What a year 2019 is shaping up to be. Life never ceases to amaze or surprise me. Specifically, I started thinking about starting a consulting practice back in the summer of 2016 and almost secured some work back then. However, the timing wasn’t quite right. The idea was put on the back burner until it was brought back to life in June of 2018, with a discussion during a trip to Toronto of becoming a third-party consulting partner for a software company I know very intimately. Five years ago, I implemented their software at the company I work for, which automates and streamlines the Financial Planning & Analysis functions of an organization (among many other functions). It’s a great software, and I worked hard to master and implement it. Flash forward from that Toronto conversation: After nine months of due diligence, negotiation, and evaluation, I officially created my own consulting company and began work.

During the past nine months, this same company also tried to hire me, but I decided that creating my own business was the best route for both me and it. I also pitched this new business idea to the company that currently employees me but ultimately decided that it was best to go at it alone. I decided that I didn’t want to give up 80% of the upside nor have the pressure of having private equity involved. Frankly, the initial billing rates I’m getting right now aren’t that appealing to private equity anyway, and I’m okay growing this much more slowly than they would have pressured me to grow it. Private equity investors aren’t interested in investing in lifestyle businesses, which is really what I’m looking to create.

Parallel to all this, I was offered the COO job by my current employer. Technically I accepted and am in an 18-month transition period before officially taking on the role. I accepted this as my back-up plan in case the consulting business didn’t work out. Until I’m ready to push the eject button I will continue to pursue both tracks. It’s crazy to think I’m considering (actually pretty much decided) that I’m going to walk away from a $350,000 comp package (current) that has potential to increase to $600,000 or more as I assume the COO role over the next 18 months. I’m willing to do this because I honestly believe that the business I’ve started has that same potential and more.

At some point, I’m going to need to initiate a conversation with my employer about my change of plans. But that is going to wait until I hit a few more milestones, which will give me the confidence to have that conversation. I won’t show my hand too early. I have a hard time seeing a possibility where I do both and maintain any sort of personal/family life (not an option). I will continue to share more details here periodically as things develop in real time.

With that, let’s dive into the nuts and bolts.

If you’re a regular reader and only want to read the new content, feel free to just skip the intro below, and head to Net Worth. If you are new or haven’t read many of these reports, I encourage you to take two minutes to read the intro below, which does change periodically.

Why I Share These Monthly Reports

Mission Statement: To Humanize Finance, Build Wealth, and Reach Financial Freedom.

For those of you new around this corner of the internet, these monthly reports are about full transparency. And, they are just as much for me as they are for you. It was a hard decision to make all of my financial details public, but it has proved to be a very motivating one. The process I go through every month to produce these reports has been enlightening and life-changing. I published my first “income and net worth report” for January of 2015 when our net worth was only $195,141, and our gross income was on pace to hit $178,000 that year.

A little over four years later, our net worth currently clocks in at $1,110,940 with a gross income over the trailing twelve months of $447,422 (peaked at $475,914 in January 2019).

- That’s a 5.7X increase in net worth due to a compound annual growth rate of nearly 50% for the past four years.

- At the same time, income has increased 2.6X, which translates to a compound annual growth rate of roughly 25%.

Honestly, I don’t think the GYFG household would have experienced these kinds of results without the existence of this blog and the accountability it brings. Knowing that I will share our results with you readers every month keeps me very focused and intentional with all things related to our financial well being. For that, I THANK YOU for taking the time to read and interact with me on this blog.

Above and beyond this benefit to my own household, my sincere hope is that my policy of full transparency will inspire you to take the helm of your own financial ship and be intentional with its direction. I truly believe that anyone can reach financial freedom if he or she is willing to do things differently than the pack. If you’re after average results, then you’ve landed on the wrong site. There’s nothing wrong with average, but the kind of results I preach are EXTRAORDINARY. Sure, the “get rich slow” method is proven, but there is an alternative, which is to “get rich fast.” Look, I have no interest in living like a starving college student until I am old and brittle to only then have the means to check off bucket-list items when my body might no longer be physically capable of doing them. And I don’t want that for you either!

Here at GYFG, we approach the pursuit of FINANCIAL FREEDOM with an abundance mindset, so you won’t hear me telling you to cut out those $5 lattes. Choose to spend on what is meaningful to you. I spend a lot, but I also strategically earn a lot, save a lot and invest a lot.

I hope these reports inspire and move you to action. Don’t take a passive role in your finances and hope for the best. Keep this famous Jim Rohn quote in mind:

“If you don’t plan your future, somebody else will. And you know what they have planned for you? NOT MUCH!”

You must be intentional with your finances if you ever want a fighting chance to make it to financial freedom. But it does not have to take 40-50 years of slaving away for The Man before you have the option to retire. I think 10-20 years is all you need, with the most aggressive folks probably able to reach financial freedom in 10 years or less. A high income paired with a high savings rate are two of the vital components of a good recipe for the 10-year track.

I know I don’t have to publish my juicy details every month, but it’s important to me that you know that I put my money where my mouth is (not so many people giving financial advice actually do this). I publish all of my financial details not to brag, but instead to show you what is working as well as what’s not working. Sometimes finance can get pretty dense, and I think real life examples and numbers can help slice through the complexities (and BS). Personally, I have always enjoyed the financial reports put out by other bloggers around the blogosphere, so I always intended to share my own.

You can find all my previous reports on the Financial Stats page.

Net Worth

Our April net worth was up $10,885 or 1.0% vs. March. Year-to-date our net worth is up $98,075 or 9.7% vs. December 2018. And if you look year-over-year our net worth is up $356,756 or 47.3% vs. April 2018. The music continues to play and the party goes on! From a net worth (and income) perspective, May could end up being a record month, with a potential 10% increase to net worth – let’s see how things shake out (timing could slip thereafter to June).

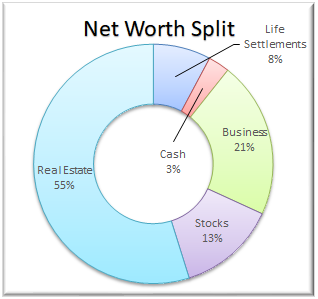

April Net Worth $1,110,940 (up $98,075 or +9.7% for 2019)

- Previous month: $1,100,055

- Difference: +$10,885

Net Worth Break Down (MoM):

The Real Estate ($609,275) category increased from 54% to 55%. This category includes the equity in our primary residence ($433,897), our investment in the Rich Uncles commercial REIT ($69,615), and our hard money loans through the PeerStreet ($105,764) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000 (which is why the PeerStreet value hasn’t been changing much MoM).

The Real Estate ($609,275) category increased from 54% to 55%. This category includes the equity in our primary residence ($433,897), our investment in the Rich Uncles commercial REIT ($69,615), and our hard money loans through the PeerStreet ($105,764) platform. I have been taking capital as it’s freed up from our after-tax PeerStreet account and using it to fund Rich Uncles as we work the RU account value up to $100,000 (which is why the PeerStreet value hasn’t been changing much MoM).

Net Cash ($32,128) remained flat at 3%. We actually have $42,563 in cash but net cash is only $32,128 after you adjust for our current credit card balance of $10,435, which we pay in full every month based on the statement due date. I started traveling again in January, so this will fluctuate a lot more going forward (and is compounded with the new travel related to the consulting business I started back in March).

{kind=link}

The Business ($234,962) category remained flat at 21%. This represents the ownership I have in the private company that I work for. This is an illiquid investment that only gets an update to its value one time per year. I net the company stock asset value of $446,962 against the company stock loan of -$212,000 to arrive at the $234,962.

Life Settlements ($86,586) remained flat at 8%. We currently have investments in seven policies at $10,000 each. They are accreting in value by about $1,000 per month. For anyone that is familiar with options, I liken the fixed return of life settlements to the theta of a short option. In this case, the accreted value is like the theta decay of an option you’ve sold. In more simple terms, with this fixed return you are amortizing (realizing) that value with the passing of time.

The Stocks ($147,988) category remained flat at 13% and represents the cumulative value of our brokerage accounts (all retirement accounts) that are invested in stocks. However, this is not all of our retirement money, as the majority of our PeerStreet investments are made through a self-directed IRA (worth about $80,000 and are counted in the Real Estate category of the pie chart).

The value of our Cars is no longer being tracked as a part of net worth.

Total Capital Deployed in 2019:

I anticipate deploying about $182,000 in new capital this year (of which 44% has already been deployed). Although a healthy sum, this is down significantly from the $414,692 that we were able to deploy in 2018. Going forward I expect there to be a lot more month-to-month variability in the capital deployed. About 65% of the total deployed this year will go towards putting the mortgage to bed (we only have $29,999 remaining on the mortgage).

You can see that I deducted the $50,000 from the stocks category due to the 401K loan that I took to apply against the mortgage. I know that may not be a popular move but it makes sense to us given our goal of paying off the mortgage and our opinion of the current market environment. This way, we locked in current gains and paid off debt, without inciting a large tax event. Based on our cash flow we can have the 401K loan paid back by the end of 2019, but the speed at which we pay it back will depend on what the market does and if/when I leave my current employer. It’s technically a five-year loan but I seriously doubt we will take that long to pay it off. In the meantime, we will be paying ourselves interest at a rate of 6.5% (the mortgage debt we paid off was at 2.25% so the net interest rate is 4.25%).

Gross Income

Income for the month of April was $27,134 vs. $26,324 in March. On a cumulative basis, we have earned $140,000 through April of 2019. We are currently behind where we were at this time last year when income through April 2018 was $168,324. A big driver here is a slowdown in real estate sales, which has translated to no escrow commissions for Mrs. GYFG (accounted for $5,000 to $8,000 a month in compensation last year). This could be another warning sign of an eventual recession – only time will tell.

That being said, I was pleasantly surprised in March to find out that I would be receiving an 18% dividend payment from the stock I own in the company I work for. This equates to a $50,000 to $60,000 payment. On top of this, May is a three-pay period month for me, so it has the potential to be our first ever six-figure income month.

In the second chart above, I also track our income on a trailing twelve months, and as expected the TTM dipped further to $447,422. That now puts us $28,492 off pace of the all-time high of $475,914 set in January 2019. The good news is that if the stars align we will crush the record set in January 2019 with a TTM of well over $500,000!

Savings Rate

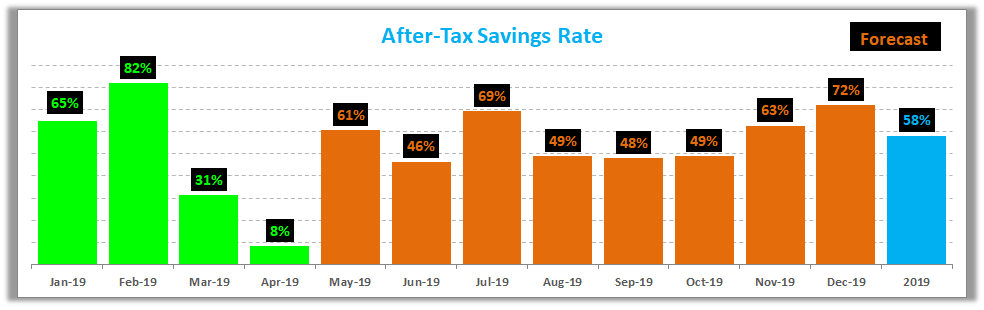

Below is how we actually did vs. our goal of saving 50% of our after-tax income. In the chart below, the green bars represent our actual savings rate for the month, the orange bars are what we anticipate based on our 2019 budget, and the blue bar is the projected savings rate for all of 2019.

Last month I said:

“March is a little misleading in that it is artificially low due to the timing of some reimbursements in travel expenses for work. At the end of March, I had almost $3,000 in expenses that hit the GYFG P&L and no offsetting reimbursement. Accordingly, I expect April to be higher than the 48% shown below.”

Boy, was I wrong! You will notice in the below chart that not only did we not exceed the 48% target for April, but we also missed it by about 1,000,000 miles. I have some explanations for this:

(1) Although I was reimbursed for some outstanding work-related travel, I still have about $4,000 that was not reimbursed within the month of April (timing).

(2) Mrs. GYFG and I decided that we wanted to rent a beach house for Father’s Day weekend and had to pre-pay $3,000 for this (see the incredible view in the pic below).

If not for these items, we would have had a savings rate of over 60% for the month. Again, May should be a blowout month, and should more than offset the miss in April (anticipated in the range of 80-90%).

Do you want to calculate your own savings rate? I’ve made it super easy for you with the savings rate calculator included in the free GYFG FI Toolkit that you can download instantly by clicking the link below. Here’s a peek below. Did I mention it’s free? You have nothing to lose and everything to gain, Freedom Fighter!

Speaking of savings rate, go check out my post where I mathematically prove the importance of your savings rate as a higher priority in achieving financial independence than your compound return. If you’re trying to build wealth quickly, then you have to read this post.

Mortgage Early Payoff Goal

After several refinances, our mortgage is a 3/1 ARM at 2.25% and we currently owe $29,999. We had originally set a goal to pay it off in seven years and three months but recently accelerated that timeline by a few years. In the progress bar below you will notice that we were originally working towards a goal completion date of 1/31/2022, but are now aiming to have this goal completed by 7/31/19.

For the past few years, I have been writing about the desire to avoid concentration risk and ensure diversification, and therefore not rush to pay off our mortgage. But in June 2018 we decided to go after this goal hard and fast. Why the change of heart? The first major driver is the fact that our income has grown far faster than we had ever imagined in our wildest dreams. Based on the 20-year plan I shared on the blog back in 2015, our income wasn’t projected to hit current levels until 2031 – that puts us 11 years ahead of schedule.

Secondly, prior to the 2018 tax reform, the tax benefit we received from being able to deduct the interest and property taxes was already minimal. And now, under the new Federal tax reform, there is zero tax benefit (due to SALT limit and the increased standard deduction to $24,000 for a married couple which is greater than our itemized deductions). I still don’t understand how anyone could be dogmatic about keeping a mortgage for the tax deduction, which is worthless under the new tax reform for most households across the USA.

Moreover, why would you spend a dollar on interest to get thirty cents back? Why not pay zero interest and keep 70 cents out of each dollar that you don’t have to pay towards interest? Our lightbulb moment came when we realized that we could get this pay-off accomplished in about a year, which became very motivating once Baby GYFG arrived. This gives us a very strong financial foundation from which to spring into our next phase of life, and wealth-building.

This acceleration means that the equity value in our home will be growing rapidly over the next six months, as will the percentage of our net worth concentration tied up in this asset. It currently makes up 39.1% of our net worth (up from 38.5% last month), and I anticipate it will make up as much as 40-45% of our net worth between now and pay-off. With the unexpected windfall in May, we may even be able to pay this off an extra two months early (within the month of May).

So close, I can taste it!!! And it tastes GOOD.

The original philosophy of this plan to pay off the mortgage was to accomplish this goal while avoiding any austerity to our lifestyle. I coined it the “pay more tomorrow” plan. In keeping with the GYFG emphasis on the income side of our financial equation, I projected that we could easily increase our income (after tax) by at least $9,600/year and dedicate that additional income to fund the goal effortlessly. This has proved to be not only true but also very conservative. To date, we have paid down the mortgage by $325,001 in four years (and four months). It’s crazy to think that we will be mortgage-free a little less than five years from setting this goal.

This goal is now 91.5% complete (vs. 88.7% in March)!

Closing Thoughts

As mentioned in the last few monthly updates, I plan to leave on the financial autopilot I set before the end of last year until the mortgage is paid off. At that point, I will become a bit more active in managing our personal finances. Currently, all my excess bandwidth has been spent getting my new consulting business off the ground. As of April 30th, I billed out ~$25,000 (of which ~$15,500 is mine to keep). Now I just have to wait to get paid (this figure is not included in the income for this report). I’m really enjoying this new business so much that I’m now working on a plan to exit my day job and go full-time entrepreneur. Always in planning mode! If you have ever read my about page (note the last bullet point), you will see that this has always been a goal of mine. Until now, I hadn’t found the right opportunity that provided more upside than I could get from working for someone else. But now…pretty excited to say that I may have.

I hope you had an Amazing April!

– Gen Y Finance Guy

8 Responses

I am with you on building a business at the same time accepting a position with a company with (relatively) big upside. About 2 months ago I accepted a position at an employer near me that improved my work-life balance but a year ago I decided to take a crack at my own business. It’s a mental struggle to balance the two along with two kids plus life. I am up for the challenge – at least that’s what I tell myself. I always liked juggling and that’s what I’ve been doing. I’ll be paying attention to your updates on how balancing both goes…some days I feel like a rock star when I’ve handled it all like a boss, some days I’m just really tired and miss concentrating on one thing at a time. Here’s to hoping more of the former in the future!!

Won’t you have to pay back the 401(k) loan if you leave your employer? Doubt that will be an issue but just flagging for you.

Yes! It will not be a problem to pay it back. I’m currently targeting a 2/28/20 exit, so that is the soonest I would have to pay it back and aligns with when we had planned this pay it back by.

Thanks for flagging it just in case.

Wow, a six figure month. That must be nice!

Also, the beach house pic looks great. Where are you renting? I’ve been trying to figure out good beach locations to rent a summer house.

Hey Rich,

Yes, May has indeed shaped up to be our first six-figure month. It’s a bit surreal! The beach house is actually in Oceanside, Ca.

Dom

Kind of funny that a few year’s back after reading your blog on paying down a mortgage I do started the same thing. My last statement was $14,000. Looks like this summer it will be $0. My $300,000 condo will be owned outright. At this point I will probably accelerate the pay down a bit faster on my second home. Recently sold all my SP500 stock and made a lump sum. Takes a bit of time, but still knocked it out in under 10 years. Thanks for the motivation and insight…I might never have started it

Congratulations, Dave! We just made our final payment in May and it is an amazing feeling to be unshackled from that huge debt. I still think it is going to take time to fully set in, since our accounts should really start to swell through the rest of the year. We have paid an average of $17,000/month towards them mortgage for the last 18 months.

Come back and celebrate when you make that last payment.

Cheers,

Dom

BOOM!!!