increasing almost 4% for the month. At some point I expect real estate (our largest holdings at $1.2M) to get impacted by the pandemic but there are several variables that may insulate us from feeling much of that impact, if any:

(1) There is $639K composed of loans with max LTVs of 65% or less. This means we wouldn’t suffer any markdowns until real estate is down greater than 35%.

(2) There is $464K tied up in the equity of our primary residence and we only re-value this once a year.

(3) Lastly, there is $100K invested in a Commercial REIT that again is only re-valued once per year.

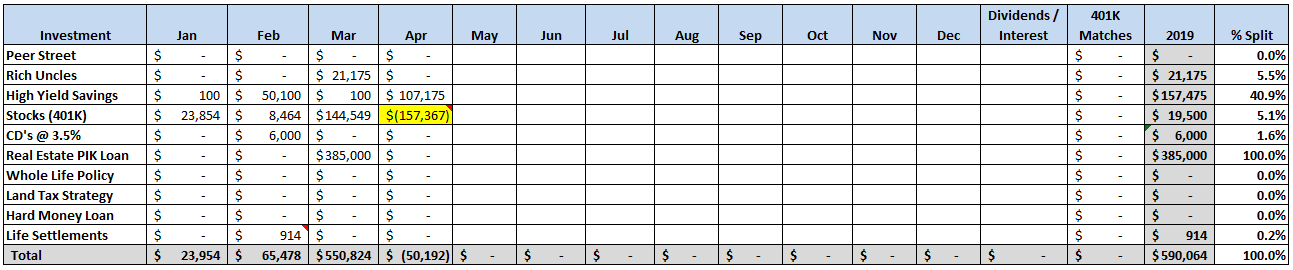

Total Capital Deployed in 2020:

My 401K for 2020 was maxed out prior to my last day with my previous employer in February. Mrs. GYFG maxed hers out in April. However, you will notice in the above table that on a net basis we have no new capital deployed to stocks in April as our liquidations to cash was significantly more than the final contributions that Mrs. GYFG made to her 401K. Overall, stocks have only received an additional $19,500 in deployed capital in 2020 and that is because I don’t touch Mrs. GYFG’s account (as in it remains invested and is the only account where we are invested in stocks).

The plan for the next couple of months is to continue building up our cash war chest. The stock market makes absolutely no sense to me right now. I don’t understand how we can have 30 million people unemployed, many businesses still shut down, trillions in federal stimulus money, trillions of dollars being printed by the fed (by increasing their balance sheet), and still no certainty on when this pandemic will be behind us. GDP for the first quarter fell at an annual rate of 4.5% with the back half of March being the only period impacted by COVID-19, meaning we have only seen the beginning of the damage done. Economists are forecasting a 20-30% annualized decline by the end of Q2. The world doesn’t make sense to me right now!

I do have some ideas bubbling around my noggin but I’m not ready to share them just yet.

Expenses

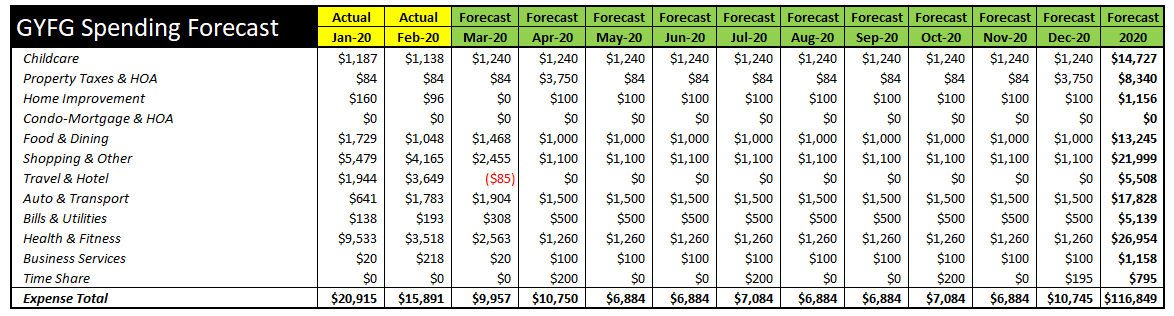

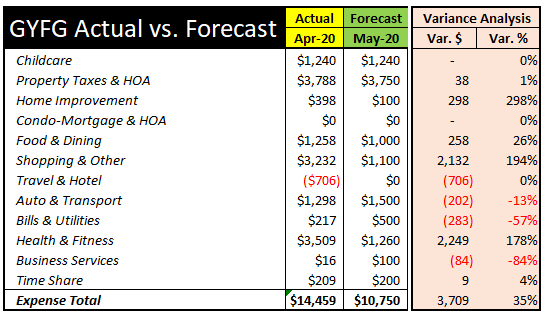

Coming into 2020 I had made the decision to not track our expenses anymore. Well, that lasted for all of two months. I have not had a section for expenses in these financial reports for well over a year, but with the new spending plan my household is adopting, I find it necessary to track our spending against that plan. Each month I will be comparing our actual spend vs. the forecast spend in the screenshot below.

The above table represents the original forecast that I put together for the remainder of 2020 and is the benchmark I will be tracking to. I expect to see more volatility in the month to month figures as our spending is lumpy and not evenly distributed. In April, we ended up spending significantly more than I had planned, but of course there are reasons why (there always are).

We only overspent by 35% – yikes! I promise we have not lost our ability to control our expenses.

We spent almost $2,000 on supplements (Health & Fitness category) for the whole family as a part of our health optimization journey in 2020. I know – I had sticker shock, too, but we are committed to our health and the program we signed up for. So far in 2020, our investment in our health has been approximately $14,000 (about $12,000 was related to all the baseline testing we did – none of which was covered by insurance). But we are already starting to see drastic improvements since starting our uniquely created personalized protocols. This may very well end up being the best investment we make in 2020!!!

Additionally, we overspent in the “Shopping & Other” category because we switched our phone service from Verizon to Mint Mobile. This required us to pay off my wife’s iPhone ($600) and pre-pay for annual service on two phones ($480). We still have a third line that I pay for my brother that will be switched over in late May. This move will end up saving us $2,000 per year going forward.

These two items account for the majority of the variance vs. the forecast. I still expect our May spending to be about 50% of our April spending. Our month over month spending will automatically decrease by $3,700 because we won’t have another property tax payment until December. We also won’t have nearly as much to spend on supplements or switching phone service (which ultimately is a savings but pulled future spending into the present).

Savings Rate

Tracking our expenses means we are back to tracking our savings rate as well. The only difference is I’m going to update it only once a year. Our goal remains saving 50% of our after-tax income.

Below is a historical snapshot of our after-tax savings rate since we started tracking it in 2015.

Do you want to calculate your own savings rate? I’ve made it super easy for you with the savings rate calculator included in the free GYFG FI Toolkit that you can download instantly by clicking the link below. Here’s a peek. Did I mention it’s free? You have nothing to lose and everything to gain, Freedom Fighter! Remember, what gets measured gets managed.

Speaking of savings rate, go check out my post where I mathematically prove the importance of your savings rate as a higher priority in achieving financial independence than your compound return. If you’re trying to build wealth quickly, then you have to read this post.

Closing Thoughts

I am starting to wonder if maybe a pandemic is just what we all needed to get back to what is really important. Please don’t take this as minimizing the real pain some are feeling – I’m not saying that those experiencing loss due to the disease or financial hardship due to loss of income needed these challenges. But personally, this pandemic has created the margin we personally needed in our calendar to address things that desperately needed our attention. We are re-calibrating and re-prioritizing our time. I’ve always been guilty of allocating too much time to work and the pursuit of financial goals and not enough time for my family and my health. This pandemic has given me an opportunity to reset.

The last six weeks have been transformational for me. Don’t get me wrong, I still have plenty of work to do, but I’ve made quantum leaps in a short period of time to evolve into the multi-dimensional man I was born to be. I’m using my business as a lever to create more free time, which is why my latest two hires were so important. I need to be the master of the business – not a slave to it. I’m grateful for the extra time with my family. And I’m grateful for the time I have to work on my health.

During these challenging times, I encourage you to find the silver lining in all of this. I still think that optimism is everything! Please find your reasons to be grateful!

Be well and stay healthy!

Cheers,

– Gen Y Finance Guy