Happy New Year!

Beginning this month, the GYFG post format has changed – specifically in how I write it. For the prior 71 monthly updates, I would sit down at the end of the month and write it in one fell swoop. But I’ve decided to write this post incrementally throughout the month, for four reasons:

(1) It helps me break it down into more manageable writing sessions.

(2) I want to start treating this monthly update more like a digital “newspaper” of my life (mostly financial, but not entirely).

(3) This new format will allow me to capture and reflect on more throughout the month (faster feedback loop).

(4) It will also allow me to share mini-posts (articles) within the main publication (newspaper). Examples below include Business Spotlight, Tax Optimization, 2020 Reading List, and 2021 Goals.

I hope you enjoy the new format.

With that said, I would remind everyone reading that even with the new format this is still only the highlight reel. I say this not because I’m inauthentic in my writing but to remind everyone that I’m still just a regular human being with struggles and faults. I’m excited by my highlights and grateful for them, but I guess I want to make sure that you don’t put me or anyone else you follow online on a pedestal. I did not get to the markers written about in this post in a day…or a year. I’ve been at this with concerted focus and massive effort for many years. My goal in sharing these highlights every month is to humanize finance and be a source of motivation and inspiration by sharing the habits and philosophies that have proved very effective in my own life. You get to choose what you adopt or ignore.

Let’s dive into the details of this month’s update!

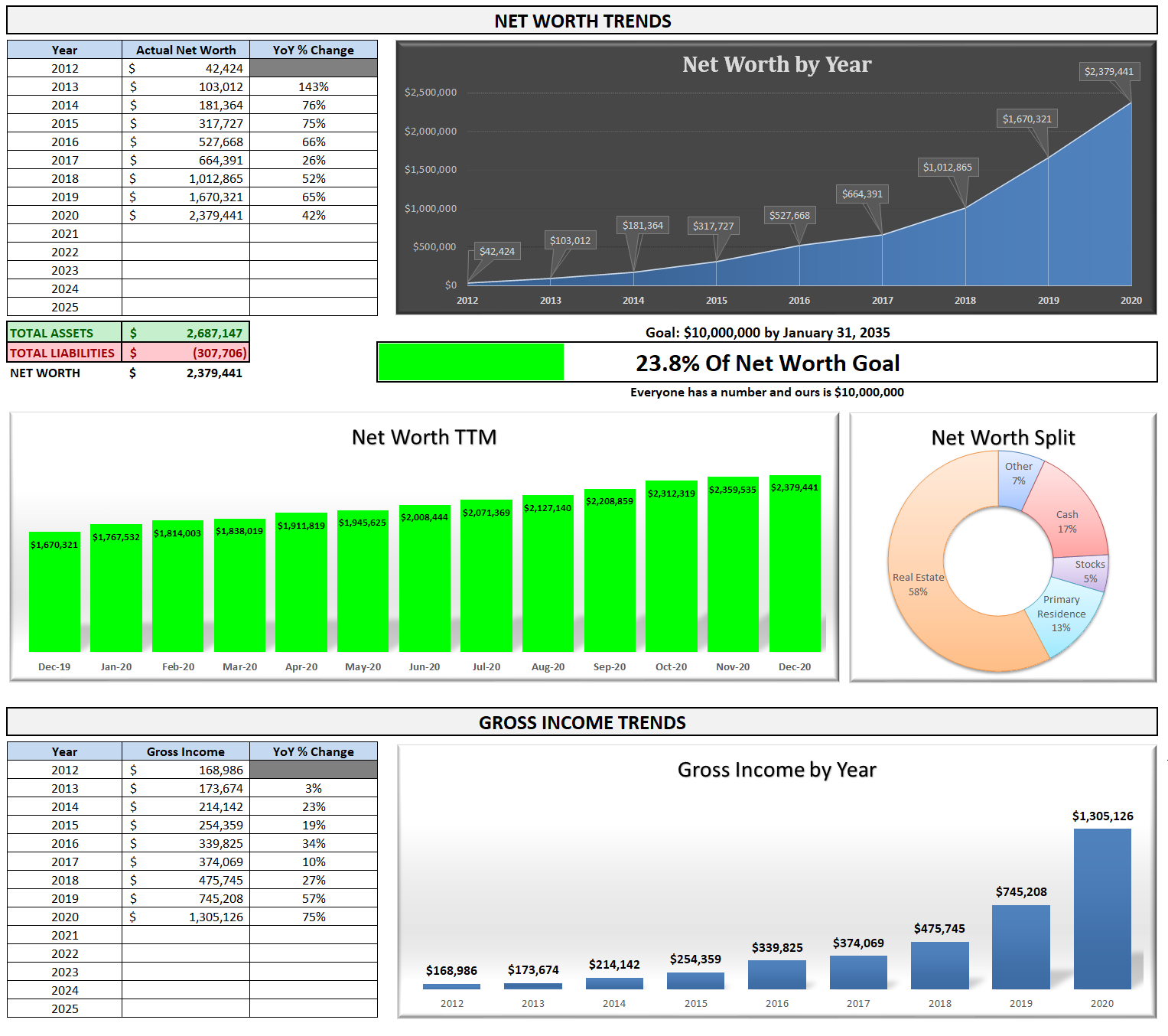

Financial Dashboard

I remember when I first created this financial dashboard back in 2015 and how that first update I shared had us at less than 2% of the way to our $10M goal. Here we are, six years later, at almost 24% of the way there. The most astonishing thing to me is the compound annual growth rate (CAGR) we have been able to maintain since 2012. Our income has grown at a robust 29% CAGR. Even more mind-blowing is that our net worth has been compounding at a 65% CAGR during that same time period.

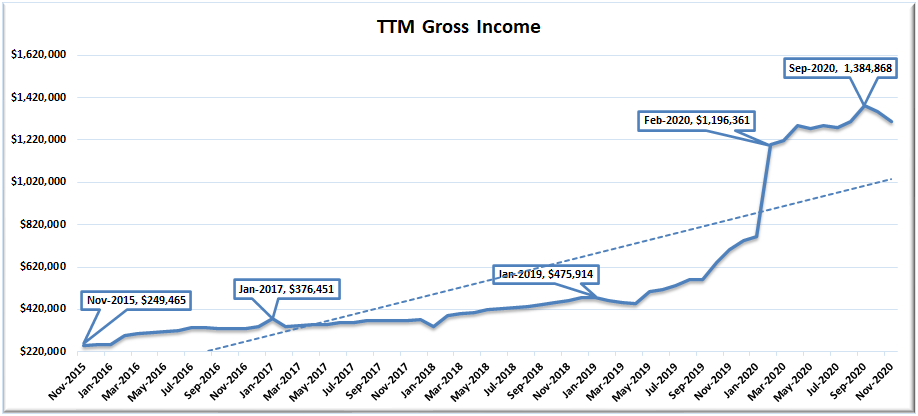

TTM Gross Income

The income figure I like to track most is our Trailing Twelve Month (TTM) gross income. We have had a very good run since 2015 but recently hit a peak in September 2020 that I think will be challenging to exceed in the short term. We have a pretty large cliff coming up in February, which will be the last month that the $415,000 gain I realized from selling the shares I owned in my previous employer will remain in the TTM range. I do expect income in Q1’21 to be very robust, but there is a chance that our TTM dips below seven figures for a short time. We finished 2020 with a final TTM of $1,305,126.

I don’t expect anyone to feel sorry for us as I know that our income has grown to a level that is no longer relatable to most readers. I do, however, hope that my transparency continues to be motivating and inspiring to others that follow along. For further context not showing in the chart above, my starting salary out of college was $52,500 and Mrs. GYFG’s was $35,000.

Based on what I currently know, I have our TTM income at December 2021 projected at $1,062,000 but will be working hard to finish north of our previous all-time high of $1,384,868 set in September of 2020. I only need to find an additional $323,000!

Net Worth:

Current Net Worth: $2,379,441 (up $709,120 or +42.5% for 2020)

Previous month: $2,359,535

Difference: +$19,906

Note: I’m still not holding a value for my business in my net worth. Depending on the multiple you use, the value of my business is somewhere in the range of $500,000 (1X) to $2,500,000 (5X). I’m hesitant to hold a value in my net worth for this until we achieve a liquidity event.

Net Worth Break Down:

Real Estate (58%) – This category no longer includes the equity in our primary residence. This is a mixture of private placement deals, equity, debt, and crowdfunding.

Primary Residence (13%) – I decided to split this out on its own because it is something I do want to manage separately from our overall holdings in Real Estate. Our primary residence currently makes up 13% of our total net worth (down from 23% in September) due to a cash-out refinance (locking in 2.8675% for 30 years) that put a mortgage back on the property. I expect the concentration to continue its downward trend until we move into our new house in October of 2021.

Net Cash (17%) – We currently have $408,000 in cash vs. $625,000 last month. As you will read in the deployments section below, we deployed $165,000 in December into investments. We also bought new appliances in anticipation of the kitchen remodel in our future home. We withheld significantly more for taxes as a final move in tax planning for the year.

Alternatives (7%) – This is a catch-all category that captures our investments in the following: life settlements, a special purpose acquisition company (SPAC), and a private investment in the Robinhood trading platform (I recently read that Robinhood is looking to go public in 2021, which could be a nice liquidity event, but mine is a small investment of $10,000).

Stocks (5%) – We have $1,000 that is being invested weekly with Betterment.

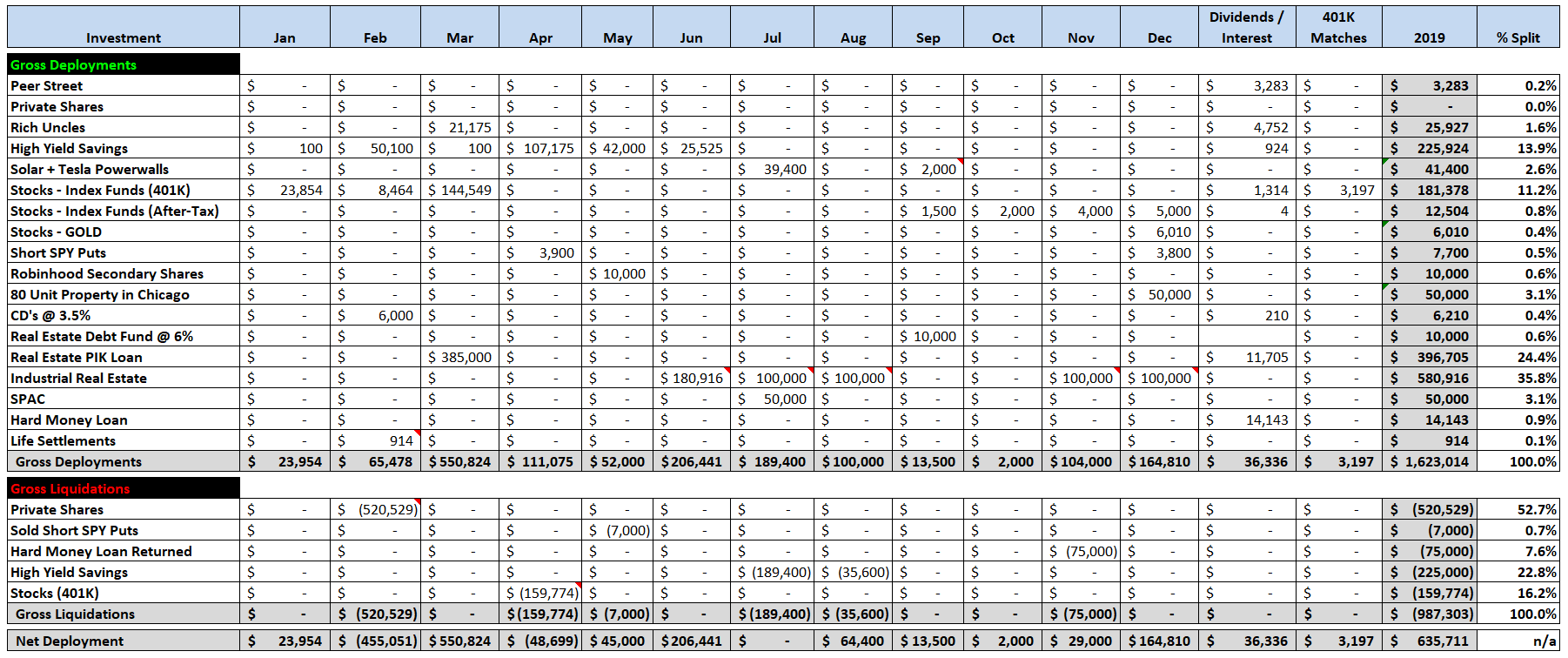

Total Capital Deployed in 2020:

This month we deployed $5,000 into stocks via Betterment and another $100,000 to increase our investment in a previous real estate investment. Besides very favorable economics, the other driver in deploying an additional $100,000 into this specific deal is the fact it is in an opportunity zone and so it allows us to defer capital gains taxes on the gain realized from selling the stock in my previous employer (see tax optimization section below).

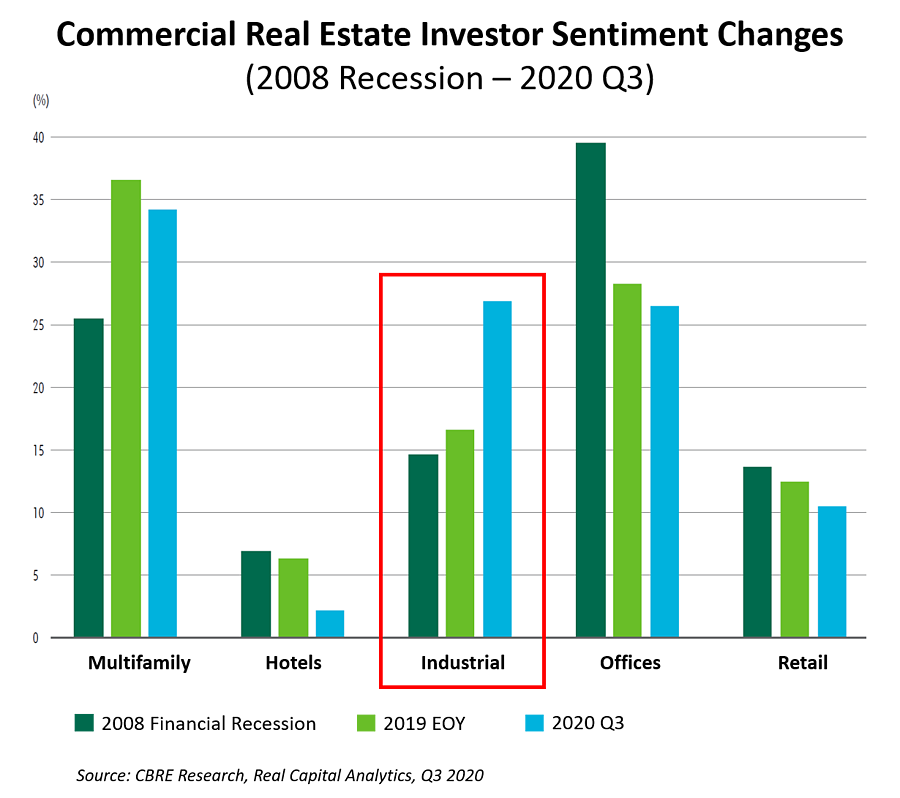

Our Dividends and Interest more than doubled from the $16,573 that we received in 2019. Based on the investments we have made this year we expect this year’s $36,336 to grow to around $150,000 when all our investments start cash-flowing. The largest part of this cash flow will be coming from the $480,916 that we deployed into an industrial real estate deal with anticipated cash-on-cash returns of ~25%, or annualized cash flow of $120,229, which we expect to start cash-flowing in the summer of 2021. (See the chart from CBRE below on Industrial Real Estate.)

This has been a much busier year in terms of capital deployments than I had anticipated but I think I have said this every year since sharing this section. We plan to take a breather for the first four months of the year until we get through tax season and shift our focus to replenishing the cash war chest and the house remodel ahead of us. The only investments we will be making will be the automated stock investments from our 401(k)s and our weekly deposits into Betterment.

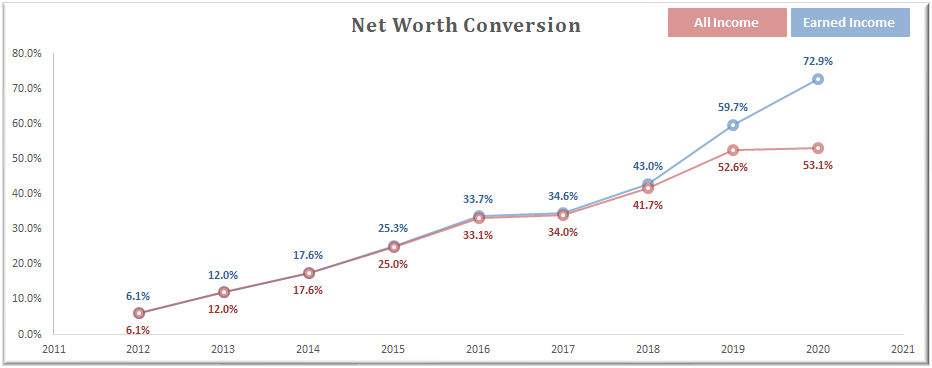

Net Worth Conversion Ratio

Definition: The Net Worth Conversion Ratio measures an earner’s ability to convert earned income into wealth (net worth). It excludes passive income since passive income is dependent on the earner’s decision of putting earned income to work or spending on consumption.

This is a new metric I will be updating and sharing monthly. Now that “the machine” is in full production, it is time to not only bring back the net worth conversion metric but to make it a star of the show. I once wrote that financial nirvana is reached once this metric exceeds 100%. When I first calculated this back in early 2016 the GYFG ratio clocked in at 25.3%. Since then we have significantly increased our savings rate and the gravitational pull of increasing both our savings rate and income helped us significantly improve the performance of this metric, which now clocks in at 72.9% (down slightly from 73% last month).

You will notice that I have shared the metric based on both ‘earned income’ and ‘all income’ but I’m most interested in the earned income calculation (per the definition above).

This Month

The goal the past five years since adopting this metric was to focus on increasing our earned income while simultaneously saving at least 50% of our after-tax income in order to create excess capital for investing. I should note that I’ve excluded from the ‘earned income’ calculation any income that’s derived passively from investments and more recently profit distributions from my business (I do include the W-2 income I earn as an employee of the business). That said, I do include the same metric on ‘all income’ as a point of reference and differentiation.

The end goal is to get to a point where net worth is 100% or greater than earned income – bonus points if the same thing can be accomplished based on all income sources.

Business Spotlight – Taking advantage of Geo-Arbitrage to hire talent

Prior to COVID, I had always intended to build a 100% remote business. We live in the digital age and technology has removed the need for dedicated office space where everyone congregates daily to pay homage to the almighty Ant Hill (vis-à-vis Corporate HQ or Corporate offices). There are three major benefits to building a remote business:

(1) Operating costs go down significantly without real estate costs (rent, utilities, etc.).

(2) No wasted time commuting to and from said offices. This also creates the ability to not just “work from home,” but truly “work from anywhere.” This optionality is super valuable to me.

(3) Geographical agnosticism when hiring talent. Talent can be sourced from not only all around the country but really from all around the world – assuming timezones are not an issue, but even if they are it still opens up a HUGE talent pool. This also has the potential to access great talent for significantly less than hiring someone in an expensive local market.

In my business I now employ people in the following locations:

- California (4 team members)

- Texas (2 team members)

- Toronto (3 team members)

- Ukraine (3 team members)

- Columbia (1 team member)

My business has realized both significant cost savings and access to really talented people by being remote and geo-agnostic. My end goal is to build a business that leverages both onshore and offshore talent and to pay well relative to the location of each specific team member. Yes, this is really good for the profitability of the business but it also provides security as we continue to build the large gap between our revenue and our expenses that would allow us to have a significant slowdown and still keep everyone employed. It also leaves plenty of room to fund fun company events to celebrate our successes together.

Tax Optimization

When it comes to building wealth there are three levers you have at your disposal:

- How much you earn

- How much you save (earnings less taxes and spending)

- The rate of return on your invested savings

I’ve listed the levers in the order of prioritization for the GYFG household. I realized early on that a high income was the fastest path to reaching financial freedom but only if paired with a robust savings rate. Your savings rate is driven by two main variables: spending and taxes. Back in 2015, we adopted the law of 50/50, which took care of the spending variable. This simple rule states that we save 50% of our after-tax income and spend the remaining 50% guilt-free. You’ll notice there is nothing in there about minimizing taxes.

It’s not that we didn’t consider taxes; we did, and we took advantage of the obvious tax deferral strategy available to us at the time – maxing out our 401(k)s. We also eventually switched to a high deductible health plan that allowed us to max out an HSA account. We began slowly investing with a goal of shifting the mix of our income from nearly 100% ordinary income taxed at the highest rates to other forms of income that would be taxed more favorably.

Frankly, it wasn’t until two years ago that our income had grown so much (our marginal tax rate had exceeded the 50% mark – approximately 52%) that I was motivated to level up this part of our situation. That meant finding a really good CPA and an attorney that could expose me to the strategies available to legally minimize our taxes. I had a hard time justifying paying the government $52 out of every additional $100 that the GYFG household worked hard to earn.

With that preamble out of the way, I would like to list what the GYFG household has done the past two years to optimize our financial lives to pay the legal minimum in taxes.

– Max out 401(K)s. Since we have two gainfully employed adults this allows us to contribute $39,000 based on the current max of $19,500 per person in 2020.

– Max out the HSA. You have to be on a high deductible health plan to take advantage of this, but in 2020 this allowed us to shield $7,100 from taxes.

– Land Conservation. I wrote about this in my October 2019 financial report whereby I bought a deduction that cost $68,600 in order to get a $343,000 tax deduction. That equated to about $150,000 in tax savings based on my estimated income for the year at the time. Well, I fell short of the estimate and ended up rolling $141,000 of that deduction from 2019 into 2020.

– Started an S-Corporation. When I started my business in February 2019, I started as a sole proprietor in order to keep costs low, with the goal of transitioning to a corporate structure once the business proved itself viable. A corporation is much more tax-efficient than a sole proprietorship. This shift has had a huge impact on the tax efficiency of my personal life as certain expenses that were previously personal expenses and paid for after-tax dollars are now business expenses paid with pre-tax dollars. In addition, the profit distribution from the company is not subject to FICA taxes. My CPA’s job is to make my personal life as tax efficient as possible by ensuring I convert as many personal expenses into legal business expenses per the IRS code.

– Investing in Opportunity Zones (<read about opportunity zones here). I first wrote about this in my June 2020 financial report. This allowed me to defer taxes on $300,000 worth of capital gains (until December of 2026) that were a result of cashing out of my former employer’s stock. The benefits of investing in an opportunity zone are threefold:

(1) To defer taxes on realized capital gains. Typically, 180 days from realizing the gain are allowed to deploy the capital in an opportunity zone, but this year, due to COVID, the deadline was extended to 12/31/20 even if this date was after the 180-day expiration. It’s a lot like doing a 1031 exchange based on the timeline given.

(2) Tax basis steps up based on the duration money is kept invested in the opportunity zone, thus reducing the deferred taxes. From the article linked above “a taxpayer who defers gains through an Opportunity Zone Fund investment receives a 10% step-up in tax basis after five years and additional 5% step-up after seven years. Note that to take full advantage of the 15% step-up in tax basis, the taxpayer must have invested by December 31, 2019.” So, based on this, as long as I hold my investments for five years, in 2026 when the deferred taxes become due, they will be on $270,000 instead of $300,000 due to the 10% step-up in basis (I’m too late to take advantage of the additional 5%).

(3) Finally, if held for 10 years the appreciation from the investment above and beyond the capital gain rolled over will not be taxable at all. AMAZING!!!

I don’t know the exact amount all this saved me but I know it is in the ballpark of $250,000 to $300,000 in tax savings for 2020 alone. Let’s just say that the ROI on paying a few thousand dollars for professional advice/service from my CPA and Attorney combined has been astronomical. It wasn’t until 2019 that I fully appreciated why the wealthy spend money on good CPAs and attorneys.

Note: if you’re wondering how I arrived at a 52% marginal tax rate, this note is for you. Based on our income we fell into the highest federal tax bracket of 37% as well as the highest California state tax rate bracket of 12.3% (there is also a 1% surcharge on all earnings in excess of $1M). On top of that is the 2.35% tax for Medicare, which has no cap on earnings (it’s 1.45% until earnings exceed $250,000 if married).

2020 Reading List

Before starting this section of the post, I didn’t realize I had read as many books as I did until coming up with my top 15 list (links below). I read 32 books this year!

Personal Finance Books

- The Psychology of Money

- The Wealthy Gardener

- The Leverage Equation

- How I Invest My Money

- Tribe of Millionaires

Personal/Professional Growth Books

Business Books

- It Doesn’t Have to be Crazy at Work

- The Harder You Work The Luckier You Get

- Demand Side Sales

- Trillion Dollar Coach (listened to audiobook)

- Trailblazer (listened to audiobook)

- The Ride of a Lifetime (listened to audiobook)

- What You Do is Who You Are (listened to audiobook)

Entertainment/Fiction

Other Books I read/listened to that were ok: Peak, Retire Early with Real Estate, Becoming the Iceman, The Happiness Curve, Thinking in Bets, 7 Powers, Choose FI: Your Blueprint to Financial Independence, Extreme Ownership, Limitless, Miracle Morning Millionaires, Build Live Give, What it Takes

Books I re-read this year: Rich Dad’s Guide to Investing, Rich Dad’s Cashflow Quadrant, Rich Dad Poor Dad, The Black Swan, The Subtle Art of Not Giving a F*ck

Note: I had read the Rich Dad series when I was in college and decided to re-read the books (actually listened to them this time) to see if I got more out of them after ~15 years had passed. I was disappointed when I didn’t find them as exciting as I did the first time I read them. I’m guessing it’s because there wasn’t anything earth-shattering to me this time around since I have been knee-deep in all things finance since then (some books have a time and a place).

2021 Goals

Professional – Successfully complete my business coaching program I paid for and started in December of 2020. The benchmarks of successful completion of this goal are as follows:

- At least one sale within three months (average lifetime value to me of a client is currently running at ~$87K)

- Five sales in 2021 (Implied revenue of $435K on top of other channels of acquisition)

- Implement CRM (actually completed before this goes to press)

- Implement Project Management Solution

The coaching program is comprehensive, but for me, the focus or emphasis is on the sales component. My coach, Paul Higgins, had a 17-year career in sales with Coca Cola and then built and sold a services-based company. He is now a business coach. I decided to hire Paul because he not only had the sales and marketing experience I needed training on but also because he had done what I plan to do with building my company and eventually exiting it through some form of liquidity event. Even better is that Paul’s business model was very similar to the one I have created in that his company provided implementation services for a particular software and was also a reseller of said software.

Fitness – Achieve body weight of 210 pounds. My strategy to achieve this are as follows:

- Three Rounds of Beachbody workouts (i.e. P90X) per week

- Intermittent Fasting five days per week

- Limit alcohol to date nights or outings with friends

As I type this I am almost five weeks into my first round of P90X in over five years. I’ve shared snippets here and there but I’ve been on a long journey of recovering from a back injury back in early 2016. While on my break at the beach in November, I went through ten sessions of Rolfing, which has absolutely changed my life. December was the first month I have had zero pain in over three years. I wish I would have found Rolfing shortly after completing my non-surgical decompression program in 2018.

I’m back to doing things that I haven’t been able to do in years.

Family – More Connection Time

- Four weeks of vacation

- Two date nights per month

- Pick my son up early from daycare once per month

- Read two parenting books

My wife and I have decided to be very diligent about booking vacations for quality family time. I also have learned that I now require more frequent breaks from the business to stay fresh and energized. It’s better for me personally, it’s better for the team (trust me), and it’s better for the success and growth trajectory of the business long term.

In Q4 of last year, I had set a goal of picking up my son early from daycare one day a week, but I wasn’t successful at making that happen. Managing the growth of the business has been more work than I realized. Every new level of growth requires me to take on new roles. I’m working hard to continue bringing on help to offload these new roles once I find stability. My current focus is building out the sales and marketing function. Prior to this, my focus was building out the operations – the consulting function that delivers the implementations I sell – while also taking on all sales activity personally. Now that I have a solid operational team, I’m building out the sales and marketing team.

All that said, I’m stepping back my goal to one time per month until I get more foundation laid in making the business more self-sufficient without my daily presence. It’s a long game!

While I work through the growing pains of building a business, these goals will help me stay connected with my family by taking breaks from the business…which can too easily become all-consuming with my personality. I have constantly been reminded of the post I wrote a while back: Don’t Get So Consumed Building Wealth That You Forget To Build A Life (just as applicable to building a business, which plays a big role in achieving my wealth-building goals).

Closing Thoughts

I’ve got mixed feelings about 2020 overall. No doubt it has been a challenging year for many who lost their jobs and maybe even lost loved ones to the COVID-19 virus. Many have had to adapt to a much more limited way of life due to restrictions, shutdowns, and social distancing. But I also see many silver linings in one of the most challenging years my generation has ever had to face. I’m in awe at the speed at which we have developed not one but three vaccines to fight this virus (and the implications of future use cases the scientific community is already discussing). We’ve accelerated trends that have been in motion for years if not decades to reach important inflection points, one of which has always been important to me and that is the ability to not only work from home but to work from anywhere.

I’ll admit that my personal day-to-day life was not affected much by the pandemic, at least not compared to others that I know. I was already working from home almost exclusively besides the 4-6 days a month that I was traveling to client sites – something I don’t miss nor do I plan to bring back as a regular part of our service offering. Instead, traveling to a client will be provided at a premium if clients want that in-person aspect. We have also been fortunate that our son’s daycare has remained open throughout all of the craziness. It’s our social life that has been impacted most, which comprised many weekends prior to COVID. We do miss going out with friends and even going out to dinner as a couple or family – we have ordered in and cooked a lot more.

Business-wise and Financially it has been an incredible year for the GYFG household.

That said, we are certainly looking forward to returning to a new normal as vaccines are distributed and we get COVID under control enough to begin lifting all the restrictions we have been living under for most of the last nine months.

I wish you all a happy, healthy, fulfilling, and more normal year ahead.

Cheers!

– Gen Y Finance Guy

p.s. next month I plan to revisit the original 10-year letter I wrote to myself, an update on our $10M blueprint, and a peek into our growing passive income streams.

9 Responses

Truly inspiring! My wife and I, income wise, are comparable to your 2015 year. I have no idea how to ramp up further from there. Any classes you took or books read that inspired you to turbo charge your income growth?

Thanks, DebtRebel!

A couple of books I read that inspired me back then are:

– The Slight Edge by Jeff Olson

– Linchpin by Seth Godin

– So Good They Can’t Ignore You by Cal Newport

It’s those along with the other 30-50 books a year I’ve been reading since 2012. I also exposed myself to a lot of blogs written by high net worth and high income individuals.

There is a quote I’m constantly removed need of from Jim Rohn and that is “that your levels of success will rarely exceed your level of personal development.”

I hope that helps.

Dom

Happy New Uear! Congrats on a great 2020! Considering the high income taxes in CA have you considered moving to 0 income tax state (Nevada, Wash, TX FL)?Your income and business income makes you a great candidate for geoarbitrage. We are moving to Wash St this summer for that reason. Good luck and have a great 2021!

Thanks, Mike!

We have discussed moving to a zero state income tax state, but we have too many ties here with friends and family. That said, as I mentioned in the post I have a great CPA and Attorney helping me save a ton on taxes.

I wish you well on your own move this summer.

Dom

GYFG, fantastic wrap-up. You are a good story-teller (that is a compliment, of course you write what is true and you always come correct!) which makes me look forward to reading your journey. Thanks again for sharing it with us.

Am happy you are keeping up with reading, and am always on the lookout for reading ideas. Two books have come from you in 2020, ‘The Wealthy Gardener’ and ‘Own the Day’*. I just put ‘Greenlights’ and ‘Becoming the Iceman’ on my list. I also enjoy(ed) when you came upon an article that you found worthwhile, so feel free to share those in 2021! One thing I was surprised to learn recently is that 1/3 of all book sales now are audiobooks. Apparently people have caught on to the idea of utilizing ‘dead time’* and podcasts are also surging in popularity. Interesting. I read 66 books (and didn’t finish 16) in 2020, and have 71 on my list which I keep as a living document. Average score on a 10-scale for the 66 is 7.4, and I now stop reading books that are boring me for whatever reason. I’m utilizing the ‘sunk cost fallacy’ to utilize my reading time better. A book I really enjoyed this last year was Tilman Fertitta’s “Shut Up and Listen!: Hard Business Truths that Will Help You Succeed” Dr. John Sarno’s ‘Healing Back Pain’ book, and recent documentary about him ‘All The Rage,’ are both recommendations for anyone with chronic back distress.

Great goals for 2021, am rooting for your physical progress and hope you continue to feel better. Awesome year for you, wishing the GYFG family and all my fellow readers a great 2021!

Hey JayCeezy,

I appreciate the kind words as always. Your comments are always something I look forward to reading. I’m glad I could help add to your list. For ‘Greenlights’ I really recommend the audiobook as Mathew personally reads it. I read a lot of articles, but most of the time it is during ‘dead time’ as you call it from my phone and I forget about saving the links. One day, when I have more time I would love to share more of the things I find interesting. I do plan to share the podcasts that are currently dominating my personal airwaves in case that may be of interest.

Like you, I have started to stop reading books that don’t do it for me. I used to suffer through a bad book, but not anymore. I think I gave up on 5 or 6 books this year – full disclosure, ‘Becoming the Iceman’ was one of those books that I stopped halfway through. I think Wim Hoff is an interesting guy but the book was just okay. I will check out your recommendations for both books and the documentary.

I wish you a happy, healthy, and prosperous year!!!

Dom

I like the way you put that, Dom. “I only need to find an additional $323,000!” So many of us think that six figure incomes is unattainable that they give up before even starting on it. By thinking in your way, we look for ways to get there instead of feeling discouraged that we might never get there.

There’s plenty of money out there for our taking, we just gotta go and find it.

I’d say the book Millionaire Fast Lane is a great motivator for someone in your position of owning his own business.

Yep, that was a good book. I read that a couple of years ago, maybe time to dust it off 🙂