If there is ever a time to turn to the great Oracle of Omaha it’s in times of market volatility. Warren Buffett reminds us as investors that “It is wise to be fearful when others are greedy and greedy when others are fearful.” This goes against human instinct, as most of us panic in times of crisis – we do the exact opposite of Buffett’s advice and panic-sell out of our investments. But one of the biggest lessons I’ve learned from reading every single shareholder letter Buffett has ever written is the importance of doing a whole lot of nothing for long periods of time.

Like Buffett, I’m constantly looking for my “margin of safety” when evaluating opportunities for capital deployment, which reminds me of another Buffet quote: “The best chance to deploy capital is when things are going down.” A lot of selling has happened these past few weeks. At its recent lowest, the S&P 500 was down ~30% from its all-time high. This market volatility paired with (driven by) the COVID-19 virus outbreak has a lot of people fearful and in full panic mode. Yet, I find myself licking my chops as I have been in de-risking mode for the past few years.

The concept of looking for a “margin of safety” in investments is what ultimately helped me develop my own philosophy of viewing all investments and capital deployments through a lens of risk mitigation first. Due to my risk mitigation approach, I have been positioning my family’s financials to be in a position of strength for the eventual market downturn. I wanted not only to be positioned to take advantage of market turbulence but also able to secure my family’s lifestyle before I took the leap of faith to start my own business. I didn’t want any pressure to have to make money to pay the mortgage or other bills.

So, five years ago I developed several rules to guide my family’s financial decisions, to put in place a solid financial foundation. These rules were put in place to maximize our optionality and decouple our daily decisions from financial pressures that typically dictate the actions of most people’s lives.

The Rules

- The Law of 50/50 – This law has been the linchpin to our financial success over the last five years. The law says that we must save 50% of our after-tax income but are free to spend the remaining 50% guilt-free.

- Aggressively Grow Income – I realized early on that extreme frugality was not for me and my family. I also realized that focusing so much on the expense side of the equation put me in a mindset of scarcity, rather than a mindset of abundance. The reality is that there is a floor in how low you can cut your expenses but no ceiling in how much you can increase your income.

- Eliminate all Debt – Debt reduces options…and I want maximum optionality. My wife and I have carried very little consumer debt over our financial lives. We have had a few car loans, but have never carried any credit card debt or other consumer debt. And although many will argue that mortgage debt is good debt, I think it still handcuffs you. I won’t argue against the position that over a long period of time you are likely to do better financially by carrying a mortgage and investing the difference you could have used to pay it down early, but I will argue that most will never do that. I personally wanted to be mortgage-free as it is a big part of my financial freedom plan. Again, I’m optimizing for optionality and I never want to be at the mercy of someone else because of debt. That’s why as I type this my family has absolutely zero debt with a net worth as of February 28, 2020 of $1,815,003.

- Risk Mitigation First – I view all investments and capital deployments through a lens of risk mitigation first. This requires being very patient and doing a whole lot of sitting on my hands. It also requires a contrarian personality. My actions over the years of writing on this blog may come across as being very risk-averse but my results show the upside of my strategy. Plus, I tend to make very big moves when I do make them. Sam at Financial Samurai once warned me (back in 2015) that one day I would feel the pressure to deploy capital more aggressively in order to hit my goal of $10M, yet I have yet to feel that pressure (all the while compounding my family’s net worth by ~60% per year since then). I make investments when I see asymmetric returns – opportunities that offer a risk of 1 to make 3 or more. This is why I like hard money lending so much, as I only invest in loans with a 60% LTV, meaning the property would have to lose 40% in value before my money is ever at risk of loss.

- Be Contrarian – Simply put, I don’t do it just because everyone else is doing it. Also, I’m not afraid to do things that may be unpopular. I chose to aggressively pay off my mortgage starting in 2015, completing that in May of 2019. The stock market had incredible gains during this time period, but my belief was that peace of mind and optionality would be worth the potential underperformance of the extra capital I plowed into paying the mortgage off. I have also always viewed a paid-off mortgage as a bond substitute as we have zero exposure to bonds, and bonds are thought to be a part of a well-diversified portfolio. Lastly, I believed that over the seven-year time horizon I set to pay the mortgage off that we could potentially outperform the stock market as returns reverted to the mean. I was also okay if I was wrong because I would still have a paid-off mortgage either way.

These are the rules whether explicitly or implicitly discussed and documented on this blog that have governed our financial lives these past five years. They will continue to guide us for many years to come. It is because of these rules that as everyone was piling on the risk for the past five years we were de-risking, and we now find ourselves in a position of strength to be greedy when others are fearful.

At the end of last month (2-2020), we found ourselves with $666,000 in cash and zero debt (beyond monthly credit cards we pay off monthly). I had also liquidated my 401k to cash back in November of 2019 in anticipation of both a market downturn and my eventual rollover from my previous employer’s 401k plan to my personal IRA. When you consider this additional $172,000 sitting in a money market, and an additional $25,000 sitting in another IRA, we really had $863,000 in cash – about 48% of our net worth. A great position to be in when the world and the markets are in full-on panic mode.

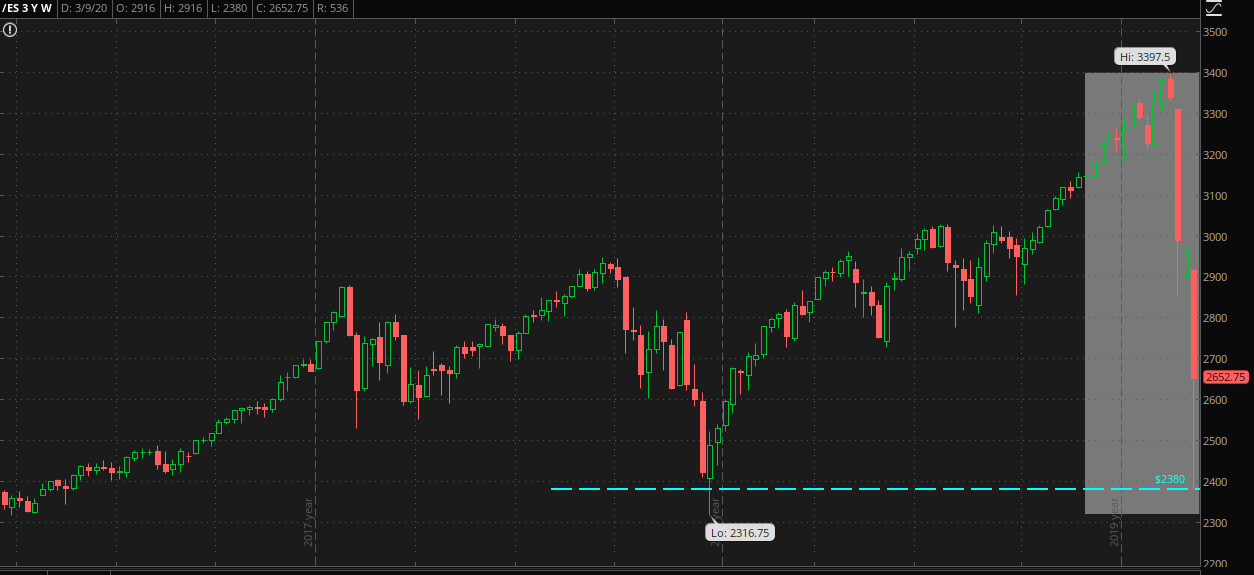

We saw the S&P 500 (and other major indices) hit lows this past week (on 3-12-2020):

From peak-to-trough the S&P 500 (futures) saw a total decline of ~30% – in a four week period. The price action was quite interesting and spectacular to watch as the markets melted down in a rapid clip. I began deploying capital once the S&P 500 was down 20% and continued as it moved towards its lows thus far. So far, I’ve deployed approximately $107,000 into equities (all this past week). Below are the investments I made:

- I purchased 200 shares of SPY at an average price of $253.58 ($50,716)

- I purchased 300 shares of LUV at an average price of $36.41 ($10,923)

- I purchased 500 shares of KO at an average price of $47.88 ($23,940)

- I purchased 1,000 shares of USO at an average price of $6.86 ($6,860)

- I purchased 100 shares of VTI at an average price of $146.27 ($14,627)

Total = $107,066

In the spirit of maximizing my “margin of safety,” I paired each of these purchases with calls sold against them, which is referred to as a covered call. In the past, I have said that I believe that every investor should learn two options strategies: the covered call and the short put. By selling calls against all of the stock I purchased, I effectively reduced my cost basis in each of those stocks and ETFs listed above, while at the same time capping my upside to 12% or higher. Here are the options I sold:

- I sold 1 call on SPY with January 2021 expiration and a $254 strike price for $29.26 ($2,926)

- I sold 1 call on SPY with January 2021 expiration and a $253 strike for $30.36 ($3,036)

Net Cost Basis on 200 Shares of SPY = $223.77 (34% below its recent high with a max gain of ~11.7% + Dividends)

- I sold 3 calls on LUV with January 2021 expiration and a $37.50 strike price for $7.70 ($2,310)

Net Cost Basis on 300 Shares of LUV = $28.71 (51% below its recent high with a max gain of ~24% + Dividends)

- I sold 5 calls on KO with January 2021 expiration and a $50 strike price for $4.33 ($2,165)

Net Cost Basis on 500 Shares of KO = $43.55 (28% below its recent high with a max gain of ~13.5% + Dividends)

- I sold 10 calls on USO with April 2020 expiration and a $7 strike price for $0.41 ($410)

Net Cost Basis on 1,000 Shares of USO = $6.45 (47% below its recent high with a max gain of ~8%)

Conclusion

If you have been reading this blog for any length of time and have adopted any of the philosophies that I’ve shared, you likely find yourself in a similar situation where you have dry powder to take advantage of the market turbulence. If you find yourself fully invested without any dry powder I do encourage you to consider the rules and philosophies that I have shared on this blog that govern my own financial life. During the Great Financial Crisis, I was just graduating from college and in no position to capitalize on the investment opportunities that presented themselves back then, but I vowed to be sure I would never be unprepared for an opportunity like that again.

I also saw people I cared about get absolutely murdered during the Great Financial Crisis, because they were over-leveraged, and lived a lifestyle that didn’t have a margin of safety built in. Not only did these people I care about struggle to keep the things they had, but they were in no position to take advantage of the sale of a lifetime. This is part of the reason why I am so averse to debt. Without that experience, I’m not sure if I would have the same beliefs and philosophies that I have today. However, I am grateful that I got to witness and learn from the past before ego and hubris got the best of me.

I know we are in the middle of some scary times but I continue to remain optimistic that this will pass and that there are still many decades of prosperity ahead of us. I just encourage each and every one of you to be prudent with your financial lives. If you are not where you want to be right now, use this as motivation to take the steps needed to build the financial foundation you desire.

I wish each and every one of you good health as we all take precautions to stop the COVID-19 virus in its tracks. Please remain calm and remember that this too shall pass.

– Gen Y Finance Guy

11 Responses

You say you capped your upside at 12% or higher. What is your downside exposure using these strategies? Are you protected from further declines?

Financial Verdict,

The downside like buying any stock is a drop in price below your cost basis. In these examples, my cost basis by selling calls was significantly below the current market price at the time of execution.

For example, one purchase I made last week involved buying 100 shares of the SPY index at $252.95, which was 25.4% below the all-time high set on 2/19/20.

When volatility explodes these premiums become very rich. I knew there was potentially more downside and I don’t believe this market is going to recover overnight. I saw that I could sell the January 2021 $253 call for $30.36 or 12% of my purchase price.

This gives me an effective purchase price of $222.59, which at the time was another 12% below the current price. My effective cost basis is still below the current market low of $237.07 that happened today (3/17 for this current down move).

So, I start seeing paper losses below $222.59 (assuming I hold to expiration, which I intend to do).

I also get to sit and collect the dividend until I’m exercised.

I rarely ever buy any stock (index or individual name) without selling/writing calls against my positions. I’m much happier capping my upside return for the reduction in cost basis. I favor a larger margin of safety over unlimited upside. I would argue that a covered call strategy is actually less risky than buying stock outright.

Dom

Interesting approach, thanks for the explanation. I am also considering starting to deploy cash to pick up a lot more equities, but I have not pulled the trigger yet.

Still monitoring the market, I think there may be more pain ahead. I probably will start adding in another week or so.

Ultimately I will go with buying stocks outright when I do. My philosophy: if you are going to sit out on the sidelines until a giant market move down, aren’t you looking for the significant upside that comes along with sitting on dry powder?

Financial Verdict,

My plan only needs to earn 5% returns for me to hit my financial goals, so if I can get 5% to 20%+, it is more than an acceptable return.

Additionally, my hypothesis is that the market is going to go lower and I won’t be able to time the bottom. Therefore by selling calls 9 months out to reduce my cost basis, I believe there is a high probability event that the calls will expire worthless and I will then just own the stock outright. But selling the calls now allows me to have an additional margin of safety now instead of waiting for a further move down (that I might miss). That said, if I’m wrong and the market recovers quickly, I will happily take my 12-20% capped returns and restore the opportunity fund (dry powder).

Dom

Good post and I like your overall philosophy of maintaining flexibility and optionality. Intuitively selling a put in this scenario also would seem to make sense if you know you would be a buyer of a particular stock at a lower price anyway.

I struggle with the idea of consistently capping your upside though on most of your equity purchases. I could see how certain scenarios make it hard to pass up, but as a general approach I wonder if it hurts your assymetric risk advantage in the long-run.

Isaac,

I agree selling puts at this point is a good choice but it is also synthetically the same position as a covered call (which is what I shared I was doing).

The thing about my activity is that I only get involved in the equities markets when volatility is high and premiums fat. That means I sit out on the sidelines a lot.

What is your biggest apprehension with capping your upside?

Dom

With so much volatility I’m getting into some options for the first time in years. Curious to get your thoughts on my preference for short-term covered calls instead of long-term. [Note this isn’t specific advice, just an example I looked up similar to your covered calls]

Today LUV with a +21% strike price (stock is currently 41.23, looking at 50 strikes):

4/17/20 (22 days): 1.04

1/15/21 (295 days): 5.70

I sure like the 22 day one, taking advantage of that time decay quickly. Then can just do another covered call next month.

Or maybe over the course of 22 days I’d think a 47.5 strike would be a good enough return (+15%) for a larger 1.63 premium. Repeat just a couple times to top the January 2021 covered calls.

What do you think?

Hey Brian – Yes, you are for sure going to get a much fast theta decay by selling options out with a shorter duration. The only risk is that the stock continues to tank and let’s say the first option expires worthless, but at expiration, the stock is now $30 a share. You will probably be less interested in selling a shorter duration option because the strikes worth selling are going to potentially lock you into a loss position if you are exercised. I was personally looking for a way to take advantage of the huge sell-off, capture volatility with fat premiums, and put a position on that was “set and forget” – with an effective cost basis that was significantly under the current price. I know I’m not good enough to try and call a bottom in prices. I also know that my personality changes when I put on short term positions like that…I get very obsessive and I don’t want to allocate that kind of mental bandwidth (it keeps me in investor mode selling further out, rather than short term trader mode).

I hate that Warren Buffet platitude only because I have read it 5,000 times in the last decade. haha