When it comes to wealth building, there are many variables to consider: the power of compounding is amazing, but it takes a long time to realize its true power. Income earning is certainly important, and so is its sister, annual income growth. Taxes paid matter. Time in the market is important, too, of course. Investment returns, which are the glittery objects that many people focus lots of energy on, do matter, despite the fact that you have absolutely no control over them. And then there’s how much you save. But which variable matters most? As I have stated in my monthly financial reports many times, it’s the rate of savings that doesn’t get the attention it deserves. This is especially true in the short run, and when you are trying to accumulate wealth as quickly as possible (20 years or less).

Overall, what are the variables that impact your ability to build wealth?

For me, there are six KEY variables that drive wealth creation:

- Annual Income (how much you earn)

- Annual Income Growth (at what rate your income increases every year)

- Effective Tax Rates (what portion of your income goes to taxes)

- Savings Rate (what is left over after taxes and spending)

- Duration (the number of years your money is put to work)

- Compound Annual Growth Rate, or CAGR (how much your money is growing every year, also know as returns)

It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for. –Robert Kiyosaki

For the most part, I think this quote by Robert Kiyosaki captures the wealth building process. Let’s break what he says down into bite-sized pieces…

“It’s not how much money you make”

It doesn’t matter whether you earn $30K a year or $300K a year if you spend every last cent of it. Without saving and investing you will never be wealthy. The reality is that there are plenty of high earners living paycheck to paycheck. The person earning a $300K salary may appear “rich,” but if he or she is spending all of it every month, it’s just a facade, a veneer of wealth. You must spend less than you make in order to have capital available to grow wealth.

Financial rule #1 is to spend less than you make!

“It’s how much you keep”

Remember the old saying “pay yourself first?” You do this by making sure that every time money comes your way you direct some to saving and some to investing before anything else. If you work for an employer and are offered a 401K or HSA, take advantage of it, as this is a way to pay yourself before Uncle Sam takes his cut. And save enough to get any employer match – that’s free money!

Financial rule #2 is to invest the difference wisely!

In optimizing how much you keep there are really three factors at play:

- Your Taxes – try to do anything and everything to ensure you are paying the minimum taxes legally allowed.

- Your Spending – remember rule #1, and spend less than you make.

- Your Savings Rate – This is what is left after taxes and spending. Surplus goes to either your savings account or investment account. This is where rule #2 comes into play, so make sure you invest the difference wisely. The lottery is not an investment! Well, maybe it is, but it’s not a very wise one.

“How hard it works for you…”

This is really just emphasizing rule #2 to invest the difference wisely. You want to put your little greenbacks to work for you. Start thinking about every dollar you save/invest as a soldier in your army. This is war, and you’re fighting for freedom: financial freedom, time freedom, and location freedom.

You want to put your money where it can appreciate and/or earn you cash flow (i.e. more income). It’s the best of both worlds when you can invest in an asset that does both.

Financial rule #3 is invest wisely so you don’t lose money!

“How many generations you keep it for…”

Duration is the key factor that determines the power of your compound annual growth rate (CAGR). The longer your money can stay invested, the more impact the compound rate will have in building your wealth.

Over the long term, it is compounding that will enable you to retire with wealth. Over the very long term, compounding makes it possible to leave a legacy long after you pass away for generations to come. But it takes decades!

Financial rule #4 is to leave your investments to work for the greatest amount of time possible!

Beyond the basics: why your savings rate matters most (and the math to prove it)

For some of you, the above might have been a review. For others, maybe breaking down the wealth building process into bite-sized pieces was enlightening. Either way, we can all benefit from a reminder of how wealth is created.

The review is our solid foundation. To drive home which of these six factors wields the most power, I’m going to use math and a few examples of different types of wealth builders.

Four Different Wealth Builders

- GYFG – Saves 50% of his income and would be considered an aggressive saver.

- Steve – Saves 5% of his income and would be considered the average American.

- Adam – Saves 10% of his income, which many financial planners tout as the sure path to wealth by age 65.

- Sally – Saves 15% of her income, somewhere in the middle of the pack.

We are going to walk through several different scenarios. Four assumptions will be held as constant:

- Taxes will be assumed at 25%.

- Duration will be 20 years.

- The wealth builders’ savings rate defined above will stay the same in all scenarios.

- Steve, Adam, and Sally are assumed to earn the historical market return of 8%.

- The only assumption that will change in each scenario will be the assumed growth rate that GYFG earns.

Chart porn ahead! Any Excel nerds besides me in the house? Of course there are unlimited permutations to this, but hey…it’s my blog! I chose the assumptions I did to keep this exercise on point.

Scenario #1: Static Income and 0% CAGR for our Super Saver GYFG

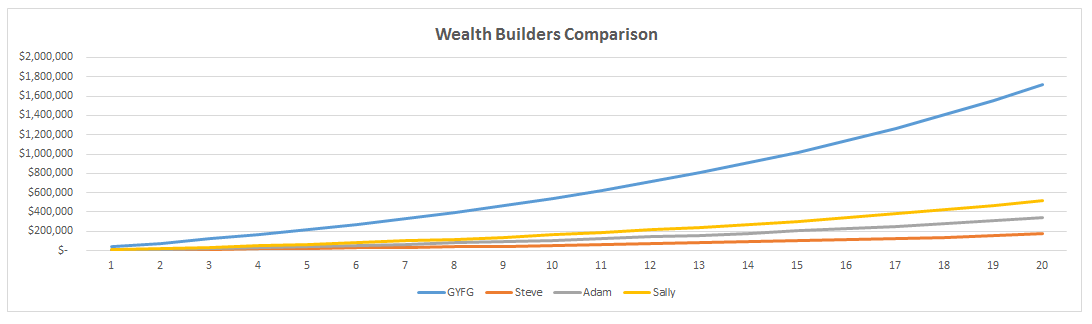

In this scenario, we assume that GYFG earns a compound annual growth rate (CAGR) of ZERO. A 0% CAGR is extremely unlikely, but this really isolates the importance of savings rate by itself. Notice how in all cases, even after earning 0%, GYFG is able to accumulate more wealth than all of the other wealth builders.

Over the 20 year period, GYFG was able to save $750K. In the green highlighted section (table above) I have provided what the returns would need to be in order for the other wealth builders to keep pace with GYFG, given their respective savings rates.

- Steve would need to earn a CAGR of 21%.

- Adam would need to earn a CAGR of 15%.

- Sally would need to earn a CAGR of 11%.

I don’t know anyone who has consistently earned these kinds of returns, outside of the world’s best investors (hello Warren Buffett). Mere mortals like me (and you) should definitely not count on earning those returns.

Let’s take a look and see what happens when GYFG also earns the historical market return of 8% like the other three.

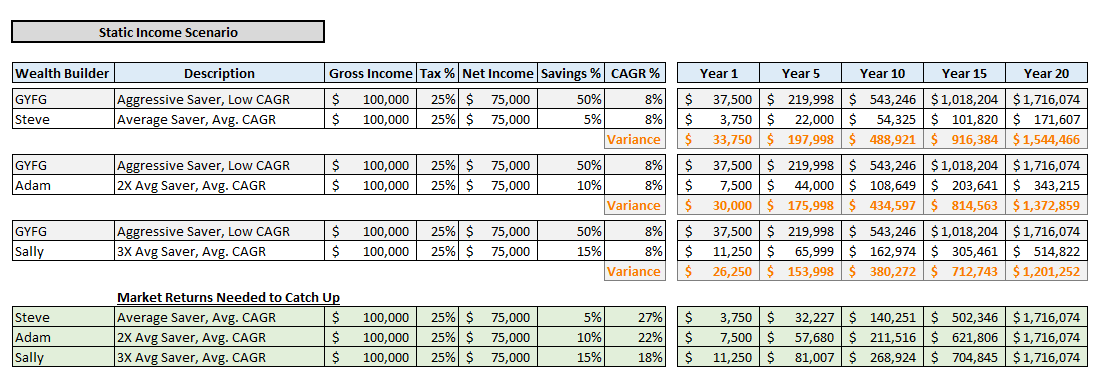

Scenario #2: Static Income for All, and 8% CAGR for All

Here, GYFG earns the historical market return of compound annual growth rate of 8%, like that of his fellow wealth builders. GYFG accumulates MUCH more wealth than all of the other wealth builders. The variance TRIPLES when you combine GYFG’s 50% savings rate with the average market return (compare chart below to one above).

Over the 20 year period, GYFG was able to save $1.7M. In the green highlighted section (table above) I have provided what the returns would need to be in order for the other wealth builders to keep pace with GYFG, given their respective savings rates.

- Steve would need to earn a CAGR of 27%.

- Adam would need to earn a CAGR of 22%.

- Sally would need to earn a CAGR of 18%.

Even less likely. I would not be willing to bet I could earn those kinds of returns, and neither should you. That’s called gambling, not investing, and the house always wins at that game.

Let’s take a look at another scenario, but this time assume that each wealth builder is able to increase their income 10% a year.

Scenario #3: Static Income and 8% CAGR for Super Saver GYFG. 10% Annual Growth in All Wealth Builders’ Income

Note: Although the table below shows the same $100,000 gross income, due to screen real estate, I’m not showing you the year over year growth in income due to the 10% annual increase. Just note that this is the income in Year 1. Then in Year 2, it increases to $110,000 and so on from there. You can see all the detail by downloading the model below.

Holy cow!!! Look at the gap explode when you add a little fuel power in the way of income growth to the mix.

Over the 20 year period, GYFG was able to save $3.9M. What would the returns need to be in order for the other wealth builders to keep pace with GYFG, given their respective savings rates?

- Steve would need to earn a CAGR of 31%.

- Adam would need to earn a CAGR of 25%.

- Sally would need to earn a CAGR of 21%.

These returns are out of reach to 99.99% of the population. I guess they’re possible if you build a business that does really well. But possible is not probable, and I’d classify these as Pie in the Sky returns, nearly impossible.

You may be asking yourself why I threw in the income growth…great question. Behind maximum savings, growth of your income is priority #2 when it comes to wealth building. It will allow you to continue to increase your savings. This is where you need your hustle. You may not start out saving 50% of your income, but as you continue to grow your income you will be able to increase your savings rate, and get there rapidly, as long as you keep your lifestyle inflation under control. By growing his income 10% a year, GYFG was able to build a net worth of $3.9M vs. the $1.7M built with a static income (that’s 2.3X more wealth).

The Big Fat Take Away

A lot of variables will affect your wealth building. But instead of getting overwhelmed by the lot of them, focus on one thing at a time, and make it the most important thing.

In case you missed it…

A HIGH SAVINGS RATE MAKES A HUGE DIFFERENCE IN YOUR ABILITY TO BUILD WEALTH QUICKLY!!!

This is THE most important variable for you to focus on when building your own wealth. The good news is that it is the variable over which you have the most control. In a way, it’s like dieting and exercising to lose weight: it is much easier to cut 100 calories from your daily diet than it is to work off 100 calories. It’s not that exercise is unimportant, but people who are successful losing weight know to leverage their efforts where it counts the most: eating fewer calories. Similarly, it takes infinitely more work (and offers drastically lower probability of success) to chase high returns than it does to simply laser-focus on increasing savings rate!

In case all the prior tables and charts were not enough, I created one last table for you. It simply summarizes the magnitude of the gap between the four wealth builders I presented you with today. It covers the full spectrum from 0% to 8% market returns.

- Against Steve, GYFG is able to accumulate 4.4X to 10.0X more wealth (Steve saves 5% of his income).

- Against Adam, GYFG is able to accumulate 2.2X to 5.0X more wealth (Adam saves 10% of his income).

- And against Sally, GYFG is able to accumulate 1.5X to 3.3X more wealth (Sally saves 15% of her income).

Your compound annual growth rate (CAGR) is the last variable for you to care about when building wealth. It matters, but not as much as you think, not as much as you might read about, and especially not as much as the power of a high savings rate.

LAST TIME, IN RED, LET’S ALL SAY IT TOGETHER NOW: IF YOU WANT TO REACH FINANCIAL FREEDOM IN 20 YEARS OR LESS, FOCUS ON INCREASING YOUR SAVINGS RATE.

Are you convinced? Have you been focusing on the wrong metrics? What is your highest priority in your own approach to wealth building?

– Gen Y Finance Guy

p.s. if you want a copy of the data set you can download it here >> Click Here

p.s.s if you want to see this taken a bit further, go and check out this post from Go Curry Cracker!

38 Responses

I love the breakdown on charts on graphs! I agree that increasing your savings is the one thing you have control over. And it’s also part of the mindset shift that has to happen to get real about financial independence. You have to make a conscious choice to think outside the box and change your financial plan to get you to where YOU want to be rather than what the typical savings rate gets you.

Agreed Maggie, I think the visuals help 🙂

Always be thinking outside the box!

Love this post GYFG!

Savings rate is really the key since there is no control over the returns.

The other thing I also like to focus on is investment fees- as compounding higher fees in mutual funds will erode the value of your portfolio. Maybe you can write a future article on savings though lower fee investments. We are saving a huge portion of our current income now to take advantage of the compounding.

Thanks again for posting!

-Chef

Glad you liked it Chef.

Totally agree on ensuring lower fees. Good idea for a future post. Will add it to the never ending list of AWESOME ideas 🙂

Good on you to start the snowball of compounding to get that exponential momentum going. As you know, time is your best friend when it comes to compounding.

Yup. There is no question that your savings rate is far, far more important than pure income. Like we learned in “The Millionaire Next Door”, truly wealthy people don’t spend a lot of money. People who like to FEEL wealthy tend to spend a lot of money and believe that their *high income level* rationalizes that spending.

We are at right around 70% savings rate.

Very impressive savings rate Steve!

Great Stuff. I love crunching numbers like this to see different scenarios. This was clear and concise and illustrated your point perfectly. I didn’t realize your 50% saving rate was Net. This whole time I thought it was gross. I did a 2016 forecast (thanks again for the idea) and if all goes according to plan I should be right around 53% saving of my net pay (34% gross). Now if I could just get my income to grow by 10% a year…

Hey Mattattack – Glad you found the post clear and that it illustrated my point 🙂

The confusion is probably my fault. I think I originally typed that somewhere or I think I typed something to the effect of “Gross Income (less taxes),” which is just a confusing way of saying “after tax” or “net.” The ultimate goal would be to save 50% of gross income (it will get there eventually). Looking at my 2015 forecast it looks like we will finish 2015 with a net savings rate of 46% and a gross savings rate of 39%.

Then in 2016 it is now looking like we will achieve a 55% net savings rate and a 42% gross savings rate (so its moving in the right direction).

Happy to hear you taking action and creating a forecast of your own. Those are some nice savings rates whether you look at the net or gross.

Get that income growing with a high savings rate and you have a recipe for turbo charged wealth building.

Cheers

Gotta love a mean savings rate. I agree that savings rate is most important, and I try to increase my savings rate by increasing my income. Cutting expenses has a limit, your income doesn’t 🙂

Great depiction & digging the break down of the quote as well! Savings rate is huge and surprisingly once you have that psychological shift it becomes easier to increase. How I challenge myself is that every time I have an increase in income (raise, bonus, small windfall, etc.) I discover ways to not give into lifestyle inflation but increase savings instead! It’s not often you will find people who do this (except in the PF community) but it’s nice to be an encourage if people are open to chatting about it. I find much more fulfillment now upping my savings goals contributions vs. spending more money.

Thanks Alyssa!

It definitely takes a mindset shift. With every raise and bonus, our aim is to get what I call in the day job “operating leverage.” Meaning that our expenses don’t grow at the same pace of income, although we do allow for some lifestyle inflation (i.e spend more money), we continue to inch up the savings rate. 5 years ago we were probably saving about 10% of our income and spending $5,000/month…now we are spending $11,000/month while saving 50% of our income (after tax). So although spending doubled our savings went up 5X (thus operating leverage is realized).

This may be one of the clearest description and break down of how a big savings rate can help you! It is getting clipped to Evernote for sure! Now that we have moved past paying back our student loans we are working to get our savings rate as high as we can. As you stated above, it is all about giving compound interest as much time to work as possible!

Congrats on paying off the student loans Thias! Sounds like a plan for success 🙂

Couldn’t agree more. Sometimes I have a way of overcomplicating things when I am talking to my wife about personal finance. So the other day I mentioned the goal of saving 50% after taxes and spending 50% after taxes. Sometimes less is more and I think a simple goal like this works just as well as all the fancy investments in the world.

Looking back at our first 5 years of wealth accumulation, it really is amazing how little of the growth has come from returns (even in a boom economy). I guess it’s simple math, but more psychological than anything else. The more we all save now, the more we will see the amazing compounding returns once our nests grow over the next few decades. And as we all know, it’s playing the long game.

-Fire Guy

This article could have been shortened to: “Vawt agrees with me, so you know I am right.”

Compounding is great, but saving money early and often makes compounding that much more powerful. I think it is a link worthy post to have skeptical friends read!

Love it!

Need to get a badge made that reads “Vawt Approves this Analysis”

BTW, got my solar installed yesterday. Now just waiting for inspection to get the green light to turn it on.

GYFG, this is a hella analysis! Do you know how much of your Net Worth is due to savings? It’s OK if you don’t, but since you ‘rebaselined’ the components in October, you can keep track of it going forward. The reason I ask if you know the amount, is over the years I have found innumerable ways to look at numbers, but very few of those ways provide actionable information. And the only way I have to measure my performance is to compare the goal to the actual.

Here is my guess, based on your gross income since 2012, your ages, your current NW as of October of $302K, savings rate goals, and percentages for your NW assets. $240K is savings. That’s about 80% (it will certainly decrease each month as your nut grows and the investment appreciation/income increases as you reach a “Critical Mass”). I am refining my “financial cold reads” and all-purpose top-level calculations (as I did with your Income Tax), so I’m interested in how close my estimate is. My goal is to get a stage act and be a “Personal Finance Mentalist” like a combination of Suze Orman and Jon Edward. OK, not really, I just like to guess.

Hey JayCeezy – Glad you liked it sense it was a comment that you left about 3-6 months ago that really got me thinking about savings rate hardcore and how important it was. You may recall gut checking my plan to $10M that calls for about $4M from pure savings/contributions alone. I think you mentioned that your NW was about 42% savings, right?

I have not tracked it all the way back to there…but I did some rough math and I came to about $233K that of NW that is savings, so not to far off 🙂

Speaking of Goal vs. Actual…that is exactly why I put together the $10M road map. It’s funny I will exceed goal I had for the 1st year but it mostly came from huge increases in income that resulted in much larger savings and not mind blowing returns. I will probably end January 2016 with a Net Worth of around $370K vs. a goal of $302K…part of that is the $35K that got added to net worth by adding the cars, but the other $33K is a result of increased savings from higher income.

You have a really good “Financial Sense” 🙂

Cheers!

Thanks, GYFG, that is interesting (the source of your increases). fwiw, my own savings component of NW is 48%, but that is over 30 years with two vicious bear markets, a five-year period of >20% stock market returns, a gradual decline in all interest rates but mortgage going from 11.5% down to 4% over that time, and two boom/bust real estate cycles. Most people overrate their investing acumen and results, I know I did until I started keeping track; it led me to focus on what I could control, which is ‘savings’ as your great article and analysis points out. I wasn’t entirely confident about my conclusion, but Vawt’s confirmation has put my mind at ease.:-)

As for the PF ‘cold reads’, it is an interest of mine (for real), has taken a lot of time-and-trial-and-error to develop (anyone can learn it, but the value of it is questionable). It does come in handy with the few family and friends that occasionally are interested in my second-set-of-eyes. ‘Cold Reads’ in general is also an interest of mine, and the best ever imo is The Amazing Kreskin. He is the epitome of Gladwell’s “Blink” concept, able to size up a person or group instantly. He does it for entertainment, and always reminds his audiences out there that a few unscrupulous people will use the learned skill with bad intention (we see this once in awhile in the world of finance and investing). Here’s a 5-min. clip for anyone interested https://www.youtube.com/watch?v=yD_GcC1ASK4

Couldnt have put it better myself. Concentrating first on the things you can actually change is huge and savings is definitely #1 on that list.

I upped my savings game earlier this year and its really making a big impact on being able to accumulate money and grow my net worth.

Awesome stuff!

It’s Kiyosaki, not Kiyozaki.

Thanks Mysticaltyger for helping catch my mistake. It has since been corrected.

Cheers!

Wow