It’s that time of year again, where Mrs. GYFG and I look at the year ahead and plan our 2017 finances. I’m not sure if I have articulated my philosophy on budgeting in prior posts or not. So, it might make sense for me to briefly touch on the topic.

You won’t find many articles on this blog about budgets or budgeting. That’s not because it’s not important, it’s just not something I personally spend a lot of time with. For the most part it is a very short conversation.

Personally, I create a budget once a year, but it is a high level view of our personal P&L. We create this as a road map for the year ahead, it’s not absolute, but it is our best guess of where we plan to spend money, and how much we plan to earn (we figure out the earning side first, before we work on the expense side). When I say we create a budget, I am referring to the royal we (a way of saying “I” when you feel like sounding schitzophrenic), as I do all the work and then pass the budget on to Mrs. GYFG for review (she hardly has any changes outside of the home improvement category). I have gotten to know her pretty well over the last 11 years that we have been together.

There are two different budgeting approaches that I would like to distinguish from each other:

Control Based Budgeting – This is the type of budgeting that I think most people are most familiar with. You set monthly/annual budget amounts, and the idea is not to spend a penny more than was budgeted. This is the most popular form of budgeting when you are early in your financial journey and need to stay tight on your expenses in order to reach your financial goals. It’s also an approach I assume a lot of the frugal weirdos use (that term is not meant to be an insult). It’s just that if you are going to be extremely frugal, then this seems like a requirement, given how slippery money can be.

Allocation Based Budgeting – Once you have gotten your financial groove and start to see a substantial increase in your income, this may be a natural progression out of control based budgeting and into allocation based budgeting. Let’s say you adopt a simple rule like the law of 50/50, where you save 50% of your after tax income, and spend the remaining 50% guilt free. Once you have your income for the year figured out, it is pretty easy to back into the spending bucket allotted for the year. It’s really just a matter of allocating that bucket to different spending categories. You may or may not spend all the money in that category or you may even decided to spend more than the original budget. You may even decide to re-allocate it to a different category later in the year.

Allocation based budgeting is really just a mechanism to get an idea of where you will be spending your money based on what you think will bring you the most joy. That may mean a sizable home improvement budget and/or a sizable travel budget. It’s likely it will change from year to year, especially as you continue to super charge your income. If you really hit the sweet spot, you will find that you can’t find a way to spend the whole 50% (like the GYFG household has, as you will see below), which will go strait to increasing your savings rate.

Of course there is a time and place for each of these approaches depending on what your goals are and where you are in your own journey. It is natural for most people who adopt a budget for the first time, to start with control based budgeting.

We exclusively use the allocation based method to budgeting.

With that, let’s dive into our 2017 budget…

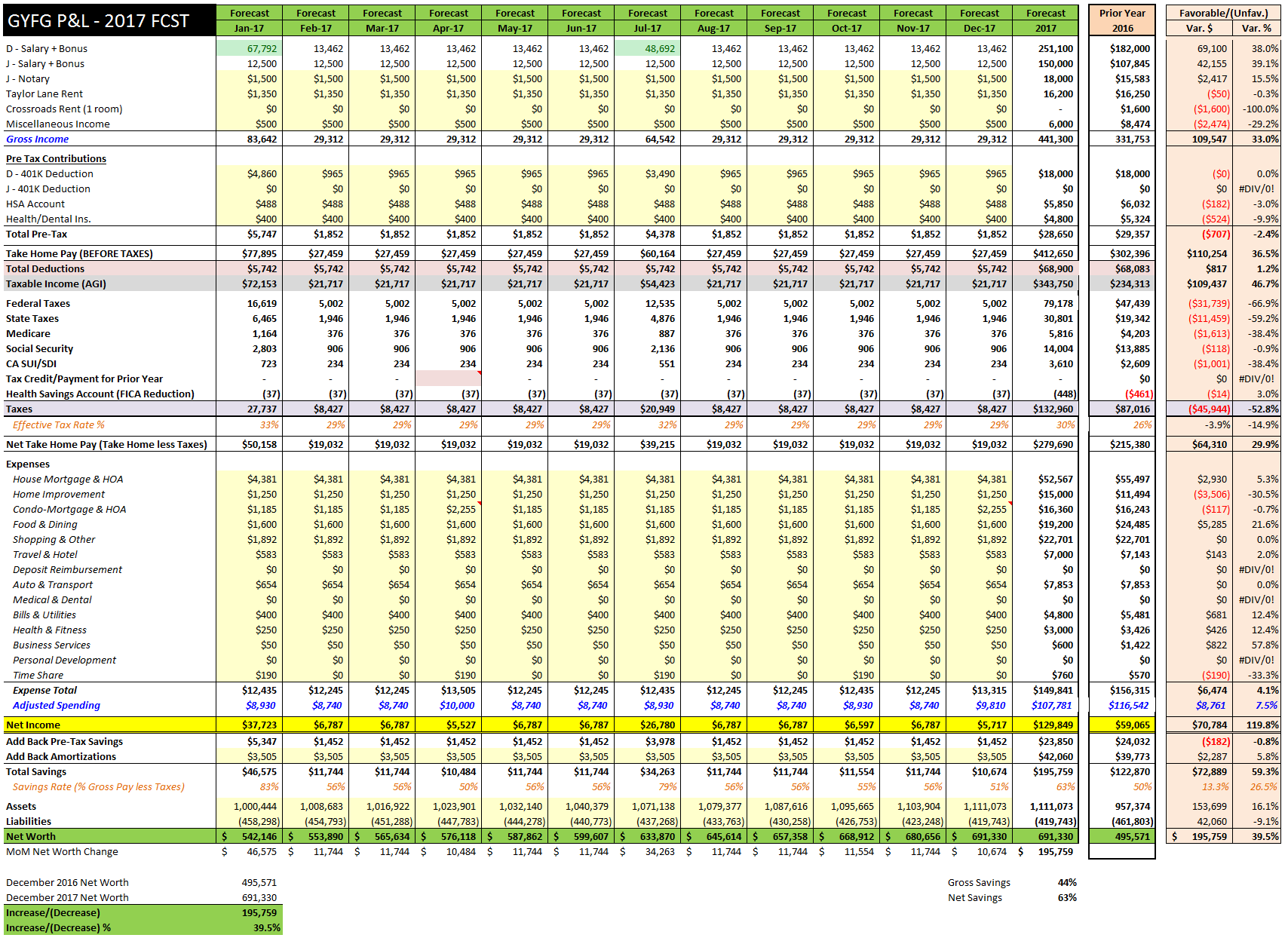

The GYFG 2017 Annual Budget In All It’s Glory

It’s probably best to break this down by each major line item. I know it’s a big screenshot above (I recommend you view it from a large computer screen; if you click on the image, you will get a larger view of the P&L), but I wanted to share with you guys exactly what I create every year.

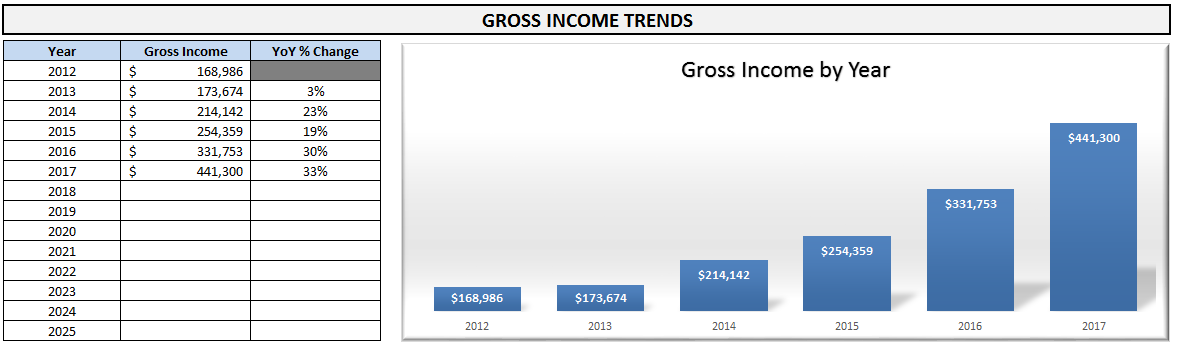

Gross Income – As I recently shared in this post, we are currently projecting gross income in 2017 of $441K (it has actually slightly come up since that post). As you know from reading this blog, we put a heavy emphasis on the income side of the equation. We experienced a 30% increase in income in 2016, and are projected for another 30% increase in 2017. There are two major variables at play here: (1) my income is increasing 40% due to the promotion to CIO and (2) my wife recently got a 25% raise and has been killing it with monthly bonuses.

As you can see from below image, our income has continued to grow at a very robust rate. Since 2012, it has compounded at 27% per year. The compound annual growth rate is even better than that if you go back even further like I did in this post (just my earnings) or this one (you will have to do the math; but it is for the GYFG combined income).

Pre-Tax Contributions – This is relatively flat YoY. We have a slight decrease in our HSA contributions due to my company upping its annual contribution into our plan. And the premiums we pay for health and dental are also forecasted to decrease by 10% as my company picks up a larger chunk of our coverage. Thank you employer!!!

Taxes – A topic that makes me want to puke, especially when I see they will be going up 53% in 2017. I know that taxes are a good problem to have, but it doesn’t feel fair to have to pony up $133K in taxes. The good news is the more you pay in taxes the more money you’re making. We just have to work on creating more tax efficient income streams outside of our day jobs, as the marginal rates are getting ridiculous. I think 2017 puts our marginal tax rate at 51.85%; 33% marginal tax rate federally, 10% state marginal tax rate, then you have medicare at 1.45%, social security at 6.2%, and lets not forget the extra medicare tax of 0.9% for high earners (you wouldn’t want to miss that one). It is what it is…

As I dive into the expense section of the P&L, I think it is important to point out that Mrs. GYFG and myself believe that we have hit a sweet spot in terms of spending. Meaning that although our goal is to save 50% and spend the other 50% (guilt free), as our income continues to increase we don’t see much need to increase our expenses. This just means our savings rate and investments can continue increasing. And after this year we will largely be done with our home improvements, which will free up $10-$15K a year, which will make it even harder (in a good way) to increase our spending.

Home Mortgage & HOA – We plan to resume our mortgage snowball plan in 2017. We will be tacking on an additional $2,400/month in principal to our mortgage. To stay on track of our 7-year goal, we technically don’t have to resume this until April of 2017, due to our recent cash-in refi. However, we have it resuming in January…at least for now. You will notice that due to the amount of money we brought into the refi, this category is actually showing a slight $3K savings YoY.

Home Improvement – This year we plan to put tile flooring on the entire bottom floor of our 2-story house. We estimate this will cost us about $10K all in. Additionally, my wife would like to put in a dry bar in our formal living/dining room (we estimate at $5K). After these two projects, we see this category shrinking dramatically in 2018 and beyond. These are the last few remaining projects on our list. This will be a nice chunk of change freed up in 2018.

Condo Mortgage & HOA – This is essentially flat YoY. This is related to our investment condo, and it is showing a slight increase of $117 due to a slight change in our adjustable interest rate. What this doesn’t currently contemplate, is that we intend to finally complete that cash-in refinance we attempted earlier this year. We anticipate the refinance to free up about $300/month in cash flow. And now that almost a year will have passed by the time we pick up where we left off, we don’t think we will have to bring any money in as we have since amortized the loan another $5,000 and comps have continue to rise as similar units sell. The only cost will be about $1,000 in closing costs.

Food & Dining – This category got a little ridiculous this year. This is an area where we get a lot of joy out of our spending. That said, we are planning for a $5,285 savings in 2017. We were both working like dogs in 2017 and just didn’t feel like finding the time to cook (although its typically something we enjoy doing). We ate out a lot more than usual. We plan to slow down a bit in 2017, and thus plan to have/make more time for cooking together.

Shopping & Other – This tends to be a catch all, because I am too lazy and not interested in expanding the current 14 expense categories. This category was actually up about 54% in 2016 and I am budgeting it to be flat in 2017. It’s likely up more than it should be because I didn’t reclassify all of the expenses Mrs. GYFG spent on what was technically the home improvement category. That’s okay because I have the transactional detail if I ever want to go back and see what we spent money on in any category.

Travel & Hotel – Flat YoY. I should point out that this amount is slightly misleading as we apply all of our cash back from rewards cards to this category. In 2016 that amounted to about $1,800, but our plan is to sign up for at least one new lucrative rewards card each year, like the Sapphire Preferred card that earned us a $900 bonus just for signing up and putting our normal spending on the card.

Auto & Transport – Actually planning for some savings here, mostly due to our insurance premiums dropping as speeding tickets fall off our record at the end of this year.

Bills & Utilities – Small savings planned, not sure why…I will need to look at this closer. It’s not a big enough dollar amount to matter though.

Health & Fitness – This is coming down about 20% since I stopped going to cross-fit and instead traded in my $125/month membership fee for an LA Fitness membership at $35/month.

Business Services – I had some one-time expenses related to growing the blog and experimenting with a few things that won’t show up in 2017 (at least I don’t think they will). It’s a savings of almost 58%, but only about $800.

Time Share – This is going up slightly YoY because I incorrectly classified the January payment, and again I am too lazy to go back and fix it, so really it’s flat YoY.

Overall, our spending is actually projected to be down by 7.5% or $8,761. Adjusted spending is the line you want to focus in on, and the the difference between this line and the expense total line is that I add back amortizations, since those are just balance sheet transfers. When you’re working to grow your wealth rapidly this is the perfect relationship where income increases while expenses decrease.

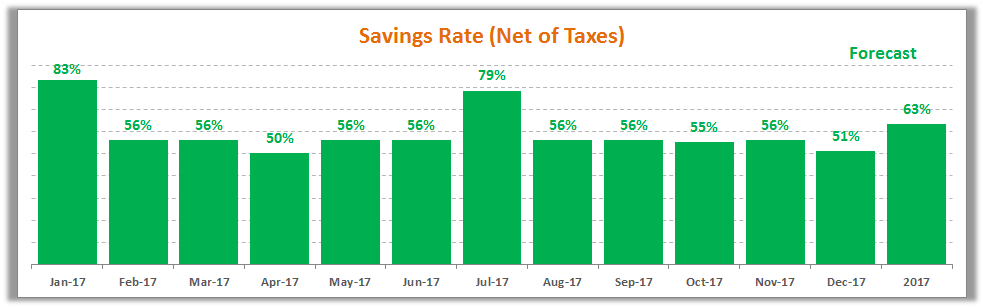

Savings & Savings Rate

Our total savings (net income + pre-tax savings + amortizations) is projected to be just shy of $200K at $195,759. As you can see from the chart above, our projected savings rate is 63%, which if achieved is a huge improvement from the 50% savings rate projected in 2016 (for context our savings rate in 2015 was 44%). This rate is always calculated based on after tax income.

The really exciting part is that our gross savings rate, which longer term we are aiming to save 50% of our gross income (not just 50% of after tax income), is moving up from 37% in 2016 to 44% in 2017. The driver here is the continued increase in our income, while our expenses remain relatively flat YoY.

Net Worth Outlook

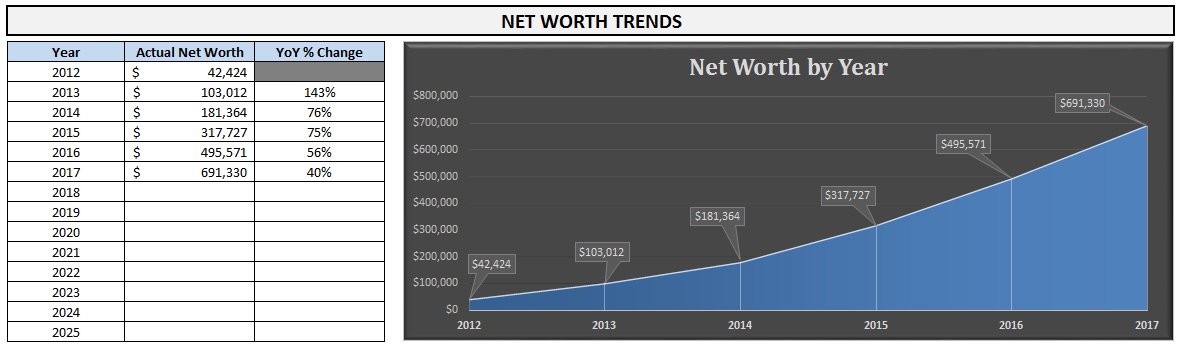

Did you notice the little section of the P&L that calculates our net worth by month and then YoY?

When we project net worth, we only include the increases that we are in control of; savings, new investment capital, and debt pay down. We don’t try to predict what our investments might appreciate or plan for dividends, 401K matches, windfalls, etc. That being said, the number is probably conservative, unless the market falls off a cliff next year.

We are expecting to grow our net worth by just shy of $200K in 2017 or 40%. To put things in perspective that is a CAGR (compound annual growth rate) of 75% between 2012 to 2017. The stretch goal will be to get it to $750K. I have some ideas on how to make this happen, but I am not quite ready to share these half baked ideas just yet.

Looking at the chart and how far we have come, there is a part of me that wants to take the time to go back an calculate (i.e estimate, because I don’t have as good of records prior to 2012) our net worth for 2009 – 2011, because at the bottom of the financial crisis we were close to NEGATIVE $330K IN NET WORTH!

During that time our condo (which we now rent out) was worth $160K less than what we paid for it (near the top of the market). I also foolishly bought a house at 19 years old (in 2007) that I ultimately let go to foreclosure that was $160K less than what I owed. I also had $13K in student loans. In less than 10 years (2009 to 2017 projected) that is just shy of a $1M swing (can’t be upset with that kind of improvement).

Well, that is a wrap. On paper, 2017 is looking to be another EPIC year!

Now its your turn. How is your 2017 shaping up? Do you have anything big planned? Everyone should spend sometime mapping out the year ahead, it is an eye opening exercise.

– Gen Y Finance Guy

10 Responses

Wow, that is a pretty intense spreadsheet for a family budget! But I’m sure after the one time setup it doesn’t take too long, especially since it sounds like you aren’t too worried about getting each individual category perfect.

The nice part about some of the home improvement stuff is it costs cash, but might not change your net worth too much as the home value will likely increase. It certainly varies by project, but compared to other expenses, home improvement is a pretty good one!

$200k in savings is nuts, congrats. You make me want to go out and earn more instead of wasting time on a blog. But I guess you do both, so I have no excuse…

Brian – It is a spreadsheet that has evolved. It all started in Mint and I created a spreadsheet that downloaded the financial data from mint and automatically populated the P&L. Then over time I added in the tax estimate calculations and net worth figures. Now all the data is pulled directly from Personal Capital.

Small correction but at your income you max out SS contributions so it doesn’t contribute to marginal rate.

Thanks for the clarification Taylor. I actually do have this cap built into my spreadsheet, but your comment reminded me to go and check the income level where this maxes out. In 2016 it was $118,500, but in Googling this I found out that it is increasing to $127,200 in 2017.

Well I’ve caught up! 😉 had to start with that, it’s been a journey and epic one at that..

On your post I must say I’m impressed on the granularity you’ve looked into here and as you say you can’t manage what you don’t measure right?

I’m sure it won’t be 100% although at the same time very few projections are and it’s then about adjusting

Thanks for sharing Dom! Sure you’ll keep us posted and some nice numbers here, looking forward to seeing your goals post for 2017 too

Nice job Jeff! I am pretty sure you are the first and only person that has read through the entire backlog of posts.

It’s just a guide with some goal posts. We blew past our income target this year by 30% and plan to do something similar in 2017 (you will see what I am talking about when I share my 2017 goals).

Cheers Dom, not a massive achievement although I certainly enjoy and have learned and been inspired by a thing or 2

Awesome, sounds good and looking forward to it!