As long time readers, many of you have picked up on the fact that I am a big believer in setting goals and long term visions. This is exactly why I share my annual goals and monthly progress in achieving those goals. It’s also why I shared my own blueprint in achieving a net worth of $10M and $600,000 in annual income.

When you put together a 20 year vision, you have to accept that lots of variables can change along the way. Today, I really want to zero in on the income side of this 20 year vision to $10M in net worth. First, my income assumptions have been absolutely blown out of the water, and we are much further along at just shy of 20 months into the plan.

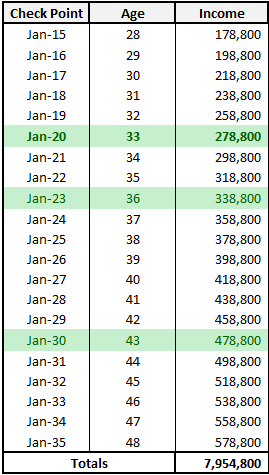

To the left is the income milestones that I had projected at the inception of the blueprint. In a recent update to the blueprint, I pointed out that we had completely blown our income projection for 2015 out of the water.

To the left is the income milestones that I had projected at the inception of the blueprint. In a recent update to the blueprint, I pointed out that we had completely blown our income projection for 2015 out of the water.

In 2015 we finished the year with $254,359 in gross income or 42% higher than projected ($178,800 projected).

We are now 8 months into 2016 and at this point we have very good visibility into what our ending income will be. In the July Financial update, I shared that we were now forecasting to finish 2016 with $315,000 in gross income. Again this is 58% higher than projected ($198,800 projected).

Before we move into expectations for 2017, let’s first put this into context. We are going to finish 2016 6 years ahead of the plan, earning what we projected to be earning in 2022.

THIS IS ABSOLUTELY MIND BLOWING TO US!

On the flip-side, this goes a long way in showing what is possible when you put you mind, energy, and focus to a vision. The subconscious goes out and figures out how to make it a reality. I have also recently learned that the subconscious doesn’t really have the ability to decipher time.

A few months ago, I shared on the blog that I was up for promotion to VP, which quickly turned into a promotion to the C-Suite. This is another one of those variables that is hard to plan for (at least the timing of it). Well, I now know that this will happen by the end of 2016, and with it comes another huge boost to earnings. I am currently projecting a $117,000 increase in total compensation in 2017.

This puts our projected gross income for 2017 at $437,000 or 100% higher than projected ($218,800).

MIND FUCKING BLOWN!!!

This will move us 12 years ahead of schedule to an income level we had not projected until 2028 when we were 41 years old. We are incredibly grateful for the opportunities we have been afforded, but also realize that there has been a lot of hard work to earn those opportunities.

At the rate things are currently moving, we should reach an annual income of $600K by 2018/2019.

Everything is great…or is it?

Heavy Concentration Risk in Day Job

I won’t deny that our income and career trajectories have far exceeded our wildest expectations. Some days I wake up and wonder if the last two years had all been a dream. It’s not a dream, it is reality. But there is another reality that we seriously need to start thinking about.

That other reality is that we have a lot of risk to our income due to it’s concentration in a few sources. We also have the majority of our income coming in the form of earned income vs. passive income. If Mrs. GYFG were to lose her job, our income would fall by 27% in 2017. If I lost my job, our income would fall by 68%. If you do the math, this means that we only have 5% of our income that is passive (100-27-68 = 5).

Although I think the probability of either of us losing our jobs next year is very low (let alone the next 5 years). It doesn’t change the fact that the prudent thing to do while our income is growing so rapidly, is to aggressively start putting that money to work to create additional cash flow that is not tied to our day jobs.

We need to do a better job of converting our earned income into passive income streams.

Another Consideration: Tax Efficiency

Many of you reading this are already aware of the rule that governs our financial life, and that is the law of 50/50. The basic’s of this principle is that we aim to save 50% of our after tax income and spend the remaining 50% guilt free.

That said, we have a longer term goal to actually save 50% of our gross income (a much harder milestone to reach). This is where tax efficiency really comes into play. The more your earned income grows, the higher your marginal tax rate. Based on our $600K annual income goal, this lands us in the highest federal tax bracket of 39.6% (assuming it’s all earned income). We also have to consider state taxes here in California, which based on the $600K goal, lands us in the 12.3% tax rate (since it’s under a million, we are clear of the 1% surcharge).

When you add that up, our marginal tax rate will be 51.9% on earned income. This would put our effective tax rate somewhere in the 35-39% range (depending on deductions, exemptions, and credits).

Let’s assume for a moment that all $600K comes from earned income. At an effective tax rate of 35% we would pay $210,000 in taxes, need to save $300,000 (based on 50% gross savings rate), and would have $90,000 remaining for living expenses. The math doesn’t work, as we currently need approximately $110,000/year to maintain our chosen lifestyle.

And at a 39% tax rate, we end up paying $234,000 in taxes and would have only $66,000 left over for living expenses.

Note: For illustration purposes (and simplicity), deductions are ignored. Also the numbers are all ball park, so please just take them as close enough.

That means that in addition to diversifying our income streams, if we want a chance at hitting our gross income savings goal of 50%, we are going to have to start focusing on creating passive income streams through more tax efficient vehicles.

Now this is not the first time this has entered my thoughts, but I am starting to feel the pressure to take action in this area.

And it all keeps pointing back to investing in Real Estate and potentially other more tax efficient assets.

Conclusion

We really need to start putting our earned income to work in order to create more tax efficient cash flows. This will help us accomplish two things:

- Diversification of Income: I would like to increase our passive income from 5% to 25% over the next 3-5 years.

- 50% Gross Income Savings Goal: We need income that is subject to lower tax rates to make this goal achievable, especially knowing that we have no interest in lowering our living expenses. In fact, we believe we have hit the sweet spot with the amount of money we spend to live the lifestyle we desire.

I have been talking about it for a year, but I think the next step is really working towards getting a 3rd piece of real estate. We just got word that we should be getting the $50,000 we loaned out as a hard money loan by the end of September, when escrow closes. We have one more refinance on our condo that we would like to finish in January of 2017, that we were unable to complete earlier this year, but have taken the necessary steps to make it happen in early 2017.

We don’t expect to be required to bring in very much money to get the refinance done on our investment condo. Back in April, it was looking like a $14,000 cash-in refinance to get the right LTV (loan to value). Property values have continued to rise, and we will have had another $4,000 in principal reduction by January of 2017. So, at the most I see this costing us $10,000 (mostly paying down the existing balance, maybe $1,000 in total closing costs at most).

January 2017 will also be a big bonus month for me. By the end of January we should have close to $155,000 of cash ready to deploy (after accounting for refinance).

We have come to accept that we are not ready to execute on another property in 2016, there are just far too many things going on, and the holidays will be here before we know it.

2017 will be the big push in moving us in the direction of more passive and tax efficient income.

What would you do? What other tax efficient assets should we be considering besides real estate? Any tax professionals that read the blog, that have any advice on how else to reduce our effective tax rate?

-Gen Y Finance Guy

25 Responses

Don’t forget that the Medicare tax on income is 1.45% (and isn’t capped, like social security), plus you begin to pay an additional 0.9% tax on earned income over $200,000. This means your marginal rate is 54.25%, so you are absolutely incentivized as much as possible to find ways to shelter that money.

I think your best bet is going to be making sure every retirement account is maxed out (i.e. 401k, HSA) and that you’re reducing your taxable income as much as possible (transit subsidies, deductible expenses for the blog, etc.).

The next step would be to shelter as much income as you can from the blog (i.e. open up a separate retirement account).

All in all though, it’s not a bad problem to have. Looking forward to hearing more about your thoughts on using real estate to reduce the tax drag.

Thanks for the reminder Josh!!!

That is just nuts, how can the government justify getting more of the income I earn than I get to keep myself? And if you really go deeper, for any of that money that gets spent, it will be taxed again in the form of sales tax. So, let’s use your 54.25% marginal tax rate. That means that for every additional dollar I earn the government will get 54 cents and I will get 46 cents. But then let’s say I go spend that 46 cents of something that includes sales tax of 8% (based on where I live). That really means that dollar in terms of spending power to me is really only worth 42 cents to me.

My 401K and HSA both get maxed out automatically.

We do have deductions that do bring out taxes down, but I ignored those to really drive home the point of the post (that I have a concentration and tax issue that needs attention).

Your right, taxes are a good problem to have, sometimes they are just annoying.

More to come on my thoughts on real estate and tax efficiency.

Cheers

Man 600k in income.. I just know that you’re going to get there, which makes me jealous 😉 great plan, GYFG! The taxes might be awful but that’s the extra price of a higher income, right?

Thanks Finance Solver!

Taxes are certainly a direct result of higher income…but just need to make sure I am not leaving money on the table by not optimizing the situation. I want to pay the least amount legally allowed by the tax code (as should we all).

Don’t forget tax loss harvesting on your taxable investments. It may be capped at $3,000/year, but if your effective tax rate is 35%, that’s $1,050 extra in your pocket for the year.

I’m not sure if your job (or you) would ever consider it, but what about asking if they’ll move you to a 1099 status (or if you set up a business and they paid your business)? Typically in this setup, they would pay you even more (Most contractor rates are 50% to 100% of W2 salary). You’d be responsible for self-employment taxes, but you could easily put $53k/year into a Solo 401k, and write off a lot of other stuff. Home office, fuel, vehicle maintenance, etc. I’m not sure if you could make it work, but if your wife worked part time for your business, she might be eligible for spousal contributions to the Solo 401k. I know it’s a long shot, but I’m just tossing ideas out there.

Sorry, I meant to say 50% to 100% more than W2 salary.

Hey Kevin,

Thanks for the ideas. So, far I don’t have any tax loss harvesting to take advantage of, which I think is a good thing. But will be sure to take advantage of any deductions I can take advantage as a result of investment losses in after tax accounts.

It’s funny you mention the 1099 idea, as I had tried to get my wife set up that way with her families business…but there is something regulation wise that makes that not possible.

Not sure if my company would go for the 1099 status or not. We definitely have consultants that are treated with 1099, but if they work for us long enough we require them to convert to an employee. At this time I am not sure why, but sounds like a conversation I should probably explore with our VP of HR.

Cheers

Just curious GenY, how much do you consider your real estate to be passive?

Obviously, you can dive deep into the rabbit hole here, but in order to be truly accurate, you’ll probably want to start tracking the hours you spend working on your real estate investments. It’s likely that you will have a lot of hours on the front end but hopefully very minimal on a month-to-month basis.

Also, are you planning to hire a maintenance person and/or a property manager to further reduce your time and increase the “passivity?”

Just don’t forget that traditional real estate isn’t truly passive! 🙂

Hey Nick,

We used to do the property management ourselves on our investment condo, and as you suggest it takes a lot of time.

We decided about 3 years ago to hire a property manager, and it has been the best $100/month we spend.

All we do is cash the check every month. In the last 3 years we have spent maybe 5 hours total.

In the event there is any repairs or maintaince that needs to be performed we have the property manager coordinate that for small things. In the event there is a bigger issue my father in law is a contractor.

So, the simple answer to your question is that I consider it to be VERY passive.

We will set up any future investment properties the same way. Yes, it eats into the cash flow and the return, but the trade off is worth it to us.

The front end time commitment is really just searching for the next property, which we have an agent that is doing the heavy lifting there.

Then it’s getting through the financing and Escrow. Should there be any rehab work needed before renting it out, our agent has a team in place, as he flips about 30-50 houses a year.

Aside from the passive nature it also serves several other purposes. Diversifies our income. But also lends itself to more favorable tax treatment.

Cheers

Oh wow, that’s quite the setup!

It really ia basically passive in that way.

Congrats!

I believe the regulation you’re talking about has to do with the 1099 income being her only source of income. If that’s the case, she should be classified as an employee. The way around that is for her to form a business and for her family business to pay her business. Then it becomes a business to business transaction, rather than her being an individual contractor that should be classified as an employee. If you set up a business with yourself and your wife as 50/50 partners, your wife’s family business could pay your new business for her services and your company could pay your new business for your services. Then both of you could contribute $53,000 per year to a 401k if you each take a $140k/year salary, contribute $18k/year each, and do a company match of $35k/year each (25% of your salaries), which is the 2016 maximum allowed. You would of course be responsible for your own taxes and your own health insurance, but done correctly, it may work out very much in your favor. Obviously, consult with an accountant and verify there are no special regulations and all that. Also speak with your company about that.

Hello GYF,

I’ve been reading your blog for a few weeks now. I love it. First time I comment here.

600 k$ is a massive income forecast. I love the fact that you are able to believe in that. I cannot yet put such numbers in my forecast (hopefully one day I will be). Believing is the first (and imo the most important) step to achieving.

What I am really interested in is :

1) What strategies did you and your spouse use to grow ranks and income in your company this fast. My main objective right now is to grow my income from my job. Would love to learn from you on this topic.

2) In forecasting the 600k$ income: how do you approach this? Do you extrapolate or do you already have a step by step plan or idea on how you are going to achieve that number?

Keep up the great posts. It is truly inspirational.

Hey Steven – Thanks for the comment. Yes, $600K is an insane number, it felt much further away when I first set it in early 2015, but now seems much more achievable.

Re: Your Questions

1 – My wife took an opportunity to go and work for her mom’s escrow business back in 2013. At the time she had to take a $30K pay cut to do so, but she knew that if she performed that here earning potential would be far greater than the $30K she had to give up in the short term. Fast forward 3 years and she is now earning almost 3X what she was earning when she first made the move. It has involved a lot of long hours in and out of the office. She has had to do a lot of networking to build up her book of business. Success in her business is not only cyclical, but it is very much a relationship business.

For myself, I was never the smartest, but I was determined to get ahead of my peers by outworking them. For the past 8 years since graduating college, I have put in 70-100 hour weeks almost religiously. Not all those hours are always at the office or working on the day job specifically. So when I wasn’t working, I was spending my time in personal and professional development. Learning new skills to increase my value with my current employer and the market at large.

I was never shy to ask for a raise when I felt I had added enough value to merit it. Most people settle for what they are given…not me. I never worked to get 3-4% cost of living adjustments. Instead I worked to add value that was 10X that, in order to get raises that were 10X the average. Since 2003 my income has grown at a compounded 37%. I have always believed that if you do what average people do, then all you can expect is average. But if you want more than you must become more (i.e personal & professional development).

When my friends were at happy hour I was still at the office. When my friends were in Vegas for the weekend, I was learning new skills. Even when I was on vacation, you would be hard pressed to find me without a stack of books and a bunch of audio to get through.

You have to have an insatiable appetite for learning and growth. I too identified and networked with the people I knew could have the most influence on my career. You have to remember that if you help enough people get what they want, you will always get what you want.

You don’t have to be the smartest person in the room, you just need to be the hardest working. Over time the power of compounding will make you stand apart from your peers. I highly recommend you check out the book the .

.

Slight Edge

It is the one book that has had the most influence in my life.

2 – How did I arrive at a $600K forecast? Well, back in 2015 when I first put the forecast together, I had our income growing $20K a year. Based on history, between my wife and I, we had always managed to do this, so I thought that was a reasonable assumption. However, as you read in the post above, I am now forecasting the $600K in the next couple years.

Being in Finance, I have the benefit of knowing the compensation for every single employee in the organization. Therefore I have a bit of an advantage of knowing the compensation ranges for my new level in the C-Suite. And in all honesty I actually think I can exceed the $600K, but because there is a lot that can happen over the next few years, I am not banking that just yet.

Hope this helps.

Cheers

Wow!

Thanks so much for taking the time to write this down and share with us. I’ll definitely get a copy of the “Slight Edge”.

Much appreciated!

25% passive income is a great goal. With passive income though I think it is important to consider two things though: capital appreciation and time.

If you put $100k into an investment that pays you $1k a year in passive income, awesome you increased your passive income. But if you are just returned that $100k of capital at the end of the year, the investment overall sucks. $1k very passive, but no capital appreciation means it returned just 1% overall. My conclusion is that even though you are going for passive income in real estate, you should still use leverage to better take advantage of the capital appreciation (even if you put 50% down).

Given that you use a property manager for a local rental, you know how valuable your time is. Often people get their investments confused with a side job. Both are great, you can have something that straddles both lines, but don’t run investment numbers without taking into account the labor you put in.

Hey Brian – I totally agree that capital appreciation and time should absolutely be considered. I am not looking to take on a second job.

I am almost done with a custom real estate financial model that I will be sharing on the blog soon. It is based on a 10-year projection with many different input variables (appreciation being one of them).

Cheers,

Dom

Congrats on the $600k. We are in a similar situation (income-wise and also live in California) and we also hope to increase our passive income this year. I’m trying to do so through blogging. I just have to get traffic up to bring in the dollars!

Hey Julie – Well the $600K is not in the bag just yet, but it seems like it is well within arms reach.

You doing anything in particular to get the blog traffic up? Are you focusing on affiliate income or ads?

Cheers

Wow! I love your enthusiasm! Sometimes the biggest thing we need is motivation apart from anything else, best of luck! And you’re right with a large income proper tax planning is crucial.

I’d love to hear a post on your process of how you’ve gotten to the role you are now.. Although I know there’s the letter you sent to the CEO, I feel breaking it down would be fantastic..

Have you considered options like lending club, more stocks, bonds? (sure you have although thought I’d throw in options there)

Looking forward to seeing you continue to grow! 🙂